Accounting Information Systems, 10e 13

Problems

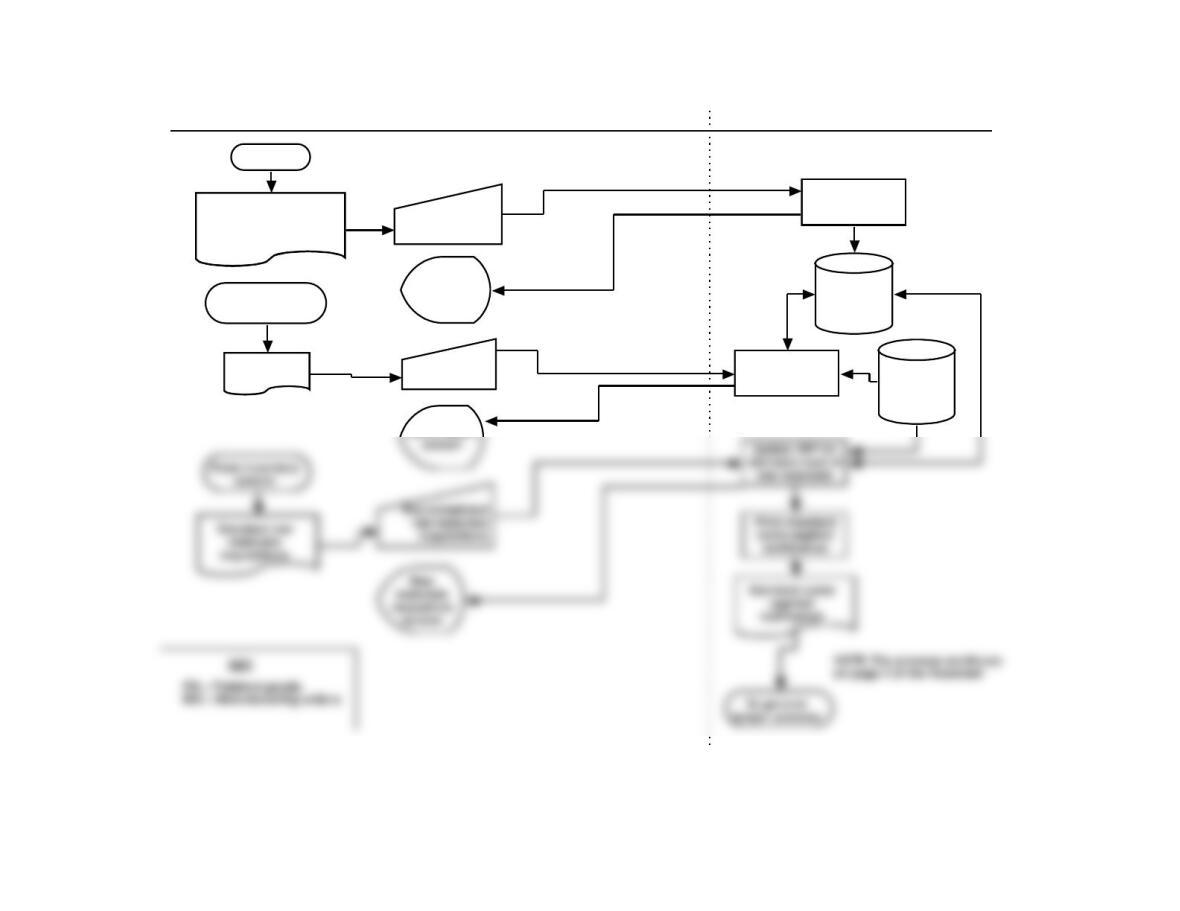

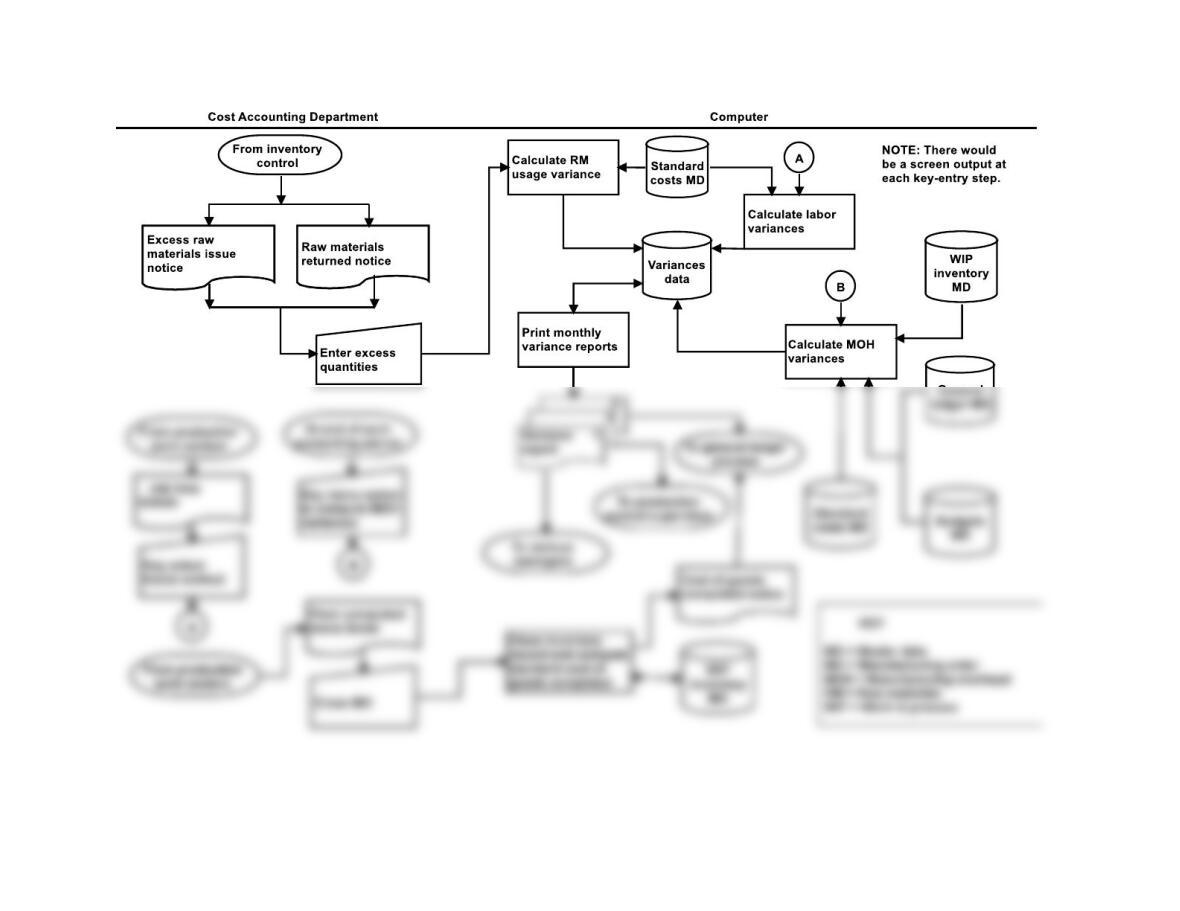

P 15-1 ANS. For solution, see Figure SM-15.6 (Note).

Note: The flowcharts assume the following:

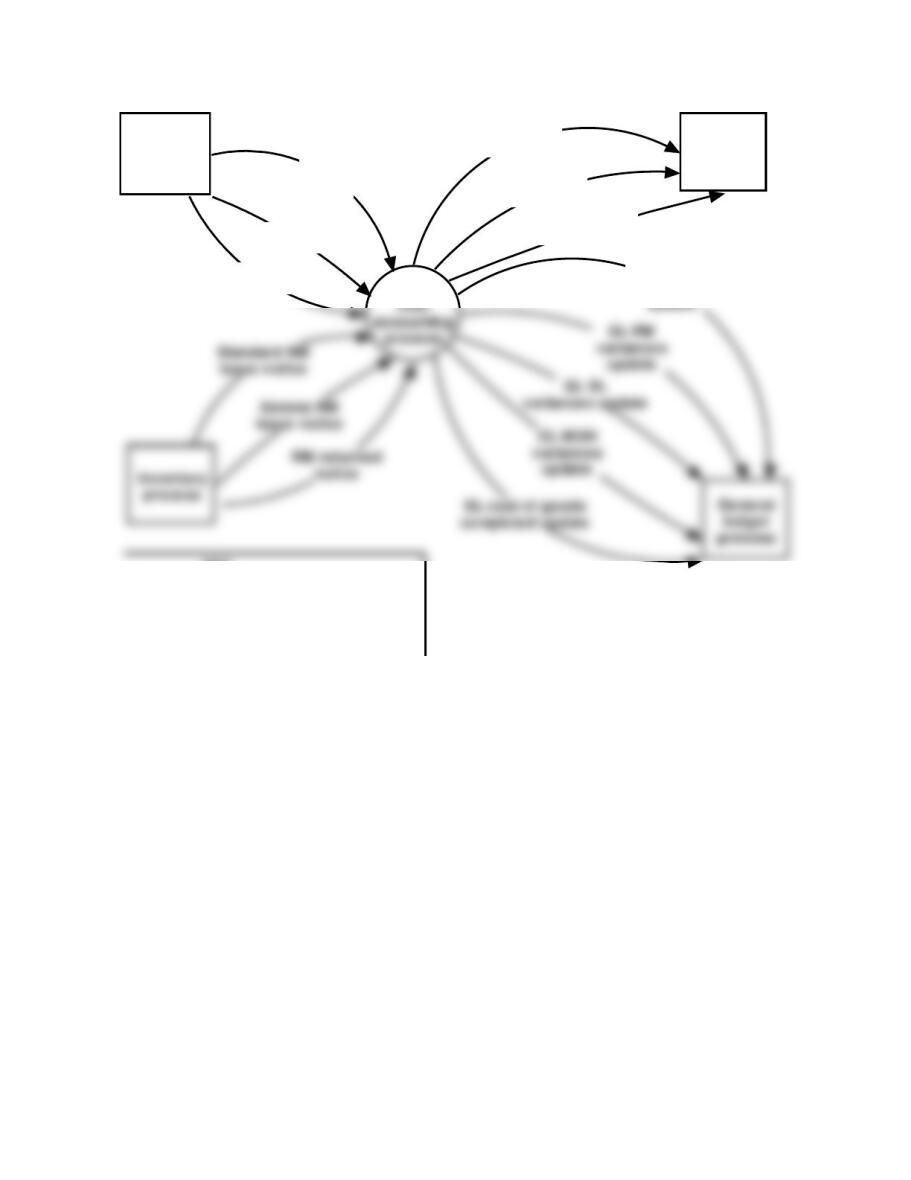

P 15-2 ANS. a. For solution, see Figure SM-15.7.

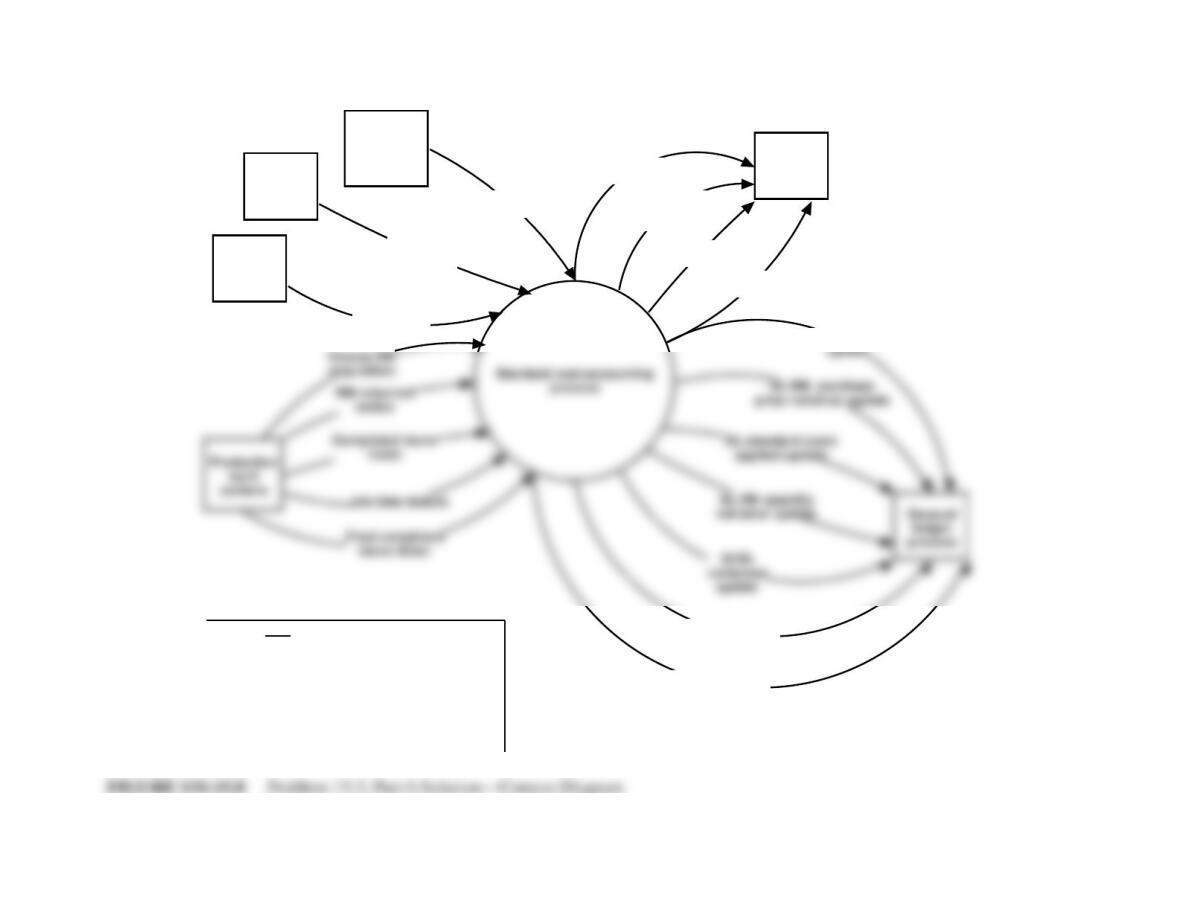

b. For solution, see Figures SM-15.8 and 15.9 (Notes).

P 15-3 ANS. For solution, see Figure SM-15.10. In addition, see the solution to DQ 15-8 for a

description of the differences between Figure 15.7 in Chapter 15 and Figure SM-

15.10.

14 Solutions for Chapter 15

Create WIP

inventory re cord

Create WIP

inventory re cord

Completed

move ticket

Notification of

manufacturing order

released to production

From DCRP

WIP

inventory

Master data

Cost Accounting De partment Computer

Standard

costs

Master data

From production

work centers

Key complete d

move ticket

Update WIP for

standard labor

and overhe ad

WIP

inventory

record

screen

Move ticket

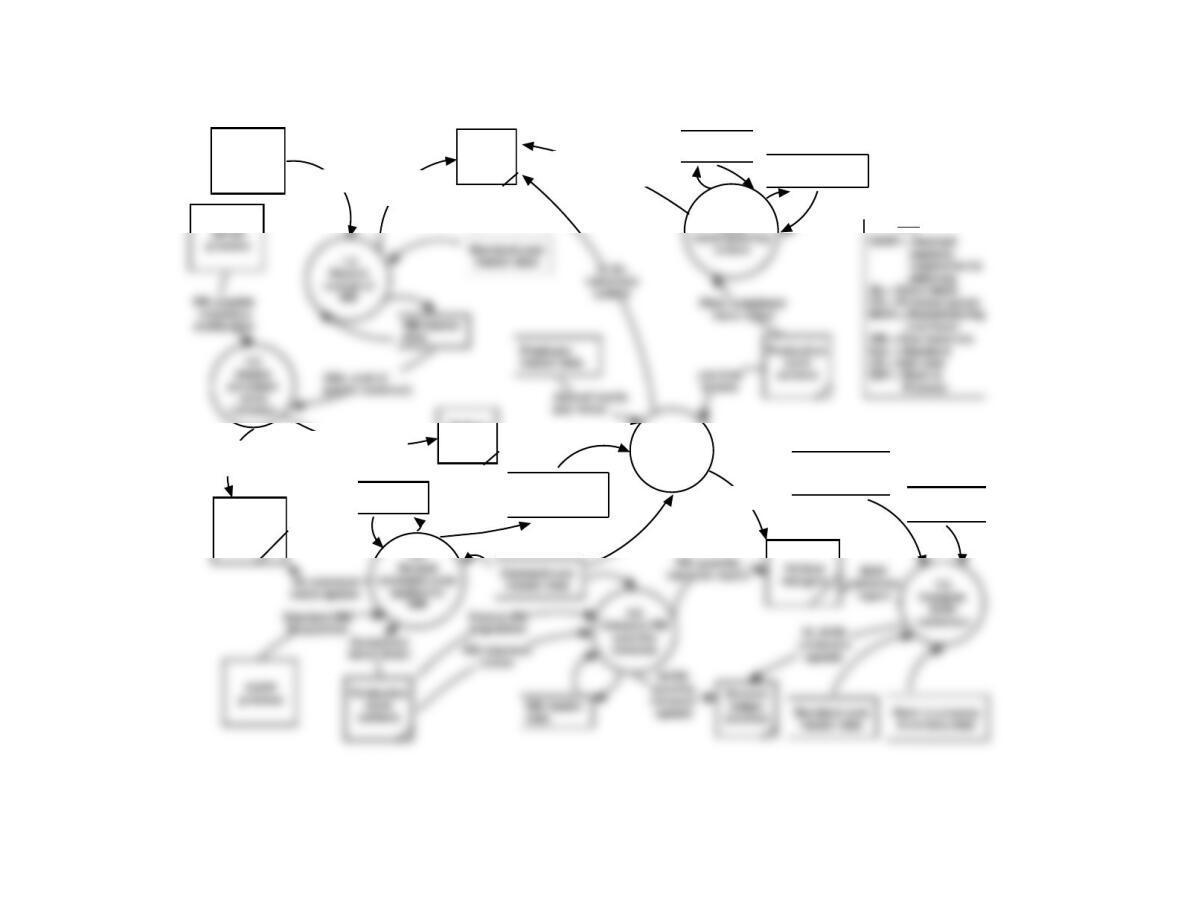

FIGURE SM-15.6 Problem 15-1, Solution Flowchart, Page 1

Accounting Information Systems, 10e 15

FIGURE SM-15.6 Problem 15-1, Solution Flowchart, Page 2

16 Solutions for Chapter 15

Standard

KEY

RM = Raw materials

DL = Direct labor

MOH = Manufacturing overhead

Various

mangers

Production

work

centers

Move

ticket

data

Job time

data

Final move

ticket data

RM variance

report

DL variance

report

MOH variances

report

GL standard

costs applied

FIGURE SM-15.7 Problem 15-2, Part a Solution

Accounting Information Systems, 10e 17

Various

mangers

DCRP

process

Standard RM

requisition

RM purchase price

variance report

RM quantity

variance

report

DL variance s

report

GL RM rece ived

Purchasing

process

RM payable

inventory

notification

RM rece ipt

notification

MOH variance s

report

KEY

DCRP = Detailed capacity re quirements planning

DL = Direct labor

MOH = M anufacturing overhead

RM = Raw materials

GL MOH variance

update

Gl cost of goods

completed update

AP/CD

process

18 Solutions for Chapter 15

RM receipt

notification

GL RM

receive d

update

General

ledger

proce ss

GL RM purchase

price v ariance

update

RM purchase price

variance re port

RM master

data

5.0

Compute DL

variance s

DL variance

report

6.0

Close

GL cost of goods

complete d update

(de bit FG, credit WIP)

FG maste r

data

Budgets

master data

General ledger

master data

KEY

General

ledger

proce ss

Work in process

inventory

Work in process

inventory data

Various

managers

Purchasing

proce ss

FIGURE SM-15.9 Problem 15-2, Part b Solution—Level 0 DFD

Accounting Information Systems, 10e 19

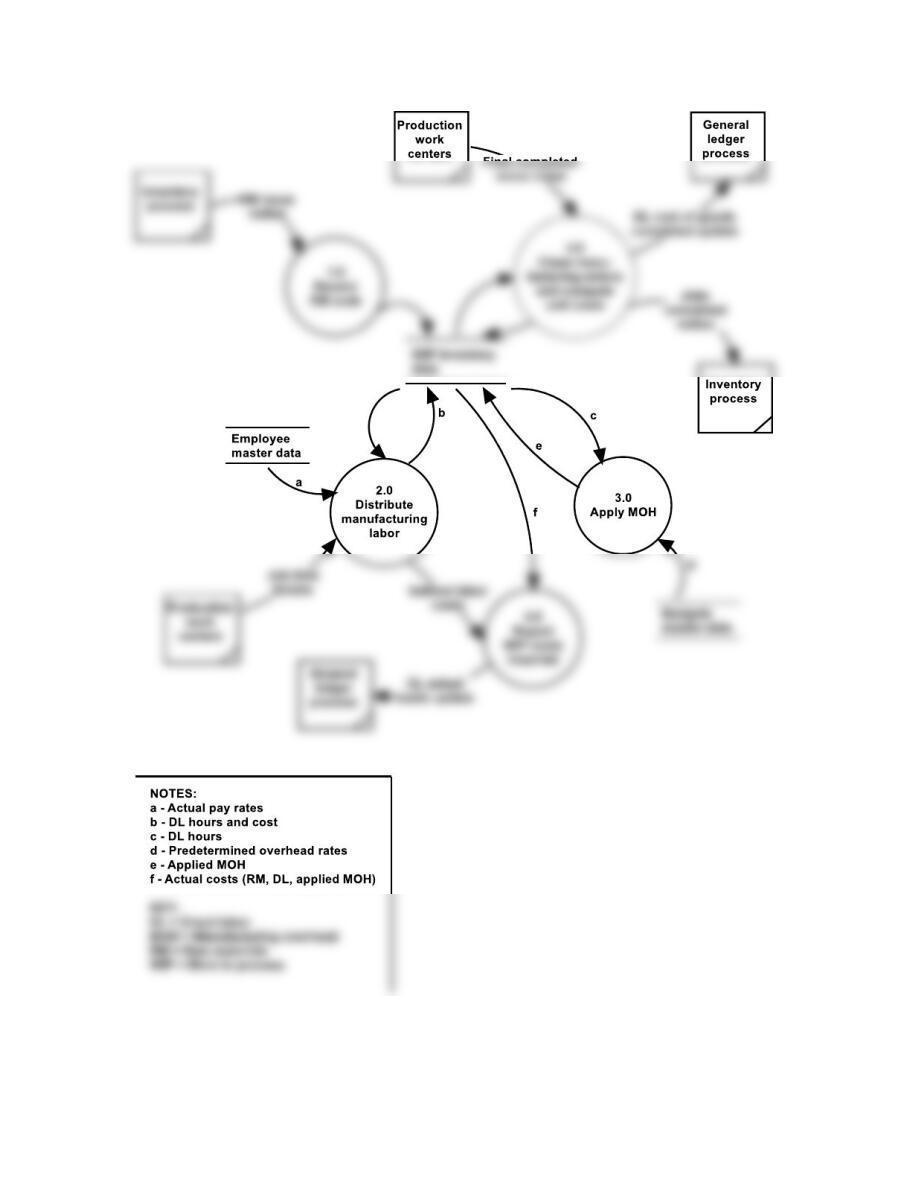

FIGURE SM-15.10 Problem 15-3 Solution

20 Solutions for Chapter 15

P 15-4 a. ANS. The following assumptions were made in solving part a:

1. All variances are unfavorable (i.e., actual costs exceed standard), resulting in

debits to the variance accounts. If, on the other hand, actual costs were less

than standard costs, the variances would be favorable and would be recorded

by credits to the variance accounts.

Debit Credit

1. GL standard costs applied update:

a. WIP inventory (SQ*SP)

RM inventory (SQ*SP)

b. WIP inventory (SH*SR)

Payroll clearing account (SH*SR)

c. WIP inventory (SQ*SR)

MOH control account (SQ*SR)

4. GL MOH variances update: (see the preceding Notes 1 and 2)

MOH budget variance (Note D)

MOH capacity (volume) variance (Note E)

MOH control account XXXX

5. GL cost of goods completed update:

Accounting Information Systems, 10e 21

Notes:

A – (AQ-SQ)*SP.

B – (AR-SR)*AH.

C – (AH-SH)*SR.

Key:

DL = Direct labor MOH = Manufacturing overhead

RM = Raw materials WIP = Work in process

AR = Actual pay rate per hour SR = Standard pay rate per hour

b. ANS. In addition to the following solution, see the assumptions in part a previously and

the Key in the solution to part a.

1. The following entry would be made to record the purchase of RM:

Debit Credit

2. The following pair of entries would be made to record the sale of goods and related cost of

goods sold:

22 Solutions for Chapter 15

3. Annually, the variance accounts would be closed to cost of goods sold (Note 3) through the

following entry:

Debit Credit

Cost of goods sold XXXX

P 15-5 ANS. The analysis should be structured to address the three areas of concern:

effectiveness of operations, efficiency of operations, and resource security

objectives. First, recognize that effectiveness will be hampered by increased risk

of stock-outs, a limited capability to work in a just-in-time environment, and the

P 15-6 ANS. a. The main concepts conveyed by lean manufacturing include the following:

• Perfect first-time quality

• Waste minimization

Accounting Information Systems, 10e 23

in the modern IPP.

b. Many of these publications argue that traditional cost accounting reports were

developed to present an accurate view of the company to outsiders and

weren’t designed to help managers run their operations better. Well-designed

accounting systems should mitigate that concern. There are many conceptual

parallels between the current trends in cost accounting and lean accounting:

• Both advocate categorizing costs in a cellular fashion. Lean accounting

principles further recommend that companies organize them by value

P 15-7 ANS. The answers to this problem will vary widely based on the companies selected.

We anticipate the student solutions to include many factors, but at some level,

their discussion should include some of the key characteristics of successful

global companies identified early in the chapter. These include the following:

• Improved internal business processes in the areas of customers,

P 15-8 ANS. The answer will vary based on the company selected, although each student

should address the points provided in the text of the question.

P 15-9 ANS. Solutions will vary according to the tables selected. However, the following

guidelines should be helpful for grading the solutions:

1. From the file, ensure that the tables are linked in relationships with cardinalities. See the

solution to SP 15-4 for an example of the E-R diagram needed for this problem.

24 Solutions for Chapter 15