CHAPTER 15

Managerial Accounting

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

*1. Identify the features of

managerial accounting and

the functions of

management.

1, 2, 3, 4, 5,

6, 7, 8

1, 2

1

1

*2. Describe the classes of

manufacturing costs and the

9, 11, 12, 13,

2

and prepare financial

manufacturer.

18, 19, 20, 21

accounting.

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Classify manufacturing costs into different categories and

compute the unit cost.

Simple

20–30

2A

Classify manufacturing costs into different categories and

compute the unit cost.

Simple

an income statement, and a partial balance sheet.

income statement, and a partial balance sheet.

correct income statement.

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

* 1. Identify the features of managerial

accounting and the functions of

management.

Q15-1

Q15-2

Q15-3

Q15-4

Q15-5

Q15-6

Q15-7

Q15-8

BE15-1

BE15-2

DI15-1

E15-1

* 3. Demonstrate how to compute cost of

goods manufactured and prepare

financial statements for a

manufacturer.

Q15–19

Q15–10

Q15–20

Q15–21

E15–15

Q15–15

Q15–16

Q15–17

Q15–18

BE15-7

BE15-8

BE15-9

BE15-10

DI15-3

E15-8

E15-9

E15–12

E15–13

E15–14

E15–16

E15–17

P15–4A

E15–10

E15–11

P15–3A

P15–5A

Q15-24

DI15-4

E15–18

CD15

BYP15–3

BYP15-4

BYP15-7

BE15-4

BE15-5

ANSWERS TO QUESTIONS

1. (a) Disagree. Managerial accounting is a field of accounting that provides economic and financial

information for managers and other internal users.

(b) Joe is incorrect. Managerial accounting applies to all types of businesses—service, merchandising,

and manufacturing.

3. Differences in the content of the reports are as follows:

Financial

Managerial

• Pertains to business as a whole and is highly

• Pertains to subunits of the business and

4. Linda should know that the management of an organization performs three broad functions:

(1) Planning requires management to look ahead and to establish objectives.

(2) Directing involves coordinating the diverse activities and human resources of a company to

produce a smooth-running operation.

(3) Controlling is the process of keeping the company’s activities on track.

Questions Chapter 15 (Continued)j

7. The differences between income statements are in the computation of the cost of goods sold as

follows:

8. The difference in balance sheets pertains to the presentation of inventories in the current asset

section. In a merchandising company, only merchandise inventory is shown. In a manufacturing

company, three inventory accounts are shown: finished goods, work in process, and raw materials.

9. Manufacturing costs are classified as either direct materials, direct labor, or manufacturing overhead.

12. A merchandising company has beginning merchandise inventory, cost of goods purchased, and

ending merchandise inventory. A manufacturing company has beginning finished goods inventory,

cost of goods manufactured, and ending finished goods inventory.

13. (a) X = total cost of work in process.

(b) X = cost of goods manufactured.

15. Direct materials used ………………………………………………………………………………… $240,000

Direct labor used ……………………………………………………………………………………… 220,000

Total manufacturing overhead ……………………………………………………………………. 180,000

Total manufacturing costs ………………………………………………………………….. $640,000

Questions Chapter 15 (Continued)

20. The value chain refers to all activities associated with providing a product or service. For a manufac–

turer, these include research and development, product design, acquisition of raw materials, production,

sales and marketing, delivery, customer relations, and subsequent service.

22. In a just-in-time inventory system, the company has no extra inventory stored. Consequently, if

some units that are produced are defective, the company will not have enough units to deliver to

customers.

23. The balanced scorecard is called “balanced” because it strives to not over emphasize any one

performance measure, but rather uses both financial and non-financial measures to evaluate all

aspects of a company’s operations in an integrated fashion.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 15-1

Financial Accounting

Managerial Accounting

BRIEF EXERCISE 15-2

BRIEF EXERCISE 15-3

BRIEF EXERCISE 15-4

BRIEF EXERCISE 15-5

BRIEF EXERCISE 15-6

Product Costs

BRIEF EXERCISE 15-7

BRIEF EXERCISE 15-8

ROLAND COMPANY

Balance Sheet

December 31, 2017

BRIEF EXERCISE 15-9

Direct

Materials Used

Direct

Labor Used

Factory

Overhead

Total

Manufacturing

Costs

BRIEF EXERCISE 15-10

Total

Manufacturing

Costs

Work in

Process

(January 1)

Work in

Process

(December 31)

Cost of Goods

Manufactured

BRIEF EXERCISE 15–11

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 15-1

DO IT! 15-2

DO IT! 15-3

TOMLIN COMPANY

Cost of Goods Manufactured Schedule

For the Month Ended April 30

DO IT! 15-4

SOLUTIONS TO EXERCISES

EXERCISE 15-1

EXERCISE 15-2

EXERCISE 15-3

EXERCISE 15-4

EXERCISE 15-5

EXERCISE 15-6

EXERCISE 15-7

EXERCISE 15-8

EXERCISE 15-9

EXERCISE 15-9 (Continued)

EXERCISE 15–10

Additional explanation to EXERCISE 15-10 solution:

EXERCISE 15-10 (Continued)

Case B

Case C

EXERCISE 15–11

(b) HORIZON COMPANY

Cost of Goods Manufactured Schedule

For the Year Ended December 31, 2017

EXERCISE 15–12

(a) CEPEDA CORPORATION

Cost of Goods Manufactured Schedule

For the Month Ended June 30, 2017

(b) CEPEDA CORPORATION

Income Statement (Partial)

For the Month Ended June 30, 2017

EXERCISE 15–13

(a) WASHINGTON CONSULTING

Schedule of Cost of Contract Services Performed

For the Month Ended August 31, 2017

EXERCISE 15–14

EXERCISE 15-14 (Continued)

AIKMAN COMPANY

Income Statement (Partial)

For the Year Ended December 31, 2017

AIKMAN COMPANY

(Partial) Balance Sheet

December 31, 2017

EXERCISE 15–15

EXERCISE 15–16

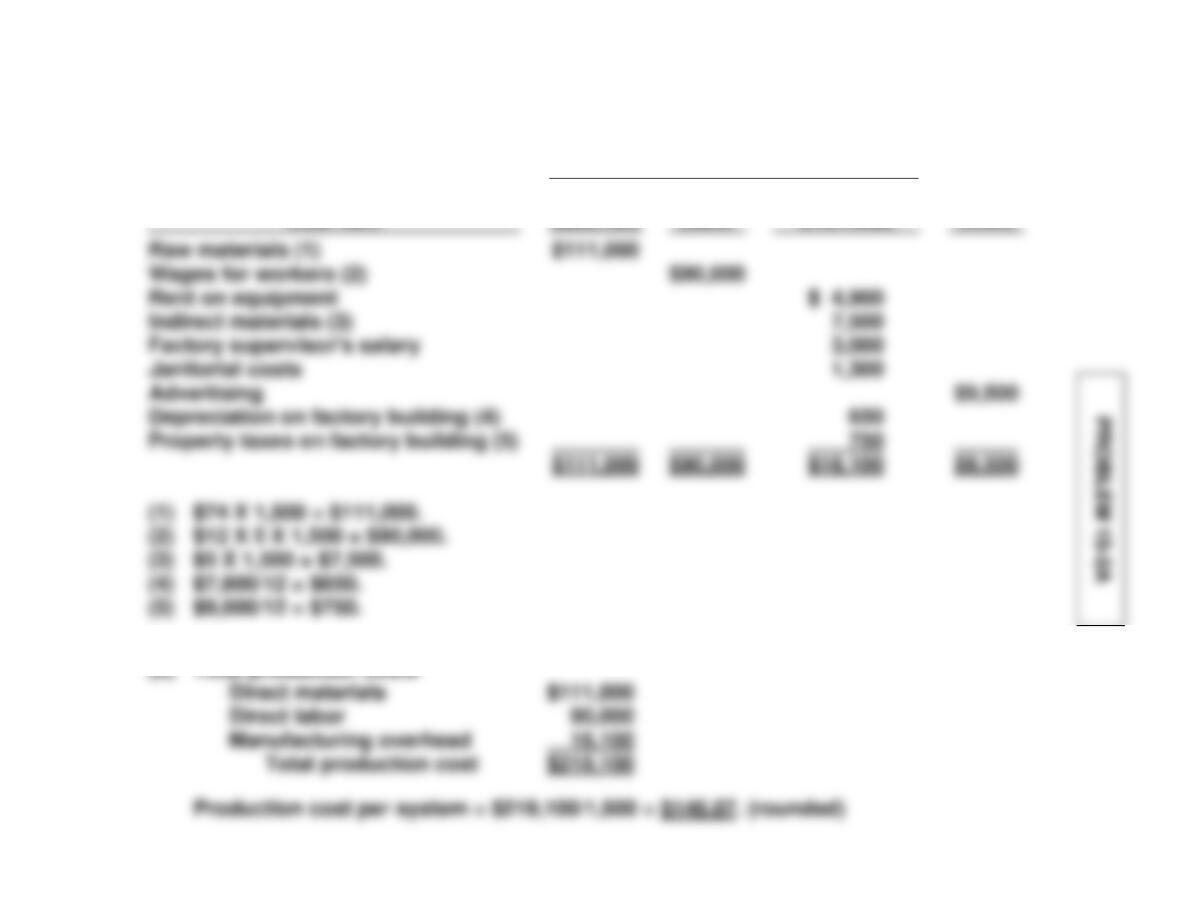

(a) ROBERTS COMPANY

Cost of Goods Manufactured Schedule

For the Month Ended June 30, 2017

(b) ROBERTS COMPANY

(Partial) Balance Sheet

June 30, 2017

EXERCISE 15–17

(b) To: Chief Accountant

From: Student

Subject: Statement Presentation of Accounts

EXERCISE 15–18

(a)

Product Costs

Cost Item

Direct

Materials

Direct

Labor

Manufacturing

Overhead

Period

Costs

(b) Total production costs

$90,000

(a)

Product Costs

Cost Item

Direct

Materials

Direct

Labor

Manufacturing

Overhead

Period

Costs

PROBLEM 15–3A

(a) Case 1

Case 2

PROBLEM 15-3A (Continued)

(b) CASE 1

Cost of Goods Manufactured Schedule

(c) CASE 1

Income Statement

CASE 1

(Partial) Balance Sheet

PROBLEM 15–4A

(a) CLARKSON COMPANY

Cost of Goods Manufactured Schedule

For the Year Ended June 30, 2017

PROBLEM 15-4A (Continued)

(b) CLARKSON COMPANY

(Partial) Income Statement

For the Year Ended June 30, 2017

(c) CLARKSON COMPANY

(Partial) Balance Sheet

June 30, 2017

PROBLEM 15–5A

(a) EMPIRE COMPANY

Cost of Goods Manufactured Schedule

For the Month Ended October 31, 2017

PROBLEM 15-5A (Continued)

(b) EMPIRE COMPANY

Income Statement

For the Month Ended October 31, 2017

CURRENT DESIGNS

CD15

The answers to parts (a) and (b) may vary from student to student.

(a) What are the primary information needs of each manager?

CD15 (Continued)

(b) Name one special-purpose management accounting report that could

be designed for each manager. Include the name of the report, the

information it would contain, and how frequently it should be issued.

Manager

Name of

report

Information report

would contain

How frequently

should it be

issued?

analysis

Bill Johnson

Sales by product

Monthly or

weekly

overhead costs

Report for

labor costs for the

CD15 (Continued)

(c) When Diane Buswell, controller for Current Designs, reviewed the

accounting records for a recent period, she noted the following items.

Classify each item as a product cost or a period cost. If a cost is a

product cost, note if it is a direct materials, direct labor, or manufactur–

ing overhead item.

Payee

Purpose

Product Costs

Period

Costs

Direct

Materials

Direct

Labor

Manufacturing

Overhead

X

BYP 15-1 DECISION-MAKING ACROSS THE ORGANIZATION

BYP 15-2 MANAGERIAL ANALYSIS

Since the questions were fairly open-ended, the following are only sug-

gested results. The class may be able to think of others, or of more items

for each one.

BYP 15-3 REAL-WORLD FOCUS

BYP 15-4 COMMUNICATION ACTIVITY

Ms. Shelly Phillips

President

Phillips Company

Dear Shelly:

BYP 15-4 (Continued)

BYP 15-5 ETHICS CASE

BYP 15-6 ALL ABOUT YOU

Student responses will vary. We have provided some basic examples that

may represent common responses.

BYP 15-7 CONSIDERING YOUR COSTS AND BENEFITS