Accounting Information Systems, 10e 1

SOLUTIONS FOR CHAPTER 15

Each end-of-chapter question in the Solutions Manual is tagged to correspond with AACSB, AICPA

and CISA standards, allowing professors to more easily manage the task of reporting outcomes to these

professional and accrediting bodies. Please see the corresponding spreadsheet file for the tagging

information.

Discussion Questions

DQ 15-1 This chapter discusses the complexities of competing in a highly competitive

global manufacturing environment. Discuss how enterprise systems can help an

organization streamline its processes and become more competitive.

ANS. The following factors were discussed in the chapter:

This answer should probably begin with a discussion of the issues facing

manufacturers in the global economy. Based on the Deloitte & Touche survey

discussed in the text, manufacturing organizations are under pressures to do the

following:

2 Solutions for Chapter 15

Enterprise systems specifically help out in the four key areas discussed as

important for achieving the three goals as follows:

• Product innovation: Enterprise systems ensure that changes made in

engineering can be automatically incorporated into production, decreasing the

time to market for new innovations. Product life-cycle management further

You may also consider structuring this discussion around how technology relates

to the ten global drivers of manufacturing competitiveness discussed in this

chapter.

DQ 15-2 What industry do you believe is a leader in enterprise systems implementations?

Discuss what you think are the major contributing reasons for that leadership.

ANS. One possible answer to the question is the automotive industry, where

manufacturers produce very complex products using highly automated processes.

DQ 15-3 Table 15.1 presents a summary of trends in cost management and cost accounting

that have occurred during the past two decades.

a. Which trends do you consider most significant? Explain your answer.

Accounting Information Systems, 10e 3

ANS. As discussed in the chapter text, the move toward more accurate and detailed cost

information that cuts across the value chain and across the life of the product

presents a significant trend toward focusing on the use of cost information to

• Some cost trends that might fly in the face of what has been learned in

traditional cost accounting classes include the following:

o Shift from direct labor to some other basis for charging overhead.

Although direct labor is becoming a less important cost component,

many firms cling to direct labor as a method for applying overhead.

Automation costs (a fixed cost) or time spent in a production step are

often cited as more meaningful bases for allocating overhead.

o Shift away from standard costs to actual costs.

o Shift away from job order to process costing.

ANS. Other than the relationships shown in Table 15.1, the following relationships

might be described:

4 Solutions for Chapter 15

DQ 15-4 “A company cannot implement manufacturing resource planning (MRP) without

making a heavy investment in computer resources.” Do you agree? Discuss fully.

ANS. Agreed. MRP’s three main components⎯material requirements planning,

capacity requirements planning, and cash flow planning⎯all involve complex

computations and manipulation of large amounts of data and large files. These

DQ 15-5 “A company cannot implement a flexible manufacturing process (FMS) without

making a heavy investment in computer resources.” Do you agree? Discuss fully.

ANS. Agreed. An examination of Figure 15.1 should reveal that most of the flexible

DQ 15-6 “A company cannot implement a just-in-time (JIT) process without making a

heavy investment in computer resources.” Do you agree? Discuss fully.

Accounting Information Systems, 10e 5

ANS. Overall, we don’t agree. JIT processes generally do not require sophisticated

computer resources. In fact, some JIT processes are implemented using the

kanban card as the medium for routing production orders and collecting data. This

DQ 15-7 In addition to the industries mentioned in Technology Summary 15.2, find two

industries currently using 3D printing either for prototyping or manufacturing.

A partial list includes jewelry, footwear, industrial design, architecture, engineering and

construction (AEC), automotive, dental and medical industries, education, geographic

information systems, and civil engineering. There are undoubtedly many others.

DQ 15-8 A main goal of just-in-time JIT is zero inventories.

a. Assume your company does not aspire to JIT and has $3,000,000 in raw

materials in stock. Identify costs that may be incurred to maintain the

inventory level.

ANS. a. The cost of carrying inventory may include incremental taxes, insurance,

spoilage, warehouse space, security, labor to move and maintain, and so on.

DQ 15-9 Without redrawing the figure, discuss the changes that would occur in Figure15.7

if the company used an actual costing process instead of a standard cost process.

6 Solutions for Chapter 15

ANS. Note: Although the question specifically states that Figure 15.7 is not to be

redrawn, your understanding of the following solution will be improved if you

review it in conjunction with the solution to P 15-3, which shows the redrawn

Figure 15.7.

Changes in process outputs:

• In the absence of a standard cost process, there would be no variance

reports to managers or variance updates to the general ledger process.

• A data flow called “GL actual costs update” would replace the flow “GL

standard cost update.”

Changes in process data:

• The standard cost master data and general ledger master data would not

appear in the process.

• The other three files would continue, but two of them would change as

follows:

Accounting Information Systems, 10e 7

DQ 15-10 Discuss how the inventory process supports the production planning process and

the risks to the production process if inventory process control goals are not

achieved. Do not limit your discussion to losses from fraud.

ANS. As organizations struggle to remain competitive in a global manufacturing

environment and to enhance their effectiveness and efficiency, inventory control

becomes critical. If inventory levels are too high, an organization risks being left

DQ 15-11 With the convergence of U.S. GAAP and IFRS standards moving forward, there is

the possibility of the elimination of the LIFO inventory valuation method. If this

happens, what will be the impact on manufacturing operations?

ANS. LIFO is a costing/valuation method and is related to cost flow, not physical flow

8 Solutions for Chapter 15

Short Problems (shown using diagramming software,

such as MS Visio)

1.1

Determine

Product

Description

Parts master

data

1.3

Determine

Product

Routing

Product Design

New parts needs

Bill of M aterials

Master

Product

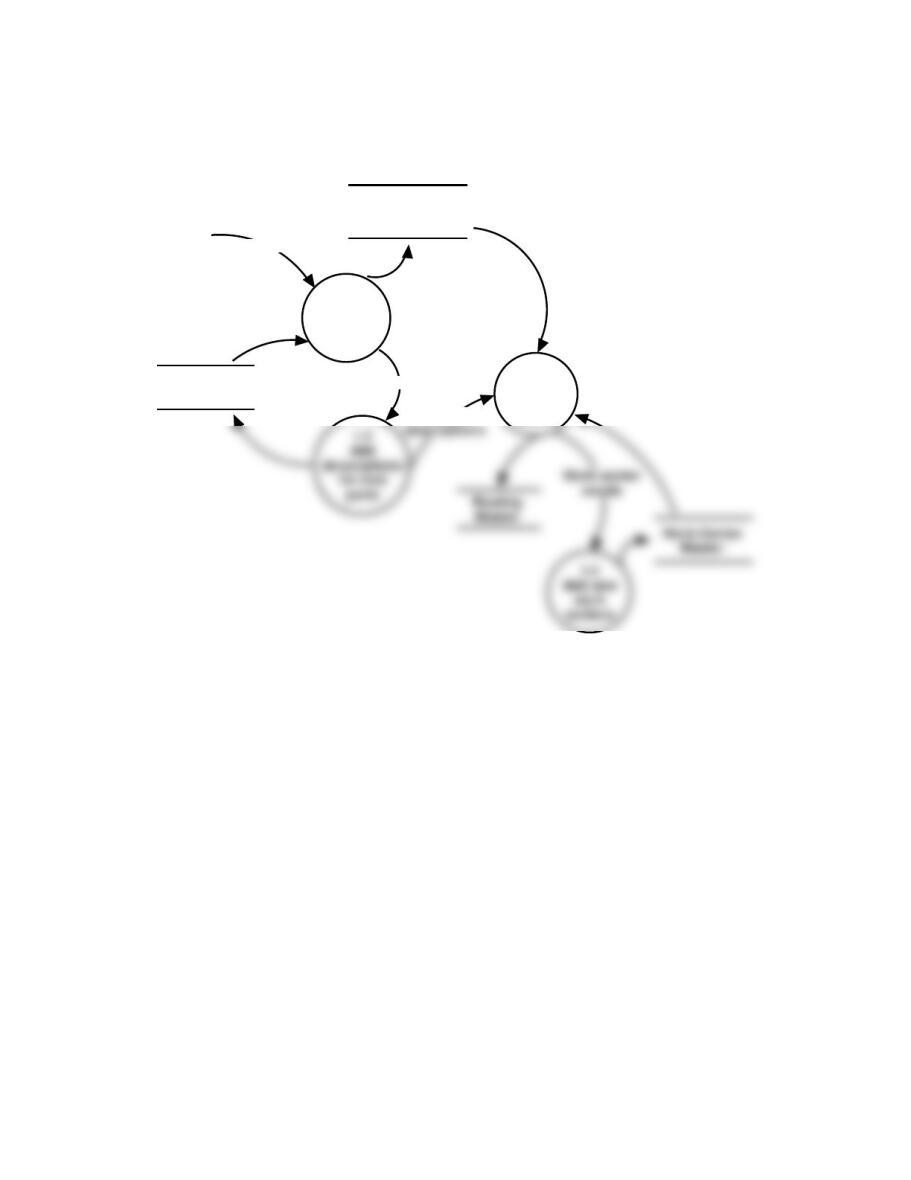

FIGURE SM-15.1 Short Problem 15-1 Solution

Accounting Information Systems, 10e 9

3.1

Explode

Bills of

Materials

3.2

Develop

Time–phased

order

requirements

Bill of materials

master

Materials

Needs

Master

production

schedule Time–phased

order requirements

schedule

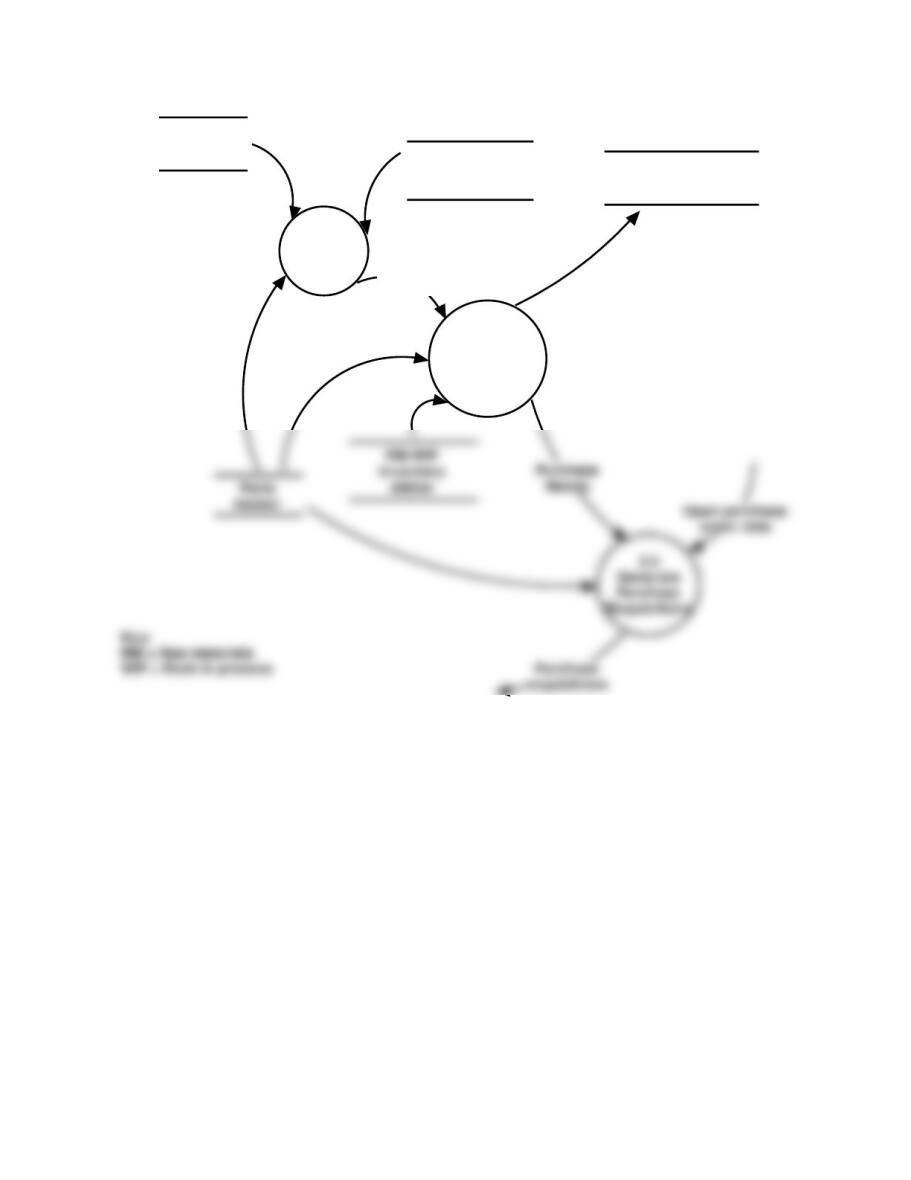

FIGURE SM-15.2 Short Problem 15-2 Solution

10 Solutions for Chapter 15

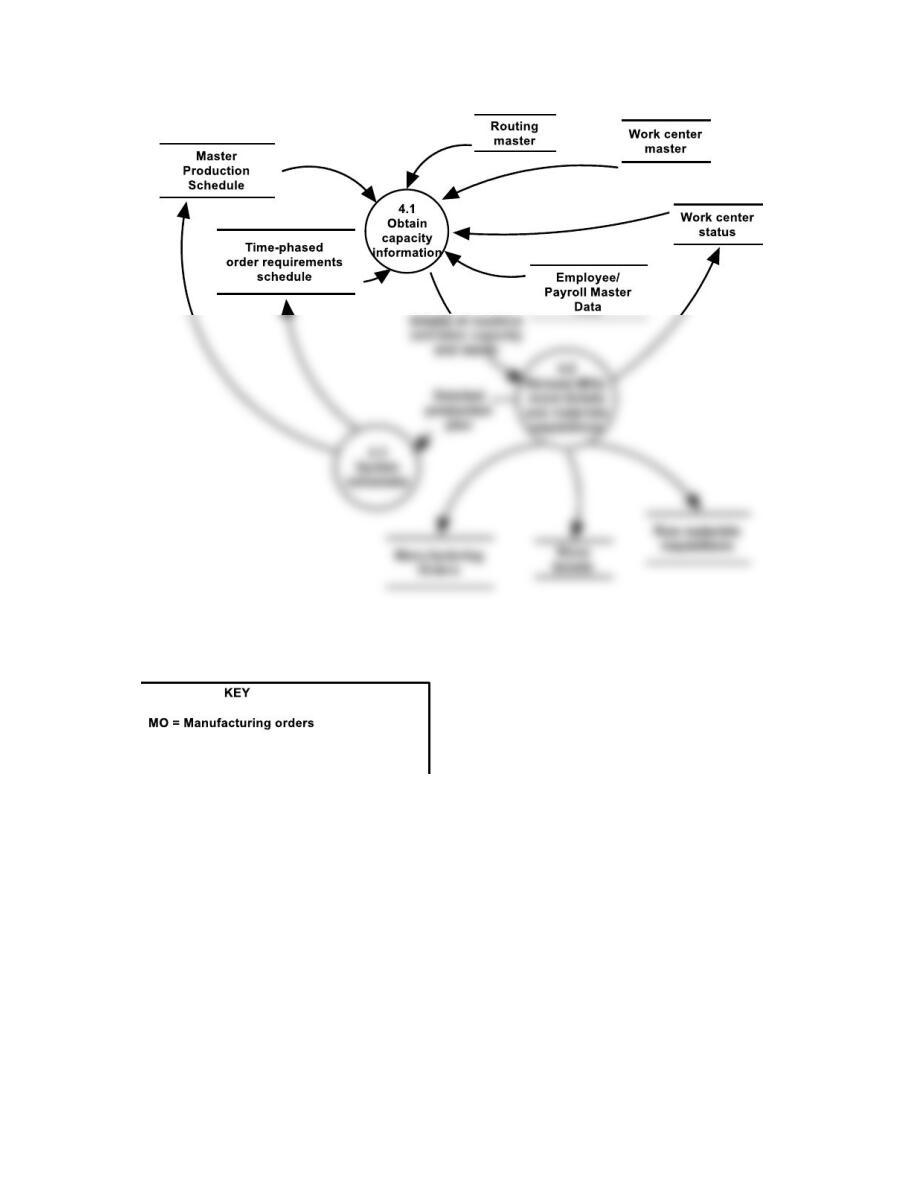

FIGURE SM-15.3 Short Problem 15-3 Solution

Accounting Information Systems, 10e 11

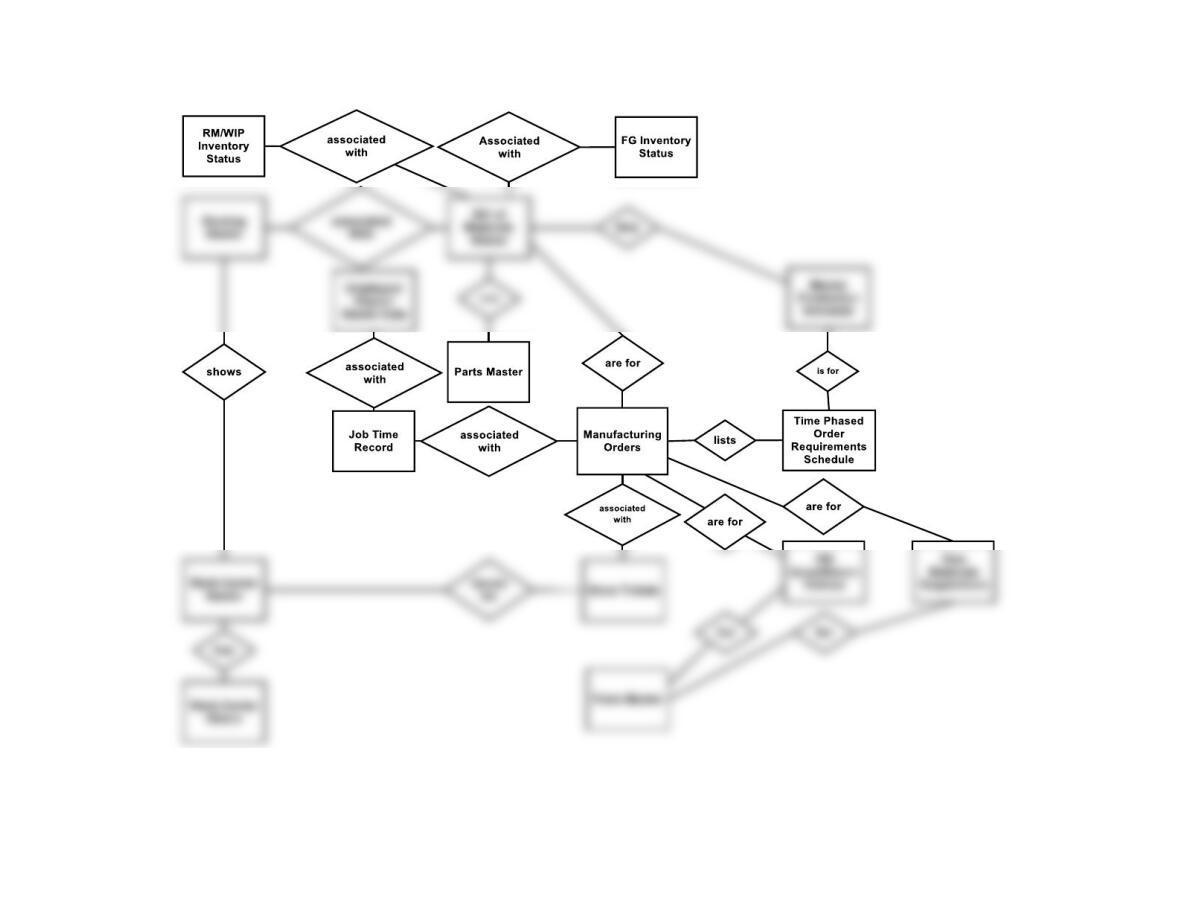

FIGURE SM-15.4 Short Problem 15-4 Solution

12 Solutions for Chapter 15

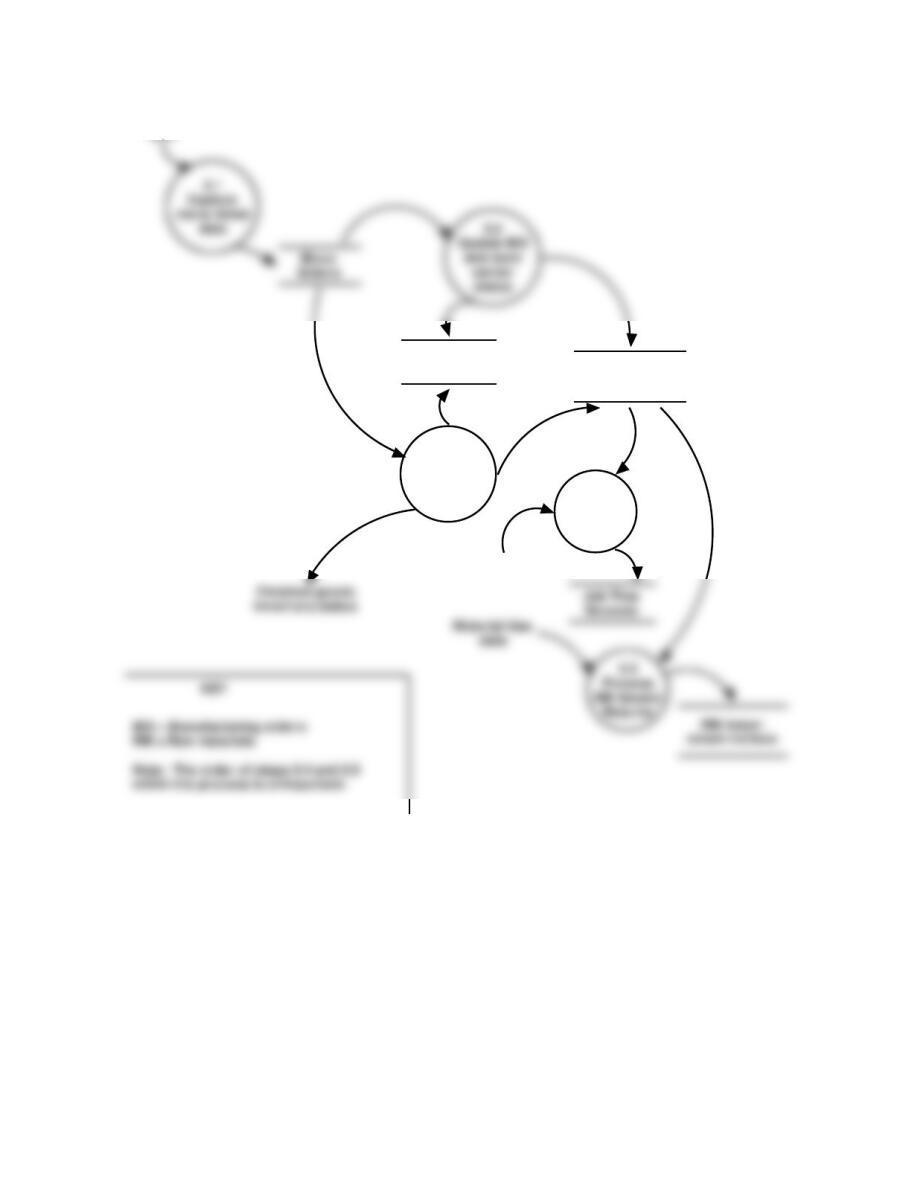

Manufacturing

Orders

Work center

status

5.3

Update work

center

status and

close MO

5.4

Process

Employee

Time

Work progre ss

data

Labor Time

FIGURE SM-15.5 Short Problem 15-5 Solution