241

WHAT’S NEW IN THE SIXTH EDITION:

There are no major changes in this chapter.

LEARNING OBJECTIVES:

By the end of this chapter, students should understand:

➢ what characteristics make a market competitive.

CONTEXT AND PURPOSE:

Chapter 14 is the second chapter in a five-chapter sequence dealing with firm behavior and the

organization of industry. Chapter 13 developed the cost curves on which firm behavior is based. These

KEY POINTS:

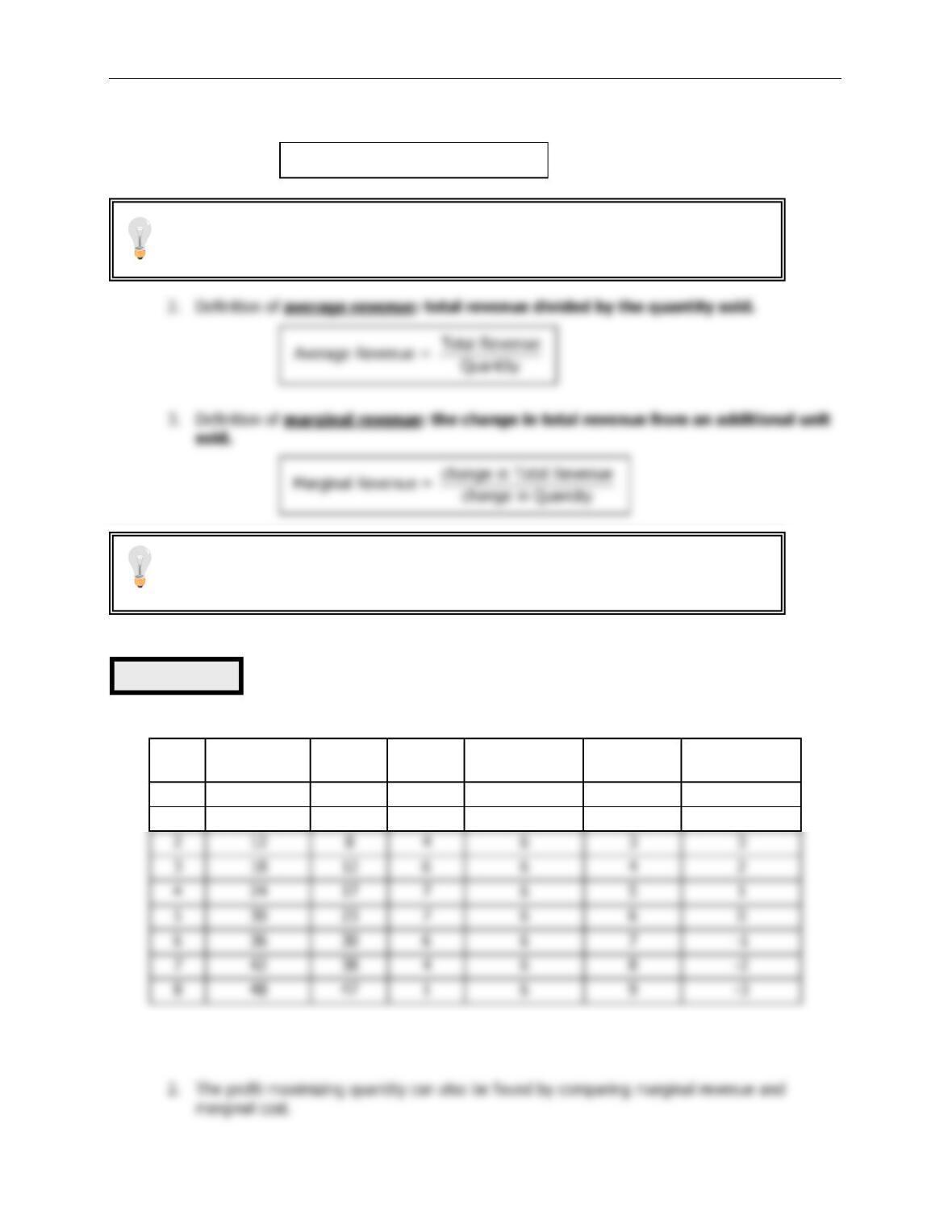

• Because a competitive firm is a price taker, its revenue is proportional to the amount of output it

produces. The price of the good equals both the firm’s average revenue and its marginal revenue.

FIRMS IN

COMPETITIVE MARKETS

14

242 ❖ Chapter 14/Firms in Competitive Markets

• In the short run when a firm cannot recover its fixed costs, the firm will choose to shut down

temporarily if the price of the good is less than average variable cost. In the long run, when the firm

can recover both fixed and variable costs, it will choose to exit if the price is less than average total

cost.

CHAPTER OUTLINE:

I. What Is a Competitive Market?

A. The Meaning of Competition

1. Definition of competitive market: a market with many buyers and sellers trading

identical products so that each buyer and seller is a price taker.

2. There are three characteristics of a competitive market (sometimes called a perfectly

competitive market).

a. There are many buyers and sellers.

B. The Revenue of a Competitive Firm

Table 1

To help students understand price-taking behavior, use the example of common

stock. Have your students assume that they inherited 100 shares of stock in a well–

Chapter 14/Firms in Competitive Markets ❖ 243

1. Total revenue from the sale of output is equal to price times quantity.

II. Profit Maximization and the Competitive Firm’s Supply Curve

A. A Simple Example of Profit Maximization: The Vaca Family Dairy Farm

Q

Total

Revenue

Total

Cost

Profit

Marginal

Revenue

Marginal

Cost

Change in

Profit

0

$0

$3

$-3

—-

—-

—-

1

6

5

1

$6

$2

$4

2

12

3

18

12

4

24

17

5

30

23

6

36

30

7

4

8

48

47

1. In this example, profit is maximized if the farm produces four or five gallons of milk (see the

fourth column).

Total Revenue = Price Quantity

Table 2

Make sure that students realize that firms in perfect competition can only change

their level of total revenue by varying their level of output because they have no

ability to change the price.

You may want to make it clear that, by definition, average revenue is always equal to

price. But marginal revenue is equal to price only for firms that operate in perfectly

competitive markets.

244 ❖ Chapter 14/Firms in Competitive Markets

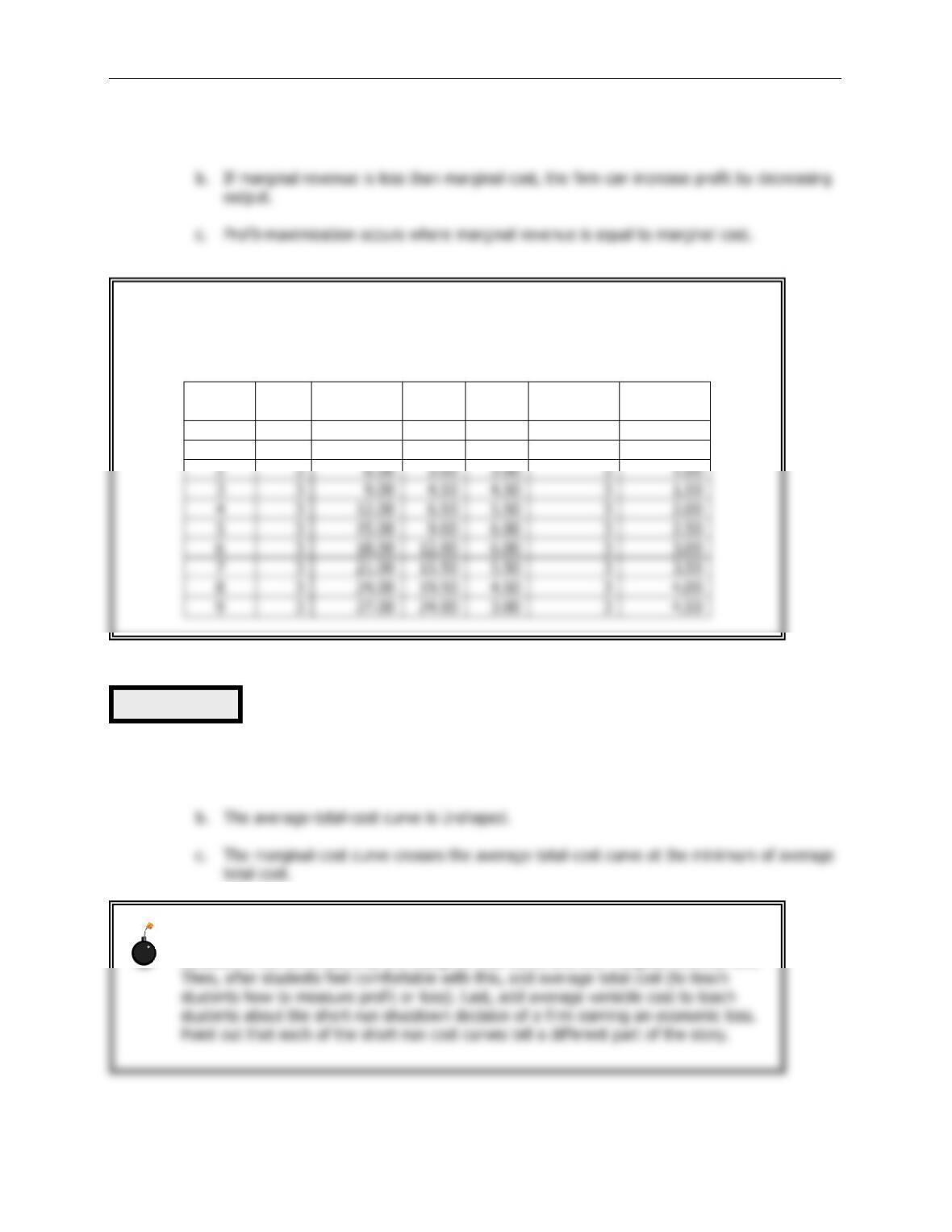

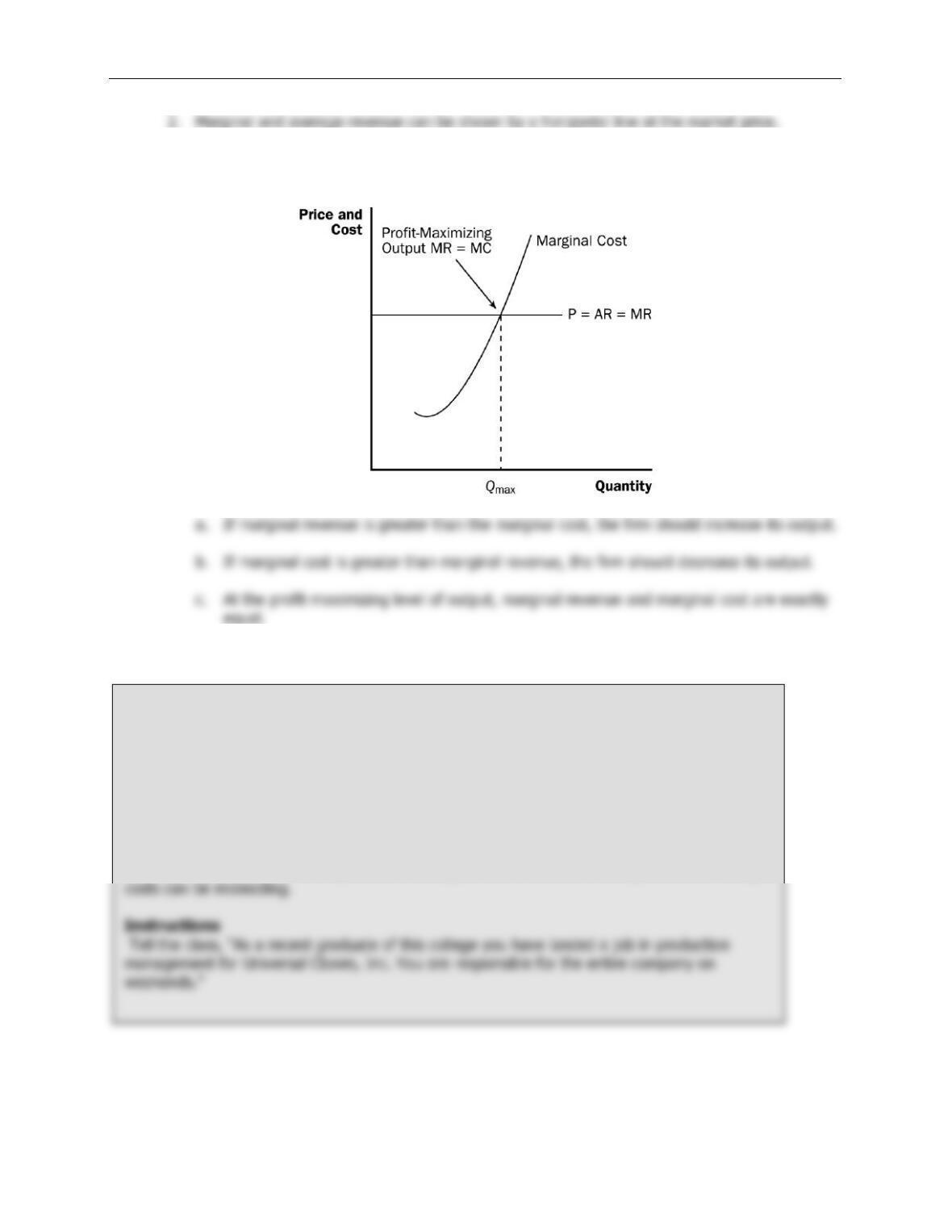

a. As long as marginal revenue exceeds marginal cost, increasing output will raise profit.

B. The Marginal-Cost Curve and the Firm’s Supply Decision

1. Cost curves have special features that are important for our analysis.

a. The marginal-cost curve is upward sloping.

Figure 1

The graphs in this chapter often confuse students because they contain many

different curves at the same time. Thus, the first time you draw the profit-maximizing

decision of the firm, use only the marginal cost curve and the marginal revenue line.

ALTERNATIVE CLASSROOM EXAMPLE:

Paulo’s Ping Pong Balls is a firm that operates in a competitive market. The ping pong balls

sell for $3 per package. Fill in the following table with the class’s help and discuss the profit–

maximizing level of output:

Output

Price

Total

Revenue

Total

Cost

Profit

Marginal

Revenue

Marginal

Cost

0

$3

$0.00

$1.50

$-1.50

—-

—-

1

3

3.00

2.00

1.00

$3

$0.50

2

3

6.00

3.00

3.00

1.00

3

3

9.00

4.50

4.50

1.50

4

3

12.00

6.50

5.50

2.00

5

3

15.00

9.00

6.00

2.50

6

3

18.00

12.00

6.00

3.00

7

3

21.00

15.50

5.50

3.50

8

3

24.00

19.50

4.50

4.00

Chapter 14/Firms in Competitive Markets ❖ 245

3. To find the profit-maximizing level of output, we can follow the same rules that we discussed

above.

4. These rules apply not only to competitive firms, but to firms with market power as well.

Activity 1—A Profitable Opportunity?

Type: In-class assignment

Topics: Profit maximization

Materials needed: None

Time: 15 minutes

Class limitations: Works in any size class

Purpose

This exercise reinforces the importance of marginal cost in decisionmaking. It shows average

246 ❖ Chapter 14/Firms in Competitive Markets

“Your costs are shown below.”

Quantity Average Total Cost

500 200

501 201

Your current level of production is 500 units. All 500 units have been ordered by your regular

customers.

Common Answers and Points for Discussion

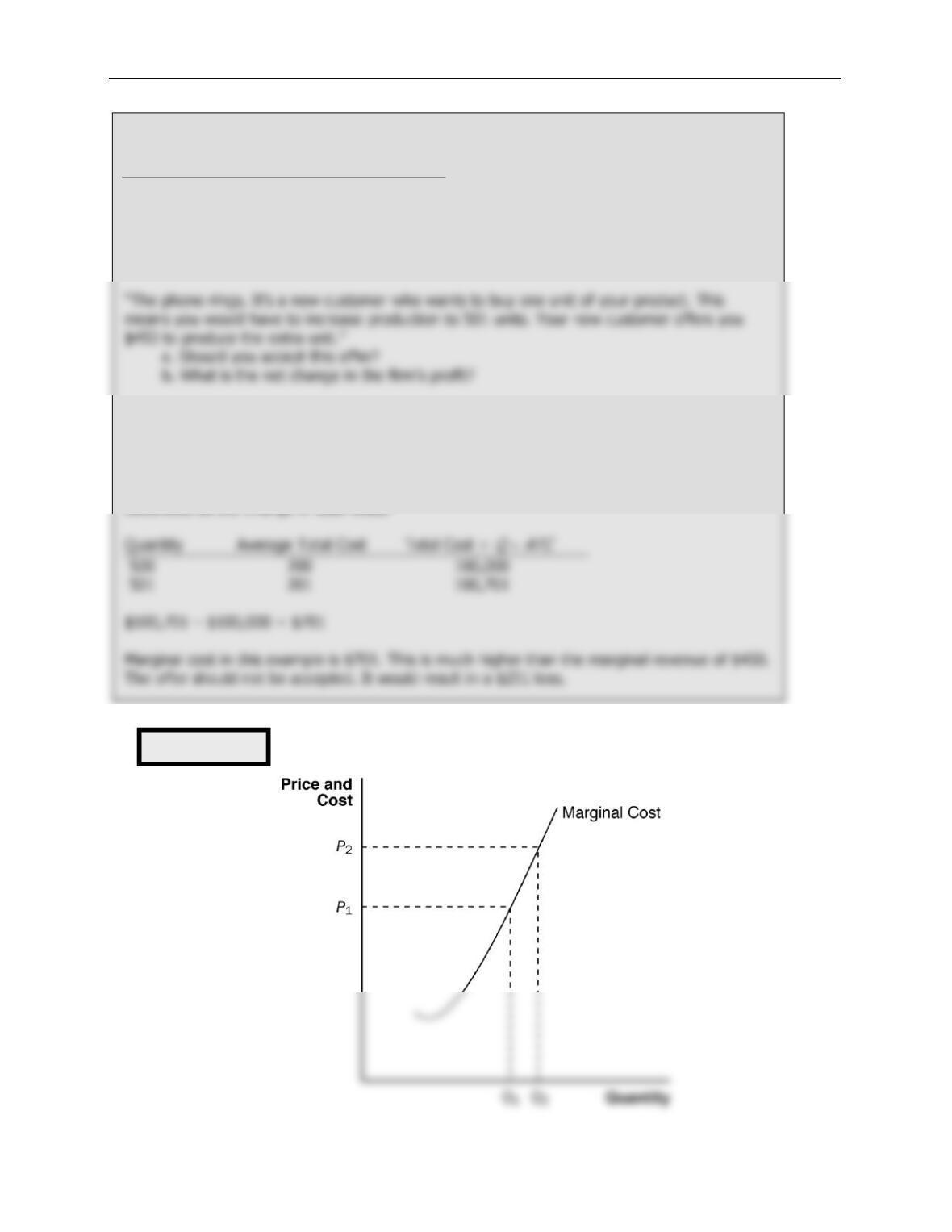

Most students will answer “yes.” Selling something for $450 when the average cost of

production is $201 seems like good business. They are wrong.

The relevant comparison is marginal cost to marginal revenue. Marginal cost can be easily

calculated as the change in total costs.

Figure 2

Chapter 14/Firms in Competitive Markets ❖ 247

5. If the price in the market were to change to

P

2, the firm would set its new level of output by

equating marginal revenue and marginal cost.

C. The Firm’s Short-Run Decision to Shut Down

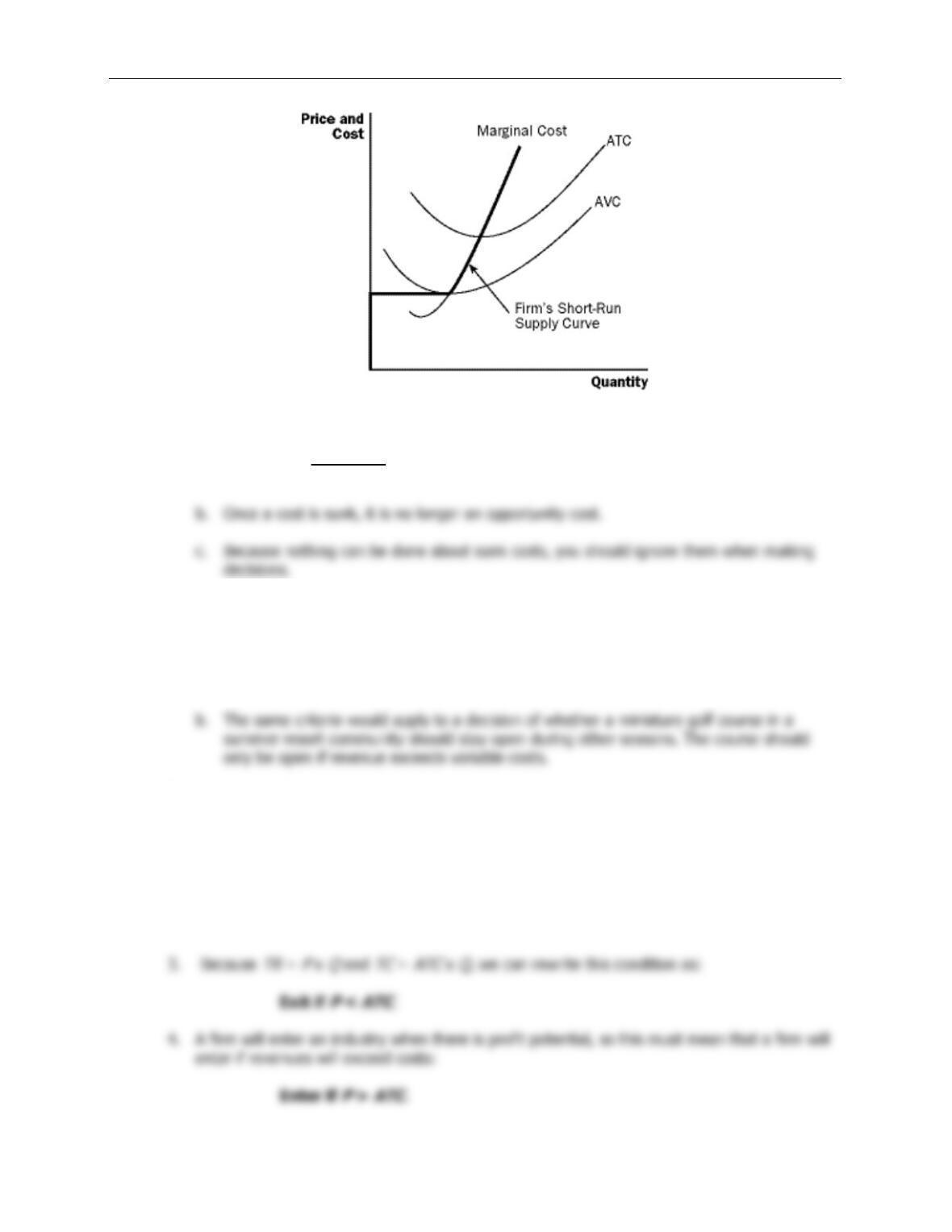

1. In certain circumstances, a firm will decide to shut down and produce zero output.

2. There is a difference between a temporary shutdown of a firm and an exit from the market.

a. A shutdown refers to a short-run decision not to produce anything during a specific

3. If a firm shuts down, it will earn no revenue and will have only fixed costs (no variable

costs).

4. Therefore, a firm will shut down if the revenue that it would earn from producing is less than

its variable costs of production:

6. We now can tell exactly what the firm will do to maximize profit (or minimize loss).

a. If the price is less than average variable cost, the firm will produce no output.

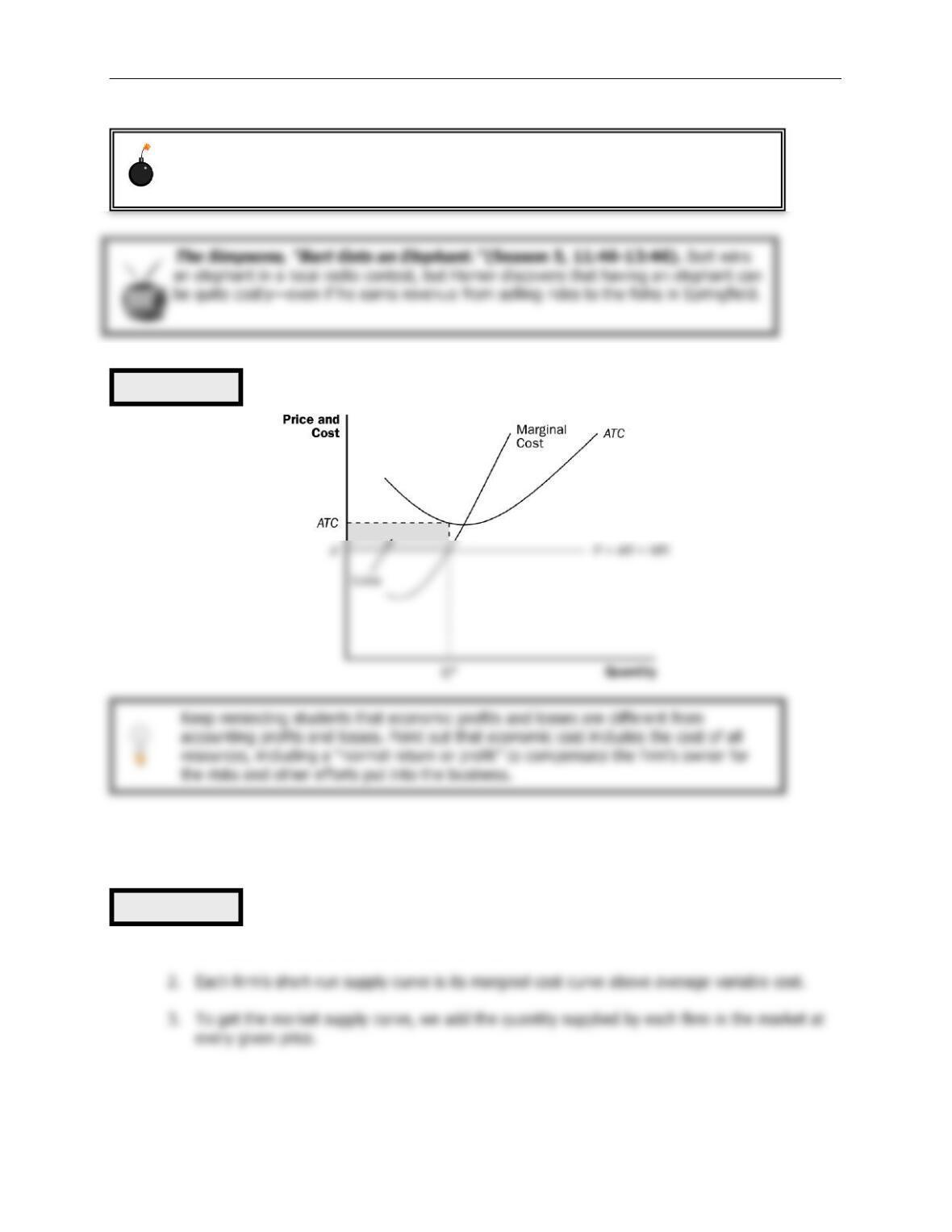

7. Therefore, the competitive firm’s short-run supply curve is the portion of its marginal revenue

curve that lies above average variable cost.

Figure 3

248 ❖ Chapter 14/Firms in Competitive Markets

8. Spilt Milk and Other Sunk Costs

a. Definition of sunk cost: a cost that has been committed and cannot be

recovered.

9.

Case Study: Near-Empty Restaurants and Off-Season Miniature Golf

a. In making a decision of whether or not to open for lunch, a restaurant owner must weigh

revenue with variable costs. (Much of the cost of running a restaurant is somewhat

fixed.)

D. The Firm’s Long-Run Decision to Exit or Enter a Market

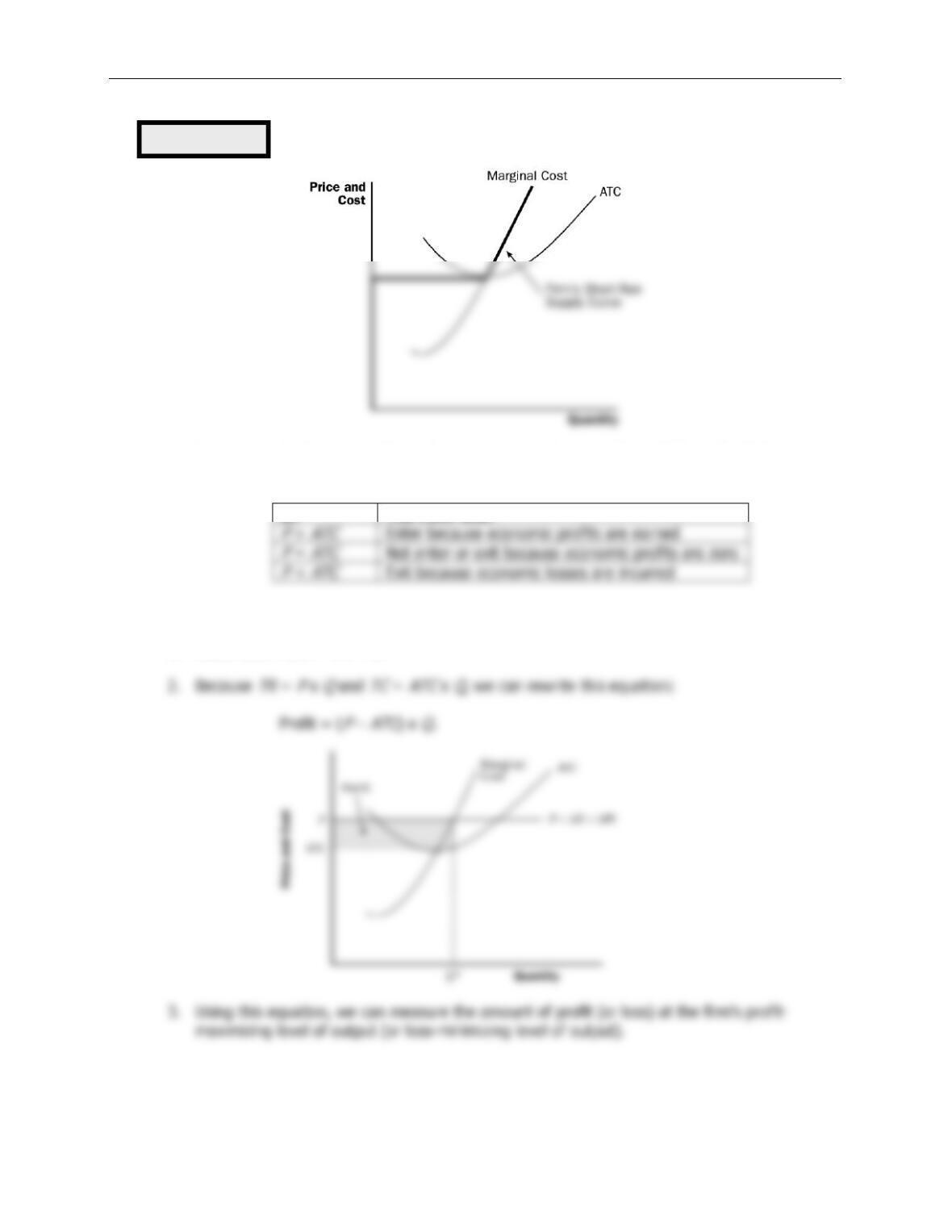

1. If a firm exits the market, it will earn no revenue, but it will have no costs as well.

2. Therefore, a firm will exit if the revenue that it would earn from producing is less than its

total costs:

Exit if

TR

<

TC

.

Chapter 14/Firms in Competitive Markets ❖ 249

5. Because, in the long run, a firm will remain in a market only if

P

≥

ATC

, the firm’s long-run

supply curve will be its marginal cost curve above

ATC

.

If:

The Firm Will:

E. Measuring Profit in Our Graph for the Competitive Firm

1. Recall that Profit =

TR

–

TC

.

Figure 4

250 ❖ Chapter 14/Firms in Competitive Markets

III. The Supply Curve in a Competitive Market

A. The Short Run: Market Supply with a Fixed Number of Firms

1. Example: a market with 1,000 identical firms.

Figure 5

Figure 6

Students always want to use the point of minimum average total cost when finding

profit on the graph. Remind them to always find the average total cost of the profit–

maximizing level of output.

Chapter 14/Firms in Competitive Markets ❖ 251

B. The Long Run: Market Supply with Entry and Exit

1. If firms in a market are earning profit, this will attract new firms.

2. If firms in an industry are incurring losses, firms will exit.

3. At the end of this process of entry or exit, firms that remain in the market must be earning

zero economic profit.

TR

=

TC

.

5. Because

TR

=

P

×

Q

and

TC

=

ATC

×

Q

, we can rewrite this as:

P

=

ATC

.

7. This implies that the long-run equilibrium of a competitive market must have firms operating

at their efficient scale.

C. Why Do Competitive Firms Stay in Business If They Make Zero Profit?

1. Profit is equal to total revenue minus total cost.

D. A Shift in Demand in the Short Run and Long Run

1. Assume that the market begins in long-run equilibrium. This means that firms are earning

zero profit and price equals the minimum of average total cost.

Figure 7