Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 14: HIGHLY LEVERAGED TRANSACTIONS:

LBO Valuation and Modeling Basics

Chapter Discussion Questions

14.1 The adjusted present value model is based on the notion that the value of a firm can be divided into present value

of the firm’s cash flows to equity investors plus the present value of the tax shield. What is the critical assumption

underlying this premise? In your view, under what circumstances might this assumption not be practical?

Answer: The APV model assumes that a firm’s value is independent of the way in which it is financed. For this to

14.2 How should the adjusted present value method be modified when it is applied to highly leveraged transactions?

14.3 What is the cost of financial distress? Be specific.

Answer: Financial distress has both a direct and indirect impact on the firm. Direct costs can include the cost

associated with reorganization in bankruptcy and possibly liquidation. Indirect costs incurred by firms able to

14.4 What does the APV valuation implicitly assume that makes its results highly problematic in valuing highly

leveraged businesses?

14.5 What is a firm’s tax shield and how can it be estimated?

Answer: A tax shield represents the present value of a firm’s anticipated tax savings resulting from the tax

14.6 What are the primary advantages and disadvantages of the using the cost of capital and adjusted present value

methods to value highly leveraged transactions?

Answer: The major advantage of the cost of capital method is that it adjusts the discount rate for changing risk due

to fluctuations in a firm’s debt to equity ratio; the major advantage of the APV model is its simplicity. In contrast,

2

14.7 Investment bankers routinely value firms using LBO analyses in addition to conventional DCF and relative

valuation methods. Under what circumstances does it make sense to employ a leveraged buyout analysis as one

means of valuing a firm?

Answer: When there is a reasonable likelihood that a financial sponsor will be interested in the target if it offers a

14.8 In what way is a conventional DCF analysis similar to a leveraged buyout analysis of a target and in what ways are

they different?

Answer: They are similar in that they both require projected cash flows, terminal value, present value calculations,

and discount rates. However, the DCF analysis solves for the present value of the firm while the LBO analysis

14.9 How may a firm’s borrowing capacity be defined?

Answer: It is the amount of debt a firm may borrow without materially increasing its cost of borrowing or

14.10 The internal rate of return is a crucial decision variable for LBO investors. What are the critical assumptions that

must be made in its calculation?

Answer: The IRR calculation considers both the initial investment in the target firm plus future capital

Solutions to End of Chapter Problems:

14.13. Assume that, based on similar transactions, an analyst believes that a buyout firm will be able to borrow

about 5.5 times first year EBITDA of $200 million (i.e., about $1.1 billion) and that the buyout firm has a

target senior to subordinated debt split of 75-to-25 percent. Further assume that investors in the buyout firm

wish to exit the business within 8 years after having repaid all of the senior debt. To accomplish this

objective, the investors intend to use 100 percent of cash available for debt reduction to pay off senior debt

and that the subordinated debt is payable as a balloon note beyond year 8. Using the scenario in the template

entitled “Excel-Based Firm Borrowing Capacity Model” on the CDROM accompanying this textbook as

the base case, answer the following questions:

a. Will the buyout firm be able to exit their investment by the 8th year if sales grow at 3 percent rather than 5

percent assumed in the base case and still satisfy the assumptions used in the base case scenario? After

re-running the model using the lower sales growth rate, what does this tell you about the model’s

sensitivity to relatively small changes in assumptions?

Answer: No, $98.1 million in senior debt would still be outstanding making the firm less attractive for an

b. How does this slower sales growth scenario affect the amount the buyout firm could borrow initially if

the investors still want to exit the business by the 8th year after paying off 100 percent of the senior debt

and to maintain the same senior to subordinated debt split?

3

Problem 14-16 Solution to Part A

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Assumptions:

Sales Growth %

0

1.03

1.03

1.03

1.03

1.03

1.03

1.03

1.03

Cost of Sales (COS) as % of Sales

0.5

0.5

0.5

0.5

0.5

0.5

0.5

0.5

0.5

Sales, General & Admin. Exp. as % of Sales

0.1

0.1

0.1

0.1

0.1

0.1

0.1

0.1

0.1

Interest on Subordinated Debt %

0.09

0.09

0.09

0.09

0.09

0.09

0.09

0.09

0.09

Tax rate

0.4

0.4

0.4

0.4

0.4

0.4

0.4

0.4

0.4

Cash & Marketable Securities as % Sales

0.01

0.01

0.01

0.01

0.01

0.01

0.01

0.01

0.01

Change in Working Capital as % of Sales

0.02

0.02

0.02

0.02

0.02

0.02

0.02

0.02

0.02

Capital Expenditures as % of Sales

0.03

0.03

0.03

0.03

0.03

0.03

0.03

0.03

0.03

($Millions)

Sales

500.0

515.0

530.5

546.4

562.8

579.6

597.0

614.9

633.4

Less: Cost of Sales

250.0

257.5

265.2

273.2

281.4

289.8

298.5

307.5

316.7

Less: Sales, General Admin. Exp.

50.0

51.5

53.0

54.6

56.3

58.0

59.7

61.5

63.3

Less: Interest Expense

Senior Debt

52.2

48.1

43.6

38.7

33.3

27.5

21.1

14.3

Subordinated Debt

27.0

27.0

27.0

27.0

27.0

27.0

27.0

27.0

Total Interest Expense

79.2

75.1

70.6

65.7

60.3

54.5

48.1

41.3

Equals: Income Before Tax

106.4

116.0

126.3

137.1

148.5

160.6

173.4

186.9

Cash Balance

5.0

5.2

5.3

5.5

5.6

5.8

6.0

6.1

6.3

Senior Debt Outstanding at yearend1

745.6

686.9

622.6

552.3

475.6

392.3

301.9

204.0

98.1

Subordinated Debt Outstanding at yearend2

300.0

300.0

300.0

300.0

300.0

300.0

300.0

300.0

300.0

5

Problem 14-16 Solution to Part B

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Assumptions:

Sales Growth %

0

1.03

1.03

1.03

1.03

1.03

1.03

1.03

1.03

Cost of Sales (COS) as % of Sales

0.5

0.5

0.5

0.5

0.5

0.5

0.5

0.5

0.5

Sales, General & Admin. Exp. as % of Sales

0.1

0.1

0.1

0.1

0.1

0.1

0.1

0.1

0.1

Cash & Marketable Securities as % Sales

0.01

0.01

0.01

0.01

0.01

0.01

0.01

0.01

0.01

Change in Working Capital as % of Sales

0.02

0.02

0.02

0.02

0.02

0.02

0.02

0.02

0.02

Capital Expenditures as % of Sales

0.03

0.03

0.03

0.03

0.03

0.03

0.03

0.03

0.03

($Millions)

Sales

500.0

515.0

530.5

546.4

562.8

579.6

597.0

614.9

633.4

Less: Cost of Sales

250.0

257.5

265.2

273.2

281.4

289.8

298.5

307.5

316.7

Less: Sales, General Admin. Exp.

50.0

51.5

53.0

54.6

56.3

58.0

59.7

61.5

63.3

Equals: EBITDA

200.0

206.0

212.2

218.5

225.1

231.9

238.8

246.0

253.4

Less: Depreciation

15.0

15.5

15.9

16.4

16.9

17.4

17.9

18.4

19.0

Less: Amortization

5.0

5.2

5.3

5.5

5.6

5.8

6.0

6.1

6.3

Plus: Interest Income

0.2

0.2

0.2

0.2

0.2

0.2

0.2

0.2

0.2

Less: Interest Expense

Senior Debt

47.3

42.9

38.2

33.1

27.5

21.4

14.8

7.7

Subordinated Debt

27.0

27.0

27.0

27.0

27.0

27.0

27.0

27.0

Total Interest Expense

74.3

69.9

65.2

60.1

54.5

48.4

41.8

34.7

6

Cash Balance

5.0

5.2

5.3

5.5

5.6

5.8

6.0

6.1

6.3

Senior Debt Outstanding at yearend1

675.0

613.4

546.0

472.4

392.5

305.6

211.6

109.9

0.1

7

14.14. By some estimates, as many as one-fourth of the LBOs between 1987 and 1990 (the first mega LBO boom)

went bankrupt. The following data illustrate the extent of the leverage associated with the largest completed

LBOs of 2006 and 2007 (the most recent mega-LBO boom). Equity Office Properties and Alltel have been

sold. Use the data given in the following table to calculate the equity contribution made by the buyout firms as

a percent of enterprise value and the dollar value of their equity contribution. What other factors would you

want to know in evaluating the likelihood that these LBOs will end up in bankruptcy?

Solution to Problem 14-17

Top Ten Completed Buyouts of 2007Ranked by Deal Enterprise Value

Target

Bidder (s)

Enterprise

Net

Debt

Equity

Value

Interest

Value (EV)

% of EV

% of

EV

of Equity

Coverage

($Billions)

($Billions)

TXU

KKR, TPG,

43.8

89.5

10.5

4.6

1.0

Goldman Sachs

Equity Office Properties

Blackstone

38.9

Sold

NA

NA

Sold

Net debt (D) as a percent of average equity is .81. Therefore, average equity (E) as a percent of average enterprise value

(EV) is 19% (i.e., Recall that E + D = EV and E/EV = 1 – D/EV). The dollar value of the average equity contribution

for the top ten 2007 buyouts was $5.3 billion (i.e., .19 x 27.9).

Solutions to End of Chapter Case Study Questions

Investor Group Takes Dun & Bradstreet Private in a Leveraged Buyout

Discussion Questions:

8

1. Speculate why the D&B board and management chose a leveraged buyout to alternative strategies?

Answer: To grow, the firm needed to reinvest in itself to change its product offering to better serve its

customers in making credit decisions and in target marketing. To do so, would require spending hundreds of

2. Why did the sponsor group contribute cash from Merger Sub Parent to Merger Sub rather than lend the money

to Merger Sub?

3. Why is D&B merged with Merger Sub and not directly with Merger Sub Parent?

4. What is the purpose of the bridge loan facilities?

5. What type of a merger is described in Figure 14.1? Why is it structured in this manner?

Answer: This is a reverse triangular merger in which Merger Sub is merged into D&B with D&B surviving.

6. Is this transaction likely to be taxable or nontaxable to pre-buyout D&B shareholders? Is D&B post-buyout

likely to be paying much in the way of taxes during the several years following closing? Explain your answer.

7. Why did the sponsor group choose to purchase preferred stock as well as common?

Answer: In the event of liquidation of the firm, preference stockholders would be paid before common

Examination Questions and Answers

True/False Questions: Answer true or false to the following questions:

1. An LBO can be valued from the perspective of common equity investors only or all those who supply funds,

including common and preferred investors and lenders. True or False

9

2. Conventional capital budgeting procedures are of little use in valuing an LBO. True or False

3. An LBO transaction makes sense from the viewpoint of all investors if the present value (of the cash flows to

the firm or enterprise value, discounted at the weighted-average cost of capital, equals or exceeds the total

investment consisting of debt, common equity, and preferred equity required to buy the outstanding shares of

the target company. True or False

4. It is impossible for a leveraged buyout to make sense to common equity investors but not to other investors,

such as pre-LBO debt holders and preferred stockholders. True or False

5. Once the LBO has been consummated, the firm's perceived ability to meet its obligations to current debt and

preferred stockholders often deteriorates because the firm takes on a substantial amount of new debt. The

firm's pre-LBO debt and preferred stock may be revalued in the market by investors to reflect this higher

perceived risk, resulting in a significant reduction in the market value of both debt and preferred equity owned

by pre-LBO investors. True or False

6. The cost of capital method attempts to adjust future cash flows for changes in the cost of capital as the firm

reduces its outstanding debt. True or False

7. The adjusted present value method values firm without debt and then subtracts the value of future tax savings

resulting from the tax-deductibility of interest. True or False

8. If the debt-to-equity ratio is expected to fluctuate substantially during the forecast period, applying

conventional capital budgeting techniques that discount future cash flows with a constant weighted average

cost of capital (CC) is appropriate. True or False

9. Many firms reduce their outstanding debt relative to equity and such changes in the capital structure distort

valuation estimates based on traditional DCF methods. True or False

10. The extremely high leverage associated with leveraged buyouts significantly increases the riskiness of the cash

flows available to equity investors as a result of the increase in fixed interest and principal repayments that

must be made to lenders. Consequently, the cost of equity should be adjusted for the increased leverage of the

firm. True or False

11. Since an LBO’s debt is to be paid off over time, the cost of equity decreases over time, assuming other factors

remain unchanged. Therefore, in valuing a leveraged buyout, the analyst must project free cash flows,

adjusting the discount rate to reflect changes in the capital structure. True or False

12. Projecting future annual debt-to-equity ratios depends on knowing the firm’s debt repayment schedules and

projecting growth in the market value of shareholders' equity. True or False

13. For simplicity, the market value of common equity can be assumed to grow in line with the projected growth

10

14. As the LBO's extremely high debt level is reduced, the cost of equity needs to be adjusted to reflect the decline

in risk, as measured by the firm's unlevered beta. True or False

15. Using the cost of capital method to value LBOs requires adjusting the firms unlevered beta in each period

using the firm's projected debt-to-equity ratio for that period. True or False

16. Because the firm's cost of equity changes over time, the firm's cumulative cost of equity is used to discount

projected cash flows. This reflects the fact that each period's cash flows generate a different rate of return.

True or False

17. An LBO deal makes sense to common equity investors if the present value of free cash flow to equity exceeds

the value of the equity investment in the deal. True or False

18. The deal makes sense to lenders and noncommon equity investors if the present value of free cash flow to

equity investors exceeds the total cost of the deal. True or False

19. Some analysts suggest that the problem of a variable discount rate can be avoided by separating the value of a

firm's operations into two components: the firm's value as if it were debt free and the value of interest tax

savings. True or False

20. Using the adjusted present value method to value a LBA assumes the total value of the firm is the present

value of the firm's free cash flows to lenders plus the present value of future tax savings discounted at the

firm's unlevered cost of equity. True or False

21. The total value of the firm according to the adjusted present value method is the present value of the firm's

free cash flows to equity investors plus the present value of future tax savings discounted at the firm's

unlevered cost of equity. True or False

22. The unlevered cost of equity is often viewed as the appropriate discount rate rather than the cost of debt or a

risk-free rate because tax savings are subject to risk, since the firm may default on its debt or be unable to

utilize the tax savings due to continuing operating losses. True or False

23. The justification for the adjusted present value method reflects the theoretical notion that firm value should is

affected by the way in which it is financed. True or False

24. The justification for the adjusted present value (APV) method reflects the theoretical notion that firm value

should not be affected by the way in which it is financed. However, recent studies empirical suggest that for

LBOs, the availability and cost of financing does indeed impact financing and investment decisions. True or

False

25. In the presence of taxes, firms are often less leveraged than they should be, given the potentially large tax

benefits associated with debt. Firms can increase market value by increasing leverage to the point at which the

additional contribution of the tax shield to the firm's market value begins to decline. True or False

11

26. The tax benefits of higher leverage may be partially or entirely offset by the higher probability of default

associated with an increase in leverage. True or False

28. In using the adjusted present value method to value highly leveraged transactions, the analyst need not be

concerned about the costs of financial distress. True or False

29. The direct cost of financial distress includes the costs associated with reorganization in bankruptcy and

30. Financial distress does not have a material indirect cost to firms able to avoid bankruptcy or liquidation. True

or False

31. In applying the adjusted present value method, the present value of a highly leveraged transaction should

reflect the present value of the firm without leverage plus the present value of tax savings plus the present

32. The expected cost of and probability of occurring of financial distress are easily forecasted. True or False

33. Many analysts use the cost of capital method because of its relative simplicity. True or False

34. In the adjusted present value method, the levered cost of equity is used for discounting cash flows during the

period in which the capital structure is changing and the weighted-average cost of capital for discounting

during the terminal period. True or False

35. The present value of tax savings is irrelevant to the adjusted present value method. True or False

36. In discount projected tax savings in the adjusted present value method, the firm's unlevered cost of equity

should be used, since it reflects a higher level of risk than either the WACC or after-tax cost of debt. Tax

savings are subject to risk comparable to the firm's cash flows in that a highly leveraged firm may default and

the tax savings go unused. True or False

37. To determine the total value of the firm using the adjusted present value method, add the present value of the

firm's cash flows to equity, interest tax savings, and terminal value discounted at the firm's unlevered cost of

equity and subtract the present value of the expected cost of financial distress. True or False

38. Although the proposition that the value of the firm should be independent of the way in which it is financed

may make sense for a firm whose debt-to-capital ratio is relatively stable and similar to the industry's, it is

highly problematic when it is applied to highly leveraged transactions. True or False

12

39. Without adjusting for the cost of financial distress, the adjusted present value method implies that the value of

40. The adjusted present value method implies that the firm should optimally use 100% debt financing to take

maximum advantage of the tax shield created by the tax deductibility of interest. True or False

41. The primary advantage of the cost of capital method is its relative computational simplicity. True or False

42. The adjusted present value approach takes into account the effects of leverage on risk as debt is repaid. True or

False

43. An LBO model is used to determine what a firm is worth in a highly leveraged transaction and is applied when

there is the potential for a financial buyer or sponsor to acquire the business. True or False

44. An LBO model helps define the amount of debt a firm can support given its assets and cash flows. True or

False

45. LBO analyses are similar to DCF valuations in that they require projected cash flows, present values, and

discount rates; however, LBO models do not require the estimation of terminal values. True or False

46. The DCF analysis solves for the present value of the firm, while the LBO analysis solves for the discount rate

47. While the DCF approach often is more theoretically sound than the IRR approach (which can have multiple

solutions), IRR is more widely used in LBO analyses since investors often find it more intuitively appealing,

that is, the higher an investment’s IRR, the better the investment’s return relative to its cost The IRR is the

discount rate that equates the projected cash flows and terminal value with the initial equity investment. True

or False

48. Financial buyers often will attempt to determine the highest amount of debt possible (i.e., the borrowing

capacity of the target firm) to maximize their equity contribution in order to maximize the IRR. True or False

49. An LBO analysis usually starts with the determination of cash available for financing a target firm’s future

debt obligations and the sources of such debt. True or False

50. The most important calculation to the financial sponsor in an LBO analysis is the IRR. True or False

Multiple Choice Questions: Circle only one of the alternatives for each of the following questions:

1. Using the cost of capital method to value an LBO involves which of the following steps?

a. Projection of annual cash flows

b. Projection of annual debt-to-equity ratios

c. Calculation of a terminal value

d. Adjusting the discount rate to reflect changing risk.

e. All of the above

13

2. Using the cost of capital method to value an LBO involves all of the following steps except for which of the

following?

a. Adjusting the discount rate to reflect changing risk.

b. Adding the present value of future tax savings to the present value of annual free cash flows to

equity.

c. Calculating a terminal value.

d. Projecting annual debt-to-equity ratios.

e. Projecting annual cash flows.

3. Which of the following are steps often found in developing a LBO model?

a. Cash flow projections

b. Determining a firm’s borrowing capacity

c. Determining a financial sponsor’s equity contribution

d. A, B, and C

e. A and C only

4. Which of the following is not true about LBO models?

a. They rarely use IRR calculations

b. Borrowing capacity is relatively unimportant

c. The financial sponsor’s equity contribution is determined before the target firm’s borrowing capacity

d. A, B, and C

e. A and B only

5. Which of the following are often viewed as disadvantages of the adjusted present value method?

a. Ignores the effects of leverage on the discount rate as debt is repaid

b. Requires estimation of the cost and probability of financial distress

c. It is unclear how to define the proper discount rate

d. A and B only

e. A, B, and C

6. Which of the following is true of the cost of capital method of valuation?

a. It is generally more tedious to calculate than alternative methodologies

b. It requires the separate estimation of the present value of future tax savings

c. It adds the present value of the firm without debt to the present value of tax savings

d. It does not adjust the discount rate as debt is repaid

e. All of the above

7. Which of the following is true of the adjusted present value method of valuation?

a. Calculates the present value of tax benefits separately

b. Calculates the present value of the firm’s cash flow without debt

c. Adds A and B together

d. A, B, and C

e. A and B only

8. Which of the following is not true about the cost of capital method of valuation?

a. It does not adjust the discount rate for risk as debt is repaid.

b. It requires the projection of future cash flows

c. It requires the projection of future debt-to-equity ratios.

14

d. It requires the calculation of a terminal value

e. None of the above

9. An LBO can be valued from the perspective of which of the following?

a. Equity investors

b. Lenders

c. All those supplying funds to finance the transaction

d. A and B only

e. A, B, and C

10. The riskiness of highly leveraged transactions declines overtime due to which of the following factors?

a. Debt reduction assuming nothing else changes

b. Increasing discount rates

c. A rising unlevered beta

d. An unchanging cost of equity

e. An unchanging weighted average cost of capital

Case Study Short Essay Examination Questions

STAPLES GOES PRIVATE IN RESPONSE

TO THE SHIFT TO ONLINE RETAILING

Key Points

• Traditional "brick and mortar" retailers are confronted increasingly by rapidly changing consumer buying patterns.

• In response, buying out public shareholders enables firms to streamline decision making and move away from an often

all-consuming focus on short-term profits.

• However, going private has its own challenges.

_____________________________________________________________________________________

Behind every major business there is an interesting start up story. Staples, the American multinational office supply

retailing corporation, is no different. Thomas Stemberg, cofounder of Staples Inc., needed a ribbon for his printer. He

was unable to buy one that day because the local supply stores were closed for a major U.S. holiday. His frustration

with having to rely on small stores for critical supplies led him to conceive of an office supply superstore. The firm

opened its first such store in Brighton Massachusetts on May 1, 1986, eventually growing to a multinational business

with more than 1,500 stores in North America in the early 2000s.

Fast forward three decades from the firm's first year of operation. A changing competitive landscape forced the firm

to move its business model from one dependent on brick and mortar stores to one relying on online sales. The number

of competitors in the office supply space had exploded and included such online retailers as Amazon.com, mass

merchandisers such as Walmart and Target, warehouse clubs such as Costco, and electronics retail stores like Best Buy.

Staples migration from physical stores has been substantial, with about 60% of its revenue coming from online

orders in 2016. But the market appeared to move faster than Staples could, resulting in a continued erosion in the firm's

revenue. Despite a 48% market share in the United States, the firm was compelled to shutter hundreds of stores in

recent years. Staple's board decided that selling the business was the best possible option for the firm's shareholders

after its shares had plunged to $7 dollars in early 2017 from a high of $18 in late 2014.

15

$6.9 billion, a wager that the office-supply chain can re-emerge as a modern seller of business services. The transaction

lets Staples focus on a turnaround plan that includes reducing its retail footprint.

Despite facing severe competitive pressures, Staples still represents substantial scale with total sales in 2016

topping $18 billion, as compared to a peak of almost $25 billion in 2011. Excluding a series of one time charges, the

firm posted an operating profit of $913 million in 2016. At the end of 2016, the firm's net debt position (i.e., cash less

Canadian retail, and business to business) in an effort to separately finance each entity within the same holding

company. In this way, default by any one subsidiary may be contained within that unit.

Private equity partners usually have a clear timeline as to when then expect to exit their investments. Given turmoil

within the retail industry, exiting these businesses any time soon is problematic. Undertaking an initial public offering

would require a significant change of heart for investors who have soured on Staples. Sycamore could sell to a strategic

buyer such as Wal-Mart if the business can be positioned as primarily an online provider of business services. Finally,

other private equity firms with excess cash to put to work may be interested in Staples.

Immucor is Acquired by TPG Capital

Key Points:

• Two-stage tender offers coupled with a top-up option increase both the speed and certainty of closing.

• Holding company structures commonly are used in leveraged buyouts because of the potential risk associated

with such transactions.

• It is especially critical to assess the credibility of assumptions underlying projected financial performance in

highly leveraged transactions.

_____________________________________________________________________________________________

16

Immucor, Inc., a Georgia corporation, develops, manufactures and sells reagents and automated systems used by

blood banks, hospitals and reference laboratories for testing blood to determine its suitability for blood transfusions.

As the leading supplier of such products, the firm has a 55% market share; a 39% operating profit margin (the highest

in the industry), and a sustainable and predictable cash flow. Nevertheless, there were signs in 2010 that something had

to change. While an aging population would increase the number of transfusions, intensifying customer price

resistance could moderate drastically the firm’s future sales growth. Developing new, more cost effective products

would require significant future spending in research and development. Annual revenue in the fiscal year ending in

May 2011 topped out at $330 million, only $1 million more than the prior year, after several years of sluggish growth.

The firm’s share price had underperformed the overall stock market since 2008.

These issues included Immucor’s desire for a dual or two-tiered tender offer and one-step merger coupled with a

top-up option to provide greater speed and assurance of closing. Subject to the Merger agreement, Immucor would

grant to TPG an irrevocable top-up option to purchase at the offer price the number of shares it needed to own at least

90% of Immucor’s outstanding shares on a fully-diluted basis. Immucor also wanted a “go shop” provision of up to six

weeks to determine if other firms might be willing to make an offer and for TPG to agree to a reverse breakup fee of

$85 million if it could not complete the deal, regardless of the reason. Moreover, Immucor wanted TPG to withdraw its

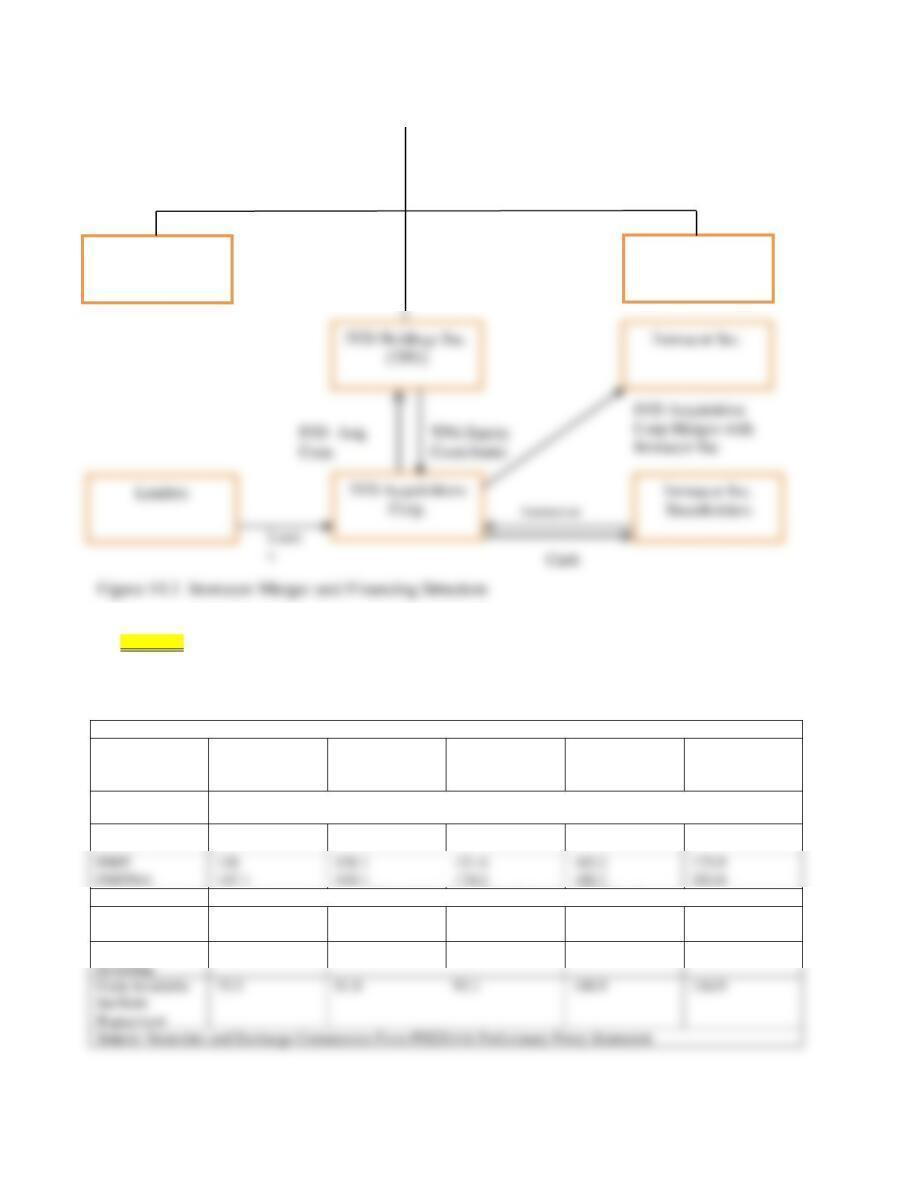

Parties to the merger agreement included Immucor, IVD Holdings Inc., and IVD Acquisitions Corp (Figure 14.1).

IVD Holdings Inc., a Delaware corporation, is a shell corporation formed solely for the purpose of acquiring

Immuncor, completing the transaction outlined in the merger agreement, and arranging financing. IVD Holdings Inc.’s

parent is an affiliate of TPG Partners VI, a limited liability partnership managed by TPG. TPG Partners VI provides the

funds that will be used by IVD holdings to make its equity contribution. IVD Acquisition Corporation, a Georgia

TPG Partners VI

(Limited

Partnership)

17

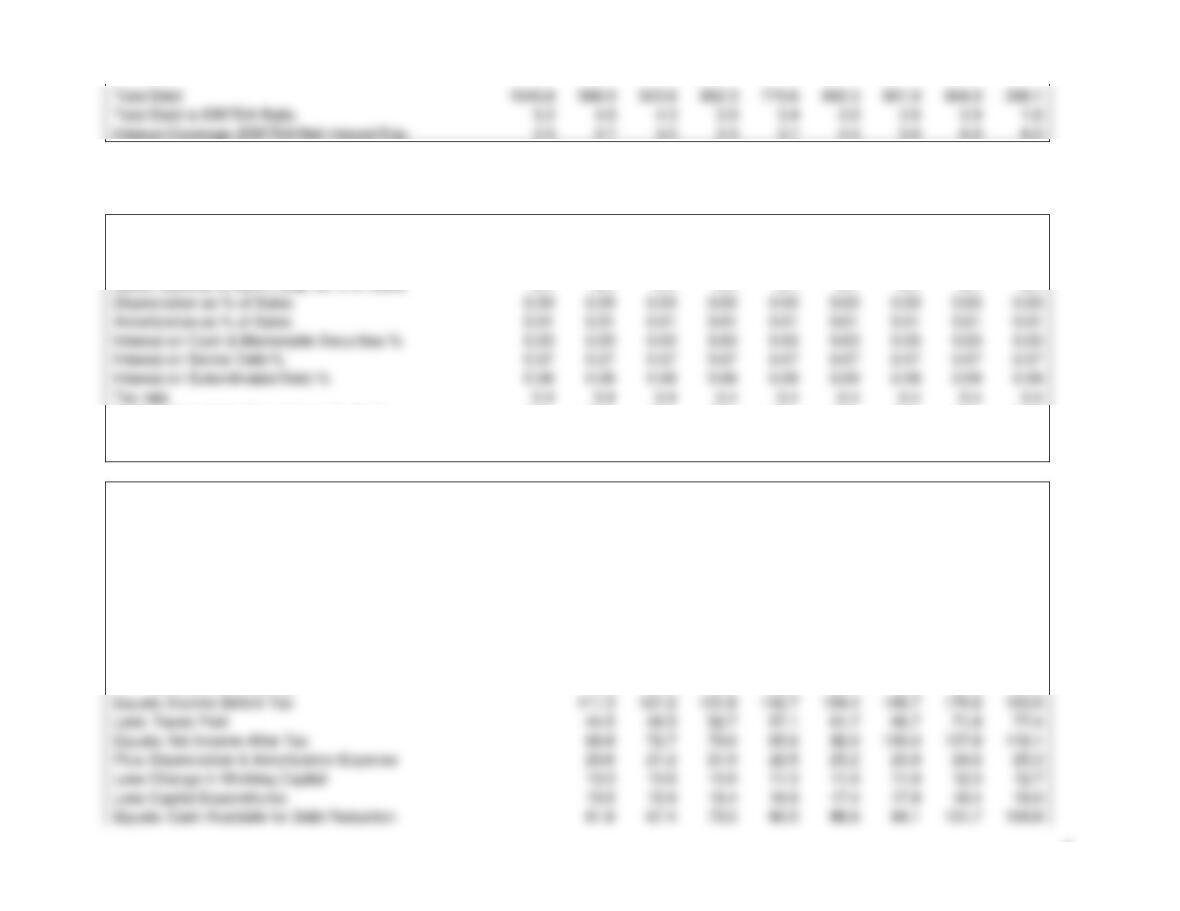

Table 14.7 provides abbreviated income and cash flow statements. Operating profit margins are essentially held

constant at about 38% throughout the five year forecast period. The projected cash available for debt repayment is a

critical projection as it provides an implicit margin of safety in terms of Immucor’s ability to repay its debt incurred as

a result of the going private.

Table 14.7 Immucor Proforma Financial Projections

FY2012 Est.

FY2013 Est.

FY2014 Est.

Fy2015 Est.

FY2016 Est.

Abbreviated Income Statement ($Millions)

Revenue

344.7

368.2

395.6

421.9

450.9

Abbreviated Cash Flow Statement ($Millions)

Cash from

Operations

87.6

94.7

106.9

121.7

132.7

Cash From

(12.1)

(12.9)

(13.8)

(14.8)

(15.8)

Parent for Other

TPG Partners VI

Portfolio

Parent for Other

TPG Partners VI

Portfolio

TPG Partners VI

Funds IVD

Holdings Inc.

18

Discussion Questions:

1. Do you believe Immucor was an attractive candidate for a leveraged buyout? Explain your answer.

Answer: Generally speaking, yes. The firm had strong brand recognition, high profit margins, and substantial

2. What is the purpose of the top up option?

Answer: The top up option is designed to ensure that the buyer can control at least 90% of the stock of the

3. Why does TPG contribute cash rather than lend the money to IVD Acquisitions Corp?

4. Why is Immucor merged with an acquisition subsidiary, IVD Acquisitions Corp, and not with the IVD

Holdings?

5. Do you believe that TPG may have overpaid for Immucor? Explain your answer.

Answer: The EBITDA multiple paid by TPG was 13.4 (purchase price / EBITDA = $1.97 / .147). This

6. Accelerating revenue growth is the primary driver of cash available for debt repayment. Explain why cash

available for debt repayment may be overstated in the projected cash flow statement.

Answer: With operating margins held constant, the primary driver to improving cash flow is the projected

7. What is the purpose of the bridge and revolving loan facilities?

Answer: The bridge loan represents temporary financing giving the firm time to raise longer term or so-called

8. What type of a merger is described in Figure 14.1? In this type of merger, which is the surviving entity,

Immucor or IVD Acquisitions Corp? Why is it structured in this manner?

Answer: This is a reverse triangular merger in which IVD Acquisitions Corp is merged into Immucor with

19

9. Is this transaction likely to be taxable or nontaxable to pre-buyout Immucor shareholders? Is Immucor post-

buyout likely to be paying much in the way of taxes during the several years following closing? Explain your

answer.

Answer: A cash-for-stock transaction will be taxable to pre-buyout shareholders. Immucor is unlikely to be

KINDER MORGAN’s TAKEOVER OF EL PASO

RAISES ETHICAL QUESTIONS

_____________________________________________________________________________________________

Key Points:

• Investor perceptions of CEO, board, and advisor behavior in transactions matters.

• Real or perceived conflicts of interest may trigger litigation.

• However, proving alleged conflicts of interest can be daunting, especially if the takeover premium is

substantial and shareholders approve the deal.

______________________________________________________________________________

Kinder Morgan’s acquisition of El Paso Corporation closed in mid-2012 in a deal valued at $21.1 billion making the

combined firms the largest independent energy pipeline company in the U.S. (See Case Study 4.2). Investors greeted

the announcement of the deal on October 17, 2011 by bidding up Kinder Morgan’s and El Paso’s shares by 4.8% and

25%, respectively. However, within weeks, the deal was embroiled in controversy over the alleged conflicts of interest

of El Paso’s CEO Douglas Foshee and the firm’s investment advisor Goldman Sachs.

Some El Paso shareholders sued to block the deal, arguing that Goldman’s position on both sides of the deal likely

led to an artificially low purchase price for the firm. That is, Goldman served as an advisor to El Paso on the deal while

also owning through its private equity arm a 19% stake in Kinder Morgan valued at more than $4 billion and had two

Investor concerns ranged from the parties involved showing very poor judgment to highly inappropriate behavior.

Apparently, the Chancellor Leo Strine of the Delaware Court of Chancery where the case was adjudicated concurred

with the plaintiffs. While refusing to halt the takeover, Chancellor Strine faulted Mr. Foshee for negotiating the deal

largely on his own and not disclosing to the El Paso board his intention to buy El Paso’s oil and gas exploration

business following closing. Strine noted that he did not halt the deal because that would have deprived the El Paso

shareholders of the purchase price premium; however, the tone of his summary comments certainly left open the option

for disaffected shareholders to seek monetary damages.

20

HCA Goes Public…Again!

________________________________________________________________________

Key Points:

• LBOs create value for equity investors through a combination of leverage, tax savings, improving operating

performance, and properly timing when investors “cash out.”

• LBO leverage and valuation multiples are often measured relative to EBITDA.

________________________________________________________________________

Hospital Corporation of America (HCA), the biggest for-profit hospital chain in the U.S, has a history of going private

through leveraged buyouts (Table 14.8). The firm initially went private in 1989. When it went public in 1992, its

backers were well rewarded. While HCA’s share price doubled (not including stock splits) between the 1992 IPO and

2006, HCA executives, frustrated as the rate of share price appreciation failed to keep pace with gains in cash flow,

Table 14.8 HCA Transaction Timeline

1989

HCA goes private in an LBO valued at $5.1 billion

1992

HCA goes public with investors increasing the value of their initial investment 8 fold

2006

HCA goes private in a highly leveraged transaction valued at $33 billion. Private equity

investors contributed 23% of the purchase price for HCA and borrowed the remainder.

2007-2010

HCA cut costs and improved annual EBITDA cash flow growth from 5 percent in 2006 to

7 percent in 2010.

Despite an enthusiastic investor response to the March 11, 2011 initial public offering, HCA faces significant future

risks. While the expansion of healthcare coverage to 32 million Americans beginning in 2014 will increase potential

revenue, the growing reliance on government reimbursement (currently 41% of total revenue) is likely to pressure

profit margins. Reimbursement rates to providers will be squeezed due to pressures to restrain growth in Medicare and

Medicaid expenditures.