Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

252 ❖ Chapter 14/Firms in Competitive Markets

E. Why the Long-Run Supply Curve Might Slope Upward

1. Because we assumed that all potential entrants faced the same costs as existing firms,

average total cost of each firm was unaffected by the entry of new firms into the market.

2. In this situation, the long-run supply of the market will be a horizontal line at minimum

average total cost.

4. In this situation, the long-run supply curve of the market will be upward sloping.

Figure 8

No matter what the shape of the long-run supply curve, an increase in demand will

Chapter 14/Firms in Competitive Markets ❖ 253

SOLUTIONS TO TEXT PROBLEMS:

Quick Quizzes

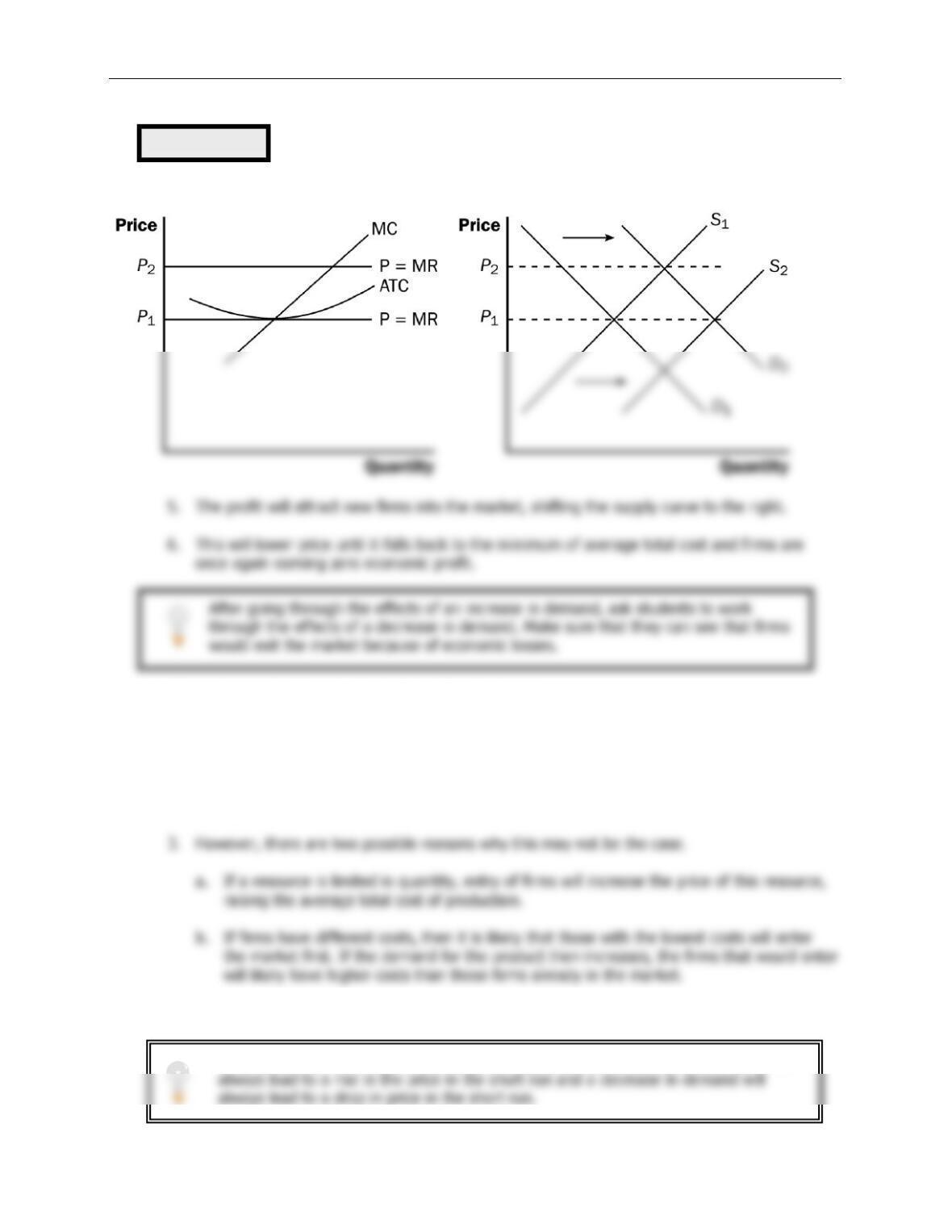

2. A profit-maximizing competitive firm sets price equal to its marginal cost. If price were above

marginal cost, the firm could increase profits by increasing output, while if price were below

marginal cost, the firm could increase profits by decreasing output.

3. In the long run, with free entry and exit, the price in the market is equal to both a firm’s

marginal cost and its average total cost, as Figure 1 shows. The firm chooses its quantity so

that marginal cost equals price; doing so ensures that the firm is maximizing its profit. In the

long run, entry into and exit from the market drive the price of the good to the minimum

point on the average-total-cost curve.

Figure 1

Questions for Review

1. A competitive firm is a firm in a market in which: (1) there are many buyers and many sellers

2. A firm’s total revenue equals its price multiplied by the quantity of units it sells. Profit is the

254 ❖ Chapter 14/Firms in Competitive Markets

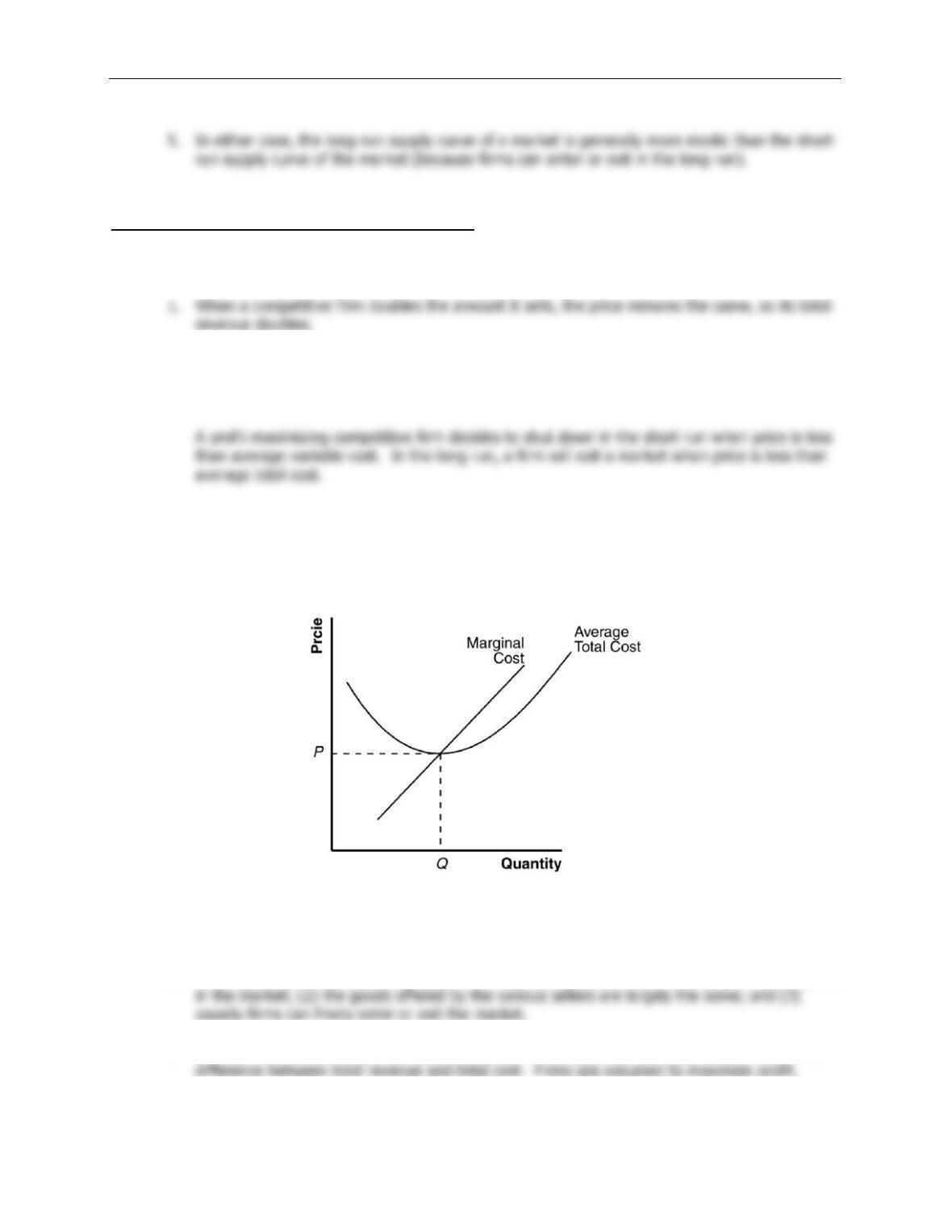

3. Figure 2 shows the cost curves for a typical firm. For a given price (such as

P

*), the level of

output that maximizes profit is the output where marginal cost equals price (

Q

*), as long as

Figure 2

4. A firm will shut down temporarily if the revenue it would get from producing is lower than the

variable costs of production. This occurs if price is less than average variable cost.

6. A firm's price equals marginal cost in both the short run and the long run. In both the short

run and the long run, price equals marginal revenue. The firm should increase output as long

7. The firm's price must equal the minimum of average total cost only in the long run. In the

short run, price may be greater than average total cost (in which case the firm is earning a

profit), price may be less than average total cost (in which case the firm is incurring a loss),

Chapter 14/Firms in Competitive Markets ❖ 255

8. Market supply curves are typically more elastic in the long run than in the short run. In a

Problems and Applications

1. a. As shown in Figure 3, the typical firm's initial marginal-cost curve is

MC

1 and its average-

total-cost curve is

ATC

1. In the initial equilibrium, the market supply curve,

S

1, intersects

b. The increase in the price of oil shifts the typical firm's cost curves up to

MC

2 and

ATC

2,

and shifts the market supply curve up to

S

2. The equilibrium price rises from

P

1 to

P

2, but

the price does not increase by as much as the increase in marginal cost for the firm. As a

result, price is less than average total cost for the firm, so profits are negative.

2. Once you have ordered the dinner, its cost is sunk, so it does not represent an opportunity

cost. As a result, the cost of the dinner should not influence your decision about whether to

finish it or not.

256 ❖ Chapter 14/Firms in Competitive Markets

3. Because Bob’s average total cost is $280/10 = $28, which is greater than the price, he will

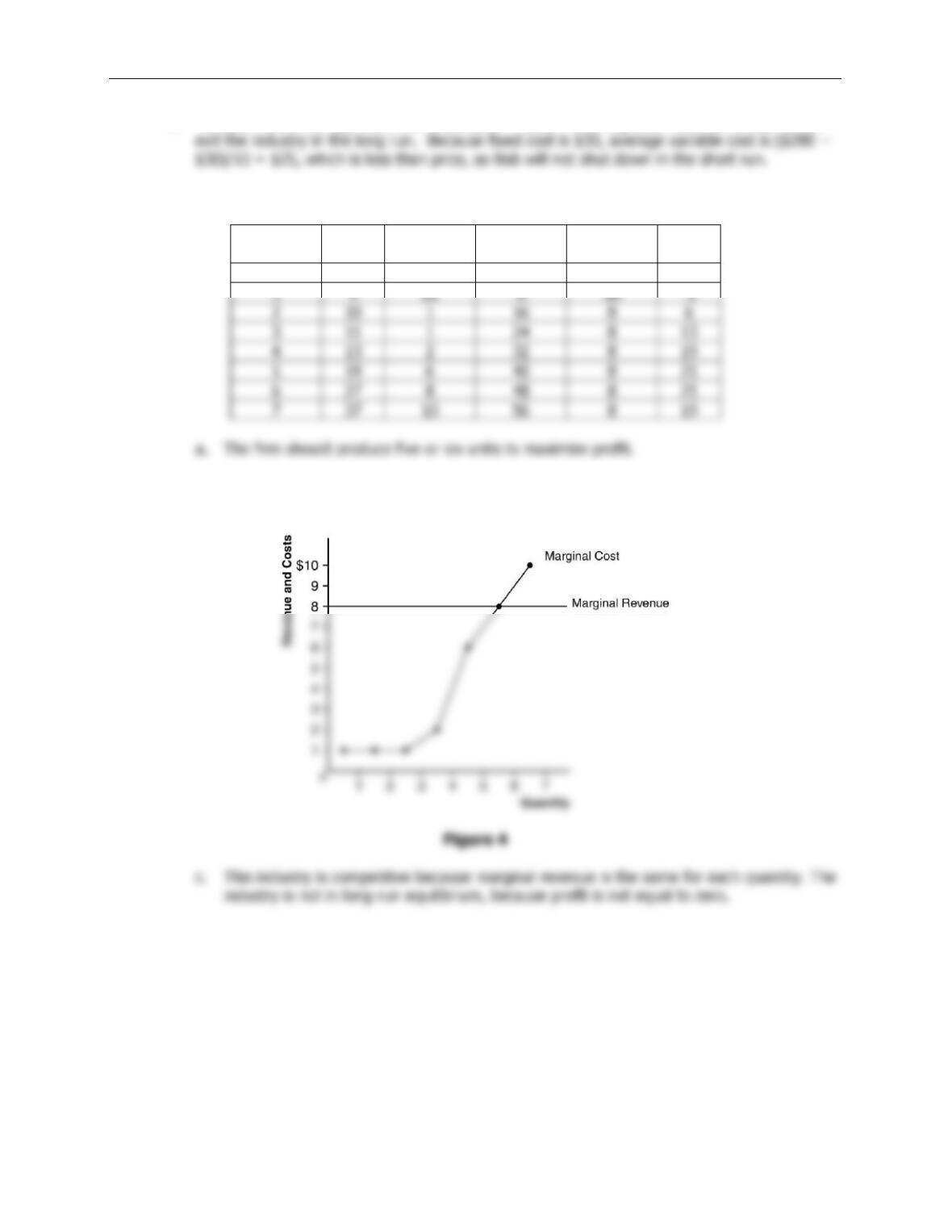

4. Here is the table showing costs, revenues, and profits:

Quantity

Total

Cost

Marginal

Cost

Total

Revenue

Marginal

Revenue

Profit

0

$8

---

$0

---

$-8

b. Marginal revenue and marginal cost are graphed in Figure 4. The curves cross at a

quantity between five and six units, yielding the same answer as in Part (a).

Chapter 14/Firms in Competitive Markets ❖ 257

5. a. Costs are shown in the following table:

Q

TFC

TVC

AFC

AVC

ATC

MC

0

$100

$0

----

----

----

----

1

100

50

$100

$50

150

50

b. If the price is $50, the firm will minimize its loss by producing 4 units. This would give

the firm a loss of $40. If the firm shuts down, it will earn a loss equal to its fixed cost

($100).

6. a. Figure 5 shows the typical firm in the industry, with average total cost

ATC

1, marginal

cost

MC

1, and price

P

1.

b. The new process reduces Hi-Tech’s marginal cost to

MC

2 and its average total cost to

ATC

2, but the price remains at

P

1 because other firms cannot use the new process. Thus

Hi-Tech earns positive profits.

Figure 5

7. Since the firm operates in a perfectly competitive market, its price is equal to its marginal

revenue of $10. This means that average revenue is also $10 and 50 units were sold.

258 ❖ Chapter 14/Firms in Competitive Markets

8. a. Profit is equal to (

P

–

ATC

) ×

Q

. Price is equal to

AR

. Therefore, profit is ($10 – $8) ×

100 = $200.

b. For firms in perfect competition, marginal revenue and average revenue are equal. Since

9. a. If firms are currently incurring losses, price must be less than average total cost.

However, because firms in the industry are currently producing output, price must be

greater than average variable cost. If firms are maximizing profits, price must be equal to

marginal cost.

b. The present situation is depicted in Figure 6. The firm is currently producing

q

1 units of

output at a price of

P

1.

c. Figure 6 also shows how the market will adjust in the long run. Because firms are

incurring losses, there will be exit in this industry. This means that the market supply

Chapter 14/Firms in Competitive Markets ❖ 259

10. a. The table below shows

TC

and

ATC

for a typical firm:

Q

TC

ATC

1

11

11

2

15

7.5

3

21

7

4

29

7.25

5

39

7.8

6

51

8.5

b. At a price of $11, quantity demanded is 200. Since marginal revenue is $11, each firm

will choose to produce 5 pies. Therefore, there will be 40 firms (= 200/5). Each producer

will earn total revenue of $55 ($11 5), total cost is $39, so profit is $16.

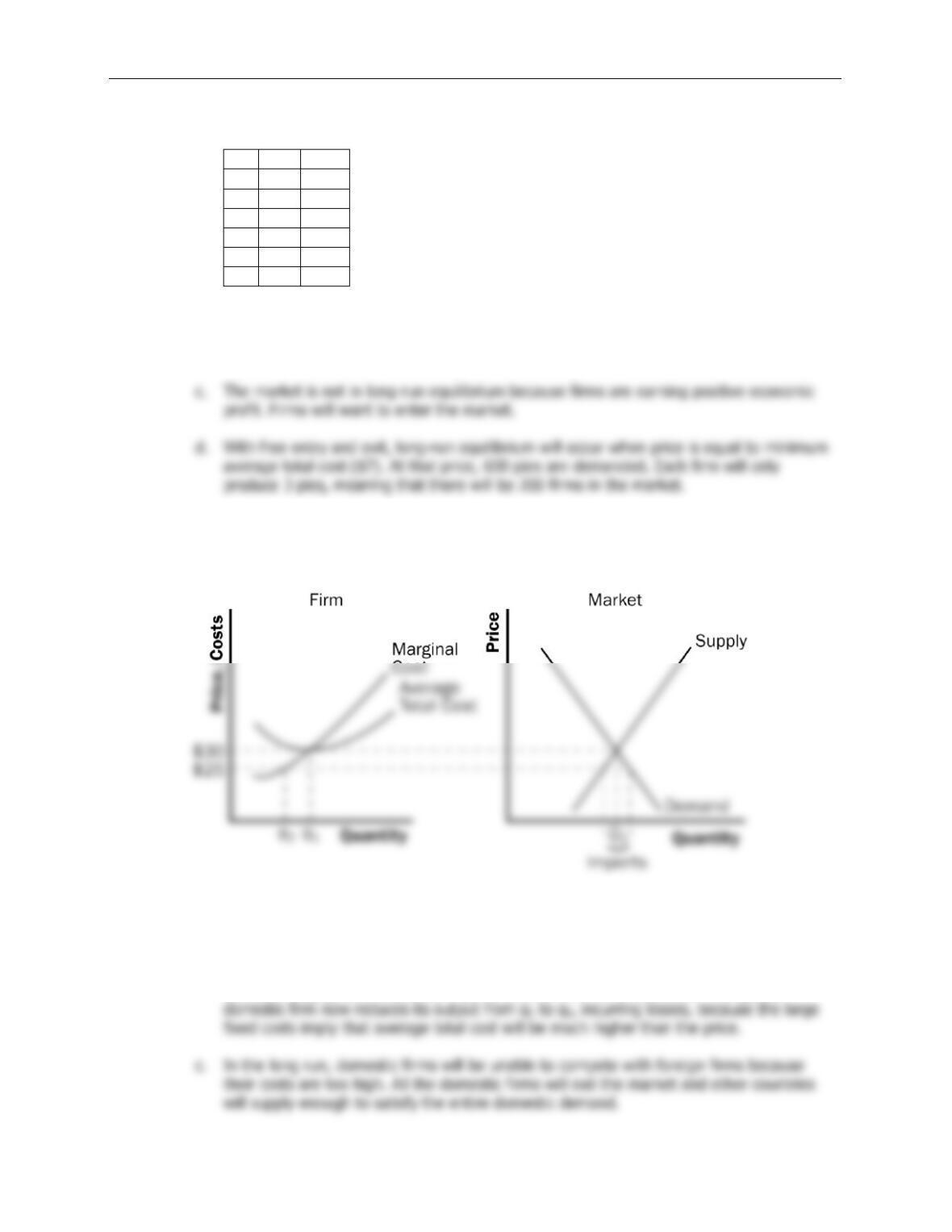

11. a. Figure 7 illustrates the situation in the U.S. textile market. With no international trade,

the market is in long-run equilibrium. Supply intersects demand at quantity

Q

1 and price

$30, with a typical firm producing output

q

1.

Figure 7

b. The effect of imports at $25 is that the market supply curve follows the old supply curve

up to a price of $25, then becomes horizontal at that price. As a result, demand exceeds

domestic supply, so the country imports textiles from other countries. The typical

260 ❖ Chapter 14/Firms in Competitive Markets

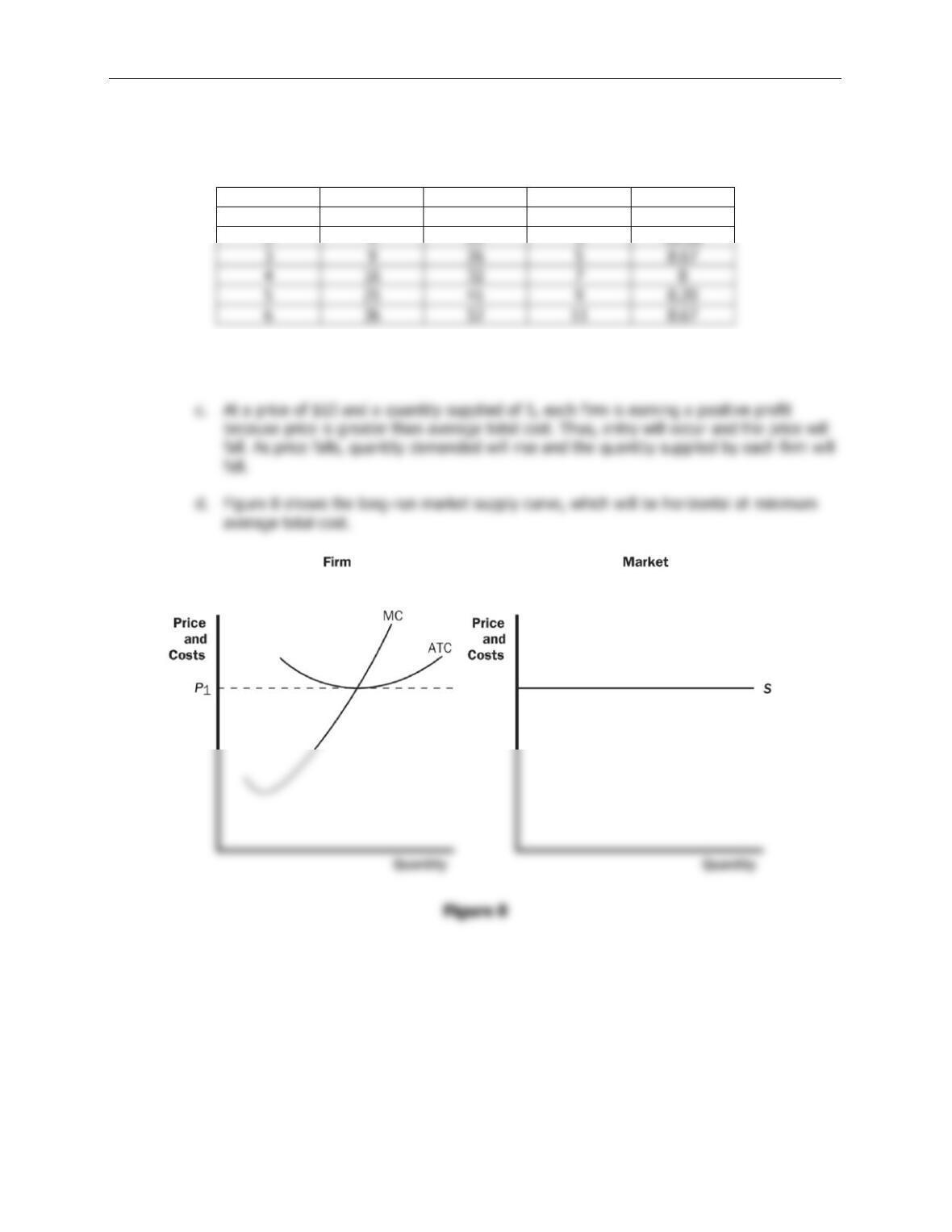

12. a. The firms' variable cost (

VC

), total cost (

TC

), marginal cost (

MC

), and average total cost

(

ATC

) are shown in the table below:

Quantity

VC

TC

MC

ATC

1

1

17

1

17

b. If the price is $10, each firm will produce 5 units, so there will be 5 100 = 500 units

supplied in the market.

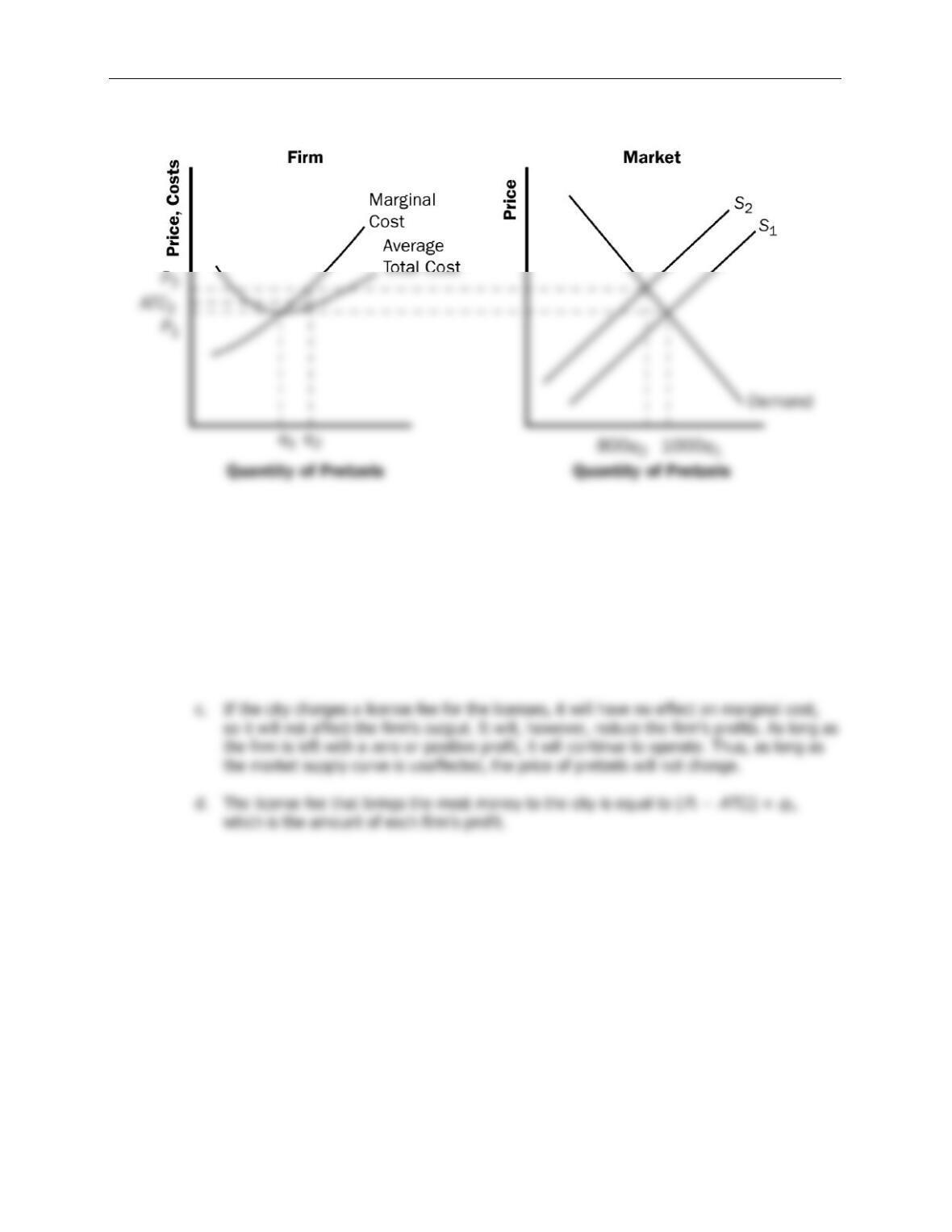

13. a. Figure 9 shows the current equilibrium in the market for pretzels. The supply curve,

S

1,

intersects the demand curve at price

P

1. Each stand produces quantity

q

1 of pretzels, so

the total number of pretzels produced is 1,000 ×

q

1. Stands earn zero profit, because

price is equal to average total cost.

Chapter 14/Firms in Competitive Markets ❖ 261

Figure 9

b. If the city government restricts the number of pretzel stands to 800, the market supply

curve shifts to

S

2. The market price rises to

P

2, and individual firms produce output

q

2.

Market output is now 800 ×

q

2. Now the price exceeds average total cost, so each firm is

making a positive profit. Without restrictions on the market, this would induce other firms

to enter the market, but they cannot because the government has limited the number of

licenses.