E14-19 Computing operating activities cash flow—indirect method

Learning Objective 2

Net Cash Prov. by Op. Act. $17,000

The records of Paramount Color Engraving reveal the following:

Compute cash flows from operating activities by the indirect method for year ended December 31, 2016.

SOLUTION

PARAMOUNT COLOR ENGRAVING

Statement of Cash Flows—Partial

Year Ended December 31, 2016

Cash Flows from Operating Activities:

Net Income

Net Cash Provided by Operating Activities

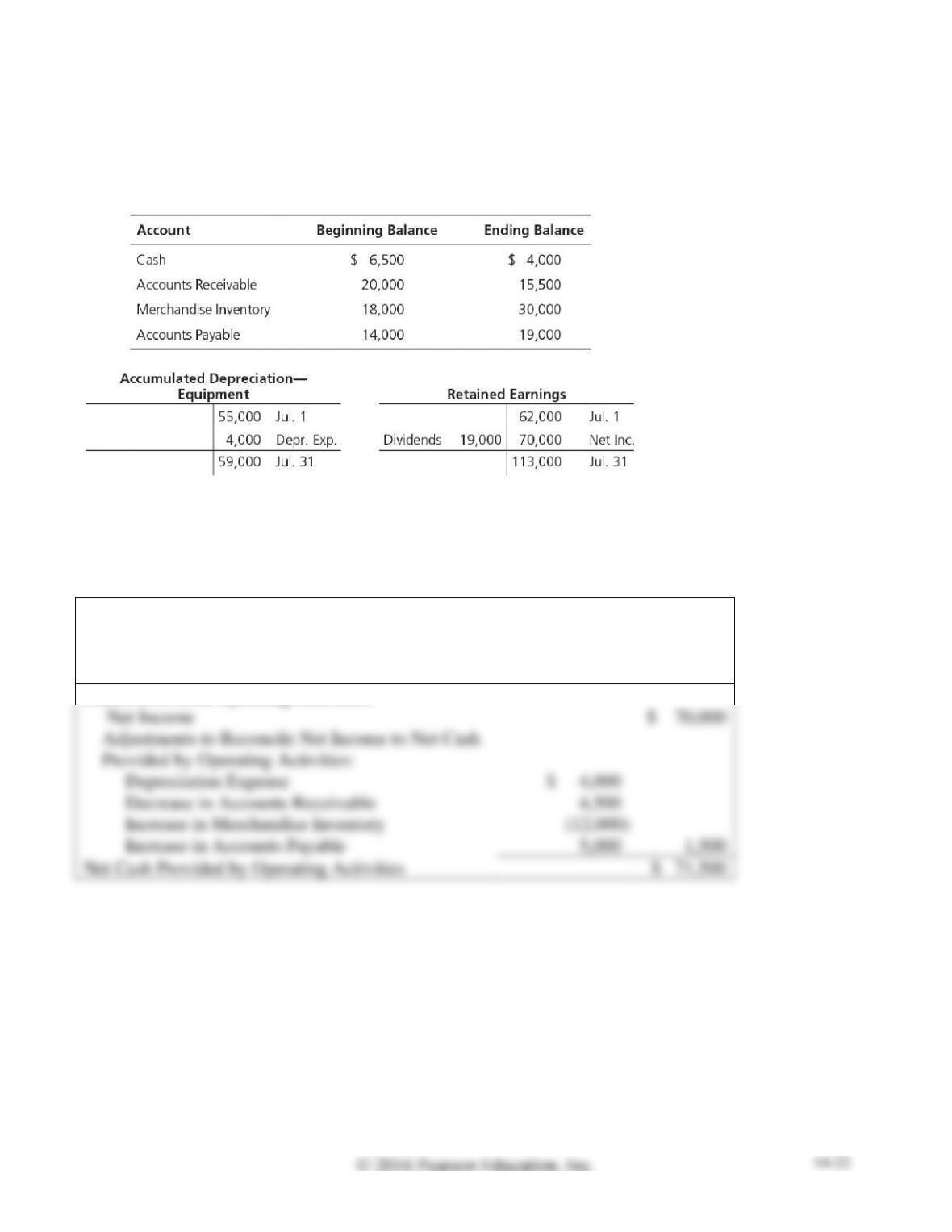

E14-20 Computing operating activities cash flow—indirect method

Learning Objective 2

Net Cash Prov. by Op. Act. $71,500

The accounting records of XYZ Sales, Inc. include the following accounts:

Compute XYZ’s net cash provided by (used for) operating activities during July 2016.

Use the indirect method.

SOLUTION

XYZ SALES, INC.

Statement of Cash Flows—Partial

For Month Ended July 31, 2016

Cash Flows from Operating Activities:

Net Income

Provided by Operating Activities:

(12,000)

Net Cash Provided by Operating Activities

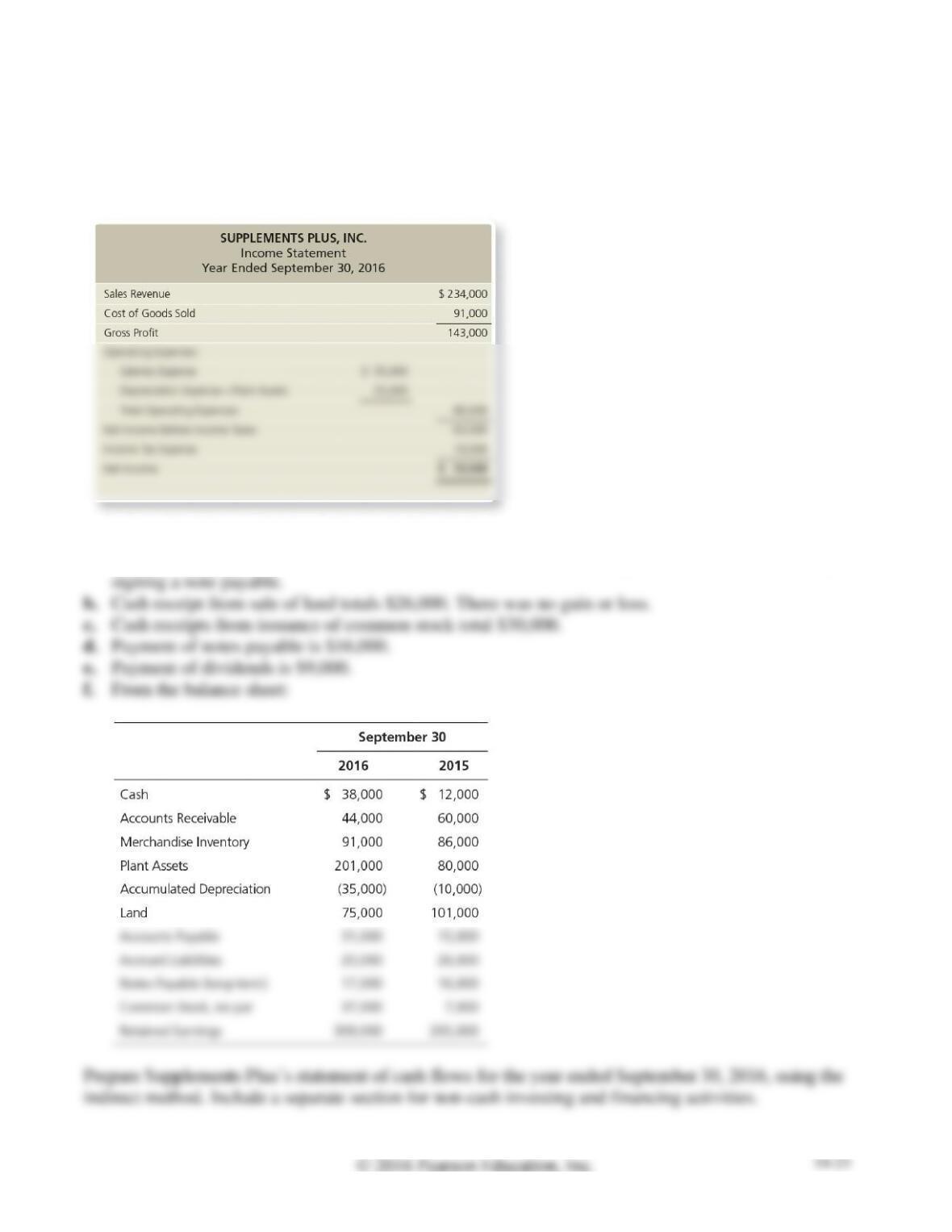

E14-21 Preparing the statement of cash flows—indirect method

Learning Objective 2

Net Cash Prov. by Op. Act. $99,000

The income statement of Supplements Plus, Inc. follows:

Additional data follow:

a. Acquisition of plant assets is $121,000. Of this amount, $104,000 is paid in cash and $17,000 by

SOLUTION

SUPPLEMENTS PLUS, INC

Statement of Cash Flows

Year Ended September 30, 2016

Cash Flows from Operating Activities:

Net Income

$ 53,000

Provided by Operating Activities:

(6,000)

46,000

Net Cash Provided by Operating Activities

99,000

Cash Flows from Investing Activities:

Acquisition of Plant Asset

Net Cash Used for Investing Activities

Cash Flows from Financing Activities:

Cash Receipt from Issuance of Common Stock

Cash Payment of Notes Payable

(16,000)

(9,000)

Net Cash Provided by Financing Activities

Net Increase (Decrease) in Cash

Cash Balance, September 30, 2015

Cash Balance, September 30, 2016

Non-cash Investing and Financing Activities:

Acquisition of Plant Assets with Notes Payable

Total Non-cash Investing and Financing Activities

E14-22 Computing cash flows for investing and financing activities

Learning Objective 2

2. Book Value on Plant Assets Sold $10,000

Consider the following facts for Vanilla Valley:

a. Beginning and ending Retained Earnings are $43,000 and $69,000, respectively. Net income for the

period is $58,000.

Requirements

1. How much are cash dividends?

2. What was the amount of the cash receipt from the sale of plant assets?

SOLUTION

Requirement 1

Retained Earnings (let Dividends = X)

Beginning

+

Net income

−

Dividends

=

Ending

$43,000

+

$58,000

−

X

=

$69,000

X

=

$32,000

Beginning

Net Income

Dividend

Ending

Requirement 2

Plant Assets (let X = Cost of Assets Sold)

Beginning

+

Acquisitions

−

Sold

=

Ending

$120,600

+

$27,000

−

X

=

$126,600

X

=

$ 21,000

Beginning

120,600

Acquisitions

Ending

126,600

Beginning

Depreciation Expense

Ending

Total Cash Receipt for Sale of Plant Assets

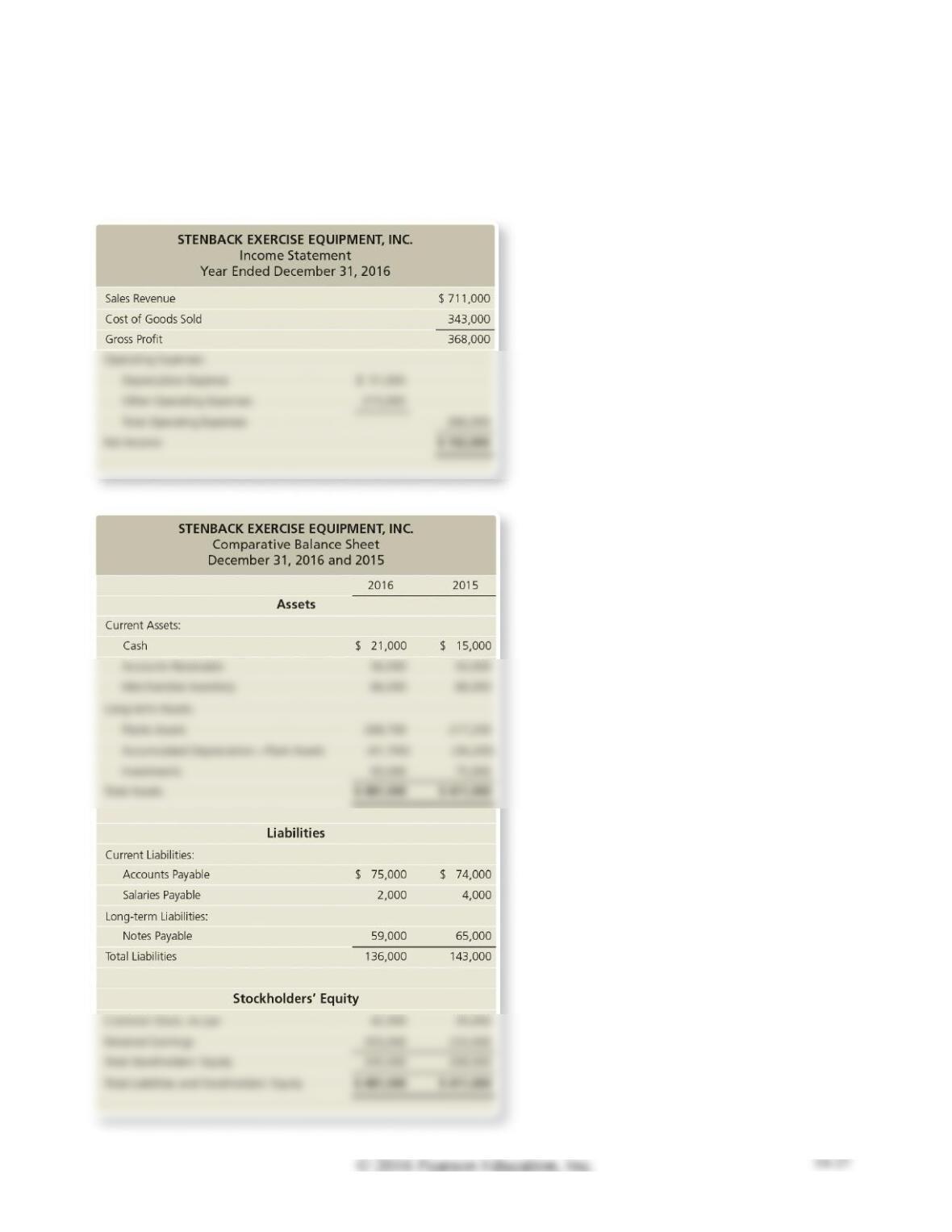

E14-23 Computing the cash effect

Learning Objective 2

2. Payment: $6,000

4. Dividends $32,000

Stenback Exercise Equipment, Inc. reported the following financial statements for 2016:

Requirements

1. Compute the amount of Stenback Exercise’s acquisition of plant assets. Assume the acquisition was

for cash. Stenback Exercise disposed of plant assets at book value. The cost and accumulated

depreciation of the disposed asset was $43,500. No cash was received upon disposal.

2. Compute new borrowing or payment of long-term notes payable, with Stenback Exercise having

only one long-term notes payable transaction during the year.

3. Compute the issuance of common stock with Stenback Exercise having only one common stock

transaction during the year.

4. Compute the payment of cash dividends.

SOLUTION

Requirement 1

12/31/2015

Acquisitions

Disposed of

12/31/2016

Accumulated Depreciation—Plant Assets

34,200

12/31/2015

51,000

Depreciation Expense

41,700

12/31/2016

Requirement 2

Notes Payable

65,000

12/31/2015

0

Issuance

Payment

6,000

59,000

12/31/2016

35,000

12/31/2015

Issuance

Retirement

42,000

12/31/2016

E14-23, cont.

Requirement 4

12/31/2015

Net Income

12/31/2016

Note: Exercise E14-23 must be completed before attempting Exercise E14-24.

E14-24 Preparing the statement of cash flows—indirect method

Learning Objective 2

Net Cash Prov. by Op. Act. $150,000

Use the Stenback Exercise Equipment data in Exercise E14-23. Prepare the company’s statement of cash

flows—indirect method—for the year ended December 31, 2016. Assume investments are purchased

with cash.

SOLUTION

STENBACK EXERCISE EQUIPMENT, INC.

Statement of Cash Flows

Year Ended December 31, 2016

Cash Flows from Operating Activities:

Net Income

$ 102,000

Provided by Operating Activities:

Net Cash Provided by Operating Activities

Cash Flows from Investing Activities:

Acquisition of Plant Asset

Net Cash Used for Investing Activities

Cash Flows from Financing Activities:

Cash Receipt from Issuance of Common Stock

Cash Payment of Notes Payable

Net Cash Used for Financing Activities

Net Increase (Decrease) in Cash

E14-25 Identifying and reporting non-cash transactions

Learning Objective 2

Total Non-cash Inv. and Fin. Act. $161,000

Motorcross, Inc. identified the following selected transactions that occurred during 2016:

a. Issued 850 shares of $5 par common stock for cash of $21,000.

b. Issued 5,600 shares of $5 par common stock for a building with a fair market value of $99,000.

c. Purchased new truck with a fair market value of $36,000. Financed it 100% with a long-term note.

d. Retired short-term notes of $26,000 by issuing 2,500 shares of $5 par common stock.

e. Paid long-term note of $8,500 to Bank of Tallahassee. Issued new long-term note of $17,000 to

Bank of Trust.

Identify any non-cash transactions that occurred during the year, and show how they would be reported

in the non-cash investing and financing activities section of the statement of cash flows.

SOLUTION

MOTOCROSS, INC.

Statement of Cash Flows – Partial

Year Ended December 31, 2016

Non-cash Investing and Financing Activities:

Acquisition of a Building by issuing Common Stock

Acquisition of a Truck by issuing a Long-Term Note

Retirement of Short-term Note by issuing Common Stock

Total Non-cash Investing and Financing Activities

E14-26 Analyzing free cash flow

Learning Objective 3

Use the Stenback Exercise Equipment data in Exercises E14-23 and E14-24. Stenback plans to purchase

a truck for $31,000 and a forklift for $120,000 next year. In addition, it plans to pay cash dividends of

$1,000. Assuming Stenback plans similar activity for 2017, what would be the amount of free cash

flow?

SOLUTION

Net Cash provided by Operating Activities

$ 150,000

= Free Cash Flow

E14A-27 Preparing operating activities cash flow—direct method

Learning Objective 4

Appendix 14A

The accounting records of Grand Auto Parts reveal the following:

Compute cash flows from operating activities using the direct method for the year ended December 31,

2016.

SOLUTION

GRAND AUTO PARTS

Statement of Cash Flows—Partial

Year Ended December 31, 2016

Cash Flows from Operating Activities:

Receipts:

Collections from Customers

Payments:

Net Cash Provided by Operating Activities

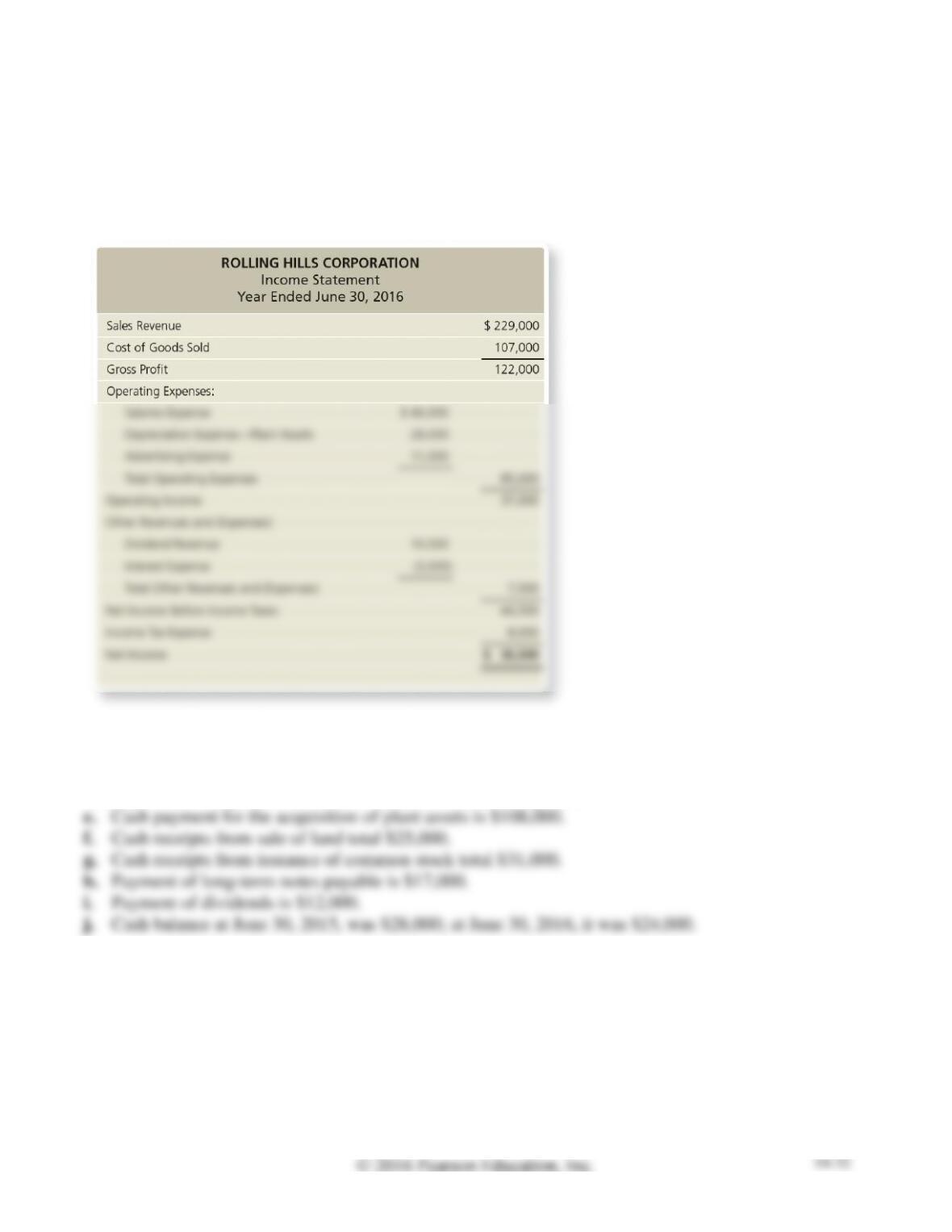

E14A-28 Preparing the statement of cash flows—direct method

Learning Objective 4

Appendix 14A

Net Cash Prov. by Op. Act. $77,000

The income statement and additional data of Rolling Hills Corporation follow:

a. Collections from customers are $14,000 more than sales.

b. Dividend revenue, interest expense, and income tax expense equal their cash amounts.

c. Payments to suppliers are the sum of cost of goods sold plus advertising expense.

d. Payments to employees are $1,500 more than salaries expense.

Prepare Rolling Hills Corporation’s statement of cash flows for the year ended June 30,

2016. Use the direct method.

SOLUTION

ROLLING HILLS CORPORATION

Statement of Cash Flows

Year Ended June 30, 2016

Cash Flows from Operating Activities:

Receipts:

Collections from Customers

Payments:

Net Cash Provided by Operating Activities

Cash Flows from Investing Activities:

Net Cash Used for Investing Activities

Cash Flows from Financing Activities:

Net Cash Provided by Financing Activities

Net Increase (Decrease) in Cash

Cash Balance, June 30, 2015

Cash Balance, June 30, 2016

$ 24,000

E14A-29 Computing cash flow items—direct method

Learning Objective 4

Appendix 14A

1. Cash Receipts from Cust. $66,000

Consider the following facts:

a. Beginning and ending Accounts Receivable are $25,000 and $27,000, respectively. Credit sales for

Requirements

1. Compute cash collections from customers.

2. Compute cash payments for merchandise inventory.

SOLUTION

Requirement 1

Sales Revenue

$ 68,000

Cost of Goods Sold

+Ending Merchandise Inventory

E14A-30 Computing cash flow items—direct method

Learning Objective 4

Appendix 14A

2. Cash Paid for Merchandise Inventory $18,482

7. Dividends $213

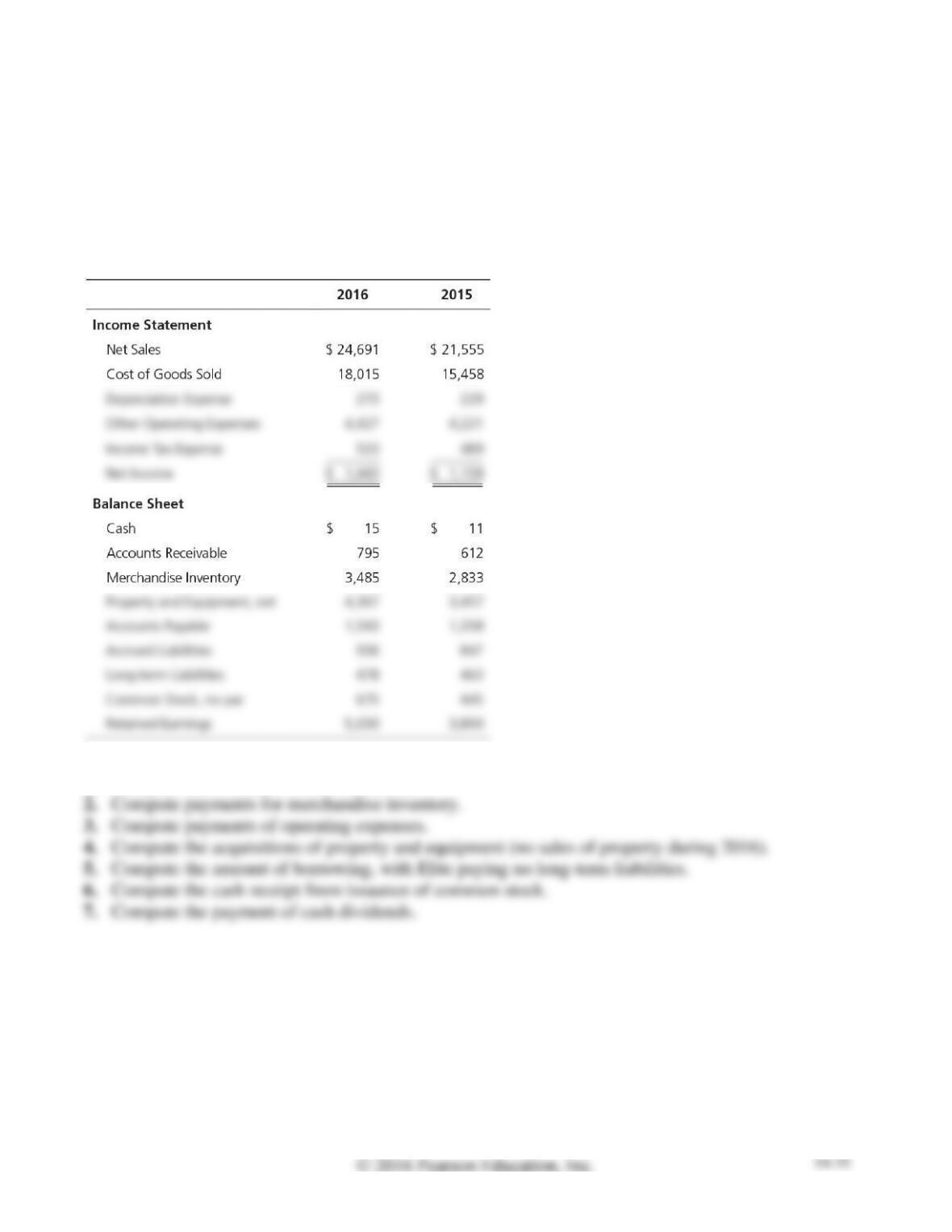

Elite Mobile Homes reported the following in its financial statements for the year ended December 31,

2016:

Requirements

1. Compute the collections from customers.

SOLUTION

Requirement 1

Sales Revenue

$ 24,691

+ Beginning Accounts Receivable

= Cash receipts from customers

Requirement 2

Cost of Goods Sold

$ 18,015

+ Ending Merchandise Inventory

+ Beginning Accounts Payable

Cash paid for Merchandise Inventory

Requirement 3

Operating Expenses

$ 4,427

+ Beginning Accrued Liabilities

= Cash receipts from customers

E14A-30, cont.

Requirement 4

Property and Equipment, net

12/31/2015

3,457

Acquisitions

1,183

273

Depreciation

12/31/2016

4,367

Requirement 5

463

12/31/2015

Issuance

Payment

0

478

12/31/2016

Requirement 6

Common Stock

445

12/31/2015

230

Issuance

Retirement

0

675

12/31/2016

Requirement 7

12/31/2015

Net Income

Dividend

12/31/2016

E14B-31 Using a spreadsheet to prepare the statement of cash flows—indirect method

Learning Objective 5

Appendix 14B

Use the Supplements Plus, Inc. data in Exercise E14-21 to prepare the spreadsheet for the 2016

statement of cash flows. Format cash flows from operating activities by the indirect method.

SOLUTION

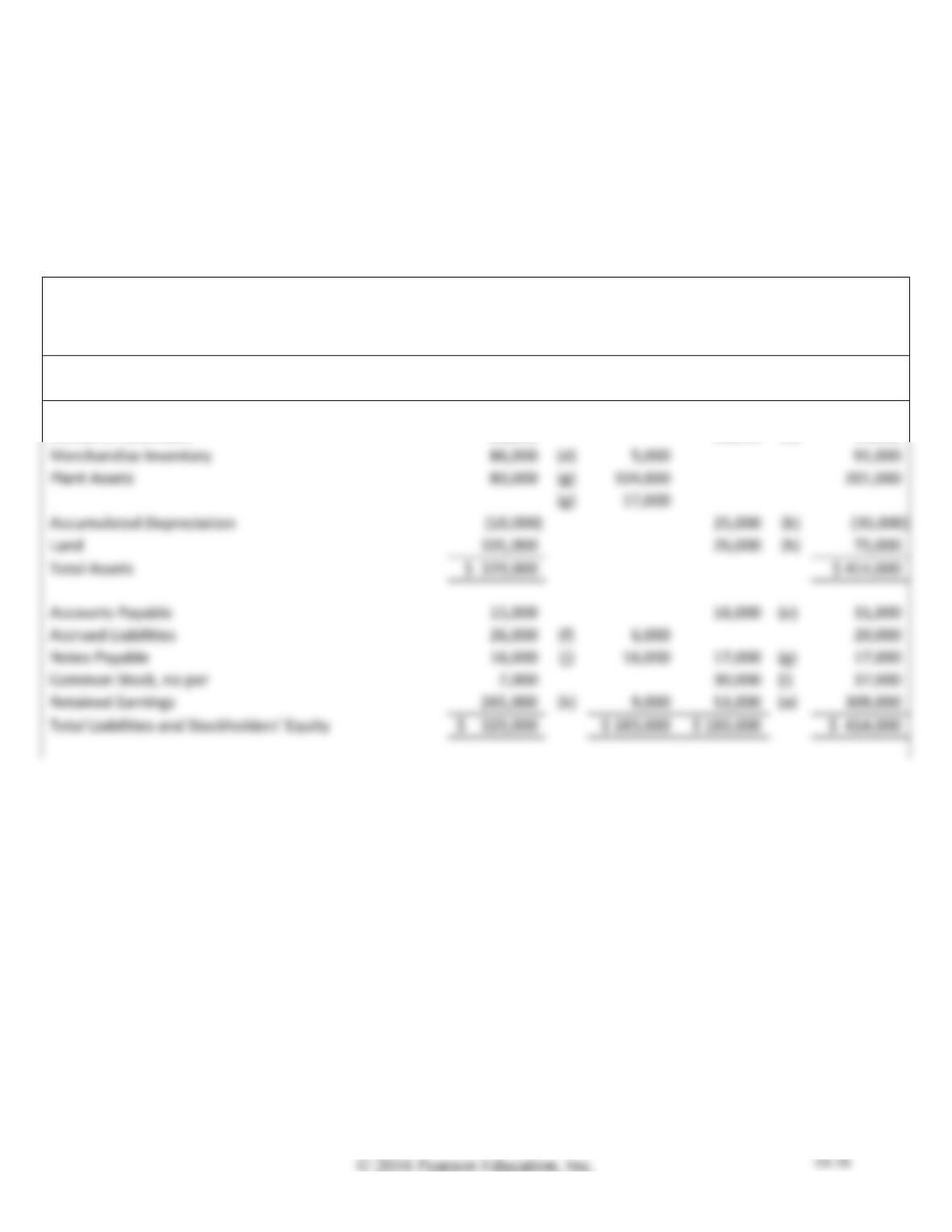

SUPPLEMENTS PLUS, INC.

Statement of Cash Flows

Year Ended September 30, 2016

Transaction Analysis

Panel A – Balance Sheet:

9/30/2015

DEBIT

CREDIT

9/30/2016

Cash

$ 12,000

(l)

26,000

$ 38,000

Accounts Receivable

60,000

16,000

(c)

44,000

Merchandise Inventory

86,000

91,000

Plant Assets

80,000

17,000

Accumulated Depreciation

25,000

26,000

75,000

Accounts Payable

15,000

16,000

31,000

Accrued Liabilities

26,000

20,000

Notes Payable

16,000

16,000

17,000

17,000

Common Stock, no par

37,000

Retained Earnings

53,000

E14B-31, cont.

Panel B – Statement of Cash Flows:

Cash Flows from Operating Activities:

Net Income

(a)

53,000

Depreciation Expense

(b)

25,000

Decrease in Accounts Receivable

(c)

16,000

Increase in Merchandise Inventory

(d)

Increase in Accounts Payable

(e)

16,000

Decrease in Accrued Liabilities

(f)

Net Cash Provided by Operating Activities

Cash Flows from Investing Activities:

Cash Receipt from Sale of Land

(h)

26,000

Cash Payment for Acquisition of Plant Assets

104,000

(g)

Net Cash Used for Investing Activities

Cash Flows from Financing Activities:

Cash Receipt from Issuance of Common Stock

(i)

30,000

Cash Payments of Notes Payable

16,000

(j)

Cash Payment of Dividends

Net Cash Provided by Financing Activities

Net Increase (Decrease) in Cash

26,000

(l)

Non-cash Investing and Financing Activities:

17,000

(g)

Total Non-cash Investing and Financing Activities

(g)

17,000

Problems (Group A)

P14-32A Identifying the purpose and preparing the statement of cash flows— indirect method

Learning Objectives 1, 2

2. Net Income $67,700

4. Net Cash Used by Op. Act. $(61,250)

Official Reserve Rare Coins (ORRC) was formed on January 1, 2016. Additional data for the year

follow:

a. On January 1, 2016, ORRC issued no par common stock for $500,000.

b. Early in January, ORRC made the following cash payments:

1. For store fixtures, $54,000

2. For merchandise inventory, $270,000

3. For rent expense on a store building, $11,000

c. Later in the year, ORRC purchased merchandise inventory on account for $244,000. Before year-

end, ORRC paid $144,000 of this accounts payable.

Requirements

1. What is the purpose of the statement of cash flows?

2. Prepare ORRC’s income statement for the year ended December 31, 2016. Use the single-step

format, with all revenues listed together and all expenses listed together.