Chapter 14

Statement of Cash Flows

Review Questions

1. What does the statement of cash flows report?

The statement of cash flows reports on a business’s cash receipts and cash payments for a specific

period.

2. How does the statement of cash flows help users of financial statements?

The statement of cash flows helps users do the following:

3. Describe the three basic types of cash flow activities.

The three basic types of cash flow activities are: operating, investing, and financing. Operating

4. What types of transactions are reported in the non-cash investing and financing activities section of

the statement of cash flows?

Investing and financing transactions that do not involve cash are called non-cash investing and

5. Describe the two formats for reporting operating activities on the statement of cash flows.

The two formats for reporting the operating activities section are the indirect and direct methods.

6. Describe the five steps used to prepare the statement of cash flows by the indirect method.

The five steps used to prepare the statement of cash flows by the indirect method are:

• STEP 2: Complete the cash flows from investing activities section by reviewing the long-term

assets section of the balance sheet.

7. Explain why depreciation expense, depletion expense, and amortization expense are added to net

income in the operating activities section of the statement of cash flows when using the indirect

method.

Depreciation expense, depletion expense, and amortization expense all impact the income statement

8. If a company experienced a loss on disposal of long-term assets, how would this be reported in the

operating activities section of the statement of cash flows when using the indirect method? Why?

9. If current assets other than cash increase, what is the effect on cash? What about a decrease in

current assets other than cash?

An increase in a current asset other than cash causes a decrease in cash. A decrease in a current asset

other than cash causes an increase in cash.

10. If current liabilities increase, what is the effect on cash? What about a decrease in current liabilities?

11. What accounts on the balance sheet must be evaluated when completing the investing activities

section of the statement of cash flows?

12. What accounts on the balance sheet must be evaluated when completing the financing activities

section of the statement of cash flows?

The long-term liability accounts and the equity accounts must be evaluated when completing the

financing activities section of the statement of cash flows.

13. What should the net change in cash section of the statement of cash flows always reconcile with?

14. What is free cash flow, and how is it calculated?

Free cash flow is the amount of cash available from operating activities after paying for planned

15A. How does the direct method differ from the indirect method when preparing the operating

activities section of the statement of cash flows?

In the indirect method, start with net income and then adjust it to cash basis through a series of

16B. Why might a spreadsheet be helpful when completing the statement of cash flows?

Companies face complex situations, and a spreadsheet can help in preparing the cash flow

Short Exercises

S14-1 Describing the purposes of the statement of cash flows

Learning Objective 1

Financial statements all have a goal. The statement of cash flows does as well. Describe how the

statement of cash flows helps investors and creditors perform each of the following functions:

a. Predict future cash flows.

b. Evaluate management decisions.

c. Predict the ability to make debt payments to lenders and pay dividends to stockholders.

SOLUTION

a.

The statement of cash flows helps evaluate management decisions by reporting on

The statement of cash flows helps predict future cash flows by reporting past cash

S14-2 Classifying items on the statement of cash flows

Learning Objective 1

Cash flow items must be categorized into one of four categories. Identify each item as operating (O),

investing (I), financing (F), or non-cash (N).

a. Cash purchase of merchandise inventory

b. Cash payment of dividends

c. Cash receipt from the collection of long-term notes receivable

d. Cash payment for income taxes

e. Purchase of equipment in exchange for notes payable

f. Cash receipt from the sale of land

g. Cash received from borrowing money

h. Cash receipt for interest income

i. Cash receipt from the issuance of common stock

j. Cash payment of salaries

SOLUTION

a.

Operating

f.

Investing

c.

Investing

h.

Operating

d.

Operating

Financing

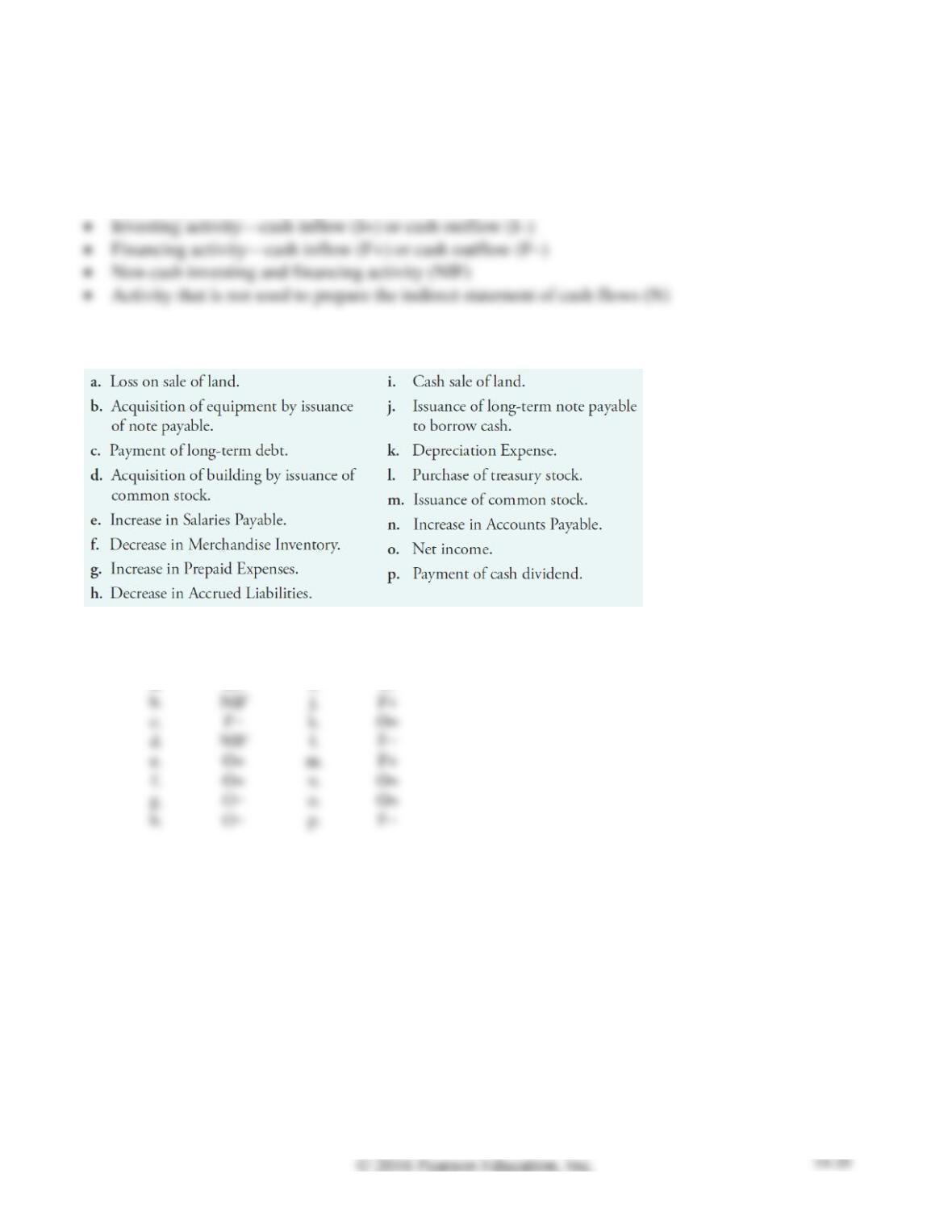

S14-3 Classifying items on the indirect statement of cash flows

Learning Objective 2

Destiny Corporation is preparing its statement of cash flows by the indirect method. Destiny has the

following items for you to consider in preparing the statement:

Identify each item as a(n):

• Operating activity—addition to net income (O+) or subtraction from net income (O–)

• Investing activity—cash inflow (I+) or cash outflow (I–)

• Financing activity—cash inflow (F+) or cash outflow (F–)

• Activity that is not used to prepare the indirect statement of cash flows (N)

SOLUTION

a.

O+

f.

O+

b.

g.

O+

d.

O+

S14-4 Computing cash flows from operating activities—indirect method

Learning Objective 2

GDM Equipment, Inc. reported the following data for 2016:

Compute GDM’s net cash provided by operating activities—indirect method.

SOLUTION

GDM EQUIPMENT, INC.

Statement of Cash Flows—Partial

Year Ended December 31, 2016

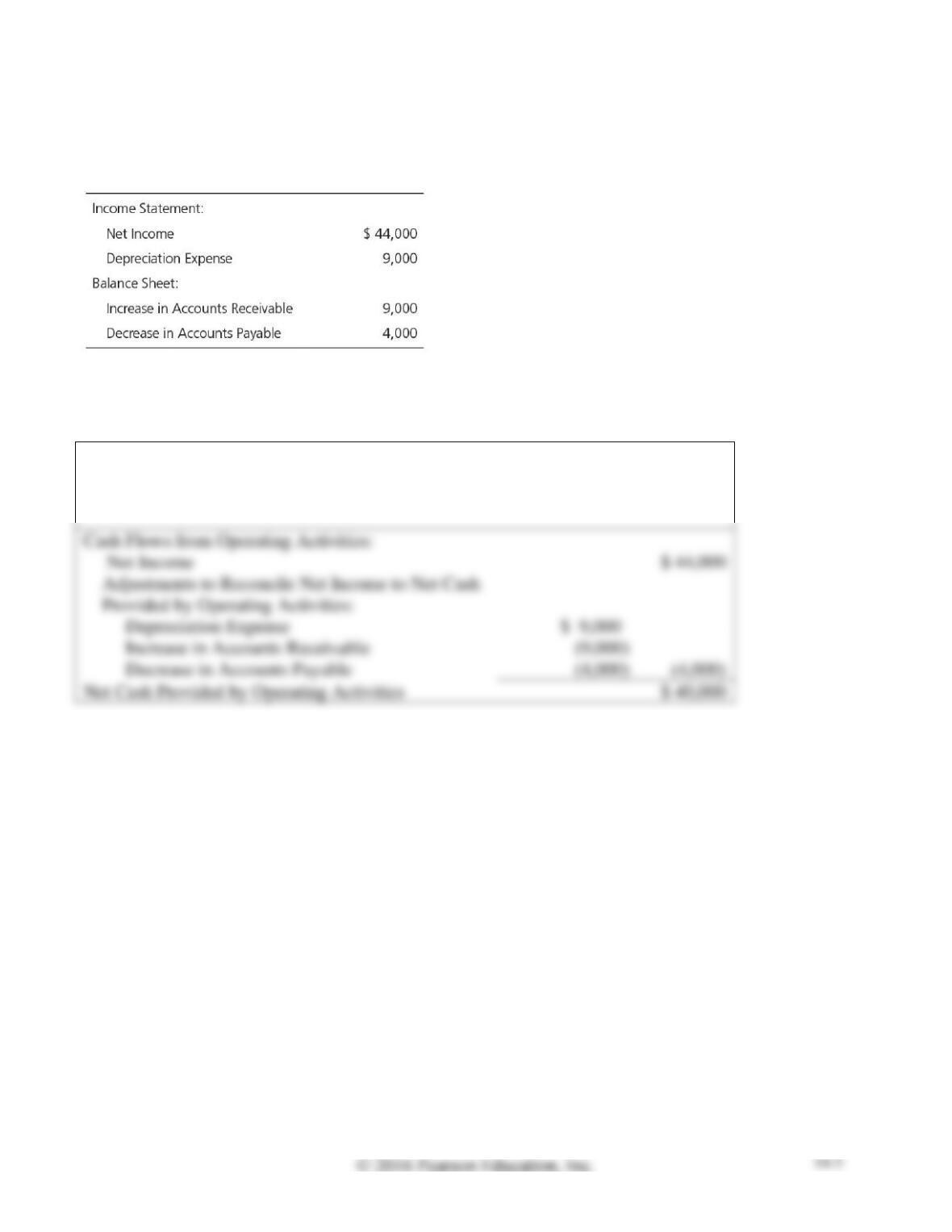

S14-5 Computing cash flows from operating activities—indirect method

Learning Objective 2

Smart Cellular accountants have assembled the following data for the year ended April 30, 2016:

Prepare the operating activities section using the indirect method for Smart Cellular’s statement of cash

flows for the year ended April 30, 2016.

SOLUTION

SMART CELLULAR

Statement of Cash Flows—Partial

Year Ended April 30, 2016

Cash Flows from Operating Activities:

Net Income

Provided by Operating Activities:

Net Cash Provided by Operating Activities

Note: Short Exercise S14-5 must be completed before attempting Short Exercise S14-6.

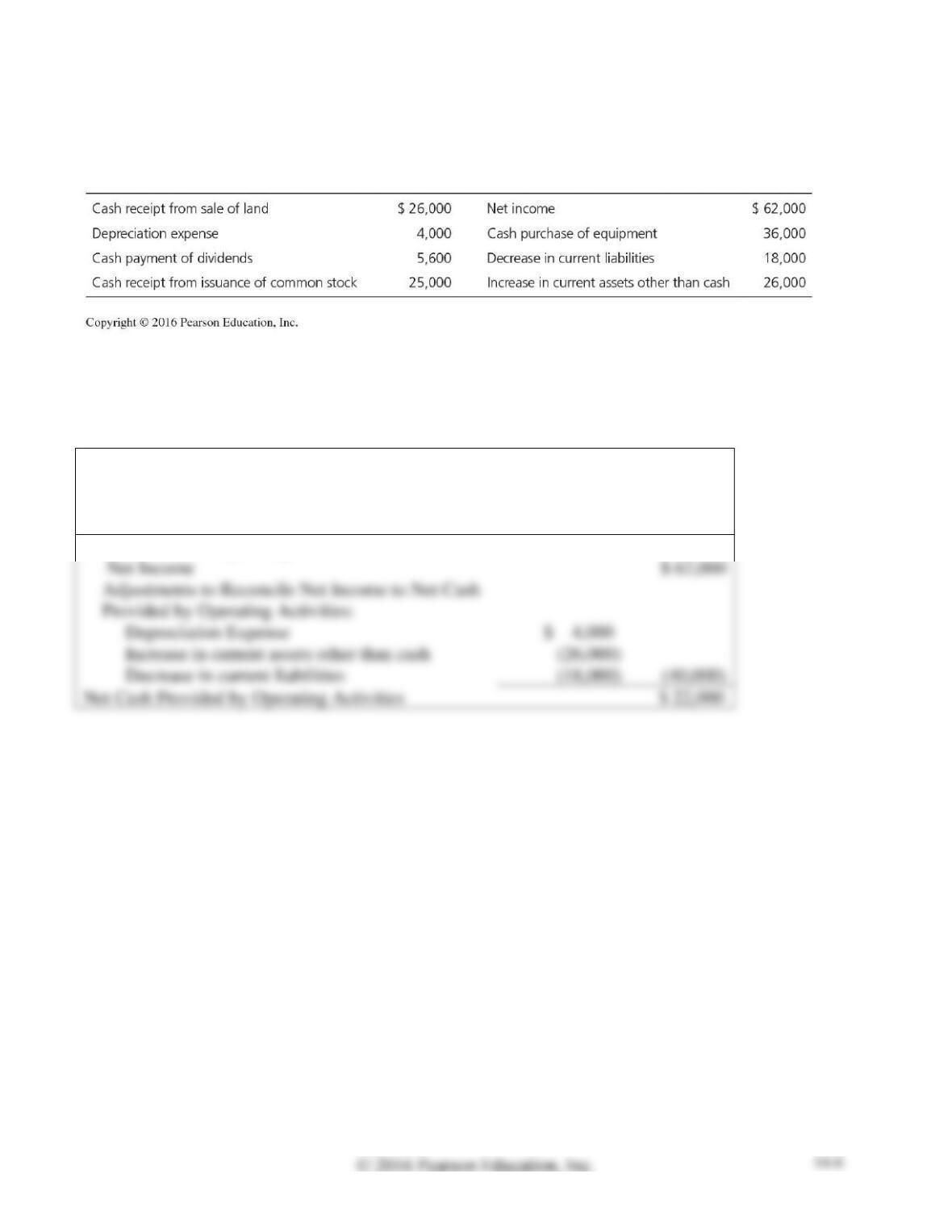

S14-6 Computing cash flows from investing and financing activities

Learning Objective 2

Use the data in Short Exercise S14-5 to complete this exercise. Prepare Smart Cellular’s statement of

cash flows using the indirect method for the year ended April 30, 2016. Assume beginning and ending

Cash are $23,300 and $54,700, respectively.

SOLUTION

SMART CELLULAR

Statement of Cash Flows

Year Ended April 30, 2016

Cash Flows from Operating Activities:

Net Income

$ 62,000

Provided by Operating Activities:

Net Cash Provided by Operating Activities

Cash Flows from Investing Activities:

Net Cash Used for Investing Activities

Cash Flows from Financing Activities:

Cash Receipt from Issuance of Common Stock

Net Cash Provided by Financing Activities

Net Increase (Decrease) in Cash

Cash Balance, April 30, 2015

Cash Balance, April 30, 2016

S14-7 Computing investing and financing cash flows

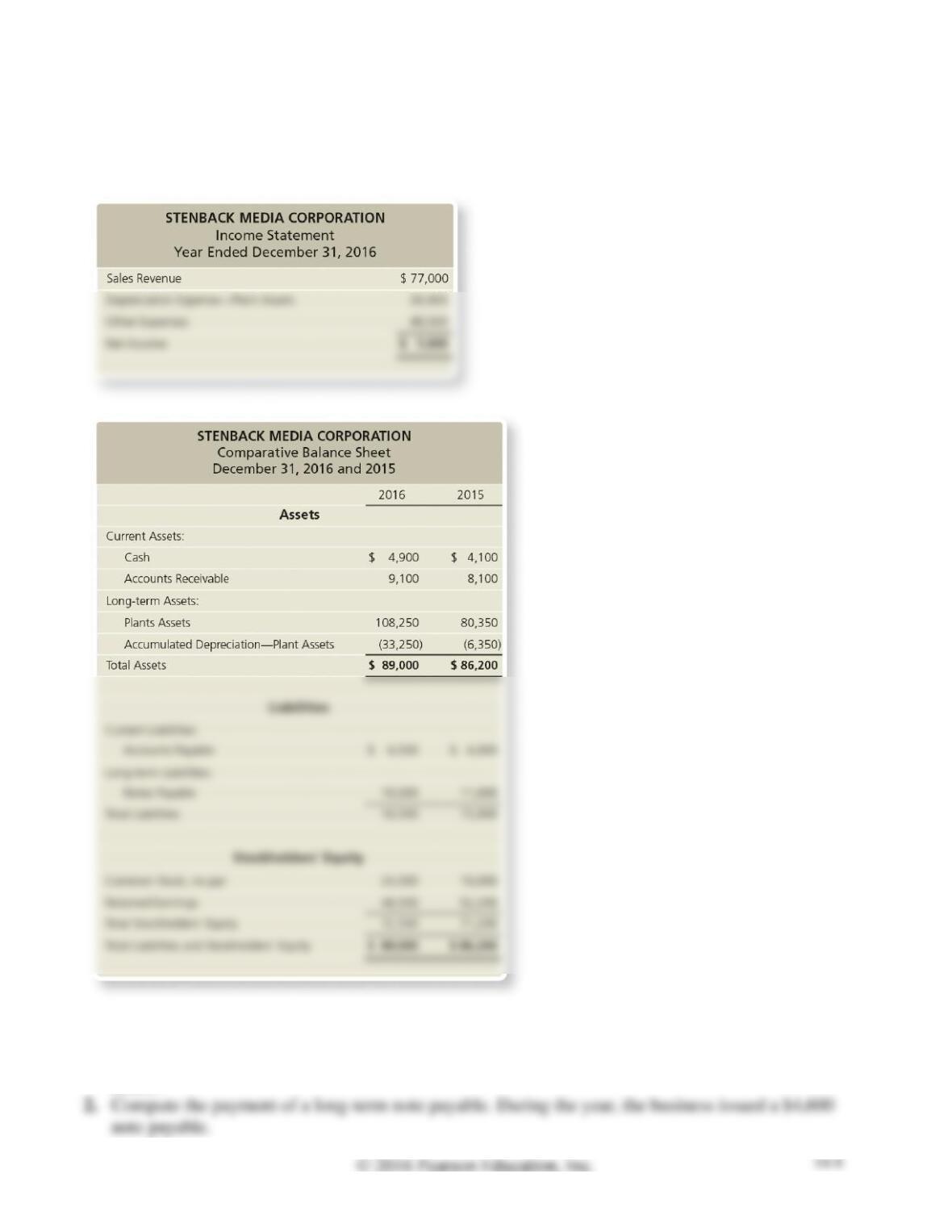

Learning Objective 2

Stenback Media Corporation had the following income statement and balance sheet for 2016:

Requirements

1. Compute the acquisition of plant assets for Stenback Media Corporation during 2016. The business

sold no plant assets during the year. Assume the company paid cash for the acquisition of plant

assets.

SOLUTION

Requirement 1

Note: Short Exercise S14-7 must be completed before attempting Short Exercise S14-8.

S14-8 Preparing the statement of cash flows—indirect method

Learning Objective 2

Use the Stenback Media Corporation data in Short Exercise S14-7 and the results you calculated from

the requirements. Prepare Stenbeck Media’s statement of cash flows— indirect method—for the year

ended December 31, 2016.

SOLUTION

STENBACK MEDIA CORPORATION

Statement of Cash Flows

Year Ended December 31, 2016

Cash Flows from Operating Activities:

Net Income

$ 1,600

Provided by Operating Activities:

Net Cash Provided by Operating Activities

30,000

Cash Flows from Investing Activities:

Net Cash Used for Investing Activities

Cash Flows from Financing Activities:

Cash Receipt from Issuance of Common Stock

Cash Receipt from Issuance of Notes Payable

(5,300)

Net Cash Used for Financing Activities

Net Increase (Decrease) in Cash

Cash Balance, December 31, 2015

Cash Balance, December 31, 2016

S14-8, cont.

Common Stock

19,000

12/31/2015

Retirement

0

5,000

Issuance

24,000

12/31/2016

Retained earnings (let Dividends = X)

Beginning

+

Net Income

−

Dividends

=

Ending

$52,200

+

$1,600

−

X

=

$48,500

X = $ 5,300

Retained Earnings

52,200

12/31/2015

1,600

Net Income

Dividend

5,300

48,500

12/31/2016

S14-9 Computing the change in cash; identifying non-cash transactions

Learning Objective 2

Brianna’s Wedding Shops earned net income of $25,000, which included depreciation of

$16,000. Brianna’s acquired a $116,000 building by borrowing $116,000 on a long-term note payable.

Requirements

1. How much did Brianna’s cash balance increase or decrease during the year?

2. Were there any non-cash transactions for the company? If so, show how they would be reported in

the statement of cash flows.

SOLUTION

Requirement 1

S14-10 Computing free cash flow

Learning Objective 3

Shauna Lopez Company expects the following for 2016:

• Net cash provided by operating activities of $144,000.

• Net cash provided by financing activities of $60,000.

• Net cash used for investing activities of $84,000 (no sales of long-term assets).

• Cash dividends paid to stockholders of $10,000.

How much free cash flow does Lopez expect for 2016?

SOLUTION

Net Cash provided by Operating Activities

$ 144,000

= Free Cash Flow

$ 50,000

S14A-11 Preparing a statement of cash flows using the direct method

Learning Objective 4

Appendix 14A

Green Bean, Inc. began 2016 with cash of $57,000. During the year, Green Bean earned revenue of

$596,000 and collected $618,000 from customers. Expenses for the year totaled $433,000, of which

Green Bean paid $214,000 in cash to suppliers and $209,000 in cash to employees. Green Bean also

paid $146,000 to purchase equipment and a cash dividend of $56,000 to its stockholders during 2016.

Prepare the company’s statement of cash flows for the year ended December 31, 2016. Format operating

activities by the direct method.

SOLUTION

GREEN BEAN, INC

Statement of Cash Flows

Year Ended December 31, 2016

Cash Flows from Operating Activities:

Receipts:

Payments:

(209,000)

Net Cash Provided by Operating Activities

Cash Flows from Investing Activities:

Net Cash Used for Investing Activities

Cash Flows from Financing Activities:

Net Cash Used for Financing Activities

Net Increase (Decrease) in Cash

Cash Balance, December 31, 2015

Cash Balance, December 31, 2016

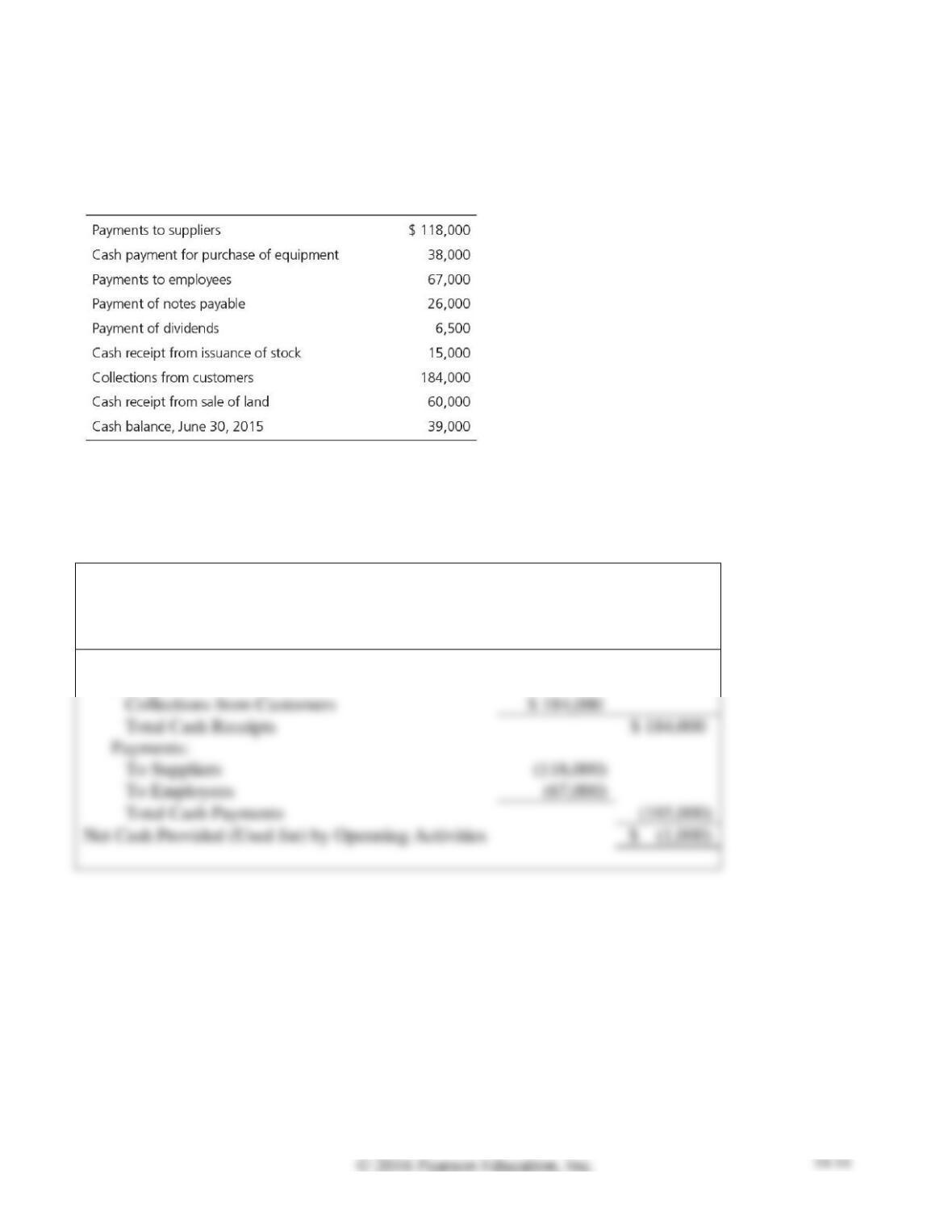

S14A-12 Preparing operating activities using the direct method

Learning Objective 4

Appendix 14A

Miss Ella’s Learning Center has assembled the following data for the year ended June 30, 2016:

Prepare the operating activities section of the business’s statement of cash flows for the year ended June

30, 2016, using the direct method.

SOLUTION

MISS ELLA’S LEARNING CENTER

Statement of Cash Flows—Partial

Year Ended June 30, 2016

Cash Flows from Operating Activities:

Receipts:

Payments:

Net Cash Provided (Used for) by Operating Activities

$ (1,000)

Note: Short Exercise S14A-12 must be completed before attempting Short Exercise S14A-13.

S14A-13 Preparing the direct method statement of cash flows

Learning Objective 4

Appendix 14A

Use the data in Short Exercise S14A-12 and your results. Prepare the business’s complete statement of

cash flows for the year ended June 30, 2016, using the direct method for operating activities.

SOLUTION

MISS ELLA’S LEARNING CENTER

Statement of Cash Flows

Year Ended June 30, 2016

Cash Flows from Operating Activities:

Receipts:

Payments:

Net Cash Provided (Used for) by Operating Activities

(1,000)

Cash Flows from Investing Activities:

Net Cash Provided by Investing Activities

Cash Flows from Financing Activities:

Net Cash Used for Financing Activities

Net Increase (Decrease) in Cash

Cash Balance, June 30, 2015

Cash Balance, June 30, 2016

S14A-14 Preparing the direct method statement of cash flows

Learning Objective 4

Appendix 14A

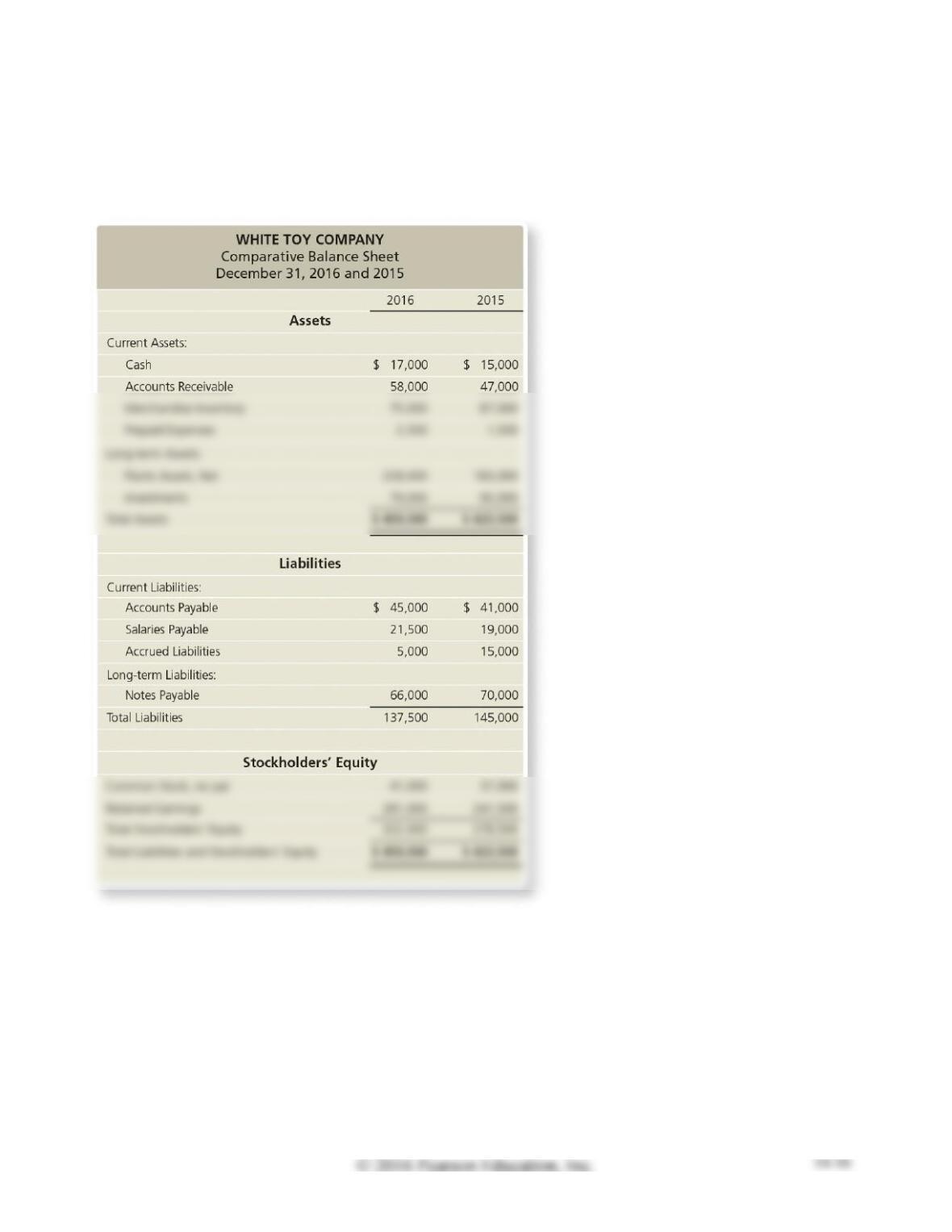

White Toy Company reported the following comparative balance sheet:

Requirements

1. Compute the collections from customers during 2016 for White Toy Company. Sales Revenue

totaled $136,000.

2. Compute the payments for inventory during 2016. Cost of Goods Sold was $80,000.

SOLUTION

Requirement 1

Sales Revenue

$ 136,000

+ Beginning Accounts Receivable

= Cash receipts from customers

Requirement 2

Cost of Goods Sold

$ 80,000

+ Ending Merchandise Inventory

+ Beginning Accounts Payable

Cash paid for merchandise inventory

$ 64,000

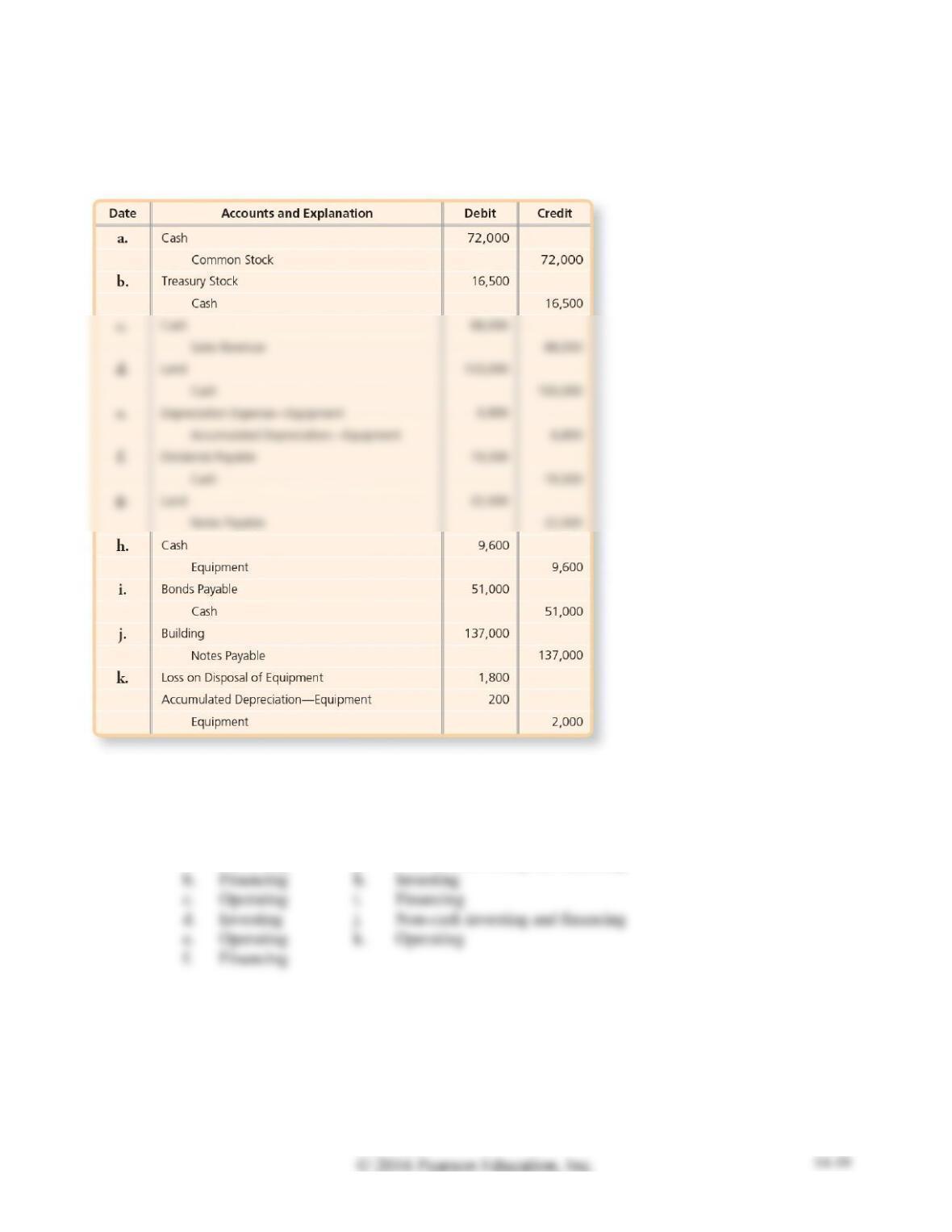

S14B-15 Using a spreadsheet to complete the statement of cash flows—indirect method

Learning Objective 5

Appendix 14B

Companies can use a spreadsheet to complete the statement of cash flows. Each item that follows is

recorded in the transaction analysis columns of the spreadsheet.

a. Net income

b. Increases in current assets (other than Cash)

c. Decreases in current liabilities

d. Cash payment for acquisition of plant assets

e. Cash receipt from issuance of common stock

f. Depreciation expense

Identify each as being recorded by a Debit or Credit in the statement of cash flows section of the

spreadsheet.

SOLUTION

a.

Debit

Credit

Debit

Exercises

E14-16 Classifying cash flow items

Learning Objective 1

Consider the following transactions:

a. Purchased equipment for $130,000 cash.

b. Issued $14 par preferred stock for cash.

c. Cash received from sales to customers of $35,000.

d. Cash paid to vendors, $17,000.

e. Sold building for $19,000 gain for cash.

f. Purchased treasury stock for $28,000.

g. Retired a notes payable with 1,250 shares of the company’s common stock.

Identify the category of the statement of cash flows in which each transaction would be reported.

SOLUTION

a.

Investing

e.

Investing & Operating (gain)

c.

Operating

g.

Non-cash investing and financing

E14-17 Classifying transactions on the statement of cash flows—indirect method

Learning Objective 1

Consider the following transactions:

Identify the category of the statement of cash flows in which each transaction would be reported.

SOLUTION

a.

Financing

g.

Non-cash investing and financing

b.

Financing

h.

Investing

d.

Investing

Non-cash investing and financing

E14-18 Classifying items on the indirect statement of cash flows

Learning Objectives 1, 2

The statement of cash flows categorizes like transactions for optimal reporting. Identify each item as

a(n):

• Operating activity—addition to net income (O+) or subtraction from net income (O–)

The indirect method is used to report cash flows from operating activities.

SOLUTION

a.

O+

i.

I+

c.

l.

O+