21

Table 14.9 illustrates the extent to which this delay in implementing the IPO affected valuation. Enterprise value can

be estimated by multiplying EBITDA by the enterprise to EBITDA multiple for similar firms. By using HCA’s 2010

Table 14.9 Increase in HCA Enterprise Value Due to Timing of IPO

Yearend 2009:

EBITDA1

Enterprise/EBITDA Multiple2

Enterprise Value

$ 5.63 billon

5.29 x

$ 29.78 billion

Yearend 2010:

EBITDA1

Enterprise/EBITDA Multiple3

Enterprise Value

$ 5.63 billion

7.99 x

$ 44.98

Increase in Enterprise Value by Undertaking IPO in 2011 Rather than 2010

$15.2 billion

See Table 14.10 for an illustration of the firm’s complex capital structure shortly before the March 8, 2011 IPO.

The capital structure is tiered to reflect the priority of creditor claims on the firm’s assets in liquidation and consists of

senior secured first lien (claim) debt, senior secured second lien (claim) debt, and unsecured debt. The wide variation in

effective interest rates reflects the variation in the maturity of the loans and whether they have a first or second claim on

assets in the event of liquidation.

Credit facilities refer to lending arrangements such as revolving credit and term loans. The senior credit facilities

contain a number of covenants designed to protect lenders restricting HCA’s ability to incur additional indebtedness,

repay subordinated indebtedness, create liens on assets, sell assets, make investments or loans, pay dividends, and enter

Exhibit 14.10 Consolidated HCA Long-Term Debt as of 12/31/2010

($Millions)

Senior Secured Asset Based Revolving Credit Facility (Effective Interest Rate = 1.5%)

$1.875

Senior Secured Revolving Credit Facility (Effective Interest Rate = 1.8%)

729

Senior Secured Term Loan Facilities (Effective Interest Rate = 6.9%)

7,530

Senior Secured First Lien Notes (Effective Interest Rate = 8.4%)

4,075

Other Senior Secured Debt (Effective Interest Rate = 7.1%)

322

Total First Lien Debt

14,531

Senior Secured Cash-Pay Notes (Effective Interest Rate of 9.7%)

4,501

Senior Secured Toggle Notes (Effective Interest Rate of 10%)

1,578

Second Lien Debt

Senior Unsecured Notes (Effective Interest Rate = 7.1%)

7,615

28,225

Less Amounts Due Within One Year

592

22

the $4.9 billion equity contribution, Bain and KKR (Kohlberg, Kravis, and Roberts) each invested $1.2 billion. Merrill

Lynch (now owned by Bank of America), Citigroup, and Bank of America contributed $1.5 billion. The company co-

founder, Thomas Frist Jr., provided $950 million (consisting mostly of his holdings of HCA shares), with the remainder

coming from 1400 other HCA executives. Merrill Lynch, Citigroup, and BofA also were lenders in the transaction to

take HCA private. Under the Dodd-Frank Act of 2010, lenders are now prohibited from also investing in such

transactions.

As of December 31, 2006, immediately after the LBO, the firm’s leverage as measured by total debt to EBITDA

was 6.7. By yearend 2010, the debt to EBITDA had dropped to 5.1. Most of the reduction in leverage during that four

year period was accomplished through growth in EBITDA, which grew by about $1.7 billion or 33% to $5.6 billion in

2010 versus $4.2 billion in 2006. This improvement in operating performance was accomplished through an expansion

Case Study HCA Goes Public…Again!

Discussion Questions:

1. The private equity investors in HCA decided in 2010 to declare dividends totaling $4.3 billion financed

with HCA borrowings. Presumably, if the additional borrowing had not taken place, the firms’ leverage

would have been lower prior to the IPO in March 2011 and the potential IPO share price could have been

higher. If you were a private equity fund manager, would you have decided to pay a dividend or to have

allowed HCA’s leverage to decline further in anticipation of the IPO? Explain your answer.

2. Based on what you know about HCA and the outlook for the U.S. healthcare industry, in what sense do

you believe HCA was an attractive LBO candidate and in what sense was it not? Be specific.

Answer: HCA possessed some of the important attributes of attractive LBO candidates, including owning

many hospitals and surgical clinics which could be used to secure additional debt and predictable cash

23

3. Critics of LBOs often argue that such transactions contribute little to society and only serve to enrich the

financial sponsor. Do you agree or disagree with this statement. Be specific.

Answer: Financial returns to sponsors reflect the risk associated with such investments. While empirical

studies often indicate very attractive financial returns to sponsors (both pre and post announcement date),

4. HCA had a negative shareholders’ equity at the end of 2010 of $(11.93) billion, just prior to the IPO,

making the firm technically insolvent. Nonetheless, the investor response to the IPO was highly

enthusiastic. Why do you believe this was the case?

5. Assume you are a private equity investor responsible for designing the “optimal” capital structure for a

firm you intend to acquire through a leveraged buyout. What factors would you take into consideration in

constructing the “optimal” capital structure? Be specific.

Answer: The optimal capital structure for the target firm should reflect the following considerations:

• Maintaining sufficient working capital to satisfy normal liquidity requirements

• Secure a revolving line of credit to satisfy unanticipated changes in liquidity needs

• Satisfying existing loan covenants

“Grave Dancer” Takes Tribune Corporation Private in an Ill-Fated Transaction

At the closing in late December 2007, well-known real estate investor Sam Zell described the takeover of the Tribune

Company as “the transaction from hell.” His comments were prescient in that what had appeared to be a cleverly

crafted, albeit highly leveraged, deal from a tax standpoint was unable to withstand the credit malaise of 2008. The end

came swiftly when the 161-year-old Tribune filed for bankruptcy on December 8, 2008.

On April 2, 2007, the Tribune Corporation announced that the firm’s publicly traded shares would be acquired in a

multistage transaction valued at $8.2 billion. Tribune owned at that time 9 newspapers, 23 television stations, a 25%

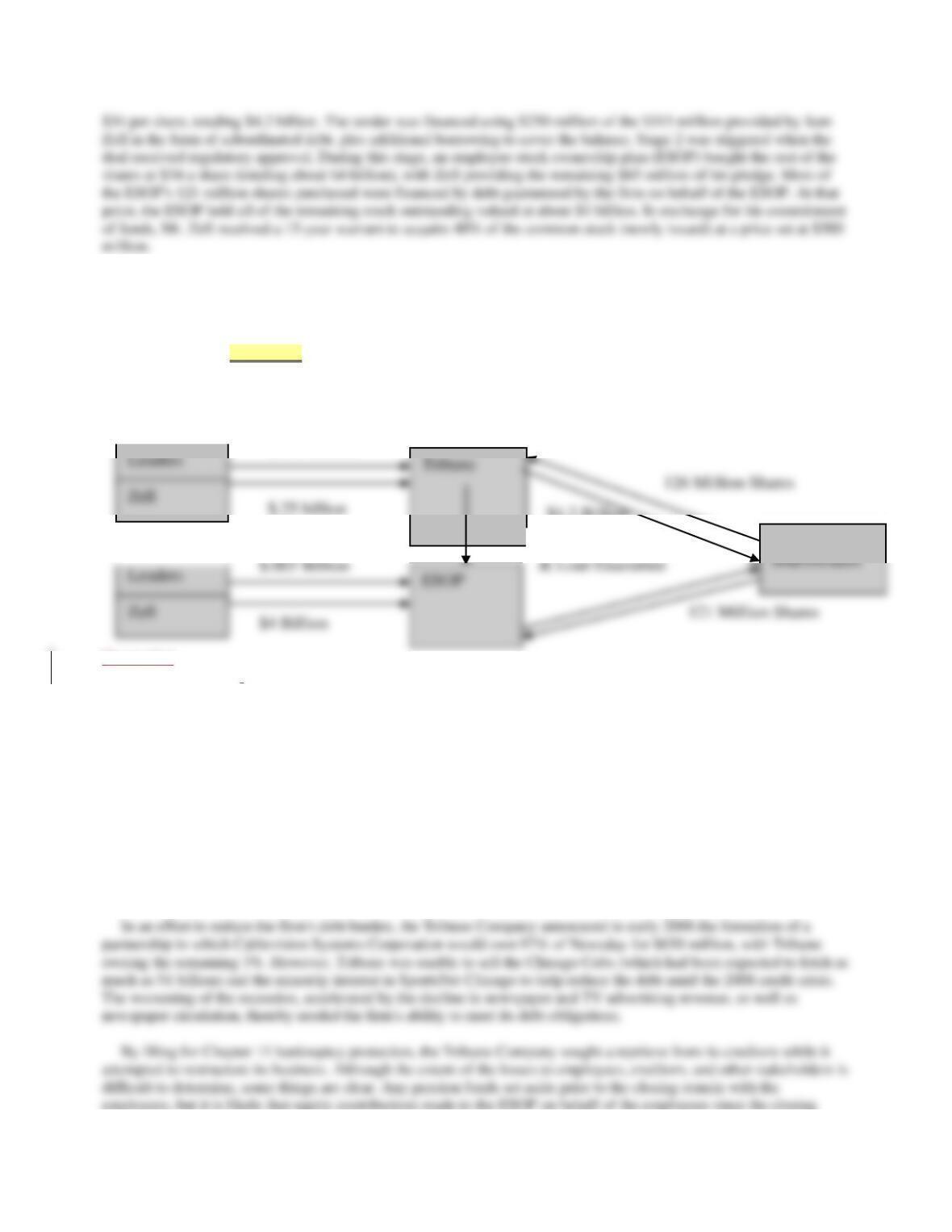

24

Following closing in December 2007, all company contributions to employee pension plans were funneled into the

ESOP in the form of Tribune stock. Over time, the ESOP would hold all the stock. Furthermore, Tribune was converted

from a C corporation to a Subchapter S corporation, allowing the firm to avoid corporate income taxes. However, it

would have to pay taxes on gains resulting from the sale of assets held less than ten years after the conversion from a C

to an S corporation (Figure 13.4).

Lenders

Zell

$.25 billion

126 Million Shares

Lenders

Zell

121 Million Shares

$4.05

Figure 13.4

Tribune deal structure.

The purchase of Tribune’s stock was financed almost entirely with debt, with Zell’s equity contribution amounting to

less than 4% of the purchase price. The transaction resulted in Tribune being burdened with $13 billion in debt

(including the approximate $5 billion currently owed by Tribune). At this level, the firm’s debt was ten times EBITDA,

more than two and a half times that of the average media company. Annual interest and principal repayments reached

$800 million (almost three times their preacquisition level), about 62% of the firm’s previous EBITDA cash flow of

$1.3 billion. While the ESOP owned the company, it was not be liable for the debt guaranteed by Tribune.

The conversion of Tribune into a Subchapter S corporation eliminated the firm’s current annual tax liability of $348

million. Such entities pay no corporate income tax but must pay all profit directly to shareholders, who then pay taxes

on these distributions. Since the ESOP was the sole shareholder, Tribune was expected to be largely tax exempt, since

ESOPs are not taxed.

Tribune

Stage 1

Stage 2

$3.85 Billion

$4.2 Billion

126 Million Shares

25

would be lost. The employees would become general creditors of Tribune. As a holder of subordinated debt, Mr. Zell

had priority over the employees if the firm was liquidated and the proceeds distributed to the creditors.

Those benefitting from the deal included Tribune’s public shareholders, including the Chandler family, which owed

12% of Tribune as a result of its prior sale of the Times Mirror to Tribune, and Dennis FitzSimons, the firm’s former

CEO, who received $17.7 million in severance and $23.8 million for his holdings of Tribune shares. Citigroup and

Discussion Questions:

1. What is the acquisition vehicle, post-closing organization, form of payment, form of acquisition, and tax

strategy described in this case study?

Answer: The ESOP is the acquisition vehicle and the subchapter S corporation is the post-closing

organization. Cash is the form of payment and the form of acquisition is stock. The tax strategy is to

2. Describe the firm’s strategy to finance the transaction?

Answer: The transaction will be financed primarily by debt. The firm’s free cash flow will be improved by

3. Is this transaction best characterized as a merger, acquisition, leveraged buyout, or spin-off? Explain your

answer.

4. Is this transaction taxable or non–taxable to Tribune’s public shareholders? To its post-transaction

shareholders? Explain your answer.

5. Comment on the fairness of this transaction to the various stakeholders involved. How would you apportion

the responsibility for the eventual bankruptcy of Tribune among Sam Zell and his advisors, the Tribune board,

and the largely unforeseen collapse of the credit markets in late 2008? Be specific.

Answer: The transaction was clearly highly leveraged by most measures. It was financed almost entirely with

debt, with Zell’s equity contribution amounting to less than 4 percent of the purchase price. The transaction

26

Kinder Morgan Buyout Raises Ethical Questions

In the largest management buyout in U.S. history at that time, Kinder Morgan Inc.’s management proposed to take the

oil and gas pipeline firm private in 2006 in a transaction that valued the firm’s outstanding equity at $13.5 billion.

Under the proposal, chief executive Richard Kinder and other senior executives would contribute shares valued at $2.8

billion to the newly private company. An additional $4.5 billion would come from private equity investors, including

Goldman Sachs Capital partners, American International Group Inc., and the Carlyle Group. Including assumed debt,

the transaction was valued at about $22 billion. The transaction also was notable for the governance and ethical issues it

raised. Reflecting the struggles within the corporation, the deal did not close until mid-2007.

Kinder Morgan’s management hired Goldman Sachs in February 2006 to explore “strategic” options for the firm to

enhance shareholder value. The leveraged buyout option was proposed by Goldman Sachs on March 7, followed by

their proposal to become the primary investor in the LBO on April 5. The management buyout group hired a number of

law firms and other investment banks as advisors and discussed the proposed buyout with credit-rating firms to assess

how much debt the firm could support without experiencing a downgrade in its credit rating.

On May 13, 2006, the full board was finally made aware of the proposal. The board immediately demanded that a

standstill agreement that had been signed by Richard Kinder, CEO and leader of the buyout group, be terminated. The

agreement did not permit the firm to talk to any alternative bidders for a period of 90 days. While investment banks and

buyout groups often propose such an agreement to ensure that they can perform adequate due diligence, this extended

period is not necessarily in the interests of the firm’s shareholders because it puts alternative suitors coming in later at a

distinct disadvantage. Later bidders simply lack sufficient time to make an adequate assessment of the true value of the

target and structure their own proposals. In this way, the standstill agreement could discourage alternative bids for the

business.

Financing LBOs—The SunGard Transaction

2 Berman and Sender, 2006

27

With their cash hoards accumulating at an unprecedented rate, there was little that buyout firms could do but to invest

in larger firms. Consequently, the average size of LBO transactions grew significantly during 2005. In a move

reminiscent of the blockbuster buyouts of the late 1980s, seven private investment firms acquired 100 percent of the

outstanding stock of SunGard Data Systems Inc. (SunGard) in late 2005. SunGard is a financial software firm known

for providing application and transaction software services and creating backup data systems in the event of disaster.

The company‘s software manages 70 percent of the transactions made on the Nasdaq stock exchange, but its biggest

business is creating backup data systems in case a client’s main systems are disabled by a natural disaster, blackout, or

terrorist attack. Its large client base for disaster recovery and back-up systems provides a substantial and predictable

cash flow.

SunGard’s new owners include Silver lake Partners, Bain Capital LLC, The Blackstone Group L.P., Goldman Sachs

Capital Partners, Kohlberg Kravis Roberts & Co., Providence Equity Partners Inc. and Texas Pacific Group. Buyout

firms in 2005 tended to band together to spread the risk of a deal this size and to reduce the likelihood of a bidding war.

Indeed, with SunGard, there was only one bidder, the investor group consisting of these seven firms.

Under the terms of the agreement, SunGard shareholders received $36 per share, a 14 percent premium over the

SunGard closing price as of the announcement date of March 28, 2005, and 40 percent more than when the news first

leaked about the deal a week earlier. From the SunGard shareholders’ perspective, the deal is valued at $11.4 billion

dollars consisting of $10.9 billion for outstanding shares and “in-the-money” options (i.e., options whose exercise price

is less than the firm’s market price per share) plus $500 million in debt on the balance sheet.

The seven equity investors provided $3.5 billion in capital with the remainder of the purchase price financed by

commitments from a lending consortium consisting of Citigroup, J.P. Morgan Chase & Co., and Deutsche Bank. The

purpose of the loans is to finance the merger, repay or refinance SunGard’s existing debt, provide ongoing working

The merger financing consists of several tiers of debt and “credit facilities.” Credit facilities are arrangements for

extending credit. The senior secured debt and senior subordinated debt are intended to provide “permanent” or long–

term financing. Senior debt covenants included restrictions on new borrowing, investments, sales of assets, mergers

and consolidations, prepayments of subordinated indebtedness, capital expenditures, liens and dividends and other

distributions, as well as a minimum interest coverage ratio and a maximum total leverage ratio.

If the offering of notes is not completed on or prior to the closing, the banks providing the financing have committed

to provide up to $3 billion in loans under a senior subordinated bridge credit facility. The bridge loans are intended as

28

The following table provides SunGard’s post-merger proforma capital structure. Note that the proforma capital

structure is portrayed as if SunGard uses 100 percent of bank lending commitments. Also, note that individual LBO

SunGard Proforma Capital Structure

Pre-Merger Existing SunGard Debt Outstanding $Millions

Senior Notes (3.75% due in 2009) 250,000,000

Senior Notes (4.785 due in 2014) 250,000,000

Total Existing Debt Outstanding 500,000,000

Debt Portion of Merger Financing

Equity Portion of Merger Financing

Equity Investor Commitment ($Millions)

Silver Lake Partners II, LP1 540,000,000

Bain Capital Fund VIII, LP 540,000,000

Blackstone Capital Partners IV, L.P. 270,000,000

Blackstone Communications Partners I, L.P. 270,000,000

1The roman numeral II refers to the fund providing the equity capital managed by the

partnership.

Case Study Discussion Questions:

1. SunGard is a software company with relatively few tangible assets. Yet, the ratio of debt to equity of almost 5

to 1. Why do you think lenders would be willing to engage in such a highly leveraged transaction for a firm of

this type?

Answer: Lenders are confident that the loans can be repaid because of the predictable cash flow associated

with SunGard’s disaster-recovery business.

29

2. Under what circumstances would SunGard refinance the existing $500 million in outstanding senior debt after

the merger? Be specific.

3. In what ways is this transaction similar to and different from those that were common in the 1980s? Be

specific.

Answer: In the 1980s, few hi-tech companies were taken private due to their lack of tangible assets and high

4. Why are payment-in-kind securities (e.g., debt or preferred stock) particularly well suited for financing LBOs?

Under what circumstances might they be most attractive to lenders or investors?

5. Explain how the way in which the LBO is financed affects the way it is operated and the timing of when

equity investors choose to exit the business. Be specific.

Answer: The greater the leverage and non-PIK debt the greater the need to manage the business for cash and

HCA’S LBO REPRESENTS A HIGH-RISK BET ON GROWTH

While most LBOs are predicated on improving operating performance through a combination of aggressive cost cutting

and revenue growth, HCA laid out an unconventional approach in its effort to take the firm private. On July 24, 2006,

management again announced that it would “go private” in a deal valued at $33 billion including the assumption of

$11.7 billion in existing debt.

The approximate $21.3 billion purchase price for HCA’s stock was financed by a combination of $12.8 billion in

senior secured term loans of varying maturities and an estimated $8.5 billion in cash provided by Bain Capital, Merrill

Lynch Global Private Equity, and Kohlberg Kravis Roberts & Company. HCA also would take out a $4 billion

revolving credit line to satisfy immediate working capital requirements. The firm publicly announced a strategy of

Discussion Questions:

30

1. Does a hospital or hospital system represent a good or bad LBO candidate? Explain your answer.

Answer: Hospitals generally represent bad candidates. Hospital cash flow is heavily dependent on

government reimbursement rates which are likely to be declining in the future as the U.S. government

2. Having pledged not to engage in aggressive cost cutting, how do you think HCA and its financial sponsor

group planned on paying off the loans?

Answer: The financial sponsor group is assuming that increased government spending in view of the

growing demands of an aging population will result in increased total spending, even though

Sony Buys MGM

Sony’s long-term vision has been to create synergy between its consumer electronics products and music, movies, and

games. Sony, which bought Columbia Pictures in 1989 for $3.4 billion, had wanted to control Metro-Goldwyn-Mayer’s

film library for years, but it did not want to pay the estimated $5 billion it would take to acquire it. On September 14,

2004, a consortium, consisting of Sony Corp of America, Providence Equity Partners, Texas Pacific Group, and DLJ

Merchant Banking Partners, agreed to acquire MGM for $4.8 billion, consisting of $2.85 billion in cash and the

assumption of $2 billion in debt. The cash portion of the purchase price consisted of about $1.8 billion in debt and $1

billion in equity capital. Of the equity capital, Providence contributed $450 million, Sony and Texas Pacific Group

$300 million, and DLJ Merchant Banking $250 million.

The Sony consortium huddled throughout the Labor Day weekend to put in place the financing for a bid of $12 per

share. What often takes months to work out in most leveraged buyouts was hammered out in three days of marathon

sessions at law firm Davis Polk & Wardwell. In addition to getting final agreement on financing arrangements

31

Discussion Questions:

1. Do you believe that MGM is an attractive LBO candidate? Why? Why not?

Answer: MGM made an attractive LBO candidate because of its ownership of a large film library, which

2. In what way do you believe that Sony’s objectives might differ from those of the private equity investors

making up the remainder of the consortium? How might such differences affect the management of MGM?

Identify possible short-term and long-term effects.

Answer: Sony wanted to gain access to the film library to help provide content for the growth in its play

station and games product lines. However, the private equity investors were more likely to want to cash out in

3-5 years or less. This may have created short-term management disagreements as Sony may have wanted to

3. How did Time Warner’s entry into the bidding affect pace of the negotiations and the relative bargaining

power of MGM, Time Warner, and the Sony consortium?

Answer: The bargaining was contentious and stalled for 5 months until Time Warner converted the bilateral

discussions into an auction. Consequently, bargaining leverage shifted to MGM and the Sony led consortium

4. What do you believe were the major factors persuading the MGM board to accept the Revised Sony bid? In

your judgment, do these factors make sense? Explain your answer.

Answer: MGM’s board and Kirk Kerkorian, MGM’s largest shareholder, were uncertain about the future

RJR NABISCO GOES PRIVATE—

KEY SHAREHOLDER AND PUBLIC POLICY ISSUES

Background

The largest LBO in history is as well known for its theatrics as it is for its substantial improvement in shareholder

value. In October 1988, H. Ross Johnson, then CEO of RJR Nabisco, proposed an MBO of the firm at $75 per share.

His failure to inform the RJR board before publicly announcing his plans alienated many of the directors. Analysts

outside the company placed the breakup value of RJR Nabisco at more than $100 per share—almost twice its then

32

the board ultimately accepted the KKR bid. The winning bid was set at almost $25 billion—the largest transaction on

record at that time and the largest LBO in history. Banks provided about three-fourths of the $20 billion that was

borrowed to complete the transaction. The remaining debt was supplied by junk bond financing. The RJR shareholders

were the real winners, because the final purchase price constituted a more than 100% return from the $56 per share

price that existed just before the initial bid by RJR management.

Potential Conflicts of Interest

In any MBO, management is confronted by a potential conflict of interest. Their fiduciary responsibility to the

shareholders is to take actions to maximize shareholder value; yet in the RJR Nabisco case, the management bid

appeared to be well below what was in the best interests of shareholders. Several proposals have been made to

minimize the potential for conflict of interest in the case of an MBO, including that directors, who are part of an MBO

effort, not be allowed to participate in voting on bids, that fairness opinions be solicited from independent financial

advisors, and that a firm receiving an MBO proposal be required to hold an auction for the firm.

Winners and Losers

RJR Nabisco shareholders before the buyout clearly benefited greatly from efforts to take the company private.

However, in addition to the potential transfer of wealth from bondholders to stockholders, some critics of LBOs argue

that a wealth transfer also takes place in LBO transactions when LBO management is able to negotiate wage and

benefit concessions from current employee unions. LBOs are under greater pressure to seek such concessions than

other types of buyouts because they need to meet huge debt service requirements.

Discussion Questions:

1. In your opinion, was the buyout proposal presented by Ross Johnson’s management group in the best interests

of the shareholders? Why? / Why not?

Answer: No. The management group proposed to buy the firm for $75 per share. Immediately, outside

33

2. What were the RJR Nabisco board’s fiduciary responsibilities to the shareholders? How well did they satisfy

these responsibilities? What could/should they have done differently?

Answer: The board’s fiduciary responsibilities were to maximize shareholder value. The board’s actions

3. Why might the RJR Nabisco board have accepted the KKR bid over the Johnson bid?

4. How might bondholders and preferred stockholders have been hurt in the RJR Nabisco leveraged buyout?

Answer: One of the most contentious discussions immediately following the closing of the RJR Nabisco

buyout centered on the alleged transfer of wealth from bond and preferred stockholders to common

5. Describe the potential benefits and costs of LBOs to shareholders, employers, lenders, customers, and

communities in which the firm undergoing the buyout may have operations. Do you believe that on average

LBOs provide a net benefit or cost to society? Explain your answer.

Answer: RJR Nabisco shareholders prior to the buyout clearly benefited greatly from efforts to take the

company private. However, in addition to the potential transfer of wealth from bondholders to stockholders,

some critics of LBOs argue that a wealth transfer also takes place in LBO transactions when LBO

Private Equity Firms Acquire Yellow Pages Business

Qwest Communications agreed to sell its yellow pages business, QwestDex, to a consortium led by the Carlyle Group

and Welsh, Carson, Anderson and Stowe for $7.1 billion. In a two stage transaction, Qwest sold the eastern half of the

yellow pages business for $2.75 billion in late 2002. This portion of the business included directories in Colorado,

Iowa, Minnesota, Nebraska, New Mexico, South Dakota, and North Dakota. The remainder of the business, Arizona,

Idaho, Montana, Oregon, Utah, Washington, and Wyoming, was sold for $4.35 billion in late 2003. Caryle and Welsh

Carson each put in $775 million in equity (about 21 percent of the total purchase price).

Qwest was in a precarious financial position at the time of the negotiation. The telecom was trying to avoid

bankruptcy and needed the first stage financing to meet impending debt repayments due in late 2002. Qwest is a local

phone company in 14 western states and one of the nation’s largest long-distance carriers. It had amassed $26.5 billion

in debt following a series of acquisitions during the 1990s.

Discussion Questions:

1. Why was QwestDex considered an attractive LBO candidate? Do you think it has significant growth potential?

Explain the following statement: “A business with high growth potential may not be a good candidate for an LBO.

QwestDex was considered an attractive candidate because of its steadily growing, highly predictable cash flow,

2. Why did the buyout firms want a 50-year contract to be the exclusive provider of publishing services to Qwest

Communications?

3. Why would the buyout firms want Qwest to continue to provide such services as billing and information

technology support? How might such services be priced?

The buyers wanted to ensure a flawless transition of payroll, IT, and other administrative support services when the

4. Why would it take five very large financial institutions to finance the transactions?

5. Why was the equity contribution of the buyout firms as a percentage of the total capital requirements so much

higher than amounts contributed during the 1980s?