CHAPTER 14

Financial Statement Analysis

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

Problems

1. Apply horizontal and vertical analysis

to financial statements.

1, 2, 3, 4

1, 2, 3, 4, 5,

6, 7, 8

1

1, 2, 3, 4

1

14, 15, 16,

3. Apply the concept of sustainable

20, 21, 22, 23

14, 15

3

12, 13

8, 9

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1

Prepare vertical analysis and comment on profitability.

Simple

20–30

2

Compute ratios from balance sheet and income statement.

Simple

20–30

3

Perform ratio analysis, and evaluate financial position

and operating results.

Simple

20–30

4

Compute ratios, and comment on overall liquidity and

profitability.

30–40

and solvency for two companies.

Compute numerous ratios.

7

Compute missing information given a set of ratios.

30–40

8

Prepare a statement of comprehensive income.

30–40

Prepare a statement of comprehensive income.

WEYGANDT FINANCIAL AND MANAGERIAL ACCOUNTING 2E

CHAPTER 14

FINANCIAL STATEMENT ANALYSIS

Number

LO

BT

Difficulty

Time (min.)

BE1

1

C

Moderate

10–12

BE2

1, 2

K, AP

Simple

8–10

BE11

2

AN

Simple

6–8

BE12

2

AN

Moderate

6–8

BE13

2

AN

Moderate

6–8

BE14

3

AP

Simple

4–6

BE15

3

AP

Simple

3–5

DI1

1

AP

Simple

6–8

DI2

2

AP

Simple

DI3

3

AP

Simple

6–8

EX1

1

AP

Simple

10–12

EX2

1

AP

Simple

EX3

1

AP

Simple

12–15

EX4

1

AP

Simple

10–12

EX5

2

AN

Simple

8–10

EX6

2

AP

Simple

8–10

EX7

2

AP

Simple

6–8

EX8

2

AP

Simple

6–8

EX9

2

AP

Simple

6–8

EX10

2

AP

Moderate

8–10

BE3

1

AP

Simple

6–8

BE4

1

AP

Simple

6–8

BE5

1

AP

Simple

4–6

BE6

1

AP

Simple

4–6

BE7

1

AP

Simple

4–6

BE8

1

AP

Simple

5–7

BE9

2

AP

Simple

4–6

BE10

2

AP

Simple

3–5

FINANCIAL STATEMENT ANALYSIS (Continued)

Number

LO

BT

Difficulty

Time (min.)

EX11

2

AP

Simple

10–12

P7

2

AN

Complex

30–40

P8

3

AP

Moderate

30–40

P9

3

AP

Moderate

30–40

BYP1

1, 2

AN, E

Moderate

20–25

BYP2

1, 2

AN, E

Simple

15–20

BYP3

1, 2

AN, E

Simple

15–20

BYP4

2

Simple

15–20

BYP5

Moderate

15–20

BYP6

1, 2

Simple

15–20

BYP7

Simple

10–15

BYP8

Simple

15–20

BYP9

3

AP

Simple

3

Moderate

3

Simple

P1

1, 2

AN

Simple

20–30

P2

2

20–30

P3

2

Simple

20–30

P4

2

AN

Moderate

30–40

P5

2

Moderate

50–60

P6

2

Simple

30–40

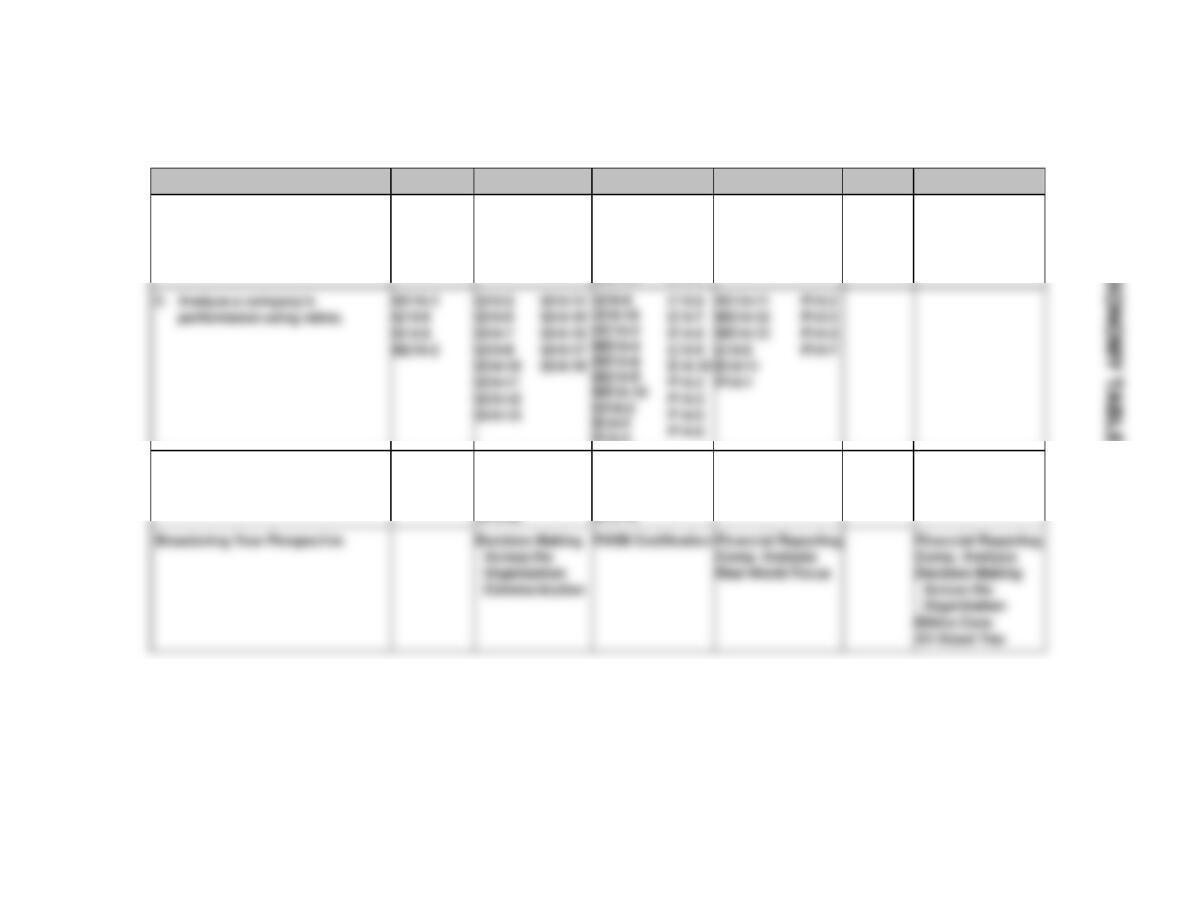

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Apply horizontal and vertical

analysis to financial statements.

BE14-2

Q14-1

Q14-2

Q14-3

BE14-1

Q14-4

BE14-2

BE14-3

BE14-5

BE14-6

BE14-7

DI14-1

E14-1

E14-3

E14-4

E14-4

3. Apply the concept of sustainable

income.

Q14-20

Q14-21

Q14-22

Q14-23

BE14-14

BE14-15

DI14-3

E14-12

E14-13

P14-8

P14-9

Ethics Case

ANSWERS TO QUESTIONS

1. (a) Jose is not correct. There are three characteristics: liquidity, profitability, and solvency.

(b) The three parties are not primarily interested in the same characteristics of a company. Short-term

creditors are primarily interested in the liquidity of the enterprise. In contrast, long-term creditors

and stockholders are primarily interested in the profitability and solvency of the company.

2. (a) Comparison of financial information can be made on an intracompany basis, an intercompany

basis, and an industry average basis (or norms).

3. Horizontal analysis (also called trend analysis) measures the dollar and percentage increase or

decrease of an item over a period of time. In this approach, the amount of the item on one statement

is compared with the amount of that same item on one or more earlier statements. Vertical analysis

(also called common-size analysis) expresses each item within a financial statement in terms of a

percent of a base amount.

5. A ratio expresses the mathematical relationship between one quantity and another. The relationship

is expressed in terms of either a percentage (200%), a rate (2 times), or a simple proportion (2:1).

Ratios can provide clues to underlying conditions that may not be apparent from individual financial

statement components. The ratio is more meaningful when compared to the same ratio in earlier

periods or to competitors’ ratios or to industry ratios.

Questions Chapter 14 (Continued)

10. Hizar Company does not necessarily have a problem. The accounts receivable turnover can be

misleading in that some companies encourage credit and revolving charge sales and slow collections

in order to earn a healthy return on the outstanding receivables in the form of high rates of interest.

13. The payout ratio is cash dividends divided by net income. In a growth company, the payout ratio is

often low because the company is reinvesting earnings in the business.

14. (a) The increase in profit margin is good news because it means that a greater percentage of net

sales is going towards income.

(b) The decrease in inventory turnover signals bad news because it is taking the company longer

to sell the inventory and consequently there is a greater chance of inventory obsolescence.

Questions Chapter 14 (Continued)

16. (a) The times interest earned, which is an indication of the company’s ability to meet interest

payments, and the debt to assets ratio, which indicates the company’s ability to withstand losses

without impairing the interests of creditors.

earning power of the investment.

17. Earnings per share means earnings per share of common stock. Preferred dividends are

subtracted from net income in computing EPS in order to obtain income available to common

stockholders.

19.

Net income – Preferred dividends

Weighted – average common shares outstanding

= Earnings per share

20. Discontinued operations refers to the disposal of a significant component of the business such as

the stopping of an entire activity or eliminating a major class of customers. It is important to report

discontinued operations separately from continuing operations because the discontinued component

will not affect future income statements.

Questions Chapter 14 (Continued)

23. The following provide examples of horizontal and vertical analysis:

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 14-1

Dear Uncle Sammy,

It was so good to hear from you! I hope you and Aunt Jennie are still enjoying

your new house.

You asked some interesting questions. They relate very well to the material

It is important to compare different financial statement elements to other

items. The amount of a financial statement element such as cash does not have

much meaning unless it is compared to something else. Comparisons can

be done on an intracompany basis. This basis compares an item or financial

Total assets

(a) The three tools of financial statement analysis are horizontal analysis,

vertical analysis, and ratio analysis. Horizontal analysis evaluates a series

(b) Horizontal Analysis

BRIEF EXERCISE 14-3

Horizontal analysis:

Increase

or (Decrease)

Dec. 31, 2017

Dec. 31, 2016

Amount

Percentage

Vertical analysis:

Dec. 31, 2017

Dec. 31, 2016

Amount

Percentage*

Amount

Percentage**

BRIEF EXERCISE 14-5

2018

2017

2016

Amount

Percentage

BRIEF EXERCISE 14-6

2017

2016

Increase

BRIEF EXERCISE 14-7

BRIEF EXERCISE 14-8

2018

2017

2016

Net income

20%

BRIEF EXERCISE 14-9

BRIEF EXERCISE 14–10

BRIEF EXERCISE 14–11

BRIEF EXERCISE 14–12

BRIEF EXERCISE 14–13

BRIEF EXERCISE 14–14

SILVA CORPORATION

Partial Statement of Comprehensive Income

BRIEF EXERCISE 14–15

HOLLOWAY CORPORATION

Partial Statement of Comprehensive Income

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 14-1

DO IT! 14-2

DO IT! 14-3

HRABIK CORPORATION

Partial Statement of Comprehensive Income

SOLUTIONS TO EXERCISES

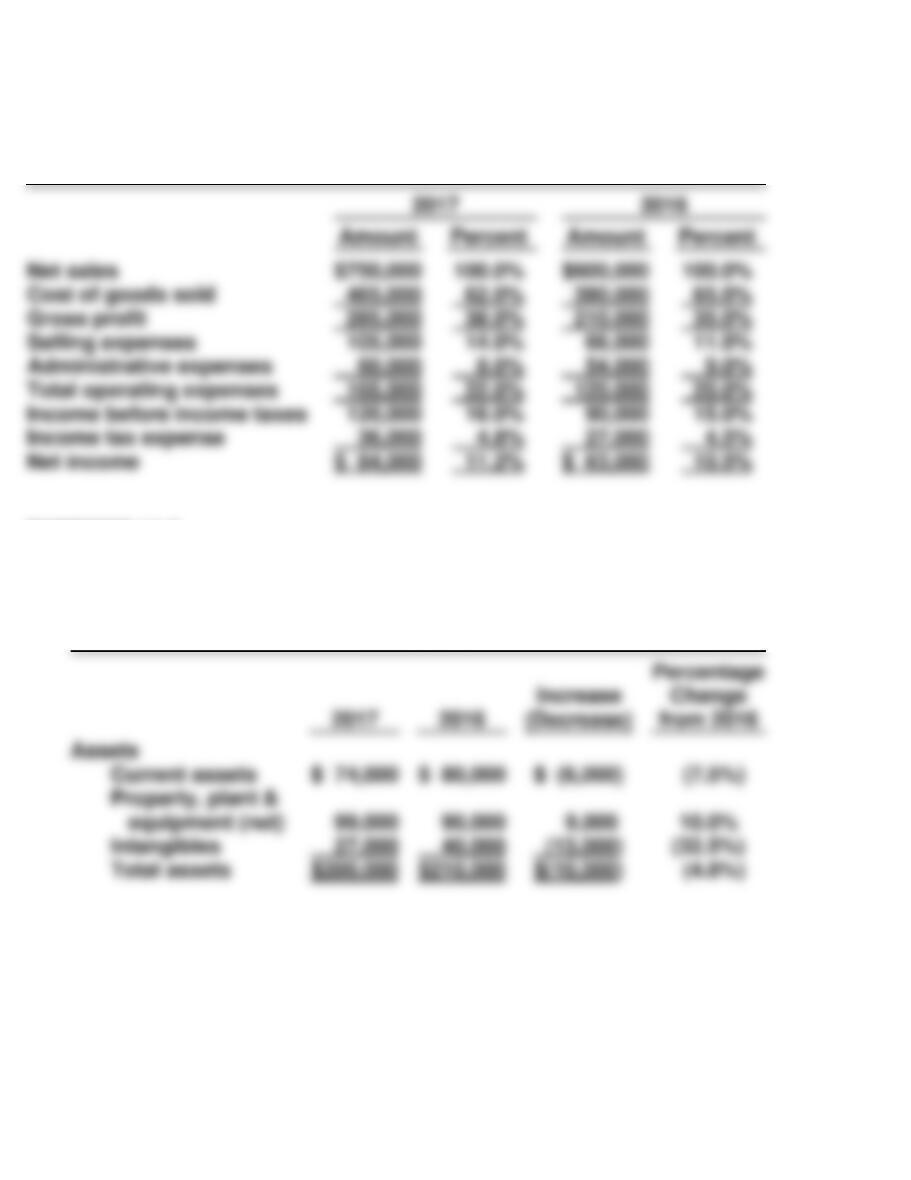

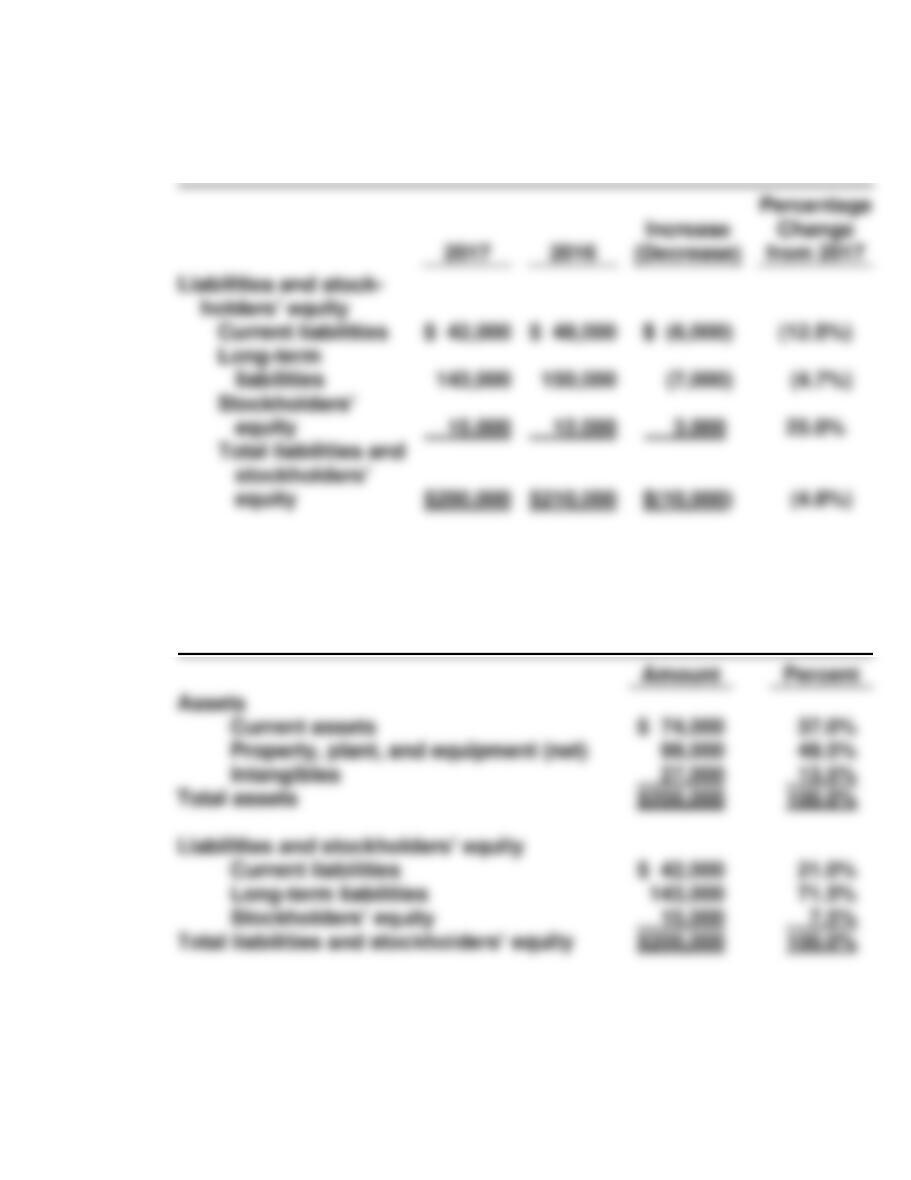

EXERCISE 14-1

KURZEN INC.

Condensed Balance Sheets

December 31

EXERCISE 14-2

NAVARRO CORPORATION

Condensed Income Statements

For the Years Ended December 31

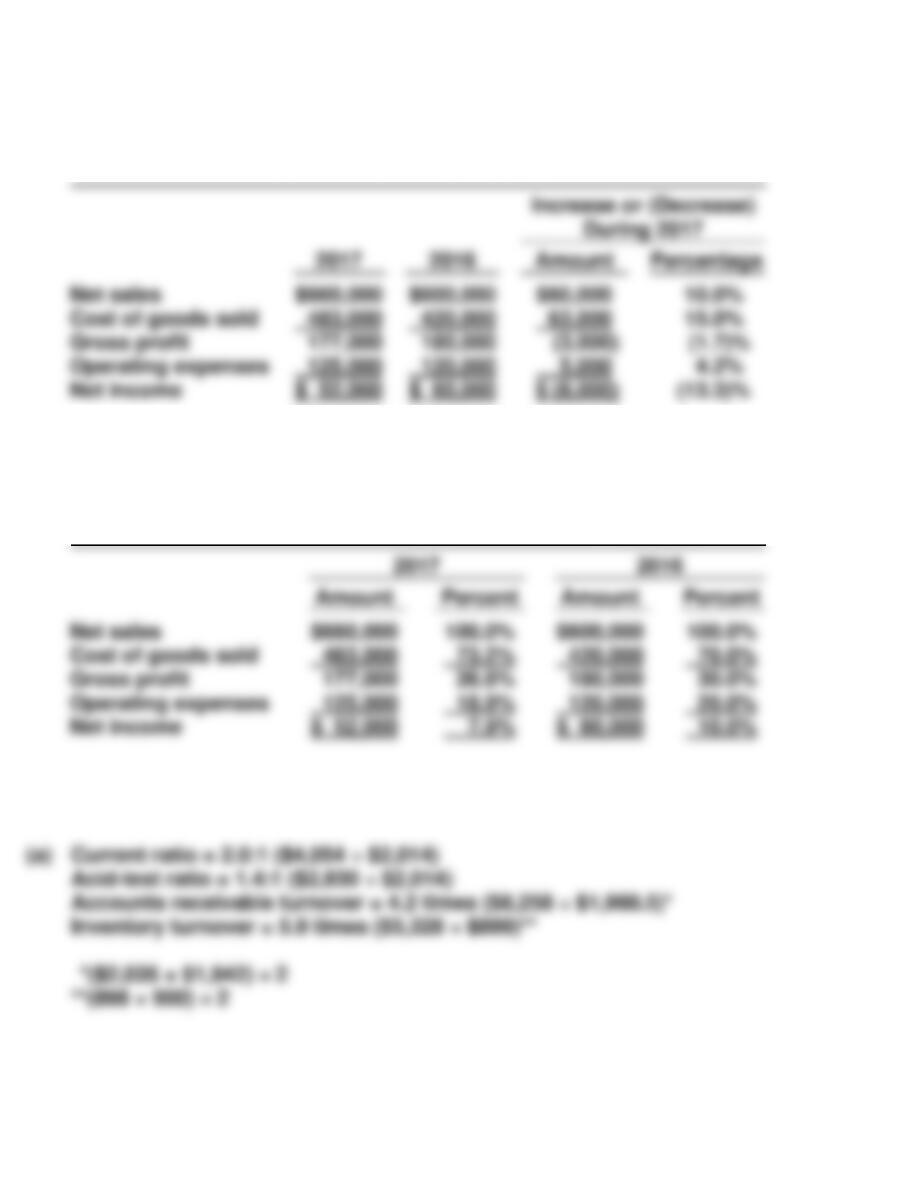

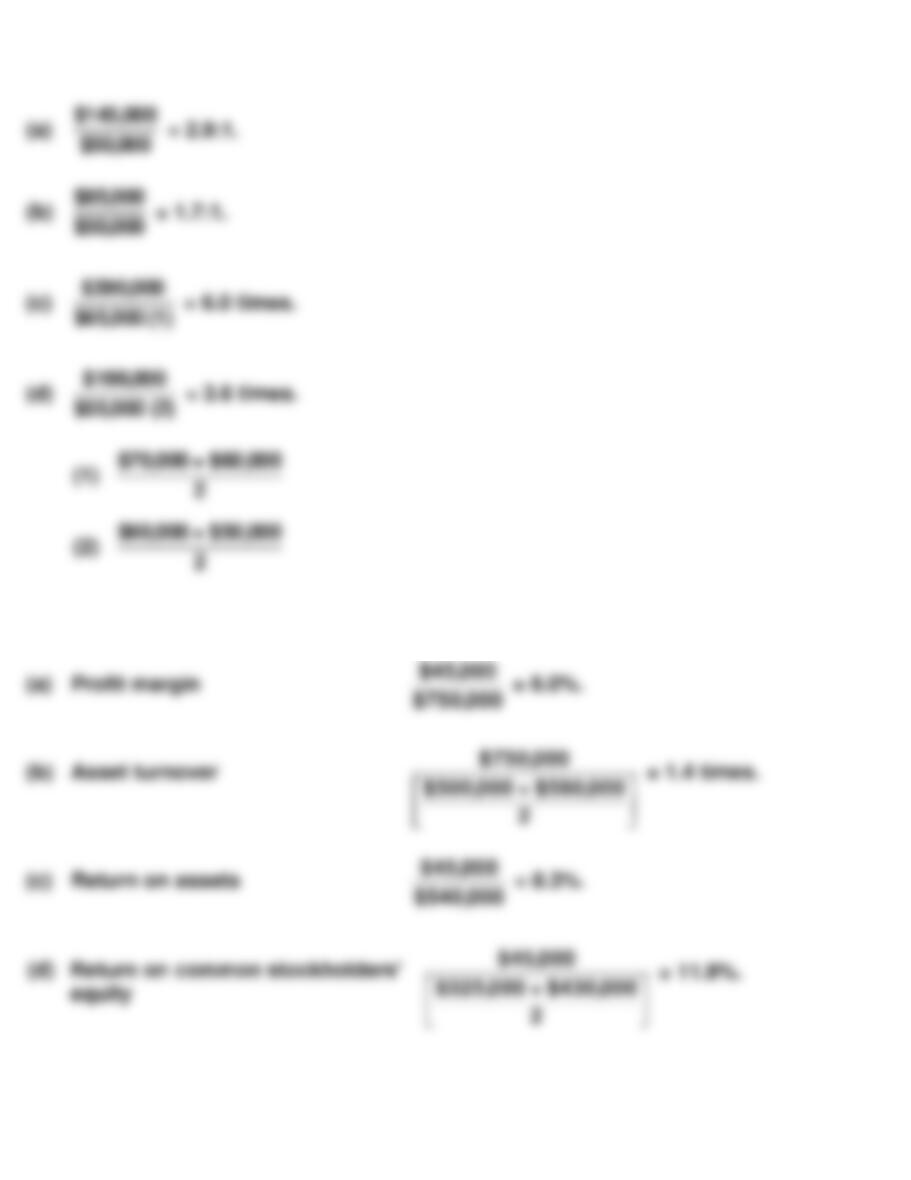

EXERCISE 14-3

(a) GURLEY CORPORATION

Condensed Balance Sheets

December 31

EXERCISE 14-3 (Continued)

GURLEY CORPORATION

Condensed Balance Sheets (Continued)

December 31

(b) GURLEY CORPORATION

Condensed Balance Sheet

December 31, 2017

EXERCISE 14-4

(a) EMLEY CORPORATION

Condensed Income Statements

For the Years Ended December 31

(b) EMLEY CORPORATION

Condensed Income Statements

For the Years Ended December 31

EXERCISE 14-5

EXERCISE 14-5 (Continued)

(b)

Ratio

Nordstrom

Macy’s

Industry

EXERCISE 14-6

EXERCISE 14-7

EXERCISE 14-8

EXERCISE 14-9

EXERCISE 14–10

EXERCISE 14-10 (Continued)

EXERCISE 14–11

EXERCISE 14–12

(a) HAAS CORPORATION

Partial Statement of Comprehensive Income

For the Year Ended October 31, 2017

(b) To: Chief Accountant

EXERCISE 14–13

(a) TRAYER CORPORATION

Partial Statement of Comprehensive Income

For the Year Ended December 31, 2017

SOLUTIONS TO PROBLEMS

PROBLEM 14-1

(a) Condensed Income Statement

For the Year Ended December 31, 2017

(b) Farris Company appears to be more profitable. It has higher relative

PROBLEM 14-1 (Continued)

PROBLEM 14-2

PROBLEM 14-2 (Continued)

PROBLEM 14-3

(a)

2017

2018

*($113,000 + $30,000 – $125,000)

**($125,000 + $45,000 – $145,000)

PROBLEM 14-3 (Continued)

PROBLEM 14-4

(a) LIQUIDITY

2016

2017

Change

turnover

PROBLEM 14-4 (Continued)

(b)

2017

2018

Change

PROBLEM 14-5

(b) The comparison of the two companies shows the following:

PROBLEM 14-6

PROBLEM 14-6 (Continued)

PROBLEM 14-7

PROBLEM 14-7 (Continued)

PROBLEM 14-8

TERWILLIGER CORPORATION

Condensed Statement of Comprehensive Income

For the Year Ended December 31, 2017

PROBLEM 14-9

JAIME CORPORATION

Statement of Comprehensive Income

For the Year Ended December 31, 2017

BYP 14-1 FINANCIAL REPORTING PROBLEM

(a) APPLE, INC.

Trend Analysis of Net Sales and Net Income

For the Three Years Ended 2013

(b) (dollar amounts in millions)

BYP 14-1 (Continued)

(c) (dollar amounts in millions)

BYP 14-2 COMPARATIVE ANALYSIS PROBLEM

(a)

PepsiCo

Coca-Cola Company

BYP 14-3 COMPARATIVE ANALYSIS PROBLEM

(a)

Amazon

Wal-Mart

BYP 14-4 DECISION MAKING ACROSS THE ORGANIZATION

The current ratio increase is a favorable indication as to liquidity, but

BYP 14-4 (Continued)

BYP 14-5 REAL-WORLD FOCUS

(a) Optional elements include:

(b) SEC-required elements include:

BYP 14-6 COMMUNICATION ACTIVITY

To: Abby Landis

From: Accounting Major

Subject: Financial Statement Analysis

BYP 14-7 ETHICS CASE

(a) The stakeholders in this case are:

BYP 14-8 ALL ABOUT YOU

BYP 14-9 FASB CODIFICATION ACTIVITY

(a) Discontinued Operations

IFRS 14-1 INTERNATIONAL FINANCIAL REPORTING PROBLEM