Accounting Information Systems, 10e 35

P-7: Follow up on open POs and receiving reports at BEPMIS.

Effectiveness goal A, vendor invoice input completeness, and vendor invoice

P-8: Select invoices for payment based on due dates.

Effectiveness goal A: Ensures that payments are made in a timely manner, not too

early and not too late (i.e., to optimize cash discounts).

P-9: Pay only open invoices and close invoices upon payment (independent

authorization to make payment) at BEPMIS.

Security of resources: Because cash cannot be expended in the absence of a

P-10: Follow up on open invoices at BEPMIS.

Effectiveness goal A, payment input completeness, and payment update

completeness: By following up on open invoices (i.e., those due for payment), we

can ensure that payments are made in time to take advantage of discounts (goal A)

and are input in a timely manner (input completeness). We assume that the AP

master data is updated simultaneously with the input of the payment data.

P-11: Digitally sign electronic payments.

Security of resources, payment input validity, payment input completeness,

payment input accuracy, payment update completeness, and payment update

36 Solutions for Chapter 13

P-12: Follow up on open invoices (at IPP).

Effectiveness goal A, payment input completeness, and payment update

P-13: CO and DO approval required for payment.

Security of resources, payment input validity, and payment input accuracy: A

contracting officer and a disbursing officer review each PIF to ensure that each

payment is authorized (validity), accurate, and is not a misuse of resources.

M-1: Independent validation of vendor invoices at IPP does not include a match to the

receiving report.

M-2: Reconcile batch totals for invoices and invoice changes.

Efficient employment of resources: Using batch totals to reconcile the invoice data

is more efficient than reviewing each invoice.

Security of resources and vendor invoice input validity: Determining that invoice

M-3: Programmed edits for formatted and translated invoice data.

Vendor invoice input accuracy and vendor invoice update accuracy: Edits at

M-4: Programmed edits for formatted and translated payment data.

Accounting Information Systems, 10e 37

M-5: Reconcile payments made by BEPMIS to PIF totals.

Efficient employment of resources: Using batch totals to reconcile the payment

data is more efficient than reviewing each payment.

M-6: Reconcile approved payments to PIF totals.

Efficient employment of resources: Using batch totals to reconcile the payment

data is more efficient than reviewing each payment.

M-7: Reconcile ACH totals to PIF totals and approved PIF totals.

Efficient employment of resources: Using batch totals to reconcile the payment

data is more efficient than reviewing each payment.

M-8: Reconcile payment made by ACH to ACH file (and PIF totals and BEPMIS

payment totals).

38 Solutions for Chapter 13

Efficient employment of resources: Using batch totals to reconcile the payment

data is more efficient than reviewing each payment.

Solution Note: Several controls not described in the previous list could be

included in the solution to this problem, as present or missing, depending on

assumptions made. For example:

• At each data entry location, we could include automated data entry,

preformatted screens, online prompting, and confirm input acceptance.

• As data is entered into the system, we might find programmed edit checks,

populate input screens with master data, and compare input data with master

data.

Accounting Information Systems, 10e 39

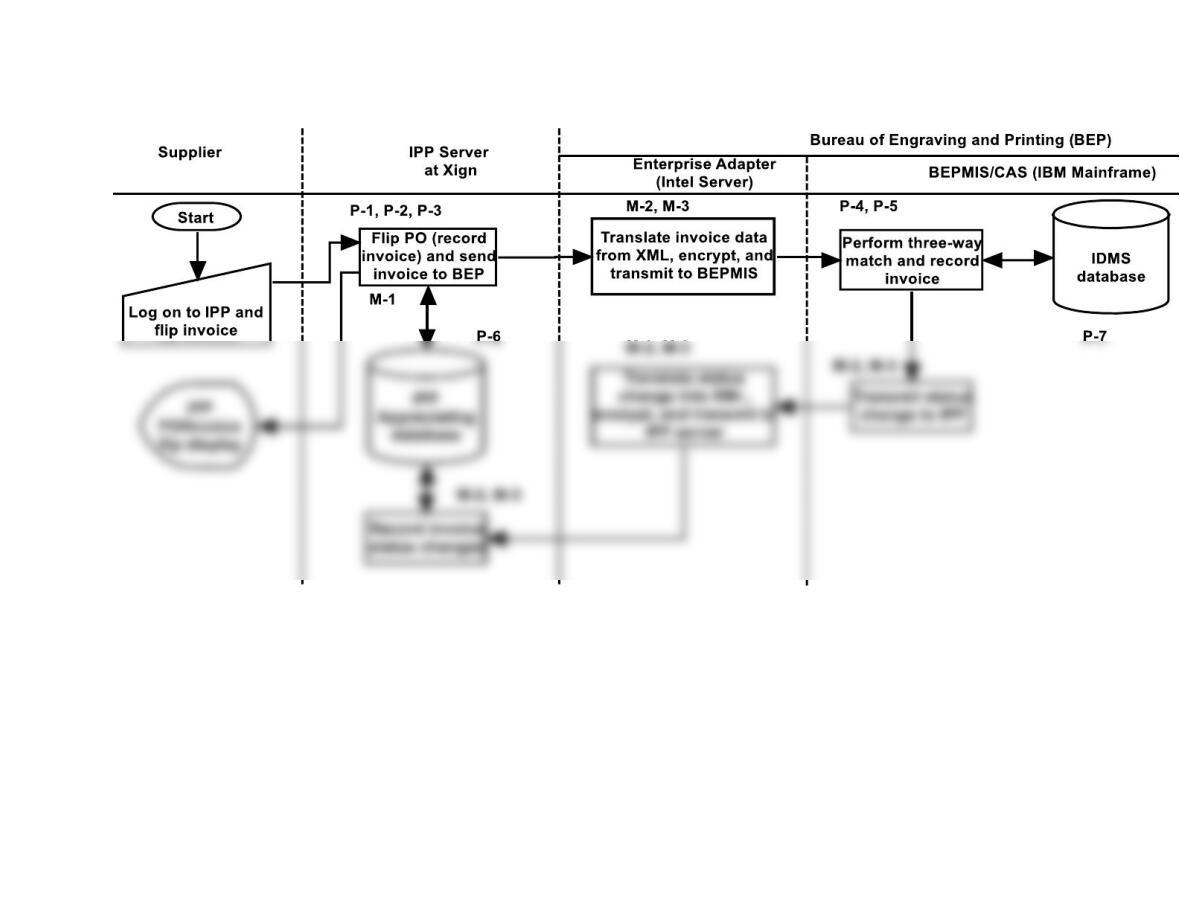

FIGURE SM-13.12 Problem 2, Part c Solution—Annotated Systems Flowchart for Internet Payment Platform

(Accounts Payable and Cash Disbursements Processes)

40 Solutions for Chapter 13

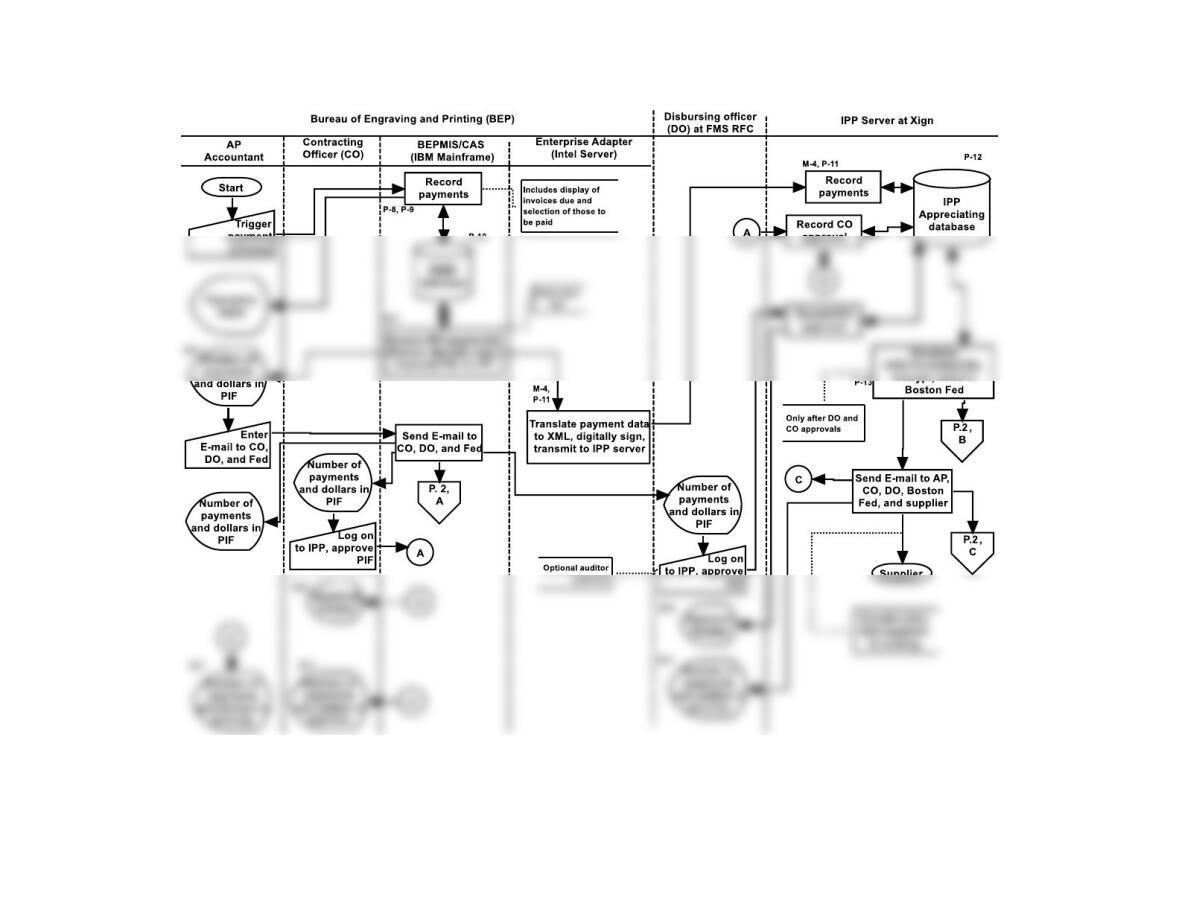

FIGURE SM-13.12 Problem 2, Part c Solution—Annotated Systems Flowchart (continued)

Accounting Information Systems, 10e 41

Supplier‘s Bank

Federal Reserve Bank

FedACH System

Federal Reserve Bank of Boston

P. 1,

C

P. 1,

B

Read e–mail

Number of

payments

and dollars

in ACH file

ACH–Form atted

file

P. 1,

A

Read e–mail

Number of

payments

and dollars

in PIF M-7

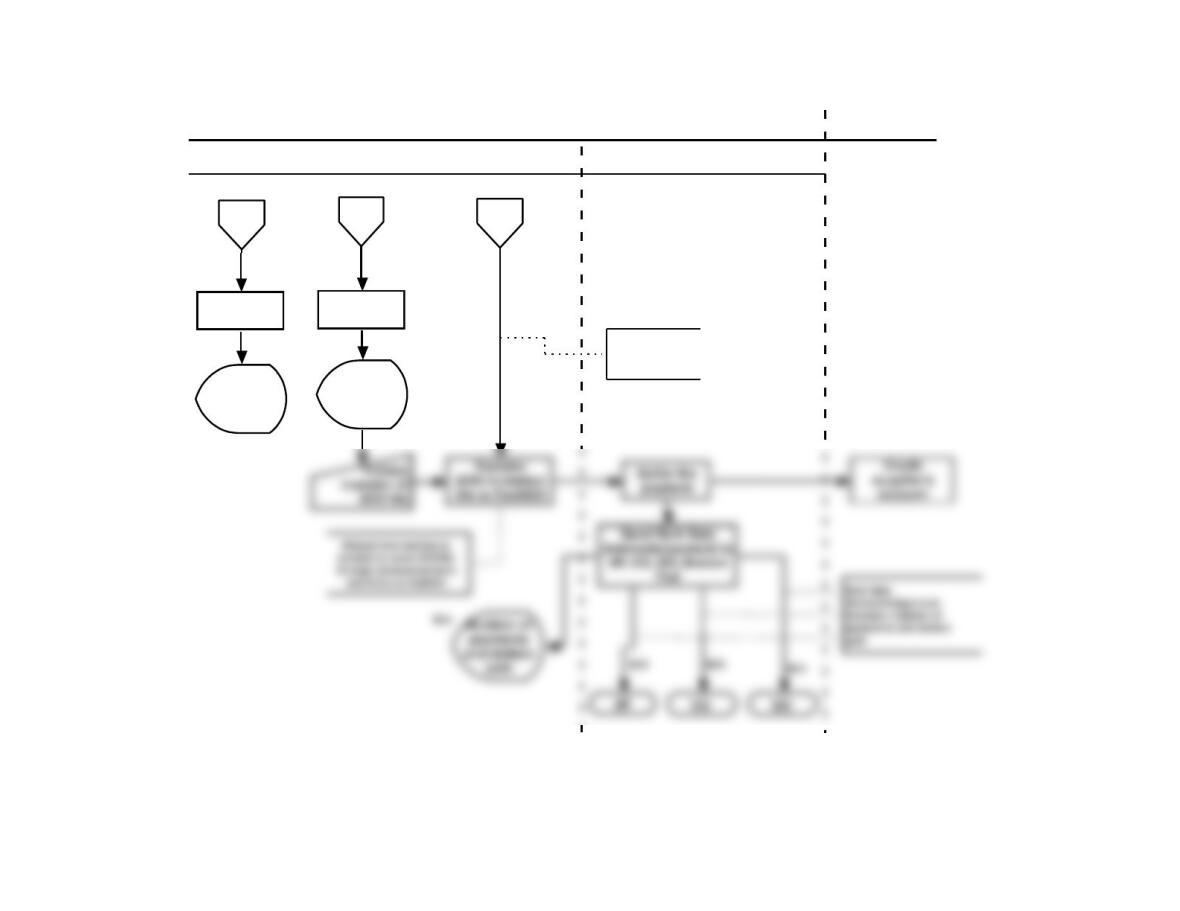

FIGURE SM-13.12 Problem 2, Part c Solution—Annotated Systems Flowchart (continued)

42 Solutions for Chapter 13

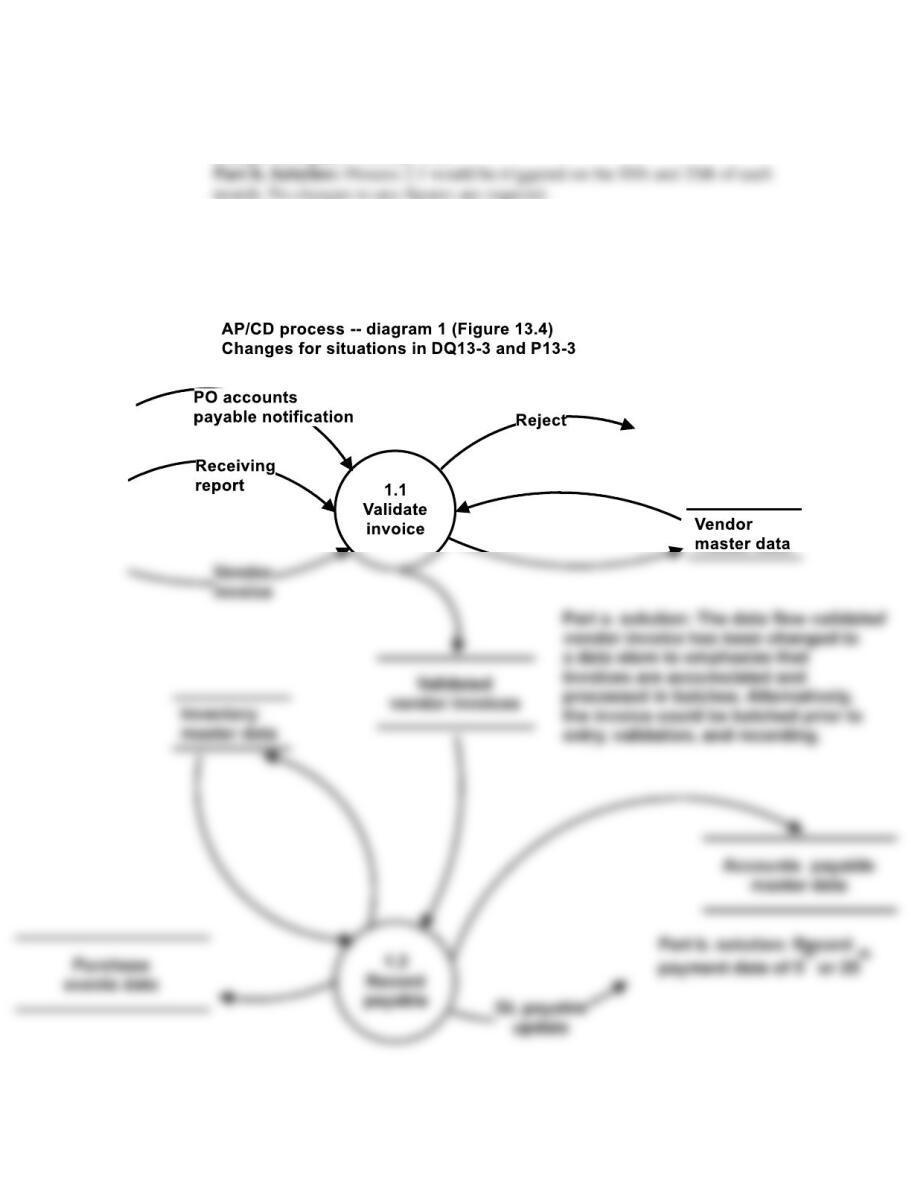

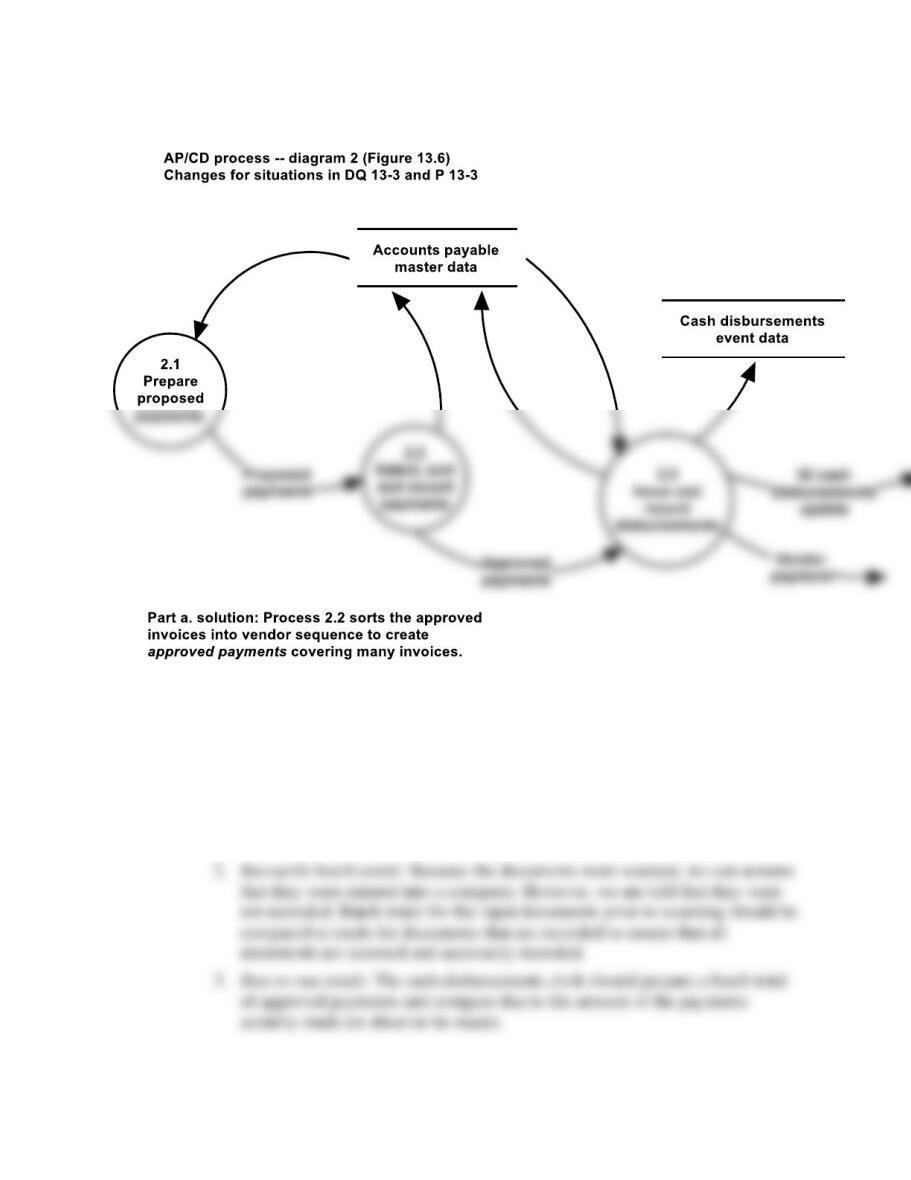

P 13-3 ANS. Part a. Solution: There are no changes to Figure 13.3. See Figure SM-13.13 for

changes to Figures 13.4 and 13.6.

Accounting Information Systems, 10e 43

FIGURE SM-13.13 Problem 3 Solution

FIGURE SM-13.13 Problem 3 Solution (continued)

P 13-4 ANS. 1. Check digit (a programmed edit): This control will detect most keying errors

(such as transpositions) as the number is input. It is best suited to numbers

such as credit card numbers, customer numbers, and vendor numbers where

the check digit is calculated, appended to the account numbers, and used each

time the account number is entered to ensure that the number has been

accurately entered.

44 Solutions for Chapter 13

4. Cash planning report: An aging of open accounts payable should be produced

on a regular basis and reviewed by the treasurer to ensure that sufficient funds

are available to pay obligations in a timely manner.

7. Match invoice with PO: Accounts payable should not create a payable without

an open PO. When the PO is used to validate the invoice, it should then be

marked as closed (or linked to the invoice) so that it cannot be used again. If

this process is followed, the second or duplicate invoice would have been

discovered because no PO would match to the invoice.

8. Reconcile run-to-run totals: If the GL is updated as a batch, then a

reconciliation of batch totals, or run-to-run totals, would detect any errors.

P 13-5 ANS. A. GL inventory received update

NOTE : Situations 3–5 do not apply to this flow.

1. Merchandise is purchased, and a periodic inventory process is used.

No entry is made (Note A)

Accounting Information Systems, 10e 45

2.Merchandise is purchased, and a perpetual inventory process is used.

Dr. Clearing account (Note A)

Cr. Accounts payable

Cr. Accounts payable

C. GL cash disbursement update

NOTE: The same entry applies to all five situations

Dr. Accounts payable

Cr. Cash (Note C)

Notes: A. In a periodic inventory system, inventory balances are only calculated

and recorded at the end of each accounting period. However, under a perpetual

system, inventory is recorded as received. Because the vendor invoice is often

46 Solutions for Chapter 13

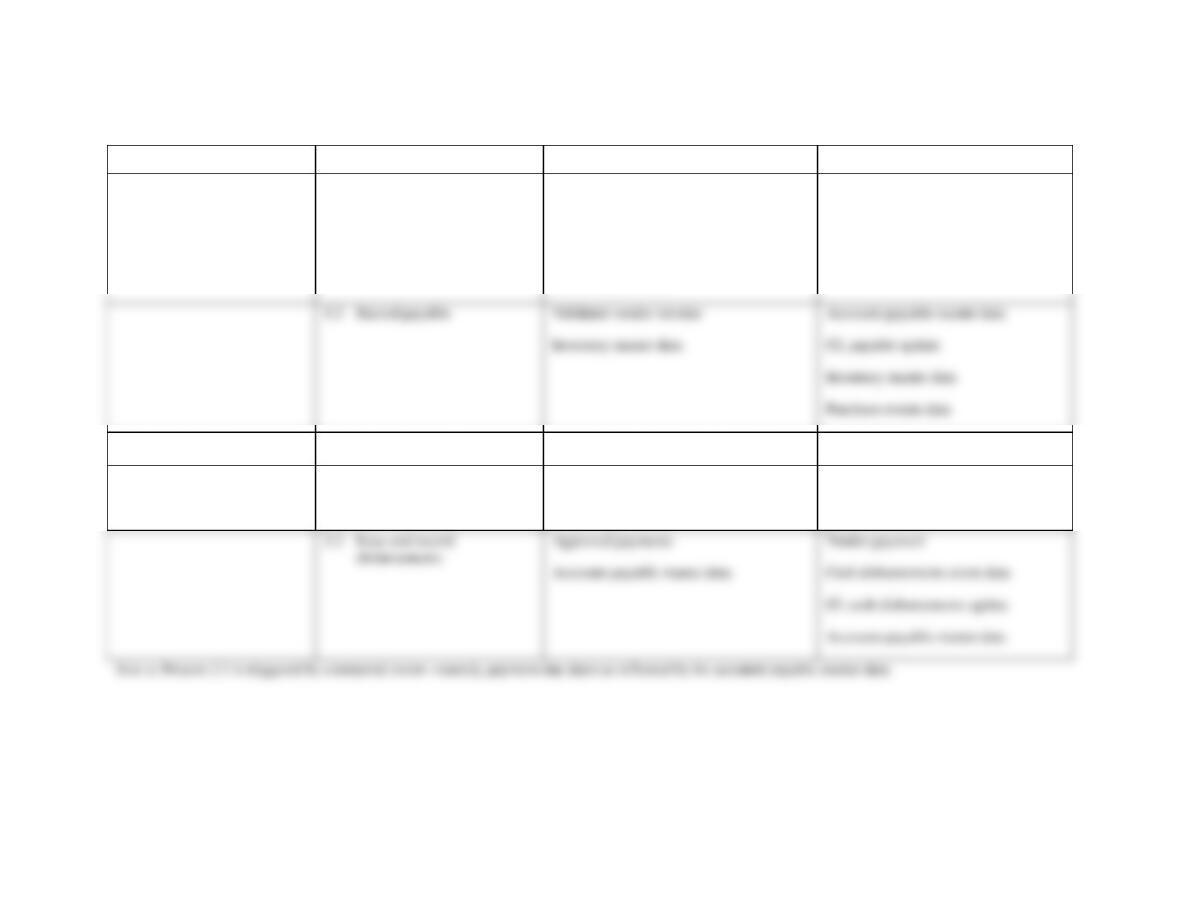

TABLE SM-13.1 Problem 6 Solution—Summary of AP/CD Process’s Processes, Inputs, Outputs, and Data

Process

Subsidiary Functions

Inputs

Outputs

1.0 Establish payable

1.1 Validate invoice

PO accounts payable notification

Receiving report

Vendor invoice

Vendor master data

Validated vendor invoice

Vendor master data

2.0 Make payment

2.1 Prepare proposed payments

Accounts payable master data (Note a)

Proposed payments

2.2 Select and record payments

Proposed payments

Accounts payable master data

Approved payments

Accounts payable master data

Accounting Information Systems, 10e 47

P 13-7 ANS.

1. J 6. I

P 13-8

ANS. Solutions will vary according to the tables selected. However, the following guidelines

should be helpful for grading the solutions:

1. From the file, ensure that the tables are linked in relationships with cardinalities.

2. For the Visio/documentation software diagram, ensure that the symbols used are correct

and the cardinalities are shown.