21

• LBOs undertaken following the 2008 recession have tended to be more conservatively financed than those

prior to 2008

_____________________________________________________________________________________

The realization of sustained earnings growth often requires a sizable initial investment. Investments in software and

other intellectual property must be expensed according to Generally Accepted Accounting Principles resulting in an

immediate reduction in earnings. While certain types of investments can be capitalized and depreciated or amortized

over their useful lives, such spending can depress near term earnings. Similarly, acquisitions made to jump start growth

often have a short-term negative impact on earnings as firms write off acquisition related expenses and incur substantial

post acquisition integration costs.

Firms with successful track records in achieving revenue and earnings growth goals such as Facebook, Google, and

Amazon.com often are able to convince investors to be patient following a major investment. However, firms with poor

track records can get hammered by investors immediately following the announcement of an aggressive investment

program. What options are available for such firms?

One alternative is to take the firm private by consolidating ownership among a few investors patient enough to allow

the firm to realize promised returns. This public to private leveraged buyout (LBO) requires an investor group or

financial sponsor (sometimes involving a firm’s management) using a combination of equity and borrowed funds to

acquire publicly held shares.4 This is exactly what data integrator Informatica did. On August 6, 2015, the firm’s

shares were removed from the NASDAQ, retiring the INFA ticker symbol, following the completion of its acquisition

In 1999, the firm displayed a meteoric price to earnings ratio common among internet firms during the dotcom

bubble enabling the firm to reach a multibillion dollar valuation. However, the firm’s valuation collapsed when the

speculative bubble burst in 2000. It would be years before the firm would again be able to reach its pre-2000 valuation.

Like competitor Tibco, Informatica had seen its revenue growth slow due to market maturation after seeing its stock

soar and then crater. Both firms have since seen their valuations grow to multibillion dollar levels, but it has taken years

to get back to where they were before the dotcom debacle. Tibco was taken private in December 2014 for $4.3 billion.

Under private ownership, Informatica will continue to focus on its main product areas, including cloud services, data

security and “big data” analysis. But the company, with the support of its new backers, will also search for potential

takeover targets as part of an effort to be a consolidator in the fragmented data integration industry. The new owners

will be able to provide financing for future takeovers.

4While public to private LBOs get the most publicity because of their size and visibility, most LBOs involve the

leveraging of private firms. The reasons for this are discussed in detail later in this chapter.

22

Financing for the Informatica LBO consisted of $650,000,000 of 7.125% senior notes due in 2023. The notes are,

fully and unconditionally guaranteed, joint and severally, on a senior unsecured basis by each of the Company’s

Berkshire Hathaway and 3G Buy American Food Icon Heinz

______________________________________________________________________________

Case Study Objectives: To illustrate

• Form of payment, form of acquisition, acquisition vehicle, and post-closing organizations and

• How complex leveraged buyout structures are organized and financed.

______________________________________________________________________________

In a departure from its traditional deal making strategy, Berkshire Hathaway (Berkshire), the giant conglomerate run by

Warren Buffett, announced on February 14, 2013 that it would buy food giant H.J. Heinz (Heinz) for $23 billion or

$72.50 per share in cash. Including assumed debt, the deal is valued at $28 billion. Traditionally, Berkshire had shown

a preference for buying entire firms with established brands and then allowing then allowing them to operate as they

had been. Investors greeted the news enthusiastically boosting Heinz’s stock price by nearly 20% to the offer price and

Berkshire’s class A common stock price by nearly one percent to $148,691 a share.

Unlike prior transactions, Berkshire teamed with 3G Capital Management (3G), a Brazilian-backed investment firm

that owns a majority stake in Burger King, a company whose business is complementary to Heinz, and interests in

other food and beverage companies. Heinz’s headquarters will remain in Pittsburgh, its home for more than 120 years.

At 20 times 2013 current earnings, the deal seems a bit pricey when compared to price to earnings ratios for

comparable firms (See Table 13.4). The risks to the deal are significant. Heinz will have well over $10 billion in debt,

compared to $5 billion now. Before the deal, Moody’s Investors Service rated Heinz just two notches beyond junk. If

future operating performance falters, the firm could be subject to a credit rating downgrade. The need to pay a 9%

preferred stock dividend will also erode cash flow. 3G will have operational responsibility for Heinz. Heinz may be

used as a platform for making other acquisitions.

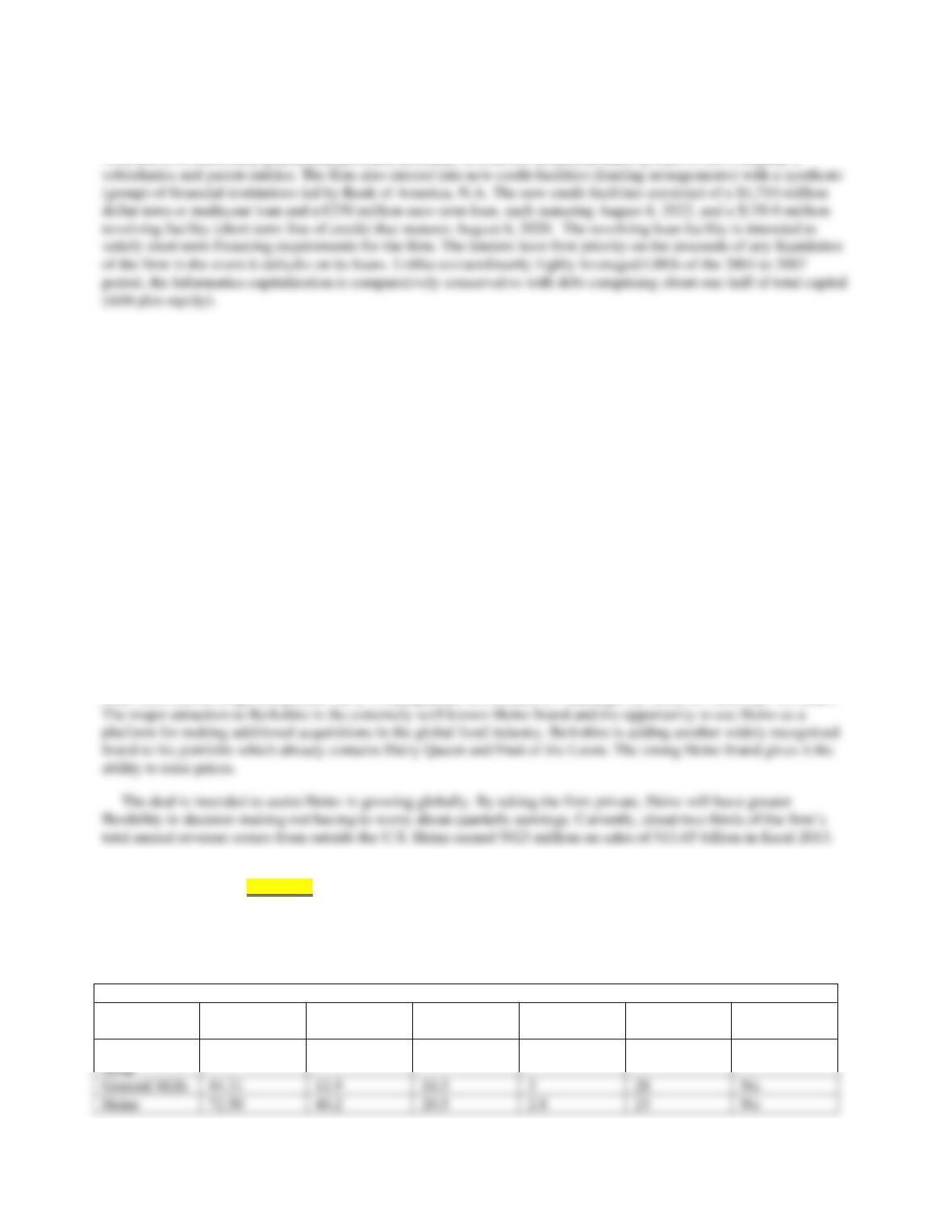

Table 13.4 Food Company Peer Group

Company

Recent price

52 Week

change

2013 Est. P/E

Dividend

Yield

Market Value

($B)

Family Stake

Campbell

$38.72

21.6%

15.2

3.0%

$12

Yes

Hershey

80.89

33.7

22.2

2.1

18

Yes

Hormel Foods

35.91

24

18.4

1.9

9

Yes

Source: Thomson Reuters **since 9/17/12 spinoff

Risk to existing bondholders is that one day they own an investment grade firm with a modest amount of debt and

the next day they own a highly leveraged firm facing a potential downgrade to junk bond status. On the announcement

date, prices of existing Heinz triple B rated bonds fell by over two cents on the dollar, while the cost to ensure such

debt (credit default swaps) soared by over 25% to a new high.

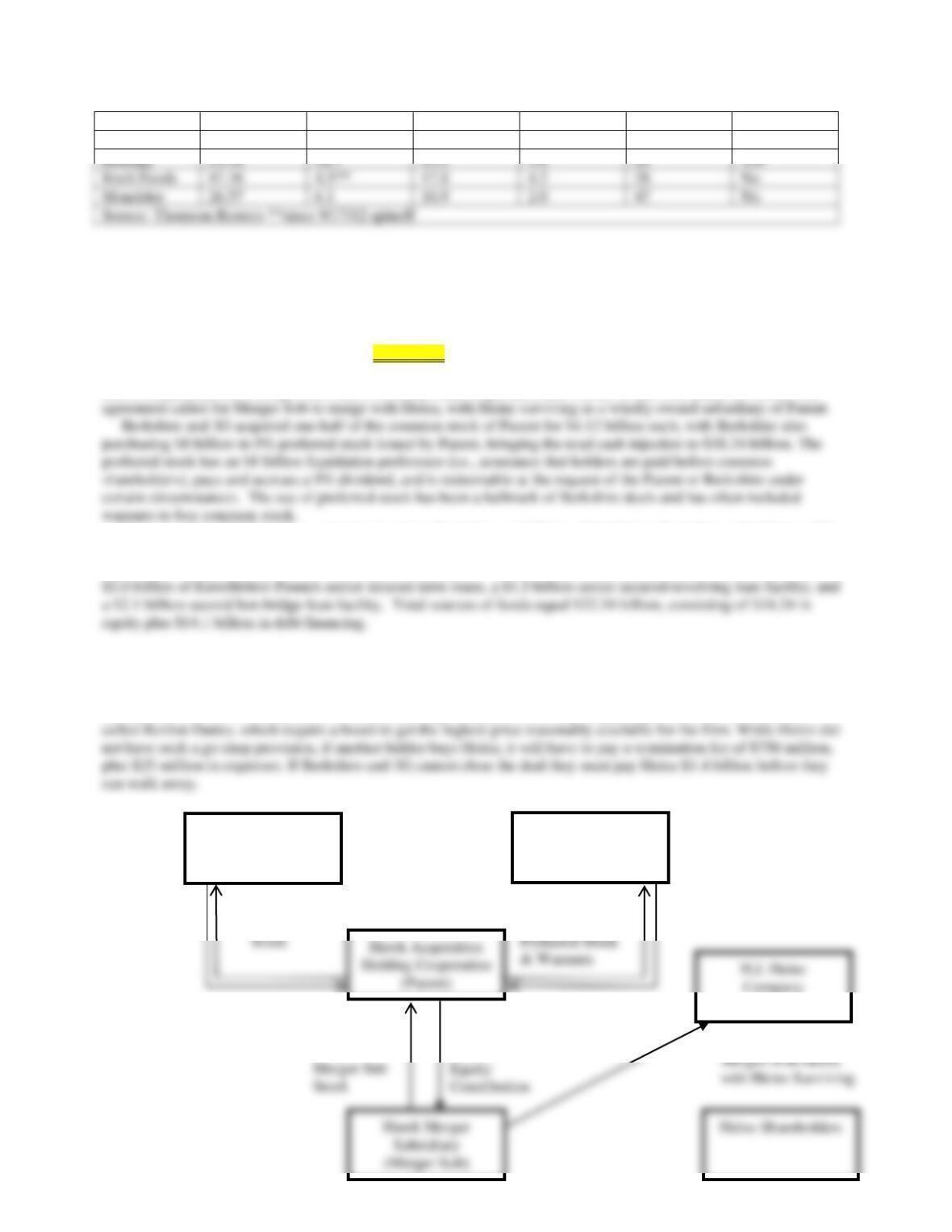

The structure of the deal is described in Figure 13.3. H.J. Heinz Company, a Pennsylvania Corporation, entered

into a definitive merger agreement with Hawk Acquisition Holding Corporation (Parent), a Delaware corporation, and

Hawk Acquisition Sub (Merger Sub), Inc., a Pennsylvania corporation and wholly owned subsidiary of Parent. The

Parent used the $18.24 billion cash injection from Berkshire and 3G (i.e., $14.12 from Berkshire + $4.12 from 3G)

to acquire the common shares of Merger Sub. J.P. Morgan and Wells Fargo provided $14.1 billion of new debt

financing to Merger Sub. The debt financing consisted of $8.5 billion in dollar-denominated senior secured term loans,

The deal does not contain a go shop provision, which allows the target to seek other bids once they have reached

agreement with the initial bidder in exchange for a termination fee to be paid to the initial bidder if the target chooses to

sell to another firm. Go shop provisions may be used since they provide a target’s board with the assurance that it got

the best deal; for firms incorporated in Delaware, the go shop provision helps target argue that they satisfied the so-

H.J. Heinz

$18.24

Billion

Hawk

3G Capital

Management

Berkshire Hathaway

Hawk Merger Sub

$4.12 Billion

Parent

Common

$14.12 Billion

in Parent and

24

Figure 13.3 Berkshire, 3G, and H.J. Heinz Deal Structure

Heinz may not have negotiated a go shop provision which is common in firms seeking to protect their

shareholder interests because it is incorporated in Pennsylvania. Pennsylvania corporate law is intended to give

complete latitude to boards in deciding whether to accept or reject takeover offers because it does not have to consider

shareholders’ interests as the dominant determinant of the appropriateness of the deal (unlike Delaware). Instead, the

Discussion Questions:

1. Identify the form of payment, form of acquisition, acquisition vehicle, and post-closing organization?

Speculate why each may have been used.

Answer: The form of payment was cash, due to its attractiveness to Heinz’s public shareholders. The use of

cash is common in these types of deals. The form of acquisition was the purchase of common stock from

public shareholders, effectively converting Heinz from a public to a private firm. The purchase of stock also

ensured that the acquirer would own all valuable intellectual property owned by Heinz such as product brand

2. How was ownership transferred in this deal? Speculate as to why this structure may have been used?

Answer: The deal structure involved a reverse triangular merger in which Heinz was merged into a wholly

owned subsidiary of Parent, with Heinz surviving. This preserves the Heinz brand name and results in a

holding company structure insulating 3G and Berkshire from Heinz liabilities in the event of bankruptcy. The

use of a subsidiary merger to transfer ownership from the Heinz’s public shareholders to the Parent may also

3. Describe the motivation for Berkshire and 3G to buy Heinz.

Answer: Berkshire saw the business as undervalued, and it fit with the firm’s tendency to invest in firms with

$8.24 Billion

25

4. How will the investors be able to recover the 20% purchase price premium?

Answer: 3G has excellent business connections in Brazil which may enable Heinz to improve its market share

5. Do you believe that Heinz is a good candidate for a leveraged buyout? Explain your answer.

Answer: Yes. In the food manufacturing business for 120 years with a widely recognizable brand, the firm has

a substantial and defensible market share in the United States. Moreover, given the nature of its basic food

6. What do you believe was the purpose of the $1.5 billion senior secured revolving loan facility, and the $2.1

billion second lien bridge loan facility as part of the deal financing package?

Answer: The revolving loan facility is commonly a part of financing such transactions as it provides a source

of financing of short-term working capital requirements and is especially important in meeting unanticipated

7. Why do you believe Berkshire Hathaway wanted to receive preferred rather than common stock in exchange

for its investing $8 billion? Be specific.

Answer: The preferred stock has a $8 billion liquidation preference (i.e., assurance that holders are paid before

common shareholders in the event of liquidation), pays and accrues a 9% dividend (a rate well above

prevailing interest rates at the time), and is redeemable at the request of the Parent or Berkshire under certain

circumstances. The latter factor gives Berkshire management substantial flexibility over the timing of when to

INSIDE M&A: VERIZON FINANCES ITS $130 BILLION BUYOUT OF

VODAFONE’S STAKE IN VERIZON WIRELESS

Key Points

• The timing of buyouts is influenced heavily by equity and credit market conditions.

• To close deals, interim or “bridge financing” often is required and replaced with longer–term or “permanent

financing.”

• How deals are financed can impact a firm’s investment strategy long after the deal is completed.

_____________________________________________________________________________________

In a deal that has been in the making for almost a decade, Verizon Communications agreed to buy British-based

wireless carrier Vodafone’s 45% ownership stake in the Verizon Wireless joint venture corporation for $130 billion.

Formed in 2000, the joint venture serves more than 100 million customers in the United States.

26

Announced on September 2, 2013, the deal marked the crowning event in the careers of Vittorio Colao and Lowell

McAdam, the chief executives of Vodafone and Verizon, respectively. The agreement succeeded in rebuilding relations

between the two firms that had long been strained by clashes about the size of the dividend paid by the JV, matters of

strategy, and who would eventually achieve full ownership.

The timing of the deal reflects the near record low interest rate environment and the strength of Verizon’s own

stock. A higher Verizon share price meant that it would have to issue fewer new shares limiting the potentially dilutive

impact on the firm’s current shareholders. Another major issue was making sure the debt markets could absorb the

sheer amount of new Verizon debt without sending interest rates spiraling upward. The huge increase in Verizon’s

leverage was sure to catch the eye of credit rating agencies charged with evaluating the likelihood that borrowers could

repay their debt on a timely basis. While Verizon’s rating was reduced, it was only one notch from what it had been to

“investment grade,” rating agency jargon for ok for investors to buy.

The record books were shattered when Verizon sold $49 billion in investment grade debt in a single day without

roiling the bond markets. The bond markets absorbed the huge debt issue because of the relative attractiveness of the

yields offered by Verizon. The debt offering included 10-year bonds that yielded 5.3% and 30-year bonds yielding

6.55%. These yields compared to the average BBB-rated industrial bond of 4.16% at the time and BBB bonds for

telecommunications companies averaging 4.34%.

The addition of a massive new debt load on Verizon’s books may tie the company’s hands in making major

investments for some time as its priority during the next several years will be reducing its leverage as quickly as

Hollywood’s Biggest Independent Studios Combine in a Leveraged Buyout

Key Points

LBOs allow buyouts using relatively little cash and often rely heavily on the target firm’s assets to finance the

transaction.

Private equity investors often “cash out” of their investments by selling to a strategic buyer.

______________________________________________________________________________

The Lionsgate-Summit tie-up represented the culmination of more than four years of intermittent discussions between

the two firms. The number of studios making and releasing movies has been shrinking amid falling DVD sales and

27

continued efforts to transition to digital distribution. As the largest independent studios in Hollywood, both firms saw

their cash flow whipsawed as one blockbuster hit would be followed by a series of failures. Film and TV program

libraries offered the only source of cash flow stability due to the recurring fees paid by those licensing the rights to use

this proprietary content.

Lionsgate is a diversified film and television production and distribution company, with a film library of 13,000

titles. The firm’s major distribution channels include home entertainment and prepackaged media (DVDs); digital

distribution (on-demand TV) and pay TV (premium network programming). Summit, also a producer and distributor of

film and TV content, has a less consistent track record in realizing successful releases, with the Twilight “franchise” its

primary success. However, Summit does have strong international licensing operations, with arrangements in the

United States, Canada, Germany, France, Scandinavia, Spain, and Australia. The acquisition also strengthens

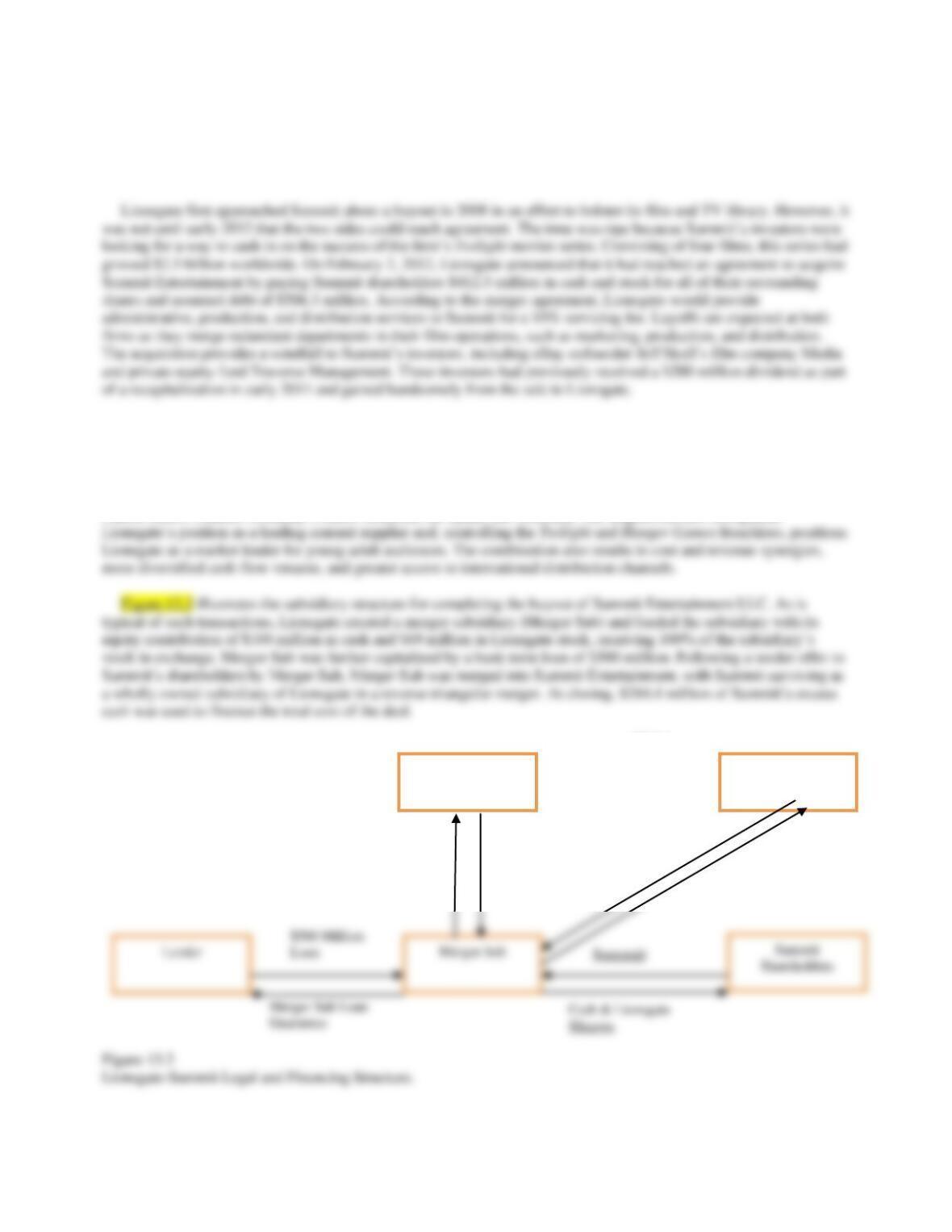

Lionsgate

Entertainment

Summit

Entertainment

Merger

Sub Stock

$100 Million in

Cash & $69

Million in

Lionsgate

Merger Sub Merges

With Summit

$284.4

Million in

Excess

Summit

Cash

Table 13.4 summarizes the sources of financing for the buyout and shows how these funds were used to pay for the

deal. Lionsgate financed the total cost of the deal of $953.4 million (consisting of $412.5 million for Summit stock +

the pretransaction term loan of $506.3 million + $34.6 million in transaction-related fees and expenses) as follows:

$100 million in cash from Lionsgate and $69 million in Lionsgate stock + $284.4 million of the $310 million in cash on

Summit’s balance sheet at closing + a new $500 million term loan. Summit’s $506.3 million term loan B was

Table 13.4

Lionsgate-Summit Transaction Overview

• Sources of Funds ($ Millions)

• Uses of Funds ($ Millions)

Lionsgate Cash Consideration1

100.0

Seller Consideration

412.5

Lionsgate Stock Consideration2

69.0

Repay Term Loan

506.3

Summit Cash on Balance Sheet

284.4

Fees and expenses

34.6

New Term Loan

Summit Pro Forma Capitalization

• As of 12/30/11

• Pro Forma

$ Millions

Adjustment ($ Millions)

$ Millions

Cash3

310

(284.4)

25.6

Revolver ($200 million)

Prior Term Loan B Due 9/2016

New Term Loan B Due 9/2016

Total Debt

Contributed Equity5

169.0

Table 13.5 presents the key features of the new term loan B facility. Note how Summit’s assets are used as collateral

to secure the loan. In addition, the lender has first priority on the proceeds from certain types of transactions, giving

Table 13.5

Initial Terms and Conditions of the New Term Loan B Facility

• Item

• Comment

Borrower

Summit Entertainment LLC (Lionsgate subsidiary)

Guarantor

Merger Sub

Security

First priority security interest in tangible and intangible assets

Pledge of equity interests of Summit and guarantor

29

Facilities

$500 million senior secured term loan B

Ratings

B1/B+

Maturity

September 2016

Mandatory

Amortization

$13.75 million, paid quarterly

Pricing

To be determined

Incremental

Facility

None

Discussion Questions

1. What about Lionsgate’s acquisition of Summit indicates that this transaction should be characterized as a

leveraged buyout? How does Lionsgate use Summit’s assets to help finance the deal? Be specific.

Answer: LBOs are characterized by a substantial increase in a firm’s post-LBO debt-to-equity ratio (a

common measure of leverage), usually as a result of the substantial increase in borrowing to purchase stock

held by its pre-buyout private or public shareholders. However, in some instances, a firm’s leverage increases

even though there is no significant increase in borrowing. This may result from the way in which the target

firm’s assets are used to finance the buyout. For example, the investor group or firm initiating the takeover

.

2. How are $34.6 million in fees and expenses associated with the transaction paid for? Be specific.

3. Speculate as to why Lionsgate refinanced as part of the transaction the existing Summit Term Loan B due in

2016 that had been borrowed in the early 2000s.

Optional

Up to one year at the discretion of the borrower

Permitted

Distributions

No distributions before loan facility is 75% amortized

30

4. Do you believe that Summit is a good candidate for a leveraged buyout? Explain your answer.

5. Why is Summit Entertainment organized as a limited liability company?

6. Why did Lionsgate make an equity contribution in the form of cash and stock to the Merger Sub rather than

making the cash portion of the contributed capital in the form of a loan?

Answer: The financial sponsor or parent firm, in this case Lionsgate, makes an equity contribution so as not to

TXU Goes Private in the Largest Private Equity Transaction in History—The Dark Side of Leverage

Key Points

The 2007/2008 financial crisis left many LBOs excessively leveraged.

As structured, the TXU buyout (now Energy Future Holdings) left no margin for error.

Excessive leverage severely limits the firm’s future financial options.

_____________________________________________________________________________

Before the buyout, TXU, a Dallas-based energy giant, was a highly profitable utility. Historically low interest rates and

an overly optimistic outlook for natural gas prices set the stage for the largest private equity deal in history. The 2007

buyout of TXU was valued at $48 billion and, at the time, appeared to offer such promise that several of Wall Street’s

largest lenders –—including the likes of Lehman Brothers and Citigroup—invested, along with such storied names in

private equity as KKR, TPG, and Goldman Sachs. However, the price of gas plummeted, eroding TXU’s cash flow.

Since the deal closed in October 2007, investors who bought $40 billion of TXU’s debt have experienced losses as high

as 70% to 80% of their value. The other $8 billion used to finance the deal came from the private equity investors,

banks, and large institutional investors. They, too, have suffered huge losses. Having met its obligations to date, the

firm faces a $20 billion debt repayment coming due in 2014.

31

with the transaction be held at the level of the Merger Sub Parent holding company so as not to leverage the utility

further.

Subsequent to closing, the new company was reorganized into independent businesses under a new holding

company, controlled by the Sponsor Group, called Texas Holdings (TH). Merger Sub (which owns TXU) was renamed

Energy Future Holdings. TH’s direct subsidiaries are EFH and Oncor (an energy distribution business formerly held by

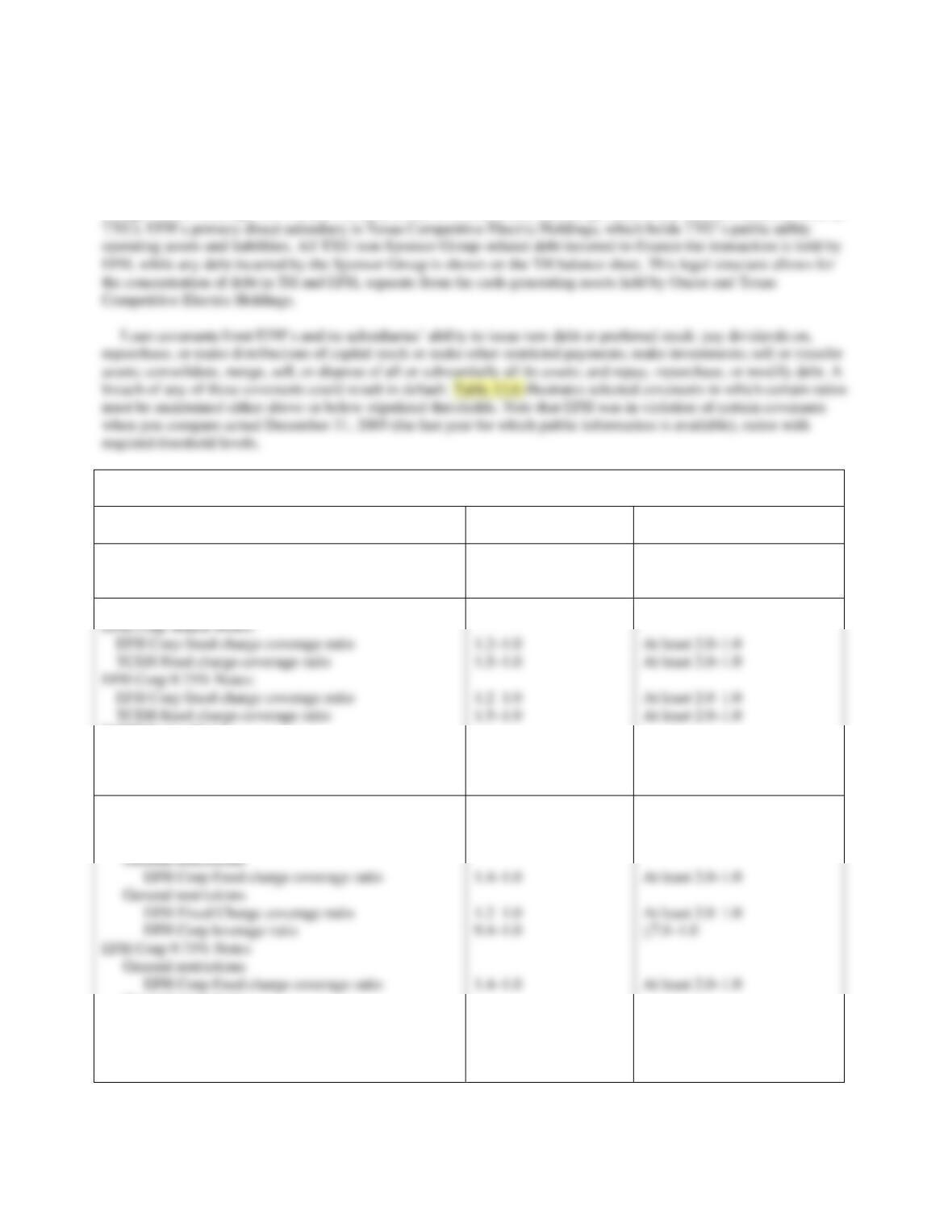

Table 13.6

EFH Holdings Debt Covenants

• December 31,

2009

• Threshold Level as of

December 31, 2009

Maintenance Covenant

TCEH Secured Facilities: Ratio of Secured debt to

adjusted EBITDA

4.76–1.00

Must not exceed 7.25–1.00

Debt Incurrence Covenants

TCEH Senior Notes:

TCEH fixed charge coverage ratio

TCEH Senior Secured Facilities:

TCEH fixed charge coverage ratio

1.5–1.0

1.5–1.0

At least 2.0–1.0

At least 2.0–1.0

Restricted Payments/Limitations on Investments

Covenants

EFH Corp Senior Notes

General restrictions

EFH Corp fixed charge coverage ratio

EFH Corp leverage ratio

TCEH Senior Notes

TCEH fixed charge coverage ratio

1.2–1.0

9.4–1.0

1.5–1.0

At least 2.0–1.0

≤7.0–1.0

At least 2.0–1.0

32

Things clearly have not turned out as expected. The firm faces an almost-untenable capital structure. The firm’s debt

traded at between 20 and 30 cents on the dollar throughout most of 2012. The $8 billion equity invested in the deal has

Discussion Questions

1. How does the postclosing holding company structure protect the interests of the financial sponsor group

and the utility’s customers but potentially jeopardize creditor interests in the event of bankruptcy?

Answer: A holding company structure was used for two reasons: (1) to limit the risks to the financial and

creditor groups to potential liabilities and (2) to satisfy the requirement by Texas public utility regulators

to insulate the public utility from the additional debt service requirements created by the debt incurred to

finance the LBO. The structure effectively concentrates debt in EFH and TH, while separating the cash

producing assets in other legal entities (i.e., Oncor and Texas Competitive Electric Holdings).

Consequently, EFH and TH could be put into Chapter 11 if need be, while limiting creditor access to

Oncor’s and Texas Competitive Electric Holdings’ assets.

2. What was the purpose of the pre-closing covenants and closing conditions as described in the merger

agreement?

Answer: The purpose of the covenants is to ensure that the target firm will operate its business between

the signing of the agreement and closing in a manner acceptable to the buyer. Also, it gives the buyer a

3. Loan covenants exist to protect the lender. How might such covenants inhibit the EFH from meeting its

2014 $20 billion obligations?

33

Answer: The loan covenants limit EFH’s ability to issue new equity, preferred stock, or to take on new

4. As CEO of EFH, would you recommend to the board of directors as an appropriate strategy for paying the

$20 billion in debt that is maturing in 2014?

Answer: The principal owners private equity buyout firms Kohlberg Kravis Roberts & Co (KKR) and

Texas Pacific Group (TPG), two of the nation’s leading private equity firms, and global investment bank

5. The substantial writedown of the net acquired assets in 2008 suggests that the purchase price paid for

TXU was too high. How might this impact KKR, TPG, and Goldman’s ability to earn financial returns

expected by their investors on the TXU acquisition? How might this writedown impact EFH’s ability

meet the $20 billion debt maturing in 2014?

Answer: The purchase price paid for TXU was clearly too high. Private equity investors were caught up in

the euphoria of 2007 when interest rates were exceptionally low and banks were aggressively competing

Lessons from Pep Boys’ Aborted Attempt to Go Private

Key Points

LBOs in recent years have involved financial sponsors’ providing a larger portion of the purchase price in cash than in

the past.

Financial sponsors focus increasingly on targets in which they have previous or related experience.

Deals that would have been completed in the early 2000s are more likely to be terminated or subject to renegotiation

than in the past.

_____________________________________________________________________________________

It ain’t over till it’s over” quipped former New York Yankees’ catcher Yogi Berra, famous for his malapropisms. The

oft–quoted comment was once again proven true in Pep Boys’ unsuccessful attempt to go private in 2012. On May 30,

2012, after nearly two years of discussions between Pep Boys and several interested parties, the firm announced that a

34

to finance a portion of the purchase price. Furthermore, Gores has experience in retailing, having several retailers

among their portfolio of companies, including J. Mendel and Mexx.

The transaction reflected a structure common for deals of this type. Pep Boys had entered into a merger agreement

with Auto Acquisitions Group (the Parent), a shell corporation funded by cash provided by Gores as the financial

sponsor, and the Parent’s wholly owned subsidiary (Merger Sub). The Parent would contribute cash to Merger Sub,

with Merger Sub borrowing the remainder from several lenders. Merger Sub would subsequently buy Pep Boys’

“Grave Dancer” Takes Tribune Corporation Private in an Ill-Fated Transaction

At the closing in late December 2007, well-known real estate investor Sam Zell described the takeover of the Tribune

Company as “the transaction from hell.” His comments were prescient in that what had appeared to be a cleverly

crafted, albeit highly leveraged, deal from a tax standpoint was unable to withstand the credit malaise of 2008. The end

came swiftly when the 161-year-old Tribune filed for bankruptcy on December 8, 2008.

On April 2, 2007, the Tribune Corporation announced that the firm’s publicly traded shares would be acquired in a

multistage transaction valued at $8.2 billion. Tribune owned at that time 9 newspapers, 23 television stations, a 25%

stake in Comcast’s SportsNet Chicago, and the Chicago Cubs baseball team. Publishing accounts for 75% of the firm’s

total $5.5 billion annual revenue, with the remainder coming from broadcasting and entertainment. Advertising and

circulation revenue had fallen by 9% at the firm’s three largest newspapers (Los Angeles Times, Chicago Tribune, and

Newsday in New York) between 2004 and 2006. Despite aggressive efforts to cut costs, Tribune’s stock had fallen more

than 30% since 2005.

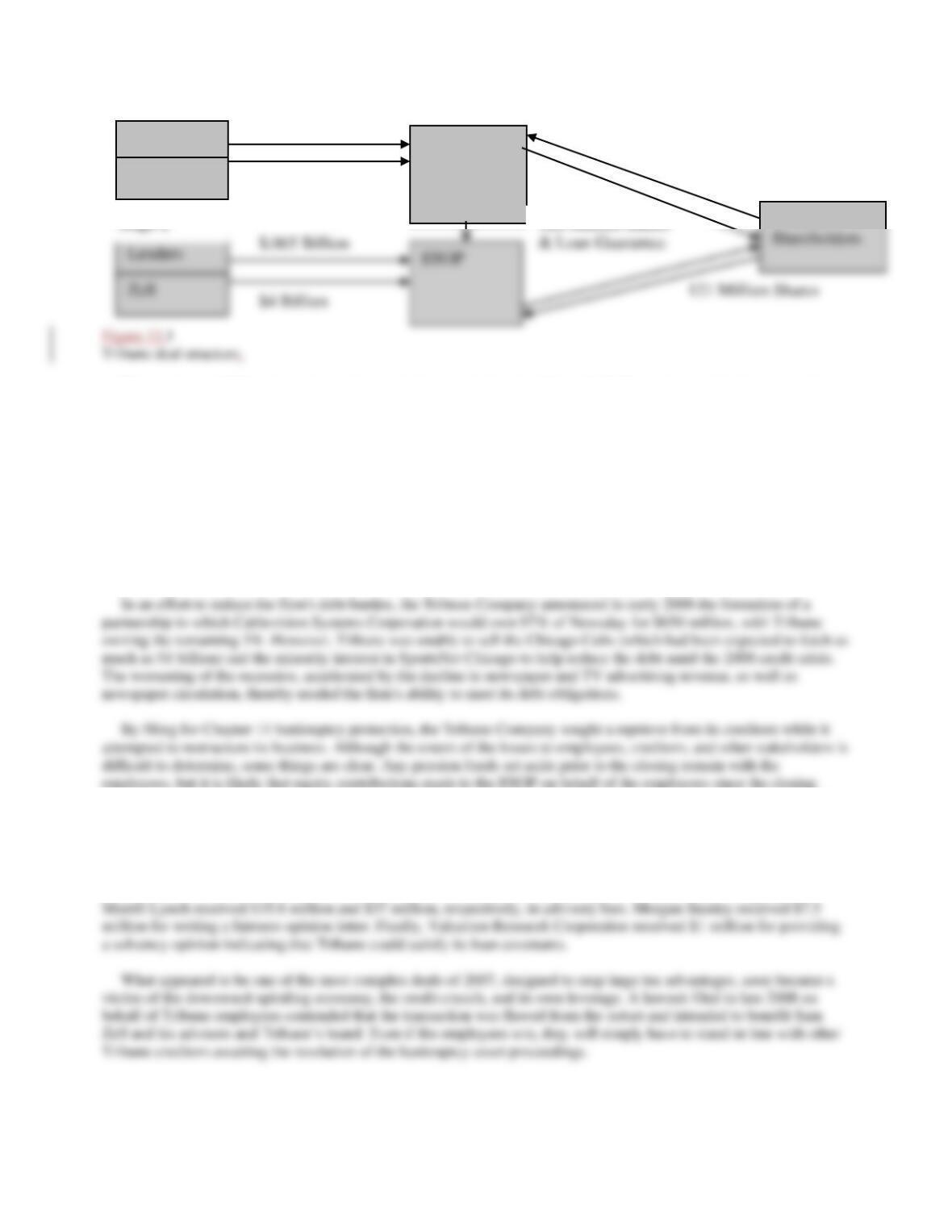

The transaction was implemented in a two-stage transaction, in which Sam Zell acquired a controlling 51% interest

in the first stage followed by a backend merger in the second stage in which the remaining outstanding Tribune shares

were acquired. In the first stage, Tribune initiated a cash tender offer for 126 million shares (51% of total shares) for

Stage 1

$3.85 Billion

35

The purchase of Tribune’s stock was financed almost entirely with debt, with Zell’s equity contribution amounting to

less than 4% of the purchase price. The transaction resulted in Tribune being burdened with $13 billion in debt

(including the approximate $5 billion currently owed by Tribune). At this level, the firm’s debt was ten times EBITDA,

more than two and a half times that of the average media company. Annual interest and principal repayments reached

$800 million (almost three times their preacquisition level), about 62% of the firm’s previous EBITDA cash flow of

$1.3 billion. While the ESOP owned the company, it was not be liable for the debt guaranteed by Tribune.

The conversion of Tribune into a Subchapter S corporation eliminated the firm’s current annual tax liability of $348

million. Such entities pay no corporate income tax but must pay all profit directly to shareholders, who then pay taxes

on these distributions. Since the ESOP was the sole shareholder, Tribune was expected to be largely tax exempt, since

ESOPs are not taxed.

would be lost. The employees would become general creditors of Tribune. As a holder of subordinated debt, Mr. Zell

had priority over the employees if the firm was liquidated and the proceeds distributed to the creditors.

Those benefitting from the deal included Tribune’s public shareholders, including the Chandler family, which owed

12% of Tribune as a result of its prior sale of the Times Mirror to Tribune, and Dennis FitzSimons, the firm’s former

CEO, who received $17.7 million in severance and $23.8 million for his holdings of Tribune shares. Citigroup and

Discussion Questions:

Lenders

Zell

Tribune

Tribune

$.25 billion

126 Million Shares

$4.2 Billion

Lenders

Zell

$4 Billion

121 Million Shares

36

1. What is the acquisition vehicle, post-closing organization, form of payment, form of acquisition, and tax

strategy described in this case study?

Answer: The ESOP is the acquisition vehicle and the subchapter S corporation is the post-closing

2. Describe the firm’s strategy to finance the transaction?

Answer: The transaction will be financed primarily by debt. The firm’s free cash flow will be improved by

3. Is this transaction best characterized as a merger, acquisition, leveraged buyout, or spin-off? Explain your

answer.

4. Is this transaction taxable or non–taxable to Tribune’s public shareholders? To its post-transaction

shareholders? Explain your answer.

5. Comment on the fairness of this transaction to the various stakeholders involved. How would you apportion

the responsibility for the eventual bankruptcy of Tribune among Sam Zell and his advisors, the Tribune board,

and the largely unforeseen collapse of the credit markets in late 2008? Be specific.

Answer: The transaction was clearly highly leveraged by most measures. It was financed almost entirely with

debt, with Zell’s equity contribution amounting to less than 4 percent of the purchase price. The transaction

resulted in the Tribune being burdened with $13 billion in debt (including the approximate $5 billion currently

Financing LBOs—The SunGard Transaction

With their cash hoards accumulating at an unprecedented rate, there was little that buyout firms could do but to invest

in larger firms. Consequently, the average size of LBO transactions grew significantly during 2005. In a move

reminiscent of the blockbuster buyouts of the late 1980s, seven private investment firms acquired 100 percent of the

outstanding stock of SunGard Data Systems Inc. (SunGard) in late 2005. SunGard is a financial software firm known

for providing application and transaction software services and creating backup data systems in the event of disaster.

The company‘s software manages 70 percent of the transactions made on the Nasdaq stock exchange, but its biggest

business is creating backup data systems in case a client’s main systems are disabled by a natural disaster, blackout, or

37

terrorist attack. Its large client base for disaster recovery and back-up systems provides a substantial and predictable

cash flow.

SunGard’s new owners include Silver lake Partners, Bain Capital LLC, The Blackstone Group L.P., Goldman Sachs

Capital Partners, Kohlberg Kravis Roberts & Co., Providence Equity Partners Inc. and Texas Pacific Group. Buyout

firms in 2005 tended to band together to spread the risk of a deal this size and to reduce the likelihood of a bidding war.

Indeed, with SunGard, there was only one bidder, the investor group consisting of these seven firms.

The software side of SunGard is believed to have significant growth potential, while the disaster-recovery side

provides a large stable cash flow. Unlike many LBOs, the deal was announced as being all about growth of the

The buyout represented potentially a significant source of fee income for the investor group. In addition to the 2

percent management fees buyout firms collect from investors in the funds they manage, they receive substantial fee

income from each investment they make on behalf of their funds. For example, the buyout firms receive a 1 percent

deal completion fee, which is more than $100 million in the SunGard transaction. Buyout firms also receive fees paid

for by the target firm that is “going private” for arranging financing. Moreover, there are also fees for conducting due

diligence and for monitoring the ongoing performance of the firm taken private. Finally, when the buyout firms exit

their investments in the target firm via a sale to a strategic buyer or a secondary IPO, they receive 20 percent (i.e., so-

called carry fee) of any profits.

The seven equity investors provided $3.5 billion in capital with the remainder of the purchase price financed by

commitments from a lending consortium consisting of Citigroup, J.P. Morgan Chase & Co., and Deutsche Bank. The

purpose of the loans is to finance the merger, repay or refinance SunGard’s existing debt, provide ongoing working

capital, and pay fees and expenses incurred in connection with the merger. The total funds necessary to complete the

merger and related fees and expenses is approximately $11.3 billion, consisting of approximately $10.9 billion to pay

SunGard’s stockholders and about $400.7 million to pay fees and expenses related to the merger and the financing

arrangements. Note that the fees that are to be financed comprise almost 4 percent of the purchase price. Ongoing

working capital needs and capital expenditures required obtaining commitments from lenders well in excess of $11.3

billion.

The merger financing consists of several tiers of debt and “credit facilities.” Credit facilities are arrangements for

extending credit. The senior secured debt and senior subordinated debt are intended to provide “permanent” or long–

term financing. Senior debt covenants included restrictions on new borrowing, investments, sales of assets, mergers

and consolidations, prepayments of subordinated indebtedness, capital expenditures, liens and dividends and other

distributions, as well as a minimum interest coverage ratio and a maximum total leverage ratio.

38

The following table provides SunGard’s post-merger proforma capital structure. Note that the proforma capital

structure is portrayed as if SunGard uses 100 percent of bank lending commitments. Also, note that individual LBO

SunGard Proforma Capital Structure

Pre-Merger Existing SunGard Debt Outstanding $Millions

Senior Notes (3.75% due in 2009) 250,000,000

Senior Notes (4.785 due in 2014) 250,000,000

6 year term

$4 billion term loan maturing in 7-1/2 years

Senior Subordinated Notes (≤$3 billion) 3,000,000,000

Equity Portion of Merger Financing

Equity Investor Commitment ($Millions)

Silver Lake Partners II, LP1 540,000,000

Bain Capital Fund VIII, LP 540,000,000

Blackstone Capital Partners IV, L.P. 270,000,000

Blackstone Communications Partners I, L.P. 270,000,000

1The roman numeral II refers to the fund providing the equity capital managed by the

partnership.

Case Study Discussion Questions:

1. SunGard is a software company with relatively few tangible assets. Yet, the ratio of debt to equity of almost 5

to 1. Why do you think lenders would be willing to engage in such a highly leveraged transaction for a firm of

this type?

2. Under what circumstances would SunGard refinance the existing $500 million in outstanding senior debt after

the merger? Be specific.

3. In what ways is this transaction similar to and different from those that were common in the 1980s? Be

specific.

39

Answer: In the 1980s, few hi-tech companies were taken private due to their lack of tangible assets and high

4. Why are payment-in-kind securities (e.g., debt or preferred stock) particularly well suited for financing LBOs?

Under what circumstances might they be most attractive to lenders or investors?

5. Explain how the way in which the LBO is financed affects the way it is operated and the timing of when

equity investors choose to exit the business. Be specific.

Answer: The greater the leverage and non-PIK debt the greater the need to manage the business for cash and

HCA’S LBO REPRESENTS A HIGH-RISK BET ON GROWTH

While most LBOs are predicated on improving operating performance through a combination of aggressive cost cutting

and revenue growth, HCA laid out an unconventional approach in its effort to take the firm private. On July 24, 2006,

management again announced that it would “go private” in a deal valued at $33 billion including the assumption of

$11.7 billion in existing debt.

The approximate $21.3 billion purchase price for HCA’s stock was financed by a combination of $12.8 billion in

senior secured term loans of varying maturities and an estimated $8.5 billion in cash provided by Bain Capital, Merrill

Lynch Global Private Equity, and Kohlberg Kravis Roberts & Company. HCA also would take out a $4 billion

revolving credit line to satisfy immediate working capital requirements. The firm publicly announced a strategy of

improving performance through growth rather than through cost cutting. HCA’s network of 182 hospitals and 94

Discussion Questions:

1. Does a hospital or hospital system represent a good or bad LBO candidate? Explain your answer.

Answer: Hospitals generally represent bad candidates. Hospital cash flow is heavily dependent on

government reimbursement rates which are likely to be declining in the future as the U.S. government