13-1

CHAPTER 13

Financial Statement Analysis

OVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated

Time in

Learning Objectives Exercises Minutes Level

Module 1

1. Explain the various limitations and considerations in financial

statement analysis.

Module 2

4. Compute and use various ratios to assess liquidity. 1 10 Mod

2 15 Mod

3 10 Mod

Module 3

5. Compute and use various ratios to assess solvency. 8 20 Mod

9 20 Mod

10 10 Mod

Module 4

6. Compute and use various ratios to assess profitability. 11 15 Mod

12 15 Mod

13-2 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Problems Estimated

and Time in

Learning Objectives Alternates Minutes Level

Module 1

1. Explain the various limitations and considerations in financial

statement analysis.

Module 2

4. Compute and use various ratios to assess liquidity. 1 40 Mod

2 40 Mod

5* 30 Mod

7* 40 Mod

Module 3

5. Compute and use various ratios to assess solvency. 1** 30 Mod

2** 30 Mod

CHAPTER 13 • FINANCIAL STATEMENT ANALYSIS 13-3

Estimated

Time in

Learning Objectives Cases Minutes Level

Module 1

1. Explain the various limitations and considerations in financial

statement analysis.

6 45 Mod

Module 2

4. Compute and use various ratios to assess liquidity. 4* 45 Mod

5* 45 Mod

7* 45 Diff

8 20 Mod

Module 3

Module 4

13-4 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISES

LO 4 EXERCISE 13-1 WORKING BACKWARD: CURRENT RATIO

The current ratio on December 31, 2015, is $120,000/$100,000 = 1.20. The ratio in-

creased during 2016 by 25%; thus, the ratio at the end of 2016 is 1.20 × 125% = 1.50.

Current liabilities are $140,000 at the end of 2016; thus, current assets are $140,000 ×

1.50 = $210,000.

LO 4 EXERCISE 13-2 ACCOUNTS RECEIVABLE ANALYSIS

1. Accounts receivable turnover:

2. Number of days’ sales in receivables:

3. The average age of a receivable in 2015 was the same number of days as the max-

imum credit period of 60 days. The average age in 2016 of 75 days, however, is sig-

nificantly in excess of the credit period. The company needs to investigate this

LO 4 EXERCISE 13-3 WORKING BACKWARD: ACCOUNTS RECEIVABLE ANALYSIS

The average time to collect accounts receivable is 30 days plus 15 days = 45 days. This

CHAPTER 13 • FINANCIAL STATEMENT ANALYSIS 13-5

LO 4 EXERCISE 13-4 INVENTORY ANALYSIS

1. Inventory turnover:

Cost of goods sold/Average inventory:

2. Number of days’ sales in inventory:

3. Inventory turnover has declined dramatically from the prior year. Many different ex-

planations are possible for this decline, such as problems in the sales effort, over-

pricing of the products relative to the competition, or inferior produce. Management

LO 4 EXERCISE 13-5 ACCOUNTS RECEIVABLE AND INVENTORY ANALYSES FOR

KELLOGG’S AND GENERAL MILLS

1. Calculations (all dollar amounts in millions):

a. Accounts receivable turnover ratio:

Kellogg’s

$14,580/[($1,276 + $1,424)/2] = $14,580/$1,350 = 10.8 times

General Mills

$17,909.6/[($1,483.6 + $1,446.4)/2] = $17,909.6/$1,465 = 12.2 times

13-6 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 13-5 (Concluded)

d. Number of days’ sales in inventory:

Kellogg’s

e. Cash-to-cash operating cycle:

Kellogg’s

33.3 + 48.0 = 81.3 days

2. General Mills has a slightly higher accounts receivable turnover ratio than Kellogg’s

and therefore a lower number of days’ sales in receivables. The two companies

LO 4 EXERCISE 13-6 LIQUIDITY ANALYSES FOR KELLOGG’S AND GENERAL MILLS

1. Calculations (all dollar amounts in millions):

Kellogg’s General Mills

a. Current ratio $3,340/$4,364 = 0.77 to 1 $4,393.5/$5,423.5 = 0.81 to 1

2. Cash flows from operations to current liabilities ratio:

= Net Cash Provided by Operating Activities/Average Current Liabilities

3. The two companies’ ratios are similar; General Mills has a slightly higher current ratio

and quick ratio. The cash flow from operations to current liabilities is also similar for the

two companies. Based on these ratios, the liquidity of the two companies is similar.

CHAPTER 13 • FINANCIAL STATEMENT ANALYSIS 13-7

LO 4 EXERCISE 13-7 LIQUIDITY ANALYSES FOR MCDONALD’S AND WENDY’S

1. Calculations:

McDonald’s Wendy’s

= 1.52 = 1.65

c. Quick assets $2,077.9 + $1,214.4 $267,276 + $73,358

= 1.20 = 1.00

2. Wendy’s current ratio is slightly higher than McDonald’s, but McDonald’s has a

slightly higher quick ratio. Both companies appear to be relatively liquid, with quick

ratios of at least 1.0.

LO 5 EXERCISE 13-8 SOLVENCY ANALYSES FOR NORDSTROM, INC.

1. Calculations (all dollar amounts are in millions):

For the year ended For the year ended

January 31, 2015 February 1, 2014

a. Debt-to-equity ratio ($9,245 – $2,440)*/$2,440 ($8,574 – $2,080)*/$2,080

$6,805/$2,440 $6,494/$2,080

c. Debt service

coverage ratio ($1,220 + $152 + ($1,320 + $170 +

$391)/($152 + $7) $445)/($170 + $407)

= $1,763/$159 = $1,935/$577

= 11.09 times = 3.35 times

13-8 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 13-8 (Concluded)

2. All four ratios indicate that Nordstrom is highly solvent. The company’s debt-to-

equity ratio decreased during the year, and the debt service coverage ratio in-

creased significantly.

LO 5 EXERCISE 13-9 SOLVENCY ANALYSIS

1. a. Debt-to-equity ratio: Total liabilities/Total stockholders’ equity

At 12/31/16: ($350,000 + $600,000)/$1,650,000

= 3.93 to 1

c. Debt service coverage for 2016 (Cash flows from operations before interest and

tax payments)/Interest and principal payments:

($185,000 + $89,000 + $96,000*)/($89,000 + $275,000**)

2. The company’s debt-to-equity ratio has decreased because of the repayment of the

short-term notes and the installment payment on the serial bonds. The ratio at the

end of 2016 of almost 0.6 to 1 indicates a relatively conservative balance of debt to

stockholders’ equity. The times interest earned ratio indicates that Impact’s profits

before interest and taxes were almost four times the amount of interest expense.

CHAPTER 13 • FINANCIAL STATEMENT ANALYSIS 13-9

LO 5 EXERCISE 13-10 WORKING BACKWARD: DEBT SERVICE COVERAGE

Madison’s cash flow from operations can be determined by solving for X in the debt ser-

vice coverage ratio formula:

LO 6 EXERCISE 13-11 PROFITABILITY ANALYSIS FOR APPLE, INC.

1. Apple’s return on common stockholders’ equity ratio (amounts in millions):

2. Return on assets is a ratio needed to decide if Apple is successfully employing lev-

LO 6 EXERCISE 13-12 WORKING BACKWARD: PROFITABILITY ANALYSIS

1. Murphy’s profit margin was 5%, and net income was $250,000. Therefore, net sales

were $250,000/0.05 = $5,000,000.

13-10 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 6 EXERCISE 13-13 RETURN ON STOCKHOLDERS’ EQUITY

Rogers’ stockholders’ equity at the end of 2015 was ($2 × 500,000) + $1,800,000 =

LO 6 EXERCISE 13-14 RETURN RATIOS AND LEVERAGE

1. Ratios:

a. Return on Sales = (Net Income + Interest Expense, Net of Tax)/Net Sales

= [$60,000 + ($50,000 × 60%)]/$650,000

= $90,000/$650,000 = 13.85%

c. Return on Assets = (Net Income + Interest Expense, Net of Tax)/Average Total

Assets

= $90,000 [from part (a)]/$1,800,000 [from part (b)] = 5%

CHAPTER 13 • FINANCIAL STATEMENT ANALYSIS 13-11

EXERCISE 13-14 (Concluded)

2. Evergreen has not been successful in using outside funds because the return on

stockholders’ equity of 3.75% is less than the return to all providers of capital, as

measured by the return on assets of 5%.

LO 6 EXERCISE 13-15 RELATIONSHIPS AMONG RETURN ON ASSETS, RETURN ON

SALES, AND ASSET TURNOVER

Case 1. Return on Assets = Net Income (assuming no interest expense)/Average

Total Assets = $10,000/$60,000 = 16.67%

Case 4. Asset Turnover = Net Sales/Average Total Assets

1.25 = $50,000/X

Average Total Assets = $40,000

Return on Assets = Net Income (assuming no interest expense)/Average

Total Assets

13-12 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 6 EXERCISE 13-16 EPS, P/E RATIO, AND DIVIDEND RATIOS

1. Ratios:

a. Earnings per Common Share = (Net Income – Preferred Dividends)/Number of

Common Shares Outstanding

= [$1,300,000 – 8%($5,000,000)]/400,000 shares

2. An investment advisor needs to be aware of industry trends, the general economic

environment, the historical performance of the company, the investor’s attitudes

about risk, and any other relevant data needed to make an informed decision.

CHAPTER 13 • FINANCIAL STATEMENT ANALYSIS 13-13

MULTI-CONCEPT EXERCISES

LO 2,3 EXERCISE 13-17 COMMON-SIZE BALANCE SHEETS AND HORIZONTAL

ANALYSIS

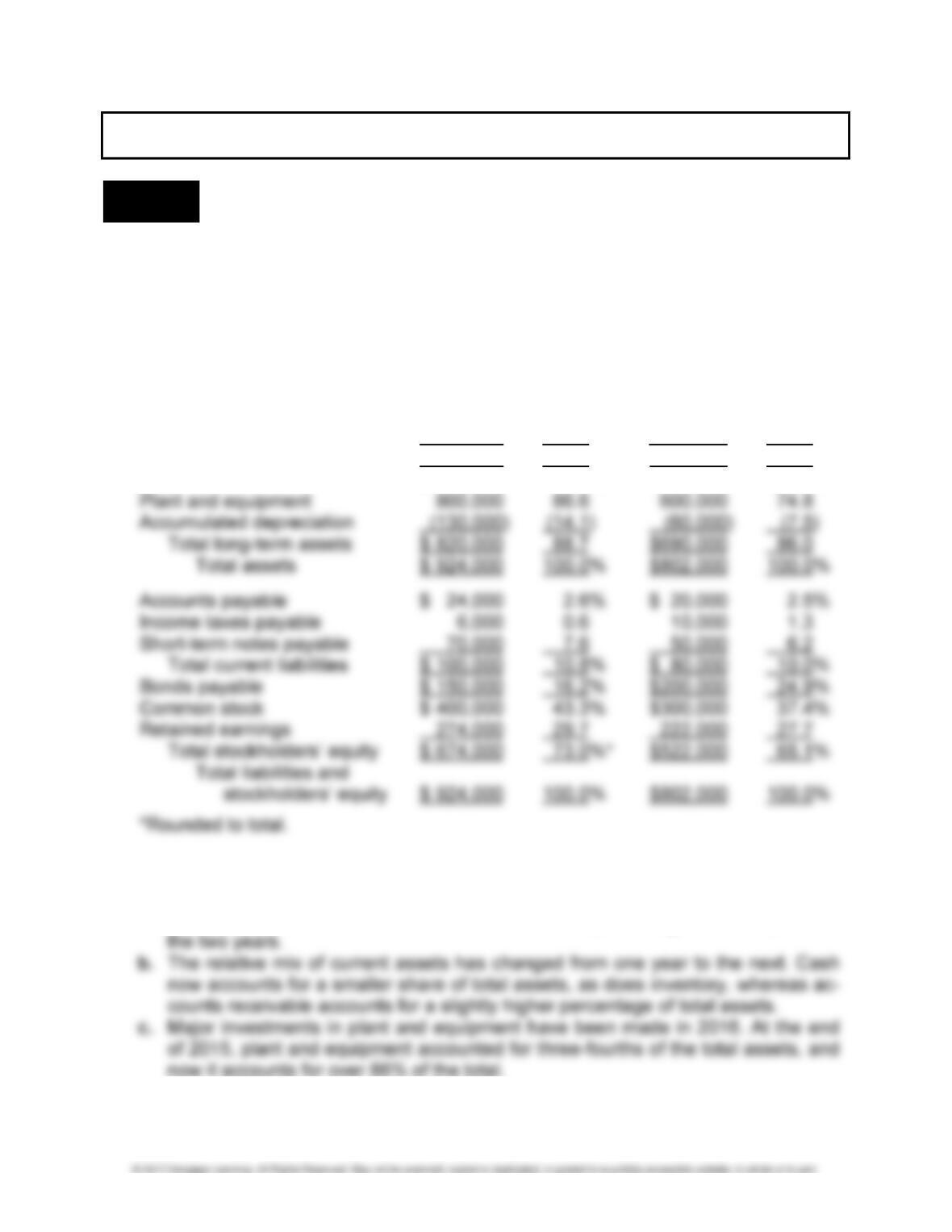

1. FARINET COMPANY

COMMON-SIZE COMPARATIVE BALANCE SHEETS

DECEMBER 31, 2016 AND 2015

12/31/16 12/31/15

Dollars Percent Dollars Percent

Cash $ 16,000 1.7%* $ 20,000 2.5%*

Accounts receivable 40,000 4.3 30,000 3.8

Inventory 30,000 3.3 50,000 6.2

Prepaid rent 18,000 2.0 12,000 1.5

Total current assets $ 104,000 11.3% $112,000 14.0%

Land $ 150,000 16.2% $150,000 18.7%

2. Observations from Farinet’s common-size balance sheets:

a. Current assets as a percentage of total assets has decreased. At the same time,

current liabilities has accounted for about the same percentage of total equities in

13-14 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 13-17 (Concluded)

d. Bonds payable now make up a smaller share of the capital structure with the re-

3. FARINET COMPANY

COMPARATIVE BALANCE SHEETS

DECEMBER 31, 2016 AND 2015

December 31 Increase (Decrease)

2016 2015 Dollars Percent

Cash $ 16,000 $ 20,000 $ (4,000) (20)%

Accounts receivable 40,000 30,000 10,000 33

Inventory 30,000 50,000 (20,000) (40)

Prepaid rent 18,000 12,000 6,000 50

4. Largest changes Refer to

a. Accumulated depreciation Fixed asset records, showing

additions to plant and equipment

CHAPTER 13 • FINANCIAL STATEMENT ANALYSIS 13-15

LO 2,3 EXERCISE 13-18 COMMON-SIZE INCOME STATEMENTS AND HORIZONTAL

ANALYSIS

1. MARINERS CORP.

COMMON-SIZE COMPARATIVE INCOME STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2016 AND 2015

(IN THOUSANDS OF DOLLARS)

2016 2015

Dollars Percent Dollars Percent

Sales revenue $60,000 100.0% $50,000 100.0%

Cost of goods sold 42,000 70.0 30,000 60.0

2. Observations from Mariners’ common-size statements:

a. Although sales increased in absolute dollars, the gross profit percentage has de-

creased significantly because of a higher ratio of cost of goods sold to sales:

from 60% to 70%.

EXERCISE 13-18 (Concluded)

3. MARINERS CORP.

COMPARATIVE STATEMENTS OF INCOME

FOR THE YEARS ENDED DECEMBER 31, 2016 AND 2015

Increase (Decrease)

2016 2015 Dollars Percent

Sales revenue $60,000 $50,000 $10,000 20%

4. Largest changes Refer to

Selling and administrative Individual records, for the

PROBLEMS

LO 4 PROBLEM 13-1 EFFECT OF TRANSACTIONS ON WORKING CAPITAL, CURRENT

RATIO, AND QUICK RATIO

1. Calculation of working capital, current ratio, and quick ratio (dollar amounts in

thousands):

Working capital

CHAPTER 13 • FINANCIAL STATEMENT ANALYSIS 13-17

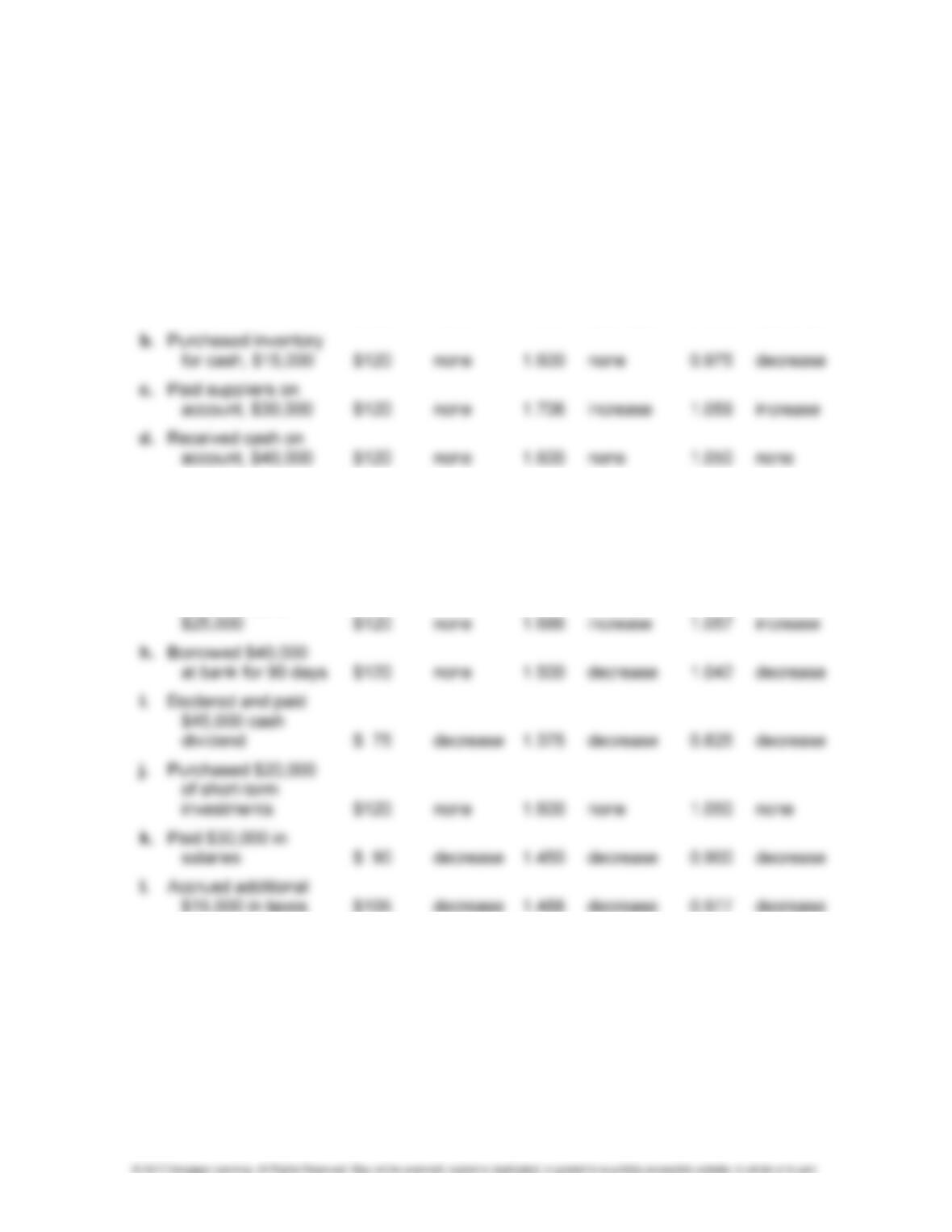

PROBLEM 13-1 (Concluded)

2. Effect of transactions on working capital, current ratio, and quick ratio:

Working Effect Effect Effect

Capital of of of

(in Thou- Trans- Current Trans- Quick Trans-

Transaction sands) action Ratio action Ratio action

a. Purchased inventory

on account,

$20,000 $120 none 1.545 decrease 0.955 decrease

e. Paid insurance for

next year, $20,000 $120 none 1.600 none 0.950 decrease

f. Made sales on

account, $60,000 $180 increase 1.900 increase 1.350 increase

g. Repaid short-term

loans at bank,

13-18 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

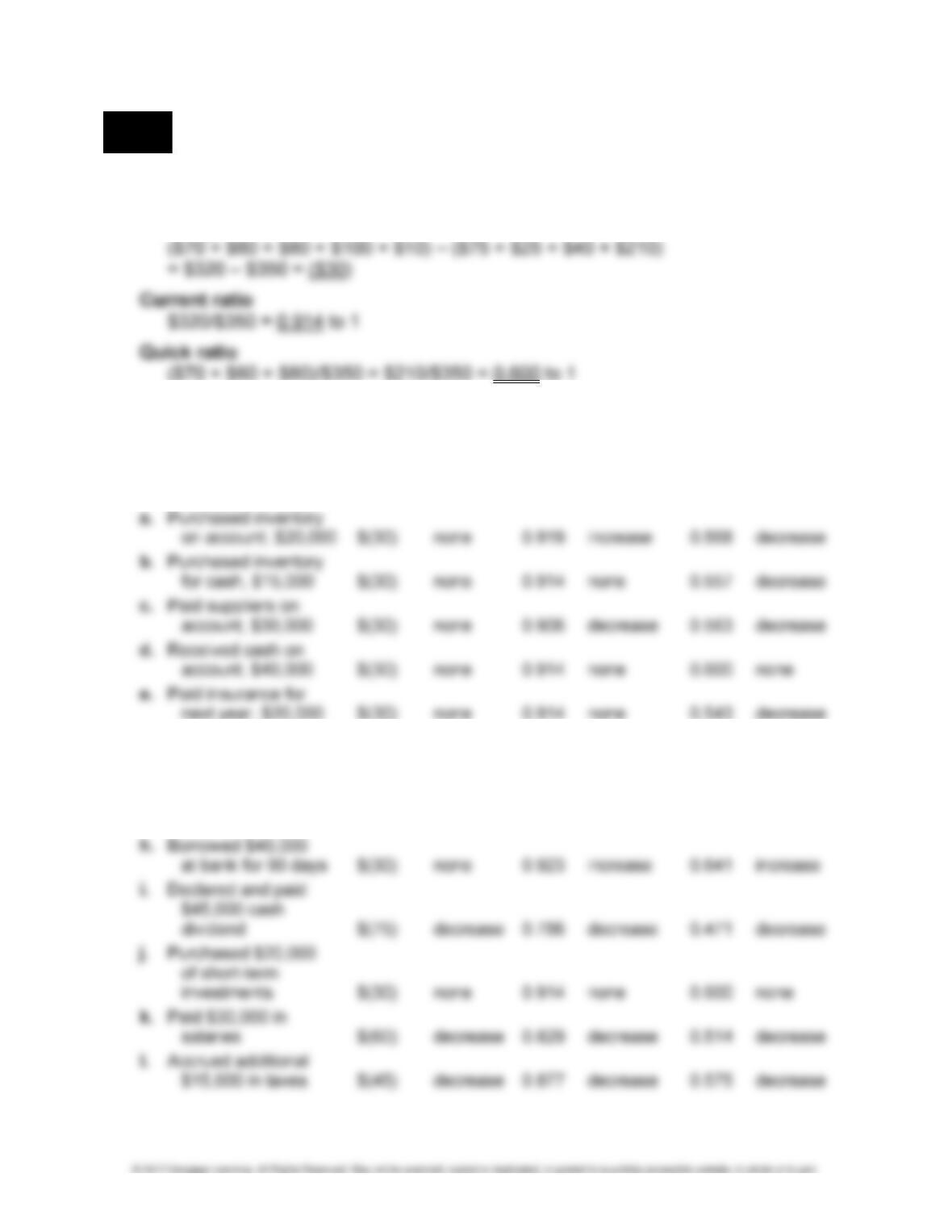

LO 4 PROBLEM 13-2 EFFECT OF TRANSACTIONS ON WORKING CAPITAL, CURRENT

RATIO, AND QUICK RATIO

1. Calculation of working capital, current ratio and quick ratio (dollar amounts in

thousands):

Working capital

2. Effect of transactions on working capital, current ratio, and quick ratio:

Working Effect Effect Effect

Capital of of of

(in Thou- Trans- Current Trans- Quick Trans-

Transaction sands) action Ratio action Ratio action

f. Made sales on

account, $60,000 $ 30 increase 1.086 increase 0.771 increase

g. Repaid short-term

loans at bank,

$25,000 $(30) none 0.908 decrease 0.569 decrease

CHAPTER 13 • FINANCIAL STATEMENT ANALYSIS 13-19

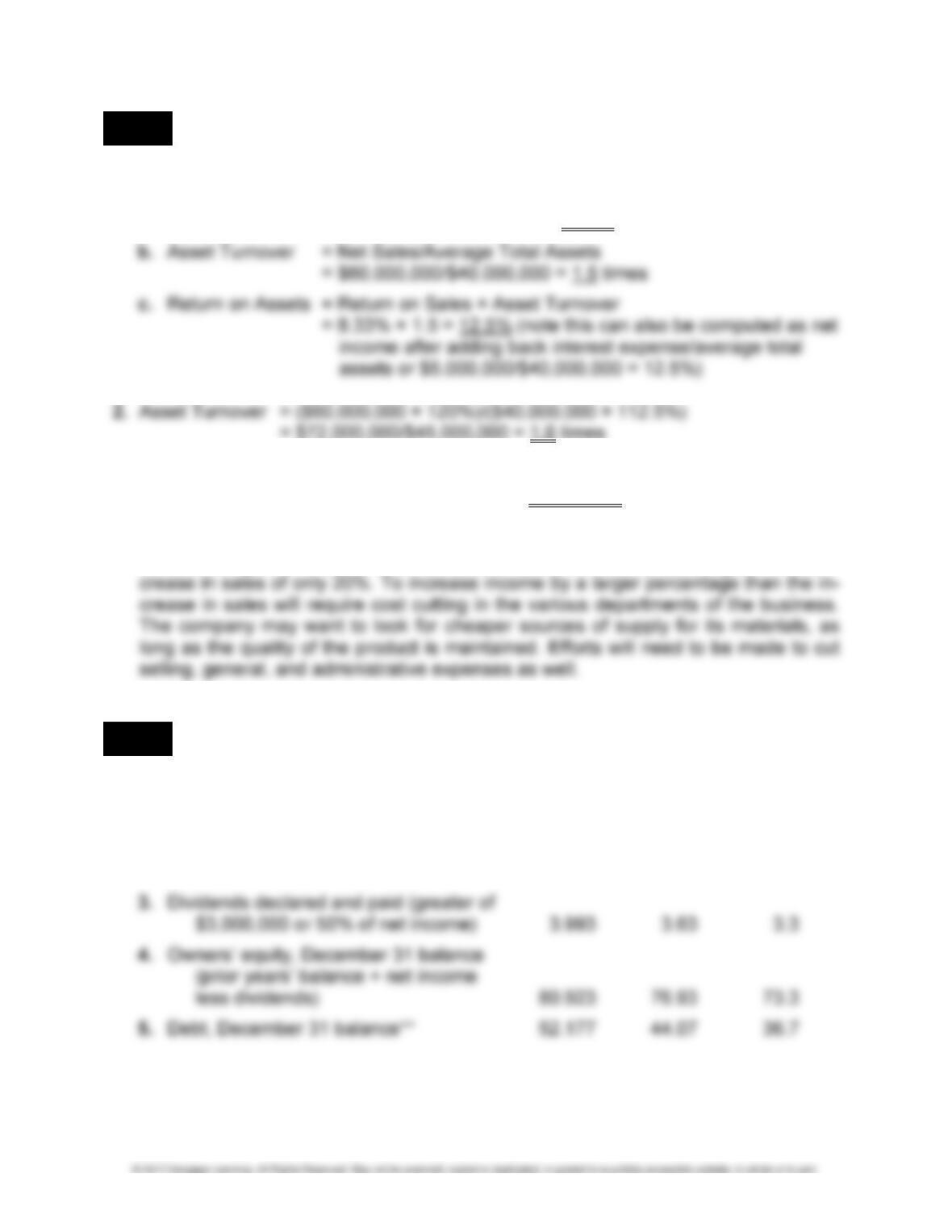

LO 6 PROBLEM 13-3 GOALS FOR SALES AND RETURN ON ASSETS

1. a. Return on Sales = Net Income (after adding back interest expense, net of tax)

/Net Sales

= $5,000,000/$60,000,000 = 8.33%

3. If average total assets are $45,000,000 and the goal is a 15% return on assets, net

income will need to be 15% of $45,000,000, or $6,750,000.

4. Income will have to increase by 35%, ($6,750,000 – $5,000,000)/$5,000,000, to

achieve the goal of a 15% return on assets. The president has set a goal for an in-

LO 6 PROBLEM 13-4 GOALS FOR SALES AND INCOME GROWTH

1. Selected financial data (in millions of dollars):

2019 2018 2017

1. Sales* 266.200 242.00 220.0

2. Net income (sales × 3%)* 7.986 7.26 6.6

13-20 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 13-4 (Concluded)

Selected ratios:

2019 2018 2017

6. Return on owners’ equity (Item 2/Item 4) 9.9% 9.4% 9.0%

Note: The return on owners’ equity ratios in the problem for 2014–2016 are

based on year-end owners’ equity rather than the average for each year. There-

2. No, the CEO will not be able to meet all her requirements if a 10% per-year growth

in income and sales is achieved. Under the stated assumptions that the net income

to sales ratio be maintained at 3% with annual sales growth of 10%, and the asset

turnover ratio be maintained at 2, the goal of holding debt to 35% of total assets will

accomplished.

3. Alternative actions to be considered to improve the return on equity and support the

increased dividend payments:

a. Improve the return on assets by

• reducing the asset base through better asset management.

4. The CEO is probably concerned with the potential impact that greater debt would

have on the company’s cost of capital. Increasing debt relative to owners’ equity

creates added risk, which translates to higher returns required by investors in the