INSTRUCTOR’S MANUAL

13–12

Lecture Suggestions

Module 1

LO 1

The Review Problem at the end of the chapter, using the lululemon athletica inc. statements, can

generate a good discussion of what can be found by performing ratio analysis on key financial

statement numbers.

Module 2

LO 4

The cash-to-cash cycle and its components, the days in inventory and the days in accounts

receivable, can be explained in conjunction with the current ratio to assess the adequacy of the

company’s current ratio. Similarly, days in accounts receivable measures how “quick” accounts

receivable actually is.

the company produces, in the form of net income. In a bank account, interest is not always

withdrawn, but is left to earn more interest than that which would be earned on the initial

investment alone. Stockholders do not withdraw all net income as dividends, but leave some

invested in the company to generate greater future income.

DECISION MODELS

There are many excellent exercises and problems in this chapter that can be adapted so

the students can solve the problems using the ratio analysis model and the business

decision model.

CHAPTER 13 FINANCIAL STATEMENT ANALYSIS

13–13

Projects and Activities

Module 1

LO 2

Horizontal Analysis

Outside assignment: lululemon athletica inc. Income Statement

The income statements for 2015, 2014, and 2013 for lululemon athletica Inc., are presented in the review

problem in your textbook. Set up a worksheet with columns similar to the Henderson Company example

(Exhibit 13-1) in your textbook to do a horizontal analysis of lululemon’s income statements through

income from operations. Round numbers to tenths of a percent to minimize rounding problems.

Solution

If you require or encourage the use of personal computers by your students, either at home or in an on-

FYE

FYE

FYE

Feb. 1

Feb. 2

Feb. 3

2015-2014

2015-2014

2014-2013

2012–

2011

2015

2014

2013

$

%

$

%

Net revenue

1,797,213

1,591,188

1,370,358

206,025

12.95%

220,830

16.11%

Cost of goods sold

883,033

751,112

607,532

131,921

17.56%

143,580

23.63%

Gross profit

914,180

840,076

762,826

74,104

8.82%

77,250

10.13%

Selling, gen & admin exp

538,147

448,718

386,387

89,429

19.93

62,331

16.13%

Income from operations

376,033

391,358

376,439

(15,325)

(3.92%)

14,919

3.96%

INSTRUCTOR’S MANUAL

13–14

In the MD &A of their FYE 2015 K-1, lululemon states1:

Gross Profit

Gross profit, as a percentage of net revenue, or gross margin, decreased 190 basis points, to 50.9% in

fiscal 2014 from 52.8% in fiscal 2013. The decrease in gross margin resulted primarily from:

• a decrease of 210 basis points due to product mix, increased product costs, and increased air

freight costs

• an increase in expenses related to our product and supply chain departments, relative to the

increase in net revenue, of 70 basis points;

• an increase in fixed costs, such as occupancy costs and depreciation, relative to the increase

in net revenue, of 40 basis points; and

• an unfavorable impact of foreign exchange rates on product costs which contributed to a

decrease in gross margin of 40 basis points

The decrease in gross margin was partially offset by a decrease in provision for inventories, charged

to cost of sales, of 110 basis points related to the pull-back of black Luon pants which was recorded

in the first quarter of fiscal 2013. A decrease in markdowns of 60 basis points driven by high sell–

through of seasonal items also partially offset the decrease in gross margin.”

CHAPTER 13 FINANCIAL STATEMENT ANALYSIS

Module 1

LO 3

Vertical Analysis

Outside assignment: lululemon athletica balance sheet

Vertical analysis involves recasting a financial statement in a form that eliminates absolute size as a

variable, and instead looks at the relative size of each element of the statement. Use the lululemon athletica

Consider the following questions:

◼ Did any items change significantly? If so, can you explain the change?

◼ What does this format show that you did not see when you merely compared the two balance

sheets?

INSTRUCTOR’S MANUAL

13–16

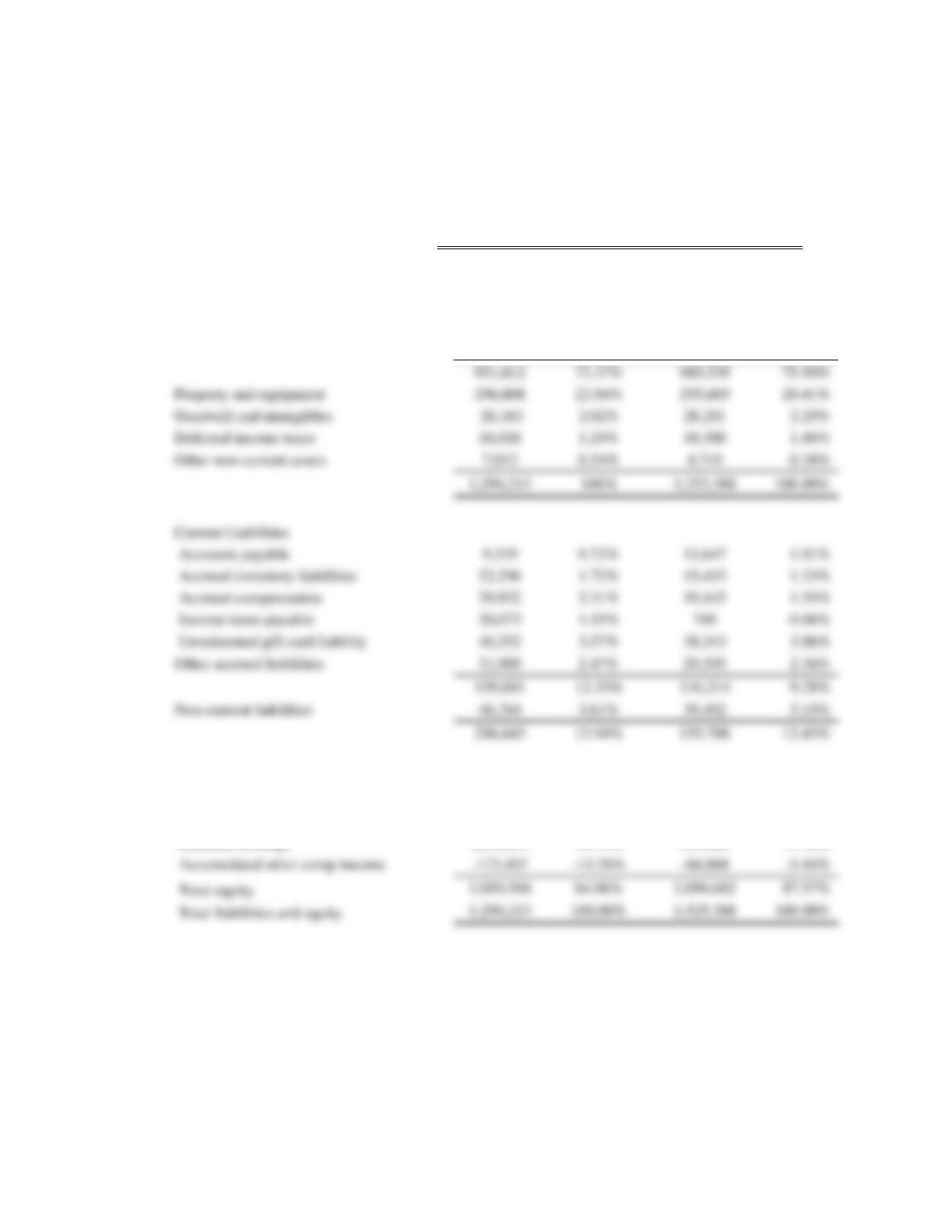

Solution lululemon athletica

2015

%

2014

%

Current Assets

Cash and cash equivalents

664,479

51.26%

698,649

55.79%

Accounts receivable

13,746

1.06%

11,903

0.95%

Inventories

208,116

16.06%

188,790

15.07%

Prepaid expenses

64,671

4.99%

46,197

3.69%

Stockholders’ equity

Common stock

661

0.05%

577

0.05%

Additional paid-in capital

241,695

18.65%

240,351

19.19%

Retained earnings

Accumulated other comp income

Total equity

84.06%

87.57%

Total liabilities and equity

100.00%

1,020,619

78.74%

923,822

73.76%

951,012

73.37%

945,539

75.50%

Property and equipment

296,008

22.84%

255,603

20.41%

Goodwill and intangibles

2.02%

2.25%

Deferred income taxes

16,018

1.24%

18,300

1.46%

Other non-current assets

0.54%

0.38%

Current Liabilities

Accounts payable

9,339

0.72%

12,647

1.01%

Accrued inventory liabilities

1.72%

1.23%

Accrued compensation

2.31%

1.55%

Income taxes payable

20,073

1.55%

0.06%

Other accrued liabilities

31,989

2.47%

29,595

2.36%

159,881

12.33%

116,214

9.28%

Non-current liabilities

46,764

3.61%

39,492

3.15%

206,645

15.94%

155,706

12.43%

CHAPTER 13 FINANCIAL STATEMENT ANALYSIS

13–17

Each asset is expressed as a percentage of total assets; each liability or equity account is expressed as a

percentage of total liabilities plus equity.

◼ Current assets: down slightly as a percentage of total assets. Biggest reason was the decrease in

cash and cash equivalents.

◼ Property and equipment increased slightly as a percentage of total assets.

Module 2

LO 4

Liquidity Analysis and the Management of Working Capital

In-class assignment: Mattel, Inc. liquidity

◼ Calculate Mattel’s current ratio.

◼ Calculate Mattel’s quick ratio. Is the difference significant between the current and quick ratios?

Can you explain what the difference means?

◼ Use the calculation of days in accounts receivable to evaluate Mattel’s current ratio. Based upon

the business Mattel is in, how would you expect their accounts receivable to differ from the

receivables of other companies?

◼ Calculate days in inventory for Mattel. How does the type of business Mattel is in influence the

contents of Mattel’s inventories, and how long these inventories are on hand?

◼ Calculate Mattel’s cash–to-cash cycle. What factors affect the company’s ability to generate cash?

◼ Is the cash flow from operations to current liabilities ratio a better indicator of Mattel’s ability to

generate enough cash to satisfy short-term obligations? Why or why not?

Solutions:

◼ Current Assets =3,185,951 1,088,949 = 2.93

Current Liabilities

INSTRUCTOR’S MANUAL

13–18

◼ The quick ratio is somewhat smaller. Students will probably use for quick assets: cash and

equivalents, and accounts receivable, which are compared to current liabilities

Module 3

LO 5

Solvency Analysis

In-class assignment: Mattel Computer Corp.

People within Mattel, as well as outside analysts, pay attention to key measures of the company’s ability to

use the resources available to it, especially in these tough economic times.

◼ Calculate Mattel’s debt–to-equity ratio for 2014 and 2013. How has it changed? Does Mattel

appear to depend heavily on debt financing?

NOTE: Other solvency ratios can be discussed using Mattel’s financial statements

Solution

Debt-to-Equity Ratio = Total Liabilities/Total Equity

CHAPTER 13 FINANCIAL STATEMENT ANALYSIS

INSTRUCTOR’S MANUAL

13–20

Mattel, Inc.

Consolidated Balance Sheet3

(Note – stockholders’ equity has been consolidated from the report for purposes of these exercises)

Assets: 2014 2013

Cash & cash equivalents

$ 971,650

$1,039,216

Accounts receivable, net

1,093,180

1,260,105

Inventories

562,047

568,843

Liabilities & Stockholders Equity:

Short-term borrowings

$ 0

$ 4,278

Accounts payable

430,259

375,328

Accrued liabilities

639,907

640,155

Income taxes payable

18,783

1,088,949

Long-term debt

Other non-current liabilities

584,026

2,949,071,

Consolidated Statement of Operations4

Mattel Computer Corporation

(Note- for purposes of these exercises, the income statement is shown only through gross profit)

2014 2013

Net sales

$ 6,023,819

$ 6,484,892

Cost of sales

3,022,797

3,006,009

Gross Profit

3,001,022

3,478,883

Prepaid expenses and other

559,074

509,829

Total current assets

3,377,993

PP&E, net

737,869

659,333

Goodwill

1,393,968

1,083,239

Other non-current assets

1,319,061

Total assets:

CHAPTER 13 FINANCIAL STATEMENT ANALYSIS

13–21

LO 6

Profitability Analysis

In-class assignment: Return on assets

A company owns two hotels, both in large cities. Revenues for the two hotels are similar. However, one

◼ Why does the new building put this manager at a disadvantage relative to her compensation?

◼ Can depreciation be calculated differently for reporting and managerial evaluation? Why or why

not?

◼ What problem would this decision present for the company as a whole?

◼ Do you think that a company has any flexibility in how it calculates return on assets (or any ratio,

for that matter) for internal use?

◼ What would you, as the company officer who supervises both managers, suggest as a solution to

this problem?

Solution

◼ The manager of the new hotel is at a disadvantage because the net book value of her assets, which

will include the new building and fixtures, will be much higher than that of the older building.

Thus, for comparable net income, she will show a lower return on assets.