1

Chapter 13: FINANCING THE DEAL

Private Equity, Hedge Funds, and Other Sources of Financing

Answers to End of Chapter Discussion Questions

13.1 What are the primary ways in which a leveraged buyuot is financed?

Answer: In a leveraged buyout, borrowed funds are used to pay for most of the purchase price. Historically, as

much as 90% or more of the purchase price was financed with debt; however, more recently, financial sponsor

13.2 How do loan and security covenants affect the way in which a leveraged buyout is managed? Note the

differences between positive and negative covenants.

Answer: Security provisions and protective covenants in loan documents are intended to ensure that the

interest and principal of outstanding loans will be repaid in a timely fashion. The number and complexity of

security provisions depends on the size of the firm. Loans to small firms tend to be secured more often than

term loans to large firms. Typical security features include the assignment of payments due under a specific

13.3 Describe common strategies LBO firms use to exit their investment. Discuss the circumstances under which

some methods are preferred to others.

Answer: Comprising about 13 percent of total transactions since 1970s, initial public offerings (i.e., IPOs)

have declined in importance as an exit strategy. At 39 percent of all exits, the most common ways of exiting

buyouts is through a sale to a strategic buyer; the second most common method at 24 percent is a sale to

2

13.4 While most LBOs are predicated on improving operating performance through a combination of aggressive

cost cutting and revenue growth, hospital chain HCA laid out an unconventional approach which relied

heavily on revenue growth in its effort to take the firm private. On July 24, 2006, management again

announced that it would “go private” in a deal valued at $33 billion including the assumption of $11.7 billion

in existing debt. Would you consider a hospital chain a good or bad candidate for an LBO? Be specific.

Answer: Answer: Hospitals generally represent bad candidates. Hospital cash flow is heavily dependent on

13.5 In a move reminiscent of the blockbuster buyouts of the late 1980s, seven private investment firms acquired

100 percent of the outstanding stock of SunGard Data Systems Inc. (SunGard) in late 2005. SunGard is a

financial software firm known for providing application and transaction software services and creating backup

data systems in the event of disaster. The company‘s software manages 70 percent of the transactions made on

the Nasdaq stock exchange, but its biggest business is creating backup data systems in case a client’s main

systems are disabled by a natural disaster, blackout, or terrorist attack. Its large client base for disaster

recovery and back-up systems provides a substantial and predictable cash flow. Furthermore, the firm had

substantial amounts of largely unencumbered current assets. The deal left SunGard with a nearly 5 to 1 debt to

equity ratio. Why do you believe lenders might have been willing to finance such a highly leveraged

transaction?

Answer: The firm had substantial market share in a stable industry, disaster recovery and back-up systems,

13.6 In an effort to take the firm private, Cox Enterprises announced on August 3, 2004 a proposal to buy the

remaining 38% of Cox Communications’ shares that they did not currently own for $32 per share. Cox

Enterprises stated that the increasingly competitive cable industry environment makes investment in the cable

industry best done through a private company structure. Why would the firm believe that increasing future

levels of investment would be best done as a private company?

Answer: Substantial levels of investment would result in increasing levels of depreciation and amortization

13.7 Following Cox Enterprises’ announcement on August 3, 2004 of its intent to buy the remaining 38% of Cox

Communications’ shares that they did not currently own, the Cox Communications Board of Directors formed

a special committee of independent directors to consider the proposal. Why?

Answer: Special board committees consisting of outside directors often are set up when company insiders are

13.8 Qwest Communications agreed to sell its slow but steadily growing yellow pages business, QwestDex, to a

consortium led by the Carlyle Group and Welsh, Carson, Anderson and Stowe for $7.1 billion in late 2002.

3

Why do you believe the private equity groups found the yellow pages business attractive? Explain the

following statement: “A business with high growth potential may not be a good candidate for an LBO.”

Answer: QwestDex was considered an attractive candidate because of its steadily growing, highly predictable

cash flow, strong management team, and the willingness of management to continue with the business. The

13.9 Describe the potential benefits and costs of LBOs to stakeholders including shareholders, employers, lenders,

customers, and communities in which the firm undergoing the buyout may have operations. Do you believe

that on average LBOs provide a net benefit or cost to society? Explain your answer.

Answer: Target shareholders prior to the buyout clearly benefit greatly from efforts to take the company

private. However, in addition to the potential transfer of wealth from bondholders to stockholders, some

critics of LBOs argue that a wealth transfer also takes place in LBO transactions when LBO management is

able to negotiate wage and benefit concessions from current employee unions. LBOs are under greater

13.10 Sony’s long-term vision has been to create synergy between its consumer electronics products business and its

music, movies, and games. On September 14, 2004, a consortium, consisting of Sony Corp of America,

Providence Equity Partners, Texas Pacific Group, and DLJ Merchant Banking Partners, agreed to acquire

MGM for $4.8 billion, consisting of $2.85 billion in cash and the assumption of $2 billion in debt. The cash

portion of the purchase price consisted of about $1.8 billion in debt and $1 billion in equity capital. Of the

equity capital, Providence contributed $450 million, Sony and Texas Pacific Group $300 million, and DLJ

Merchant Banking $250 million. In what way do you believe that Sony’s objectives might differ from those

of the private equity investors making up the remainder of the consortium? How might such differences affect

the management of MGM? Identify possible short-term and long-term effects.

Answer: Sony wanted to gain access to the film library to help provide content for the growth in its play

station and games product lines. However, private equity investors often want to cash out in 5-7 years or less.

Solutions to Chapter Case Study Questions

4

Implications of a Credit Rating Downgrade Following a Merger or Acquisitions

Discussion Questions and Answers:

1. What are positive (or affirmative) and negative covenants? How can such covenants affect EnscoRowan’s

future investment decisions? Be specific.

Answer: Loan covenants are commitments made by borrowers to lenders. They can take many forms and

often are expressed as maximum debt to equity or debt to total capital ratios. They can also affect the

amount and timing of dividends paid and capital outlays as well as minimum working capital levels and

2. What is a revolving credit line? What does it mean that EnscoRowan’s revolving credit line was unsecured?

Why is this important?

Answer: A revolving-credit facility is used to satisfy daily liquidity requirements, often secured by the

firm’s most liquid assets such as receivables and inventory. Borrowers seek revolving lines of credit on

which they draw on a daily basis. Under a revolving credit arrangement, the bank agrees to make loans up to

3. EnscoRowan has high fixed costs in terms of its investments in shallow and deep water rigs and their

maintenance. As such, the firm has substantial operating leverage when the market for offshore drilling

recovers. What is operating leverage and how can it boost the firm’s financial returns? (Hint: See Chapter 7.)

Answer: Operating leverage refers to the way in which a firm combines fixed and variable expenses (i.e., its

ratio of a firm’s fixed expenses to total cost of sales). It is measured by the extent to which a firm’s

4. What factors do you believe a lender would consider in determining how much to lend to EnscoRowan? Be

specific.

Answer: Lenders focus on a borrower’s capacity to repay both principal and interest on a timely basis. This

entails looking at a potential borrower’s history in repaying prior loans, current and future pre-financing

5. Why was the form of payment stock and not cash or cash and stock? Explain your answer.

Examination Questions and Answers

True/False Questions: Answer true or false to the following questions:

1. Leveraged buyout firms use the unencumbered assets and operating cash flow of the target firm to finance the

transaction. True or False

2. Accounts receivable represent an undesirable form of collateral from the lender’s point of view because they

are often illiquid. True or False

3. Because of their high liquidity, lenders often lend up to 100% of the book value of accounts receivable

pledged as collateral in leveraged buyouts. True or False

4. A negative loan covenant is a portion of a loan agreement that specifies the actions the borrowing firm agrees

to take during the term of the loan. True or False

5. Loan agreements commonly have cross-default provisions allowing a lender to collect its loan immediately if

the borrower is in default on a loan to another lender. True or False

6. Junk bonds are high-yield bonds either rated by the credit-rating agencies as below investment grade or not

rated at all. True or False

7. According to fraudulent conveyance laws, if a new company is found by the court to have been inadequately

capitalized to remain viable, the lender could be stripped of its secured position in the assets of the company or

its claims on the assets could be made subordinate to those of the general creditors. True or False

8. Typical LBO targets are in mature industries such as manufacturing, retailing, textiles, food processing,

apparel, and soft drinks. True or False

9. High growth firms with high reinvestment requirements often make attractive LBO targets. True or False

10. Premiums paid to LBO target firm shareholders often exceed 40%. True or False

11. The high premiums paid to LBO target shareholders reflect the tax benefits associated with the high leverage

of such transactions and the improved operating efficiency following the completion of the buyout resulting

from management incentive plans and the discipline imposed by the need to repay debt. True or False

12. Investors in highly leveraged transactions who are primarily focused on relatively short-to-intermediate term

financial returns are often called financial buyers. True or False

13. When a public company is subject to a leveraged buyout, it is said to be “going private.” True or False

14. A leveraged buyout initiated by a firm’s management is called a management buyout. True or False

15. Financial buyers usually hold onto their investments for at least 15–20 years. True or False

16. Investors in LBOs are frequently referred to as financial buyers, because they are primarily focused on

relatively short-to-intermediate-term financial returns. True or False

17. LBO capital structures are often very complex, consisting of bank debt, subordinated unsecured debt,

preferred stock, and common equity. True or False

18. LBO investors seldom sell assets to repay debt used to acquire the firm. True or False

19. LBO investors often use public offerings of the firm’s stock or sell the firm to a strategic buyer in order to exit

the business. True or False

20. LBO investors will often use the target firm’s cash in excess of normal working capital requirements to

finance the transaction. True or False

21. Asset based lending does not require the borrower to pledge assets as collateral underlying the loans. True or

False

22. The loan agreement stipulates the terms and conditions under which the lender will loan the borrower funds.

True or False

23. A single asset is often used to collateralize loans from different lenders in LBO transactions. True or False

24. Asset based lenders will usually lend up to 100% if the book value of the LBO target’s receivables. True or

False

25. Cash flow lenders view the borrower’s future cash flow generation capability as the primary means of

recovering a loan, while largely ignoring the assets of the LBO target. True or False

26. Junk bonds have invariably proved to be a reliable source of low-cost financing in LBO transactions during

the last 30 years. True or False

27. Fraudulent conveyance laws are intended to prevent shareholders, secured creditors, and others from

benefiting at the expense of unsecured creditors. True or False

28. To avoid being subject to fraudulent conveyance laws, a properly structured LBO should have a balance sheet

that clearly indicates solvency at the time of closing. True or False

29. The risk associated with overpaying is magnified for leveraged buyout transactions. True or False

30. Under-performing operating units of large companies are often excellent candidates for LBOs. True or False

31. Junk bonds are always high risk. True or False

32. Firms with redundant assets and predictable cash flow are often good candidates for leveraged buyouts. True

or False

33. Common exit strategies for LBOs include sale to a strategic buyer, an IPO, a leveraged recapitalization, or a

sale to another buyout firm. True or False

34. Divisions of larger companies are generally poor candidates for successful leveraged buyouts. True or False

35. Financial buyers usually plan to hold onto acquired firms longer than strategic buyers. True or False

36. Borrowers often seek revolving lines of credit that they can draw upon on a daily basis to run their business.

True or False

37. A term loan usually has a maturity of less than one year. True or False

38. The loan agreement stipulates the terms and conditions under which the lender will loan the firm funds. True

or False

39. An affirmative covenant is a portion of a loan agreement that specifies the actions the borrowing firm cannot

take during the term of the loan. True or False

40. Borrowers often prefer term loans because they do not have to be concerned that these loans will have to be

renewed. True or False

41. LBOs can be of an entire company or divisions of a company. True or False

42. When a public company is subject to an LBO, it is said to be going private, because more than 50% of the

equity of the firm has been purchased by a small group of investors and is no longer publicly traded. True or

False

43. The LBO that is initiated by the target firm’s incumbent management is called a management buyout. True or

False

44. LBO firms seldom purchase a firm to use as a platform to undertake other leveraged buyouts in the same

industry. True or False

45. A common technique used during the 1990s was to wait for favorable periods in the stock market to sell a

portion of the LBO’s equity to the public. The proceeds of the issue would be used to repay debt, thereby

reducing the LBO’s financial risk. True or False

46. LBO investors have become much more actively involved in managing target firms in recent years than they

have in the past. True or False

47. There is some evidence that the Sarbanes-Oxley Act of 2002 has also been a factor in some firms going

private as a result of the onerous reporting requirements of the bill. True or False

48. The growth in LBO activity is not simply a U.S. phenomenon. Western Europe has seen a veritable explosion

in private equity investors taking companies private, reflecting ongoing liberalization in the European Union

as well as cheap financing and industry consolidation. True or False

49. The promissory note commits the borrower to repay the loan, only if the assets when liquidated fully cover the

unpaid balance. True or False

50. If the borrower defaults on the loan or otherwise fails to honor the terms of the agreement, the lender can seize

and sell the collateral to recover the value of the loan only if the borrower agrees that it is unlikely that the

loan will be repaid. True or False

51. Because term loans are negotiated privately between the borrower and the lender, they are much more

expensive than the costs associated with floating a public debt or stock issue. True or False

52. Limitations the lender imposes on the borrower on the amount of dividends that can be paid, the level of

salaries and bonuses that may be given to the borrower’s employees, the total amount of indebtedness that can

be assumed by the borrower, and investments in plant and equipment and acquisitions are called affirmative

covenants. True or False

53. Secured debt often is referred to as mezzanine financing. True or False

54. Bridge financing is usually expected to be replaced within two years after the closing date of the LBO

transaction. True or False

9

55. Debt issues not secured by specific assets are called debentures. True or False

56. An indenture is a contract between the firm that issues the long-term debt securities and the lenders. True or

False

57. Preferred stock often is issued in LBO transactions, because it provides investors a fixed income security,

which has a claim that is junior to common stock in the event of liquidation. True or False

58. The acquirer often is asked for a commitment letter from a lender, which commits the lender to providing

financing for the transaction. True or False

59. If the LBO is structured as a direct merger in which the seller receives cash for stock, the lender will make the

loan to the buyer once the appropriate security agreements are in place and the target’s stock has been pledged

against the loan. The target then is merged into the acquiring company, which is the surviving corporation.

True or False

60. LBOs may be consummated by establishing a new subsidiary that merges with the target. This may be done to

avoid any negative impact that the new company might have on existing customer or creditor relationships.

True or False

61. Management buyouts without a financial equity contributor are relatively rare. True or False

62. LBO exit strategies involving selling to a strategic buyer usually result in the best price as the buyer may be

able to generate significant synergies by combining the firm with its existing business. True or False

63. LBOs normally involve public companies going private. True or False

64. Most highly leveraged transactions consist of acquisitions of private rather public firms. True or False

65. Private equity investments are normally focused on the manufacturing industry. True or False

Multiple Choice Questions: Circle only one of the alternatives for each of the following questions:

1. Which of the following is generally not true about leveraged buyouts?

a. Borrowed funds are used to pay for all or most of the purchase price, perhaps as much as 90%

b. Tangible assets of the target firm are often used as collateral for loans.

c. Bank loans are often secured by the target firm’s intangible assets

d. Secured debt is often referred to as junk bond financing.

e. C and D only

2. Asset based lending is commonly used to finance leveraged buyouts. Which of the following is not true about

such financing?

a. The borrower generally pledges tangible assets as collateral.

10

b. Lenders look at the target firm’s assets as their primary protection.

c. Bank loans are secured frequently by receivables and inventory.

d. Loans maturing in more than one year are often referred to as term loans.

e. The target firm’s most liquid assets generally secure longer-term loans.

3. Security provisions and protective covenants are included in loan documents to increase the likelihood that the

interest and principal of outstanding loans will be repaid in a timely fashion. Which of the following is not

true about security provisions and protective covenants?

a. Security features include the assignment of payments due under a specific contract to the lender.

b. Negative covenants include limits on the amount of dividends that might be paid

c. Limitations on the amount of working capital that the borrower can maintain.

d. Periodically, financial statements must be sent to lenders.

e. Automatic loan repayment acceleration if the borrower is in default on any loans outstanding

4. Which of the following is not true about junk bonds?

a. Junk bonds are either unrated or rated below investment grade by the credit rating agencies

b. Typically yield about 1-2 percentage points below yields on U.S. Treasury debt of comparable

maturities.

c. Junk bonds are commonly used source of “permanent” financing in LBO transactions

d. During recessions, junk bond default rates often exceed 10%

e. Junk bond default risk on non-investment grade bonds tends to increase the longer the elapsed time

since the original issue date of the bonds

5. Which of the following characteristics of a firm would limit the firm’s attractiveness as a potential LBO

candidate?

a. Substantial tangible assets

b. High reinvestment requirements

c. High R&D requirements

d. B and C

e. All of the above

6. Premiums paid to LBO firm shareholders average

a. 20%

b. 70%

c. 5%

d. Less than typical mergers

e. More than typical mergers

7. Factors that are most likely to contribute to the magnitude of premiums paid to LBO target firm shareholders

are

a. Tax benefits

b. Improved operating efficiency

c. Improved decision making

d. A, B, and C

e. A and C only

8. Which of the following is not true about attractive LBO candidates?

a. Most assets tend to be encumbered

b. Have low leverage

c. Have predictable cash flow

11

d. Have assets that are not critical to the ongoing operation of the firm

e. Are in mature, moderately growing industries

9. Which of the following is generally not considered a characteristic of a financial buyer?

a. Focus on short-to-intermediate returns

b. Concentrate on actions that enhance the ability of target firm’s ability to generate cash flow to satisfy

debt service requirements

c. Intend to own the business for very long periods of time

d. Manage the business to maximize return to equity investors

e. All of the above

10. Which of the following are commonly used sources of funding for leveraged buyouts?

a. Secured debt

b. Unsecured debt

c. Preferred stock

d. Seller financing

e. All of the above

11. Fraudulent conveyance is best described by which of the following situations:

a. A new company spun off by its parent to the parent’s shareholders that enters bankruptcy is found to

have been substantially undercapitalized when created

b. An acquiring company pays too high a price for a target firm

c. A company takes on too much debt

d. A leveraged buyout is taken public when its operating cash flows are increasing

e. None of the above

12. LBO investors must be very careful not to overpay for a target firm because

a. Major competitors tend to become more aggressive when a firm takes on large amounts of debt

b. High leverage increases the break-even point of the firm

c. Projected cash flows are often subject to significant error limiting the ability of the firm to repay its

debt

d. A and B only

e. A, B, and C

13. LBOs often exhibit very high financial returns during the years following their creation. Which of the

following best describes why this might occur?

a. LBOs invariably improve the firm’s operating efficiency

b. LBOs tend to increase investment in plant and equipment

c. The only LBOs that are taken public are those that have been the most successful

d. LBOs experience improved decision making during the post-buyout period

e. None of the above

12

14. Which of the following is not typically true of LBOs?

a. Managers are generally also owners

b. Most employees are given the opportunity to participate in profit sharing plans

c. The focus tends to be on improving operational efficiency though cost cutting and improving

productivity

d. R&D budgets following the creation of the LBO are always increased significantly

e. All of the above

15. Which of the following tends to be true of LBOs

a. LBOs rely heavily on management incentives to improve operating performance

b. The premium paid to target firm shareholders often exceeds 40%

c. Tax benefits are predictable and are built into the purchase price premium

d. The cost of equity is likely to change as the LBO repays debt

e. All of the above

16. An investor group acquired all of the publicly traded shares of a firm. Once acquired, such shares would no

longer trade publicly. Which of the following terms best describes this situation?

a. Merger

b. Going private transaction

c. Consolidation

d. Tender offer

e. Joint venture

17. The management team of a privately held firm found a lender who would lend them 90 percent of the purchase

price of the firm if they pledged the firm’s assets as well as their personal assets as collateral for the loan. This

purchase would best be described by which of the following terms?

a. Merger

b. Leveraged buyout

c. Joint venture

d. Tender offer

e. Consolidation

Case Study Short Essay Examination Questions

ABBOTT LABS SUFFERS CREDIT DOWNGRADE IN WAKE OF TAKEOVER OF ST. JUDE’S MEDICAL

Case Study Objectives: To Illustrate

• M&A financing methods,

• Form of payment and form of acquisition,

• A common legal structure for transferring ownership, and

13

• Tax considerations.

Medical equipment makers are under pressure to offer a wider portfolio of products to their hospital customers, which

have been through a wave of mergers in recent years giving them more heft to negotiate pricing with their suppliers. In

announcing its takeover of American medical equipment manufacturer, St. Jude’s Medical Inc. (St. Jude), U.S. based

Abbott Laboratories Inc. (Abbott) said the buyout was to expand its heart device business. Abbott is a diversified

In terms of total dollars, Abbott agreed to pay approximately $23.6 billion, including approximately $13.6 billion in

cash and about $10 billion in Abbott common shares, which represented approximately 254 million shares of Abbott

Table 13.5 Breakdown of Total Merger Consideration

(Millions of Dollars and Shares, except for Per Share Amounts and Exchange Ratio)

St. Jude Medical Sharesa

291

Cash Consideration Per Share Paid to St. Jude Shareholders and Equity Stock Option Holders

$46.75

Cash Portion of the Purchase Price

$13,610

St. Jude Sharesa

291

Exchange Ratio (Abbott shares per St. Jude Share)

.8708

Abbott Common Shares Issued

254

$39.36

Equity Portion of Purchase Price

$9,978

Estimated Fair Value of St. Jude Medical Stock Option Awardsc

$11

Total Consideration Paid

$23,599

aRepresents about 287 million St. Jude shares outstanding as of January 4, 2017, plus about 4 million vested stock

options and accelerated restricted stock units settled upon the close of the transaction.

Investors also reasoned that the additional debt required to finance the deal would seriously limit the firm’s ability to

pursue future strategic opportunities. Expressing investor displeasure, Abbott Lab’s market value plunged more than $5

billion or 6% in a single day following the takeover announcement on April 26, 2016.

With combined revenue of $26.8 billion, Abbott said its deal would help it compete against larger rivals Medtronic

Plc, Boston Scientific Corp, and Edward Life Sciences. The combination of Abbott and St. Jude creates a medical

device manufacturer with leading positions in high growth cardiovascular markets, including atrial fibrillation,

Abbott funded the deal through a combination of cash on hand at Abbott and St. Jude, as well as new debt financing

consisting of a senior unsecured term loan facility, the issuance of senior unsecured notes, and a senior unsecured

bridge loan facility. Upon signing the merger agreement, Abbott obtained a debt commitment letter in which lenders

agreed to provide, subject to certain loan covenants, a $17.2 billion senior unsecured bridge loan facility to finance the

14

merger, the repayment of a portion of Abbott’s higher cost debt and St. Jude’s debt assumed by Abbott as part of the

deal, and associated transaction fees.

At yearend 2016, Abbott’s total long-term debt soared to $20.7 billion from $5.9 billion at the end of 2015. Cash and

cash equivalents at the end of 2016 stood at $18.6 billion. The combined firms’ net debt position at that time was $2.1

billion (i.e., $20.7 billion less $18.6 billion). The sharp ramp-up in Abbott’s leverage, concerns about realizing

anticipated synergy in a timely manner, and the sustainability of projected cash flows jeopardized the firm’s credit

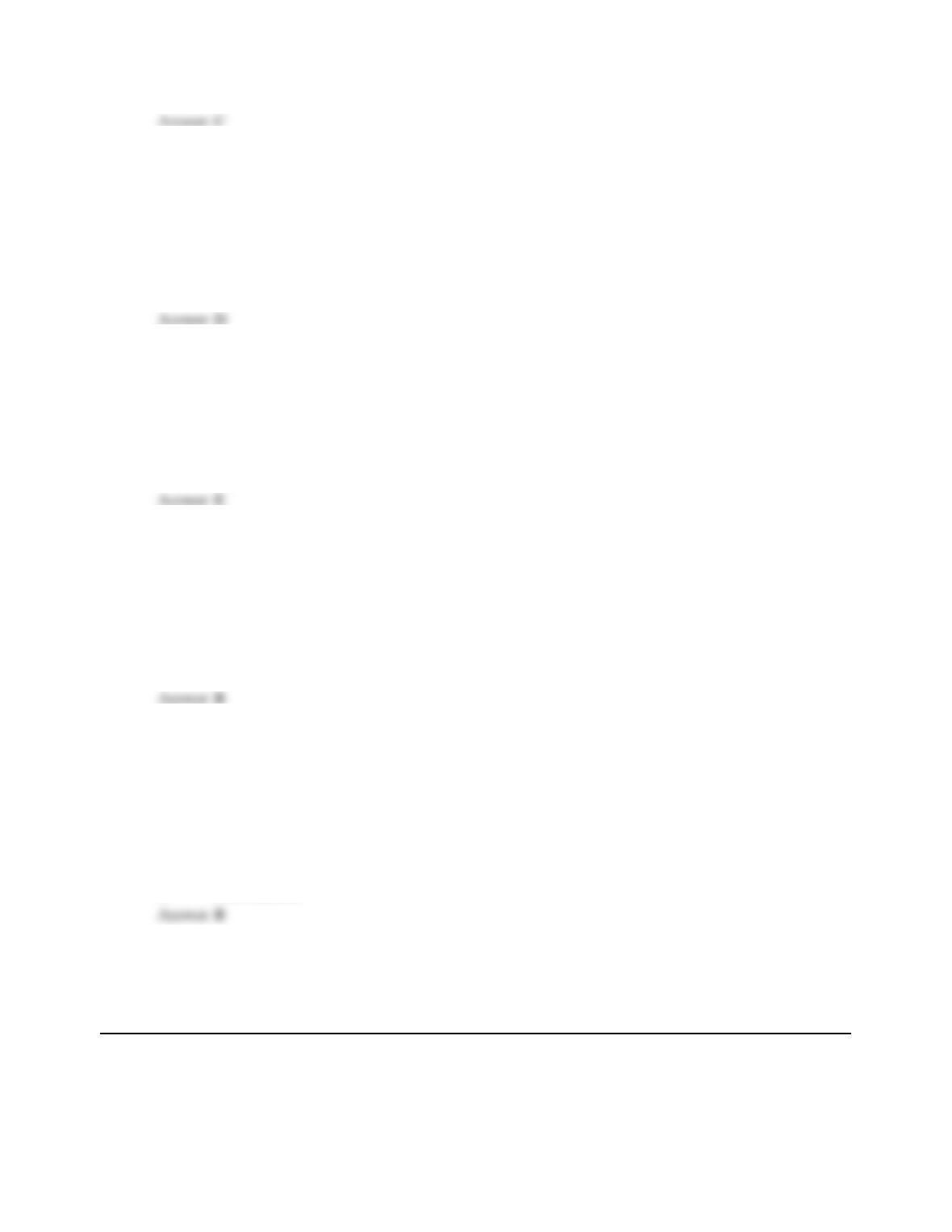

Figure 13.3 Abbott Labs and St. Jude’s Medical Reverse Triangular Merger

Whether the deal delivers investors their required financial returns or not depends on a variety of factors: some

within the control of Abbott’s management and some not. Management’s execution of the postmerger integration of St.

Jude’s will be challenging given the likely turmoil that often ensues in mergers of this size and complexity. This turmoil

Abbott Labs

St. Jude Medical (Receives assets

Merger Sub

(Shell created by Abbott and

St. Jude Shareholders (receive

Abbott’s voting common and

Abbott’s

Voting Stock

Subsidiary’s

Stock

Subsidiary’s Assets

and Liabilities

Abbott’s Stock

15

can result in a loss of key employees at both firms, as well as increased customer and supplier attrition. Such disruption

often delays the realization of both the magnitude and timing of the projected synergies so critical to recovering the

Discussion Questions and Answers:

1. What is the form of payment and form of acquisition used in this transaction? Speculate as to why they

were these chosen?

Answer: The form of payment was a combination of cash and stock. Abbott could not easily finance an

entirely cash transaction so some portion of the payment was offered in stock. From St. Jude’s shareholders

2. What are positive (or affirmation) and negative covenants? How can such covenants affect Abbott’s future

investment decisions? Be specific.

Answer: Loan covenants are commitments made by borrowers to lenders. They can take many forms and

often are expressed as maximum debt to equity or debt to total capital ratios. They can also affect the

amount and timing of dividends paid and capital outlays as well as minimum working capital levels and

3. The deal is taxable to St. Jude shareholders to the extent that they realize a gain. The reason is that the

reverse triangular merger structure used in this instance does not qualify as a tax free merger. Why?

4. What is a bridge loan? What does it mean that they were unsecured? The terms of these bridge loans were to

automatically terminate no later than July 27, 2017, at which point Abbott was to have its permanent

long-term financing in place. What is “permanent financing?” Explain your answer.

Answer: Bridge loans are short duration loans granted to bridge the gap between when funds are needed but

not available. They are granted until the borrower is able to secure longer-term or permanent financing or

16

5. The merger is characterized as a reverse triangular merger. Speculate as to why this structure may have

been chosen? Explain your answer.

Answer: The reverse triangular merger may have been chosen as it eliminates the need for parent firm

6. Abbott could have directly merged with St. Jude. Why was a wholly-owned merger sub created by Abbott to

own St. Jude’s assets and liabilities instead? Explain your answer.

Answer: By holding St. Jude as a wholly owned subsidiary, Abbott is limiting its exposure to any significant

The Legacy of Leverage, Bad Assumptions and Poor Timing:

The Largest LBO in U.S. History Goes Bankrupt

________________________________________________________________________________

Key Points:

• Leverage offers the prospect of outsized financial returns for investors

• However, excessively leveraged firms often have little margin for error

• If key assumptions underlying the deal are unrealistic, the only alternative may be bankruptcy

• Chapter 11 reorganization can be protracted

______________________________________________________________________________

Energy Future Holdings Corporation emerged from bankruptcy in late 2016 bringing to a close a deal based on

excessive optimism, poor timing and unrealistic assumptions. What follows is a discussion of why the LBO seemed

attractive, the deal’s complex legal and financial structure, factors that ultimately pushed the firm into bankruptcy, and

how the firm was ultimately reorganized.

Amid great fanfare, a consortium of storied investor groups along with highly sophisticated lenders took Texas

based electric utility holding company TXU private on October 7, 2007. Immediately following closing, TXU Corp

was renamed Energy Future Holdings (EFH). EFH consisted on two subsidiaries: Oncor, a business that sells electricity

in wholesale markets to other utilities and big businesses, and Texas Competitive Electric Holdings (TCEH), which

holds TXU’s public utility operating assets and liabilities. The latter firm is the one that ultimately filed for bankruptcy.

The U.S went into recession in December 2007 and did not emerge until June 2009 according to the National

Bureau of Economic Research, the widely recognized organization that defines such things. The recession reduced the

demand for electricity and forced natural gas prices lower. While the recession clearly exacerbated the situation, much

of the damage done to EFH was self-inflicted by the complex financial engineering used to finance the deal and by the

byzantine legal structure created to limit investors’ exposure to potential liabilities. These factors made it increasingly

difficult for the firm to meet its scheduled debt service payments and ultimately to reorganize in bankruptcy.

17

downfall of the firm. Unable to meet its commitments and with lenders running out of patience, the firm sought the

protection of Chapter 11 of the U.S. Bankruptcy Court in late spring of 2014.

How could investors with sterling reputations and sophisticated lenders make such a big mistake? Simply saying it

was due to greed would be overly simplistic. The investors and lenders participating in this deal were at some level

victims of their own earlier success. Private equity firms seek unusually high returns on the equity they put into

projects by borrowing as much as they feel can be managed. And given Federal Reserve policies that pushed interest

rates to historical lows, LBO financial sponsors were encouraged to take on much more debt than would have been

considered prudent had interest rates been higher. Investors and lenders were piling into LBO deals in 2007 in a search

for higher financial returns. The prior successes of the LBO sponsors lent credibility to the deals they put together. The

conditions were ripe for the addictive effects of over-optimism and cheap money to create a mega deal whose success

was dependent on literally everything going according to plan.

Wall Street banks were similarly enamored with the proposed deal to take TXU private. They were competing in

2007 to make loans to buyout firms on easier terms, with the banks also investing their own funds in the deal. The

allure to the banks was the prospect of dividing up as much as $1.1 billion in fees for originating the loans, repackaging

such loans into pools called collateralized loan obligations, and reselling them to long-term investors such as pension

funds and insurance companies. In doing so, the loans would be removed from the banks’ balance sheets, eliminating

potential losses that could arise if the deal soured at a later date. Furthermore, the deal appeared to be attractive as an

investment opportunity as some banks put up $500 million of their own cash for a stake in the TXU.

18

.

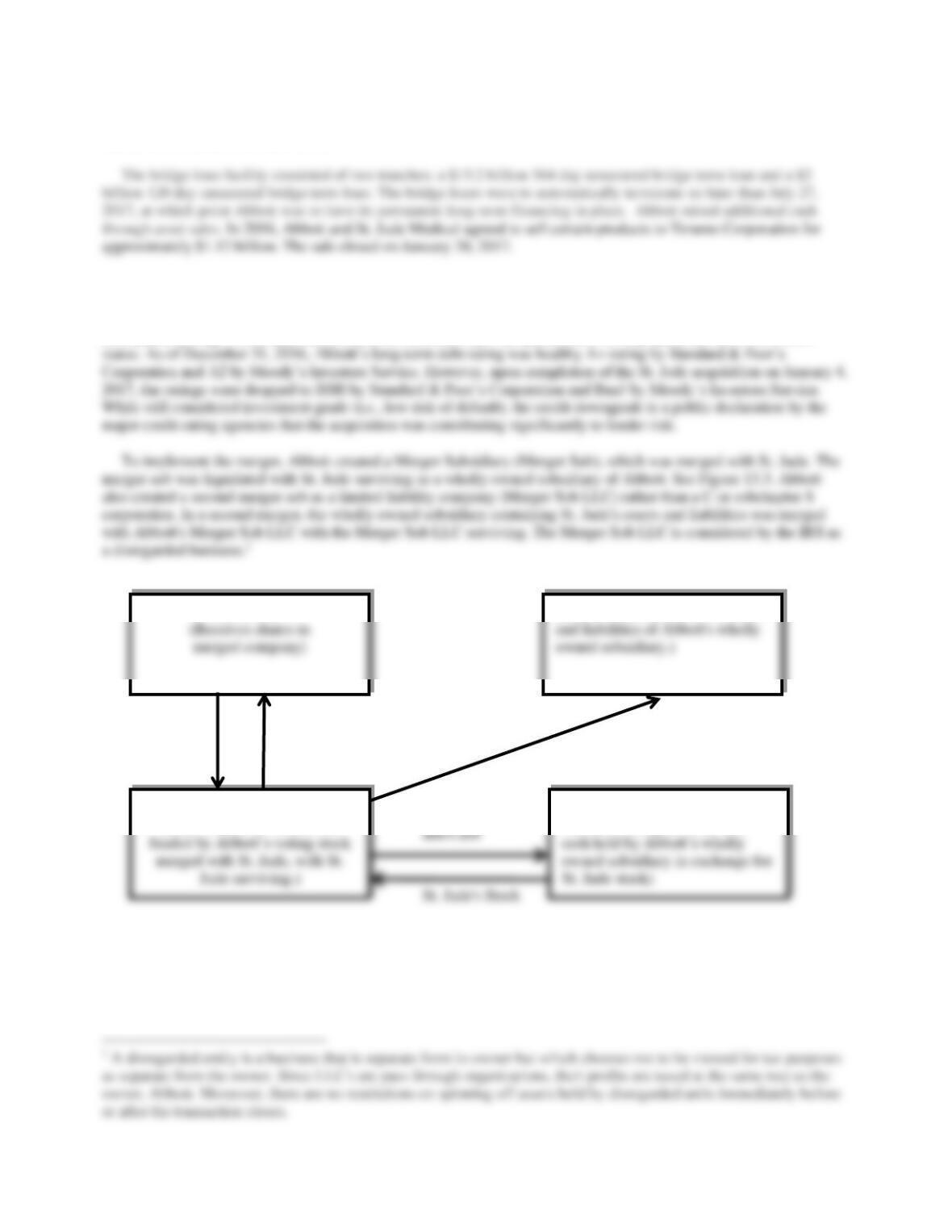

Subsequent to closing, Merger Sub was reorganized into a new holding company, controlled by the Financial

Sponsor Group and renamed Energy Future Holdings (EFH). EFH consisted of two subsidiaries: a regulated business,

Oncor, and an unregulated business, Texas Competitive Electric Holdings (TCEH). All TXU non-Sponsor Group

related debt incurred to finance the transaction is held by EFH. See Figure 13.4.

The firm faced an untenable financial position by 2014. Absent a turnaround in natural gas prices, EFH had to find

a way to substantially reduce the burden of the pending 2014 $20 billion loan payment with its lenders through a debt

for equity swap, more favorable terms on existing debt, or by pursuing Chapter 11 bankruptcy. In December 2012 in

an effort to extend debt maturities to buy time for a turnaround and to reduce interest expense, EFH exchanged $1.15

Merger Sub

Parent

(Sponsor

Group)

TXU

Figure 13.3 Forward Triangular Cash Merger

Cash

Merger Sub

Stock

Energy Future Holdings –

EFH (Formerly Merger

Sub)

Texas Competitive Electric

Holdings-TCEH

Oncor

Figure 13.4 Post Merger Organization

19

aspects of the plan. A sticking point with creditors was how to value the unregulated subsidiary for tax purposes. Under

the terms of the proposed deal, the lenders would forgive debt for ownership of the unregulated subsidiary (TCEH)

through a debt for equity swap with bondholders and a subsequent tax free spin off to avoid a huge tax bill for EFH.

EFH bondholders owed $1.7 billion were set to take control of the regulated Oncor unit.

In an effort to gain support for its reorganization plan, EFH called off the bankruptcy auction of its 80% stake in

Oncor on June 26, 2015 and proceeded to promote the spin-off of Oncor in a tax free transaction. EFH would leave

$805 million in cash to pay TCEH secured creditors. The bankruptcy court judge approved the firm’s reorganization

plan on December 3, 2015. The tax free spin off of Oncor was completed on October 4, 2016 paving the way for

emergence from Chapter 11, almost two and one-half years after the firm had sought court protection.

Discussion Questions and Answers:

1. This chapter identifies a number of ways in which LBOs can create value for their investors. The financial

sponsor group was relying on which of the sources of value creation identified in this chapter. Be specific.

In your opinion, were the financial sponsors placing too great a bet on factors that were beyond their

control? Explain your answer.

Answer: For public firms, LBOs create value by reducing underperformance related to agency conflicts

between management and shareholders; for private firms, LBOs improve access to capital. For both

public and private firms, LBOs create value by temporarily shielding the firm from taxes, reducing debt,

improving operating performance, and timing properly the sale of the business. In the case of the TXU

2. How does the postclosing holding company structure protect the interests of the financial sponsor group

and the utility’s customers but potentially jeopardize creditor interests in the event of bankruptcy?

20

Answer: A holding company structure was used for two reasons: (1) to limit the risks to the financial and

creditor groups to potential liabilities and (2) to satisfy the requirement by Texas public utility regulators

to insulate the public utility from the additional debt service requirements created by the debt incurred to

finance the LBO. The structure effectively concentrates debt in EFH and TH, while separating the cash

3. What was the purpose of the pre-closing covenants and closing conditions as described in the merger

agreement?

Answer: The purpose of the covenants is to ensure that the target firm will operate its business between

the signing of the agreement and closing in a manner acceptable to the buyer. Also, it gives the buyer a

4. Loan covenants exist to protect the lender. How might such covenants inhibit the EFH from meeting its

2014 $20 billion obligations?

Answer: The loan covenants limit EFH’s ability to issue new equity, preferred stock, or to take on new

INFORMATICA GOES PRIVATE TO IMPLEMENT

AN AGGRESSIVE SPENDING PROGRAM

Key Points

• Firms hoping to spur growth through new capital investments and takeovers often find it difficult to do so as a

public firm due to investor impatience

• One option is to take the firm private