E13-21, cont.

Requirement 2

E13-22 Journalizing issuance of stock and preparing the stockholders’ equity section of the

balance sheet

Learning Objective 2

March 23 Common Stock $210 CR

The charter of Cherry Blossom Corporation authorizes the issuance of 900 shares of preferred stock and

3,500 shares of common stock. During a two-month period, Cherry Blossom completed these stock-

issuance transactions:

Requirements

1. Record the transactions in the general journal.

WCAP-TV, Inc.

Balance Sheet (Partial)

September 30, 2016

Stockholders’ Equity

Paid-In Capital:

Preferred Stock, $2, no-par; 100,000 shares authorized, 300 shares

issued and outstanding

$ 24,000

Total Paid-In Capital

Retained Earnings

$ 88,250

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Mar. 23

Cash ($10 per share × 210 shares)

2,100

Common Stock—$1 Par Value ($1 per share × 210 shares)

210

Paid-In Capital in Excess of Par—Common ($2,100 – $210)

1,890

Issued common stock for cash.

Inventory

Equipment

Common Stock—$1 Par Value ($1 per share × 350 shares)

350

Issued common stock for inventory and equipment.

17

Cash ($50 per share × 900 shares)

Preferred Stock—$50 Par Value

Issued preferred stock for cash.

Requirement 2

Total Paid-In Capital

CHERRY BLOSSOM CORPORATION

Balance Sheet (Partial)

April 30, 2016

Stockholders’ Equity

Paid-In Capital:

Preferred Stock, 6%, $50 par value; 900 shares authorized, issued

E13-23 Journalizing treasury stock transactions and reporting stockholders’ equity

Learning Objective 3

2. Total Stockholders’ Equity $53,500

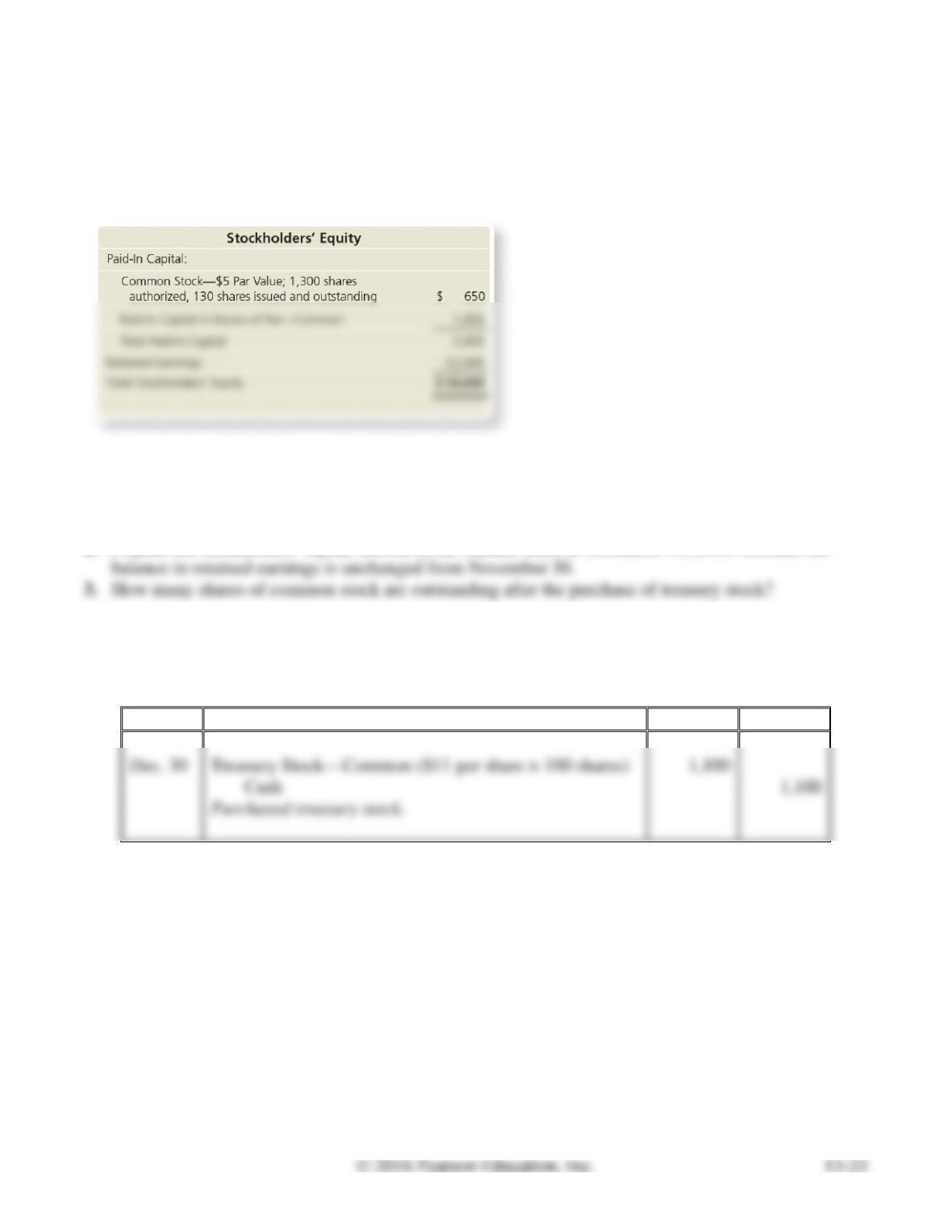

Pioneer Amusements Corporation had the following stockholders’ equity on November 30:

On December 30, Pioneer purchased 100 shares of treasury stock at $11 per share.

Requirements

1. Journalize the purchase of the treasury stock.

2. Prepare the stockholders’ equity section of the balance sheet at December 31, 2016. Assume the

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

E13-23, cont.

Requirement 2

Total Paid-In Capital

Requirement 3

There are 30 shares outstanding after the purchase of the treasury stock (130 shares − 100 shares).

E13-24 Journalizing issuance of stock and treasury stock transactions

Learning Objectives 2, 3

Sept. 22 Treasury Stock $3,300 CR

Stock transactions for Cautious Driving School, Inc. follow:

PIONEER AMUSEMENTS CORPORATION

Balance Sheet (Partial)

December 31, 2016

Stockholders’ Equity

Paid-In Capital:

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Mar. 4

Cash ($8 per share × 29,000 shares)

232,000

Common Stock ($1 per share × 29,000 shares)

29,000

Paid-In Capital in Excess of Par—Common ($232,000 − $29,000)

203,000

Issued common stock for cash.

May 22

9,900

Cash

9,900

Purchased treasury stock.

Sep. 22

Cash ($25 per share × 300 shares)

7,500

Treasury Stock—Common ($11 cost per share × 300 shares)

3,300

Paid-In Capital from Treasury Stock Transactions ($14 × 300 shares)

4,200

Sold treasury stock with cost of $11 per share.

Oct. 14

Cash ($6 per share × 600 shares)

3,600

Paid-In Capital from Treasury Stock Transactions ($5 × 600 shares)

3,000

Treasury Stock—Common ($11 cost per share × 600 shares)

6,600

Sold treasury stock with cost of $11 per share.

E13-25 Computing dividends on preferred and common stock and journalizing

Learning Objective 4

1. Preferred Dividend 2016 $7,680

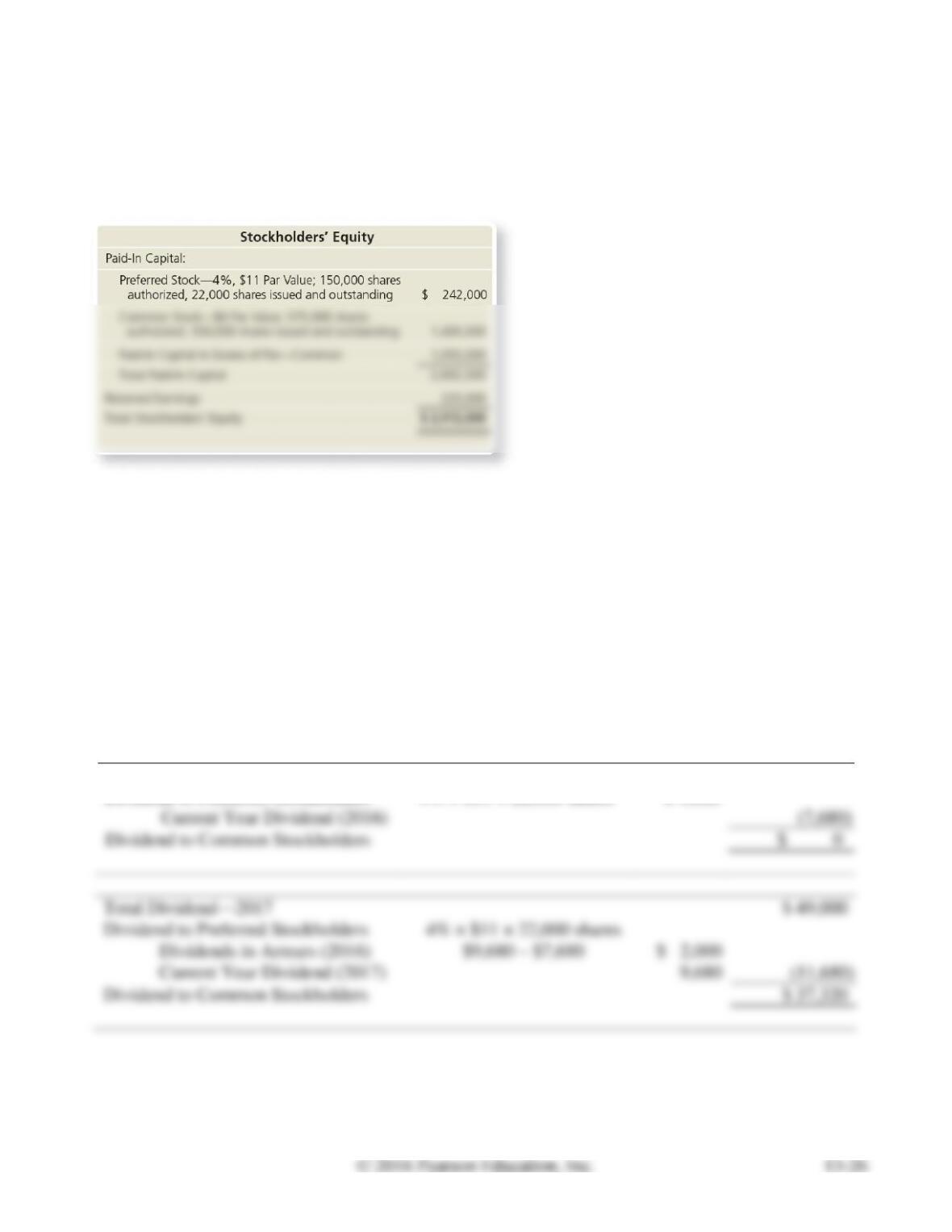

Horizon Communications has the following stockholders’ equity on December 31, 2016:

Requirements

1. Assuming the preferred stock is cumulative, compute the amount of dividends to preferred

stockholders and to common stockholders for 2016 and 2017 if total dividends are $7,680 in 2016

and $49,000 in 2017. Assume no changes in preferred stock and common stock in 2017.

2. Record the journal entries for 2016, assuming that Horizon Communications declared the dividend

on December 1 for stockholders of record on December 10. Horizon Communications paid the

dividend on December 20.

SOLUTION

Requirement 1

Total Dividend—2016

$ 7,680

Dividend to Preferred Stockholders

4% × $11 × 22,000 shares

$ 9,680

Dividend to Common Stockholders

Total Dividend—2017

Dividend to Preferred Stockholders

Dividend to Common Stockholders

E13-25, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2016

Dec. 1

Cash Dividends

7,680

Dividends Payable—Preferred

7,680

7,680

7,680

E13-26 Computing dividends on preferred and common stock and journalizing

Learning Objective 4

2. July 1 Cash Dividends $155,000 DR

The following elements of stockholders’ equity are from the balance sheet of Sacchetti Marketing Corp.

at December 31, 2015:

Sacchetti paid no preferred dividends in 2015.

Requirements

1. Compute the dividends to the preferred and common shareholders for 2016 if total dividends are

$155,000 and assuming the preferred stock is noncumulative.

2. Record the journal entries for 2016 assuming that Sacchetti Marketing Corp. declared the dividends

on July 1 for stockholders of record on July 15. Sacchetti paid the dividends on July 31.

SOLUTION

Requirement 1

Total Dividend—2016

$ 155,000

$ 150,500

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2016

July 1

Cash Dividends

155,000

Dividends Payable—Preferred

4,500

Dividends Payable—Common

150,500

4,500

150,500

155,000

E13-27 Journalizing a stock dividend and reporting stockholders’ equity

Learning Objective 4

2. Total Stockholders’ Equity $127,600

The stockholders’ equity of Poolside Occupational Therapy, Inc. on December 31, 2015, follows:

On April 30, 2016, the market price of Poolside’s common stock was $15 per share and the company

declared a 8% stock dividend. The stock was distributed on May 15.

Requirements

1. Journalize the declaration and distribution of the stock dividend.

2. Prepare the stockholders’ equity section of the balance sheet as of May 31, 2015. Assume Retained

Earnings are $124,000 on April 30, 2016, before the stock dividend, and the only change made to

Retained Earnings before preparing the balance sheet was closing the Stock Dividends account.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Apr. 30

Stock Dividends ($15 per share × 600 × 0.08)

720

Common Stock Dividend Distributable ($2 per share × 600 × 0.08)

96

624

May 15

Common Stock Dividend Distributable

96

96

E13-27, cont.

Requirement 2

E13-28 Journalizing cash and stock dividends

Learning Objective 4

1. Common Stock $15,200 CR

Pottery Schools, Inc. is authorized to issue 200,000 shares of $2 par common stock. The company issued

76,000 shares at $4 per share. When the market price of common stock was $6 per share, Pottery

declared and distributed a 10% stock dividend. Later, Pottery declared and paid a $0.10 per share cash

dividend.

Requirements

1. Journalize the declaration and the distribution of the stock dividend.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Stock Dividends ($6 per share × 76,000 shares × 0.10)

45,600

15,200

30,400

Common Stock Dividend Distributable

15,200

15,200

Common Stock Dividend Distributable ($2 per share × 76,000

POOLSIDE OCCUPATIONAL THERAPY, INC.

Balance Sheet (Partial)

May 31, 2016

Stockholders’ Equity

Paid-In Capital:

Total Paid-In Capital

Total Stockholders’ Equity

Common Stock—$2 Par Value; 1,600 shares authorized, 648 shares

E13-28, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Cash Dividends ($0.10 × (76,000 shares + 7,600 shares ))

8,360

8,360

8,360

8,360

E13-29 Reporting stockholders’ equity after a stock split

Learning Objective 4

Total Stockholders’ Equity $4,120

Tour Golf Club Corp. had the following stockholders’ equity at December 31, 2015:

On June 30, 2016, Tour split its common stock 2-for-1. Prepare the stockholders’ equity section of the

balance sheet immediately after the split. Assume the balance in retained earnings is unchanged from

December 31, 2015.

SOLUTION

TOUR GOLF CLUB, CORP.

Balance Sheet (Partial)

June 30, 2106

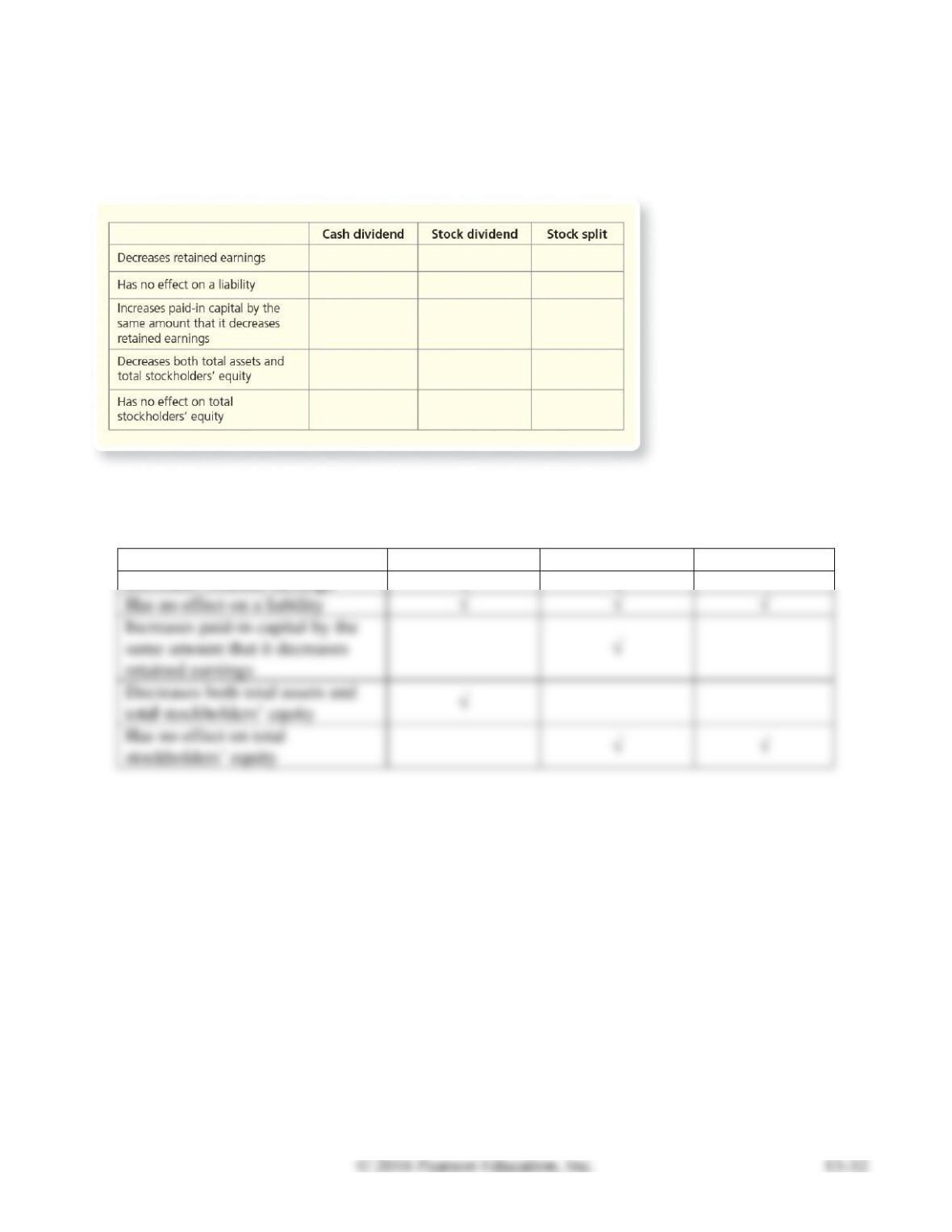

E13-30 Determining the effects of cash dividends, stock dividends, and stock splits

Learning Objective 4

Complete the following chart by inserting a check mark (?) for each statement that is true.

SOLUTION

Cash dividend

Stock dividend

Stock split

Decreases retained earnings

√

√

Has no effect on a liability

√

√

E13-31 Determining the effect of stock dividends, stock splits, and treasury stock transactions

Learning Objectives 3, 4

Many types of transactions may affect stockholders’ equity. Identify the effects of the following

transactions on total stockholders’ equity. Each transaction is independent.

a. A 10% stock dividend. Before the dividend, 560,000 shares of $1 par value common stock were

outstanding; market value was $10 per share at the time of the dividend.

b. A 2-for-1 stock split. Prior to the split, 65,000 shares of $1 par value common stock were

outstanding.

c. Purchase of 1,500 shares of $0.50 par treasury stock at $7 per share.

d. Sale of 900 shares of $0.50 par treasury stock for $9 per share. Cost of the treasury stock was $8 per

share.

SOLUTION

a.

No effect (increases Paid-In Capital, but decreases Retained Earnings)

No effect

c.

E13-32 Preparing a statement of retained earnings

Learning Objective 5

Retained Earnings Dec. 31, 2016 $97,000

Susan May Bakery, Inc. reported a prior-period adjustment in 2016. An accounting error caused net

income of prior years to be overstated by $4,000. Retained Earnings at December 31, 2015, as

previously reported, was $42,000. Net income for 2016 was $79,000, and dividends declared were

$20,000. Prepare the company’s statement of retained earnings for the year ended December 31, 2016.

SOLUTION

SUSAN MAY BAKERY, INC.

Statement of Retained Earnings

Retained Earnings, January 1, 2016, as originally reported

Prior Period Adjustment

Retained Earnings, January 1, 2016, as adjusted

Net income for the year

Dividends Declared

Retained Earnings, December 31, 2016

E13-33 Computing earnings per share and price/earnings ratio

Learning Objective 6

Temple Corp. earned net income of $128,500 and paid the minimum dividend to preferred stockholders

for 2016. Assume that there are no changes in common shares outstanding. Temple’s books include the

following figures:

Requirements

1. Compute Temple’s EPS for the year.

2. Assume Temple’s market price of a share of common stock is $8 per share. Compute Temple’s

price/earnings ratio.

SOLUTION

Requirement 1

Earnings per

share

=

(Net income − Preferred

dividends)

/

Average number of common shares

outstanding

Requirement 2

Price/earnings

ratio

=

Market price per share of common stock

/

Earnings per share

$3.20 per share

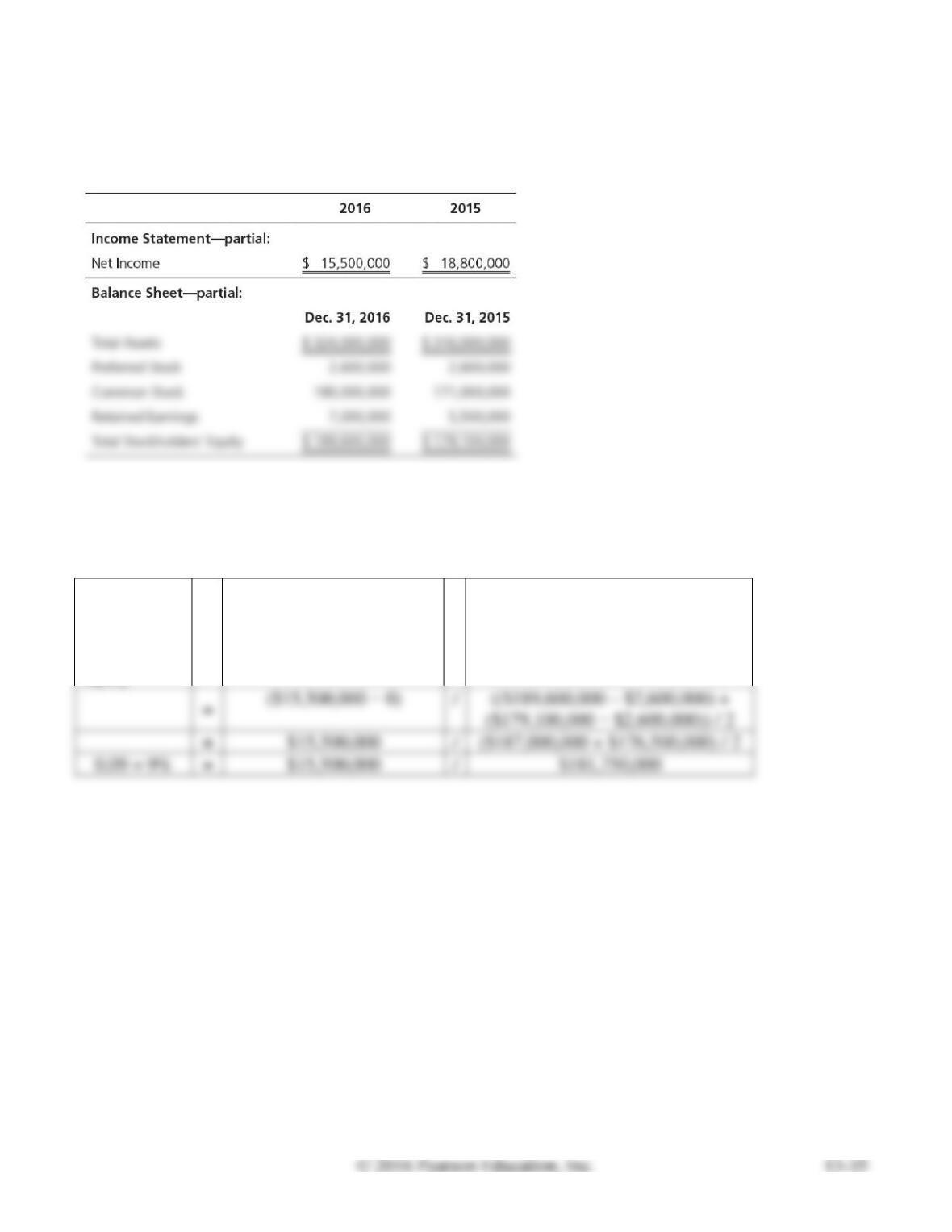

E13-34 Computing rate of return on common stockholders’ equity

Learning Objective 6

Louisville Exploration Company reported these figures for 2016 and 2015:

Compute rate of return on common stockholders’ equity for 2016 assuming no dividends were paid to

preferred stockholders.

SOLUTION

Rate of

return on

common

stockholders’

equity

=

(Net income − Preferred

dividends)

/

Average common stockholders’

equity = Total equity – preferred

equity

Problems (Group A)

P13-35A Organizing a corporation and issuing stock

Learning Objectives 1, 2

John and Michael are opening a paint store. There are no competing paint stores in the area. They must

Requirements

1. What is the main advantage they gain by selecting a corporate form of business now?

2. Would you recommend they initially issue preferred or common stock? Why?

3. If they decide to issue $10 par common stock and anticipate an initial market price of $40 per share,

how many shares will they need to issue to raise $2,250,000?

SOLUTION

Requirement 1

Students’ answers may vary. The following are advantages of the corporate form of business. A

corporation:

a. Does not hold individual stockholders personally liable for the debts of the corporation

e. Makes transfer of ownership easy

Requirement 2

Requirement 3

P13-36A Identifying sources of equity, stock issuance, and dividends

Learning Objectives 1, 2, 4

4. Common stock dividends $840,000

Travel Comfort Specialists, Inc. reported the following stockholders’ equity on its balance sheet at June

30, 2016:

Requirements

1. Identify the different classes of stock that Travel has outstanding.

2. What is the par value per share of Travel’s preferred stock?

3. Make two summary journal entries to record issuance of all the Travel stock for cash. Explanations

are not required.

SOLUTION

Requirement 1

Requirement 2

P13-36A, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Cash

1,000,000

1,000,000

Cash

4,020,000

1,320,000

2,700,000

Requirement 4

Total Dividend—2016

$ 900,000

Dividend to Preferred Stockholders

$ 60,000

Dividend to Common Stockholders

$ 840,000

Date

Accounts and Explanation

Debit

Credit

2016

June 30

Cash Dividends

900,000

Dividends Payable—Preferred

60,000

Dividends Payable—Common

840,000

July 20

60,000

840,000

900,000

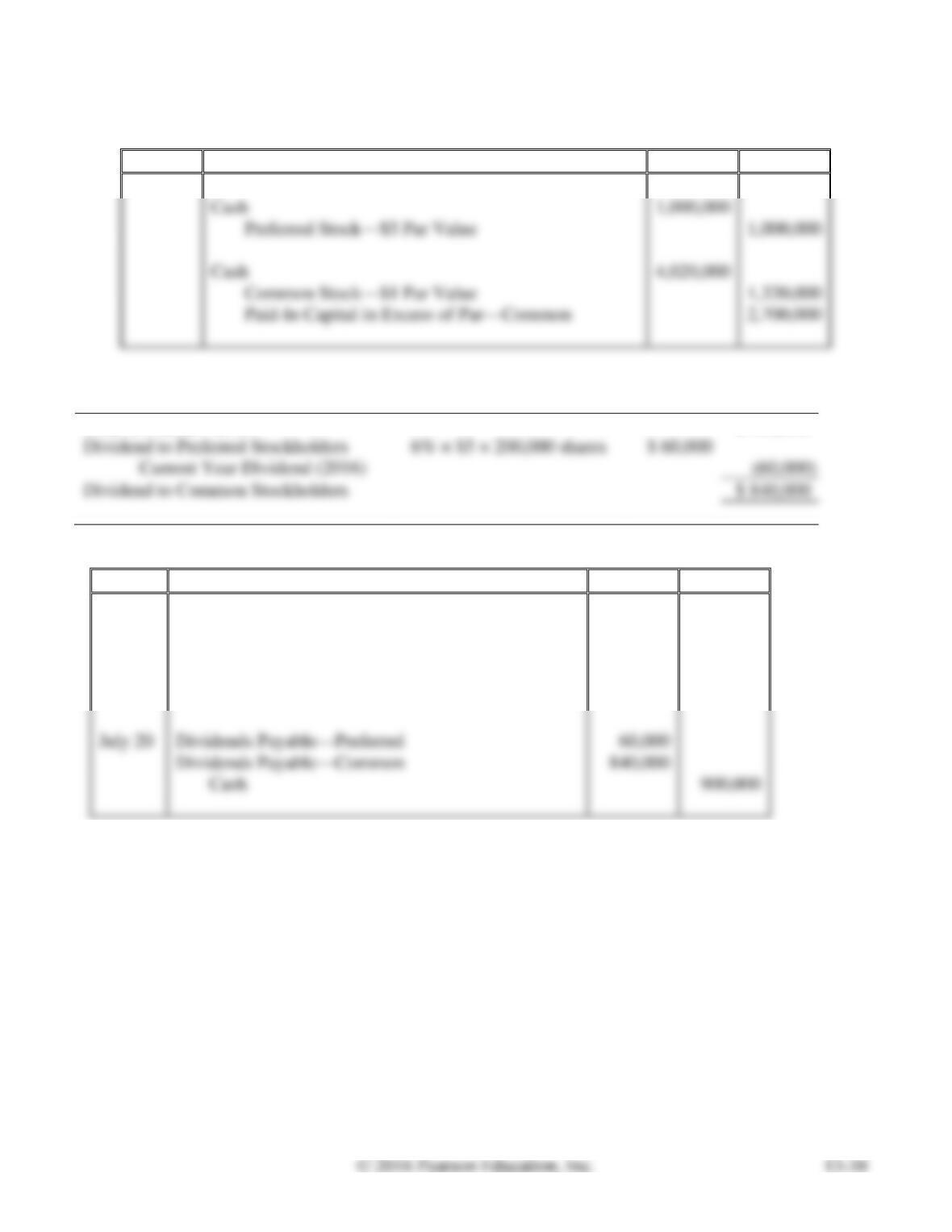

P13-37A Journalizing stock issuance and cash dividends and preparing the stockholders’ equity

section of the balance sheet

Learning Objectives 2, 4

2. Total Stockholders’ Equity $323,000

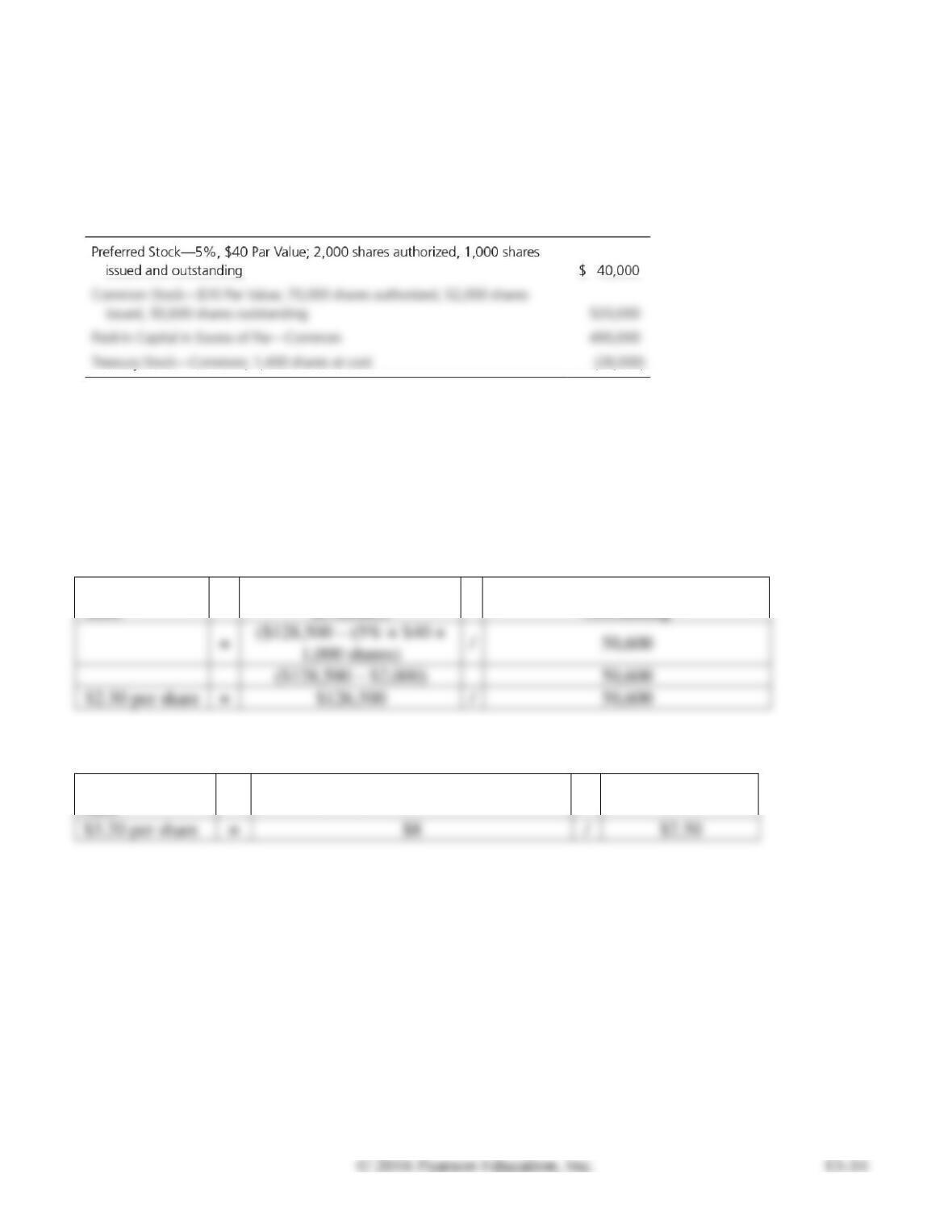

C-C ell Wireless needed additional capital to expand, so the business incorporated. The charter from the

state of Georgia authorizes C-Cell to issue 50,000 shares of 7%, $50 par value cumulative preferred

stock and 120,000 shares of $2 par value common stock. During the first month, C-Cell completed the

following transactions:

Requirements

1. Record the transactions in the general journal.

2. Prepare the stockholders’ equity section of C–Cell’s balance sheet at October 31, 2016. Assume C–

Cell’s net income for the month was $96,000.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Oct. 2

Building

120,000

Common Stock—$2 Par Value ($2 per share × 22,000 shares)

44,000

76,000

Cash ($70 per share × 900 shares)

63,000

Preferred Stock—$50 Par Value ($50 per share × 900 shares)

45,000

Paid-In Capital in Excess of Par—Preferred ($63,000 − $45,000)

18,000

Cash

60,000

Common Stock—$2 Par Value ($2 per share × 12,000 shares)

24,000

Paid-In Capital in Excess of Par—Common ($60,000 – $24,000)

36,000

Cash Dividends

16,000

Dividends Payable—Preferred

Dividends Payable—Common

12,850

12,850

16,000

*Total Dividend

$ 16,000

Dividend to Preferred Stockholders

7% × $50 × 900 shares

$ 3,150

(3,150)

Dividend to Common Stockholders

$ 12,850