40

2. Having pledged not to engage in aggressive cost cutting, how do you think HCA and its financial sponsor

group planned on paying off the loans?

Answer: The financial sponsor group is assuming that increased government spending in view of the

Case Study. Sony Buys MGM

Sony’s long-term vision has been to create synergy between its consumer electronics products and music, movies, and

games. Sony, which bought Columbia Pictures in 1989 for $3.4 billion, had wanted to control Metro-Goldwyn-Mayer’s

film library for years, but it did not want to pay the estimated $5 billion it would take to acquire it. On September 14,

2004, a consortium, consisting of Sony Corp of America, Providence Equity Partners, Texas Pacific Group, and DLJ

Merchant Banking Partners, agreed to acquire MGM for $4.8 billion, consisting of $2.85 billion in cash and the

assumption of $2 billion in debt. The cash portion of the purchase price consisted of about $1.8 billion in debt and $1

billion in equity capital. Of the equity capital, Providence contributed $450 million, Sony and Texas Pacific Group

$300 million, and DLJ Merchant Banking $250 million.

The combination of Sony and MGM will create the world’s largest film library of about 7,600 titles, with MGM

contributing about 54 percent of the combined libraries. Sony will control MGM and Comcast will distribute the films

over cable TV. Sony will shut down MGM’s film making operations and move all operations to Sony. Kirk Kerkorian,

who holds a 74 percent stake in MGM, will make $2 billion because of the transaction. The private equity partners

could cash out within three-to-five years, with the consortium undertaking an initial public offering or sale to a strategic

investor. Major risks include the ability of the consortium partners to maintain harmonious relations and the

problematic growth potential of the DVD market.

Discussion Questions:

1. Do you believe that MGM is an attractive LBO candidate? Why? Why not?

Answer: MGM made an attractive LBO candidate because of its ownership of a large film library, which

41

2. In what way do you believe that Sony’s objectives might differ from those of the private equity investors

making up the remainder of the consortium? How might such differences affect the management of MGM?

Identify possible short-term and long-term effects.

Answer: Sony wanted to gain access to the film library to help provide content for the growth in its play

3. How did Time Warner’s entry into the bidding affect pace of the negotiations and the relative bargaining

power of MGM, Time Warner, and the Sony consortium?

Answer: The bargaining was contentious and stalled for 5 months until Time Warner converted the bilateral

4. What do you believe were the major factors persuading the MGM board to accept the Revised Sony bid? In

your judgment, do these factors make sense? Explain your answer.

Answer: MGM’s board and Kirk Kerkorian, MGM’s largest shareholder, were uncertain about the future

RJR NABISCO GOES PRIVATE—

KEY SHAREHOLDER AND PUBLIC POLICY ISSUES

Background

The largest LBO in history is as well known for its theatrics as it is for its substantial improvement in shareholder

value. In October 1988, H. Ross Johnson, then CEO of RJR Nabisco, proposed an MBO of the firm at $75 per share.

His failure to inform the RJR board before publicly announcing his plans alienated many of the directors. Analysts

outside the company placed the breakup value of RJR Nabisco at more than $100 per share—almost twice its then

current share price. Johnson’s bid immediately was countered by a bid by the well-known LBO firm, Kohlberg, Kravis,

and Roberts (KKR), to buy the firm for $90 per share (Wasserstein, 1998). The firm’s board immediately was faced

with the dilemma of whether to accept the KKR offer or to consider some other form of restructuring of the company.

The board appointed a committee of outside directors to assess the bid to minimize the appearance of a potential

conflict of interest in having current board members, who were also part of the buyout proposal from management, vote

on which bid to select.

Aggressive pricing actions by such competitors as Phillip Morris threatened to erode RJR Nabisco’s ability to

service its debt. Complex securities such as “increasing rate notes,” whose coupon rates had to be periodically reset to

42

ensure that these notes would trade at face value, ultimately forced the credit rating agencies to downgrade the RJR

Nabisco debt. As market interest rates climbed, RJR Nabisco did not appear to have sufficient cash to accommodate the

additional interest expense on the increasing return notes. To avoid default, KKR recapitalized the company by

investing additional equity capital and divesting more than $5 billion worth of businesses in 1990 to help reduce its

crushing debt load. In 1991, RJR went public by issuing more than $1 billion in new common stock, which placed

about one-fourth of the firm’s common stock in public hands.

When KKR eventually fully liquidated its position in RJR Nabisco in 1995, it did so for a far smaller profit than

expected. KKR earned a profit of about $60 million on an equity investment of $3.1 billion. KKR had not done well for

the outside investors who had financed more than 90% of the total equity investment in KKR. However, KKR fared

much better than investors had in its LBO funds by earning more than $500 million in transaction fees, advisor fees,

management fees, and directors’ fees. The publicity surrounding the transaction did not cease with the closing of the

transaction. Dissident bondholders filed suits alleging that the payment of such a large premium for the company

represented a “confiscation” of bondholder wealth by shareholders.

Potential Conflicts of Interest

In any MBO, management is confronted by a potential conflict of interest. Their fiduciary responsibility to the

shareholders is to take actions to maximize shareholder value; yet in the RJR Nabisco case, the management bid

appeared to be well below what was in the best interests of shareholders. Several proposals have been made to

Winners and Losers

RJR Nabisco shareholders before the buyout clearly benefited greatly from efforts to take the company private.

However, in addition to the potential transfer of wealth from bondholders to stockholders, some critics of LBOs argue

that a wealth transfer also takes place in LBO transactions when LBO management is able to negotiate wage and

benefit concessions from current employee unions. LBOs are under greater pressure to seek such concessions than

other types of buyouts because they need to meet huge debt service requirements.

Discussion Questions:

1. In your opinion, was the buyout proposal presented by Ross Johnson’s management group in the best interests

of the shareholders? Why? / Why not?

Answer: No. The management group proposed to buy the firm for $75 per share. Immediately, outside

analysts placed a break-up value of the firm of at least $100 per share. The firm was finally sold for more than

2. What were the RJR Nabisco board’s fiduciary responsibilities to the shareholders? How well did they satisfy

these responsibilities? What could/should they have done differently?

Answer: The board’s fiduciary responsibilities were to maximize shareholder value. The board’s actions

43

3. Why might the RJR Nabisco board have accepted the KKR bid over the Johnson bid?

4. How might bondholders and preferred stockholders have been hurt in the RJR Nabisco leveraged buyout?

Answer: One of the most contentious discussions immediately following the closing of the RJR Nabisco

buyout centered on the alleged transfer of wealth from bond and preferred stockholders to common

5. Describe the potential benefits and costs of LBOs to shareholders, employers, lenders, customers, and

communities in which the firm undergoing the buyout may have operations. Do you believe that on average

LBOs provide a net benefit or cost to society? Explain your answer.

Answer: RJR Nabisco shareholders prior to the buyout clearly benefited greatly from efforts to take the

company private. However, in addition to the potential transfer of wealth from bondholders to stockholders,

some critics of LBOs argue that a wealth transfer also takes place in LBO transactions when LBO

management is able to negotiate wage and benefit concessions from current employee unions. LBOs are under

Case Study. Private Equity Firms Acquire Yellow Pages Business

Qwest Communications agreed to sell its yellow pages business, QwestDex, to a consortium led by the Carlyle Group

and Welsh, Carson, Anderson and Stowe for $7.1 billion. In a two stage transaction, Qwest sold the eastern half of the

yellow pages business for $2.75 billion in late 2002. This portion of the business included directories in Colorado,

Iowa, Minnesota, Nebraska, New Mexico, South Dakota, and North Dakota. The remainder of the business, Arizona,

Idaho, Montana, Oregon, Utah, Washington, and Wyoming, was sold for $4.35 billion in late 2003. Caryle and Welsh

Carson each put in $775 million in equity (about 21 percent of the total purchase price).

Qwest was in a precarious financial position at the time of the negotiation. The telecom was trying to avoid

bankruptcy and needed the first stage financing to meet impending debt repayments due in late 2002. Qwest is a local

phone company in 14 western states and one of the nation’s largest long-distance carriers. It had amassed $26.5 billion

in debt following a series of acquisitions during the 1990s.

The Carlyle Group has invested globally, mainly in defense and aerospace businesses, but it has also invested in

companies in real estate, health care, bottling, and information technology. Welsh Carson focuses primarily on the

44

communications and health care industries. While the yellow pages business is quite different from their normal areas

of investment, both firms were attracted by its steady cash flow. Such cash flow could be used to trim debt over time

Discussion Questions:

1. Why was QwestDex considered an attractive LBO candidate? Do you think it has significant growth potential?

Explain the following statement: “A business with high growth potential may not be a good candidate for an LBO.

QwestDex was considered an attractive candidate because of its steadily growing, highly predictable cash flow,

2. Why did the buyout firms want a 50-year contract to be the exclusive provider of publishing services to Qwest

Communications?

3. Why would the buyout firms want Qwest to continue to provide such services as billing and information

technology support? How might such services be priced?

The buyers wanted to ensure a flawless transition of payroll, IT, and other administrative support services when the

4. Why would it take five very large financial institutions to finance the transactions?

The $7.1 billion transaction was large by conventional LBO standards. By borrowing from a consortium of banks,

5. Why was the equity contribution of the buyout firms as a percentage of the total capital requirements so much

higher than amounts contributed during the 1980s?

The equity contribution amounted to about one-fifth of the total purchase price, two-to-three times the average of

Cox Enterprises Offers to Take Cox Communications Private

In an effort to take the firm private, Cox Enterprises announced on August 3, 2004 a proposal to buy the remaining

38% of Cox Communications’ shares that they did not currently own for $32 per share. Cox Communications is the

45

third largest provider of cable television, telecommunications, and wireless services in the U.S, serving more than 6.2

million customers. Historically, the firm’s cash flow has been steady and substantial.

The deal is valued at $7.9 billion and represented a 16% premium to Cox Communication’s share price at that time.

Cox Communications would become a subsidiary of Cox Enterprises and would continue to operate as an autonomous

business. In response to the proposal, the Cox Communications Board of Directors formed a special committee of

independent directors to consider the proposal. Citigroup Global Markets and Lehman Brothers Inc. have committed

Discussion Questions::

1. Why did the board feel that it was appropriate to set up special committee of independent board directors?

Answer: Special board committees consisting of outside directors often are set up when company insiders are

2. Why does Cox Enterprises believe that the investment needed for growing its cable business is best done

through a private company structure?

Answer: Substantial levels of investment would result in increasing levels of depreciation and amortization

Financing Challenges in the Home Depot Supply Transaction

Buyout firms Bain Capital, Carlyle Group, and Clayton, Dubilier & Rice (CD&R) bid $10.3 billion in June 2007 to buy

Home Depot Inc.’s HD Supply business. HD Supply represented a collection of small suppliers of construction

products. Home Depot had announced earlier in the year that it planned to use the proceeds of the sale to pay for a

portion of a $22.5 billion stock buyback.

Three banks, Lehman Brothers, JPMorgan Chase, and Merril Lynch agreed to provide the firms with a $4 billion

loan. The repayment of the loans was predicated on the ability of the buyout firms to improve significantly HD

Supply’s current cash flow. Such loans are normally made with the presumption that they can be sold to investors, with

the banks collecting fees from both the borrower and investor groups. However, by July, concern about the credit

quality of subprime mortgages spread to the broader debt market and raised questions about the potential for default of

loans made to finance highly leveraged transactions. The concern was particularly great for so-called “covenant–lite”

loans for which the repayment terms were very lenient.

of a $1 billion “covenant–lite” loan and a $1.3 billion “payment–in–kind” loan. Home Depot agreed to assume the loan

payments on the $1 billion loan if the investor firms were to default and to lower the selling price to $8.5 billion for

87.5 percent of HD Supply, with Home Depot retaining the remaining 12.5 percent.

Case Study Discussion Questions:

1. Based on the information given it the case, determine the amount of the price reduction Home Depot accepted

for HD Supply and the amount of cash the three buyout firms put into the transaction?

2. Why did banks lower their lending standards in financing LBOs in 2006 and early 2007? How did the lax

standards contribute to their inability to sell the loans to investors? How did the inability to sell the loans once

made curtail their future lending?

Answer: Banks were willing to lower lending standards in order to generate fee income in what was a highly

Cerberus Capital Management Acquires Chrysler Corporation

According to the terms of the transaction, Cerberus would own 80.1 percent of Chrysler’s auto manufacturing and

financial services businesses in exchange for $7.4 billion in cash. Daimler would continue to own 19.9 percent of the

new business, Chrysler Holdings LLC. Of the $7.4 billion, Daimler would receive $1.35 billion while the remaining

$6.05 billion would be invested in Chrysler (i.e., $5.0 billion is to be invested in the auto manufacturing operation and

$1.05 billion in the finance unit). Daimler also agreed to pay to Cerberus $1.6 billion to cover Chrysler’s long-term debt

and cumulative operating losses during the four months between the signing of the merger agreement and the actual

closing. In acquiring Chrysler, Cerberus assumed responsibility for an estimated $18 billion in unfunded retiree pension

and medical benefits. Daimler also agreed to loan Chrysler Holdings LLC $405 million.

The transaction is atypical of those involving private equity investors, which usually take public firms private,

expecting to later sell them for a profit. The private equity firm pays for the acquisition by borrowing against the firm’s

assets or cash flow. However, the estimated size of Chrysler’s retiree health-care liabilities and the uncertainty of future

cash flows make borrowing impractical. Therefore, Cerberus agreed to invest its own funds in the business to keep it

running while it restructured the business.

47

However, the 2008 credit market meltdown, severe recession, and subsequent free fall in auto sales threatened the

financial viability of Chrysler, despite an infusion of U.S. government capital, and it’s leasing operations as well as

GMAC. GMAC applied for commercial banking status to be able to borrow directly from the U.S. Federal Reserve. In

Discussion Questions and Answers:

1. What were the motivations for this deal from Cerberus’ perspective? From Daimler’s perspective?

Answer: Daimler had demonstrated an inability to realize the originally projected synergies and believed that

the risks of continued ownership outweighed potential future profits. Moreover, relations with the UAW were

such that they were unlikely to get significant relief from the bone-crushing retiree liabilities. In contrast, by

2. What are the risks to this deal’s eventual success? Be specific.

Answer: The risks include the assumption that the UAW will make significant concessions on retiree medical

3. Cite examples of economies of scale and scope?

4. Cerberus and Daimler will own 80.1% and 19.9% of Chrysler Holdings LLC, respectively. Why do you think

the two parties agreed to this distribution of ownership?

5. Which of the leading explanations of why deals sometimes fail to meet expectations best explains why the

combination of Daimler and Chrysler failed? Explain your answer.

6. The new company, Chrysler Holdings, is a limited liability company. Why do you think CCM chose this legal

structure over a more conventional corporate structure?

48

Pacific Investors Acquires California Kool in a Leveraged Buyout

Pacific Investors (PI) is a small private equity limited partnership with $3 billion under management. The objective of

the fund is to give investors at least a 30-percent annual average return on their investment by judiciously investing

these funds in highly leveraged transactions. PI has been able to realize such returns over the last decade because of its

focus on investing in industries that have slow but predictable growth in cash flow, modest capital investment

requirements, and relatively low levels of research and development spending. In the past, PI made several lucrative

investments in the contract packaging industry, which provides packaging for beverage companies that produce various

types of noncarbonated and carbonated beverages. Because of its commitments to its investors, PI likes to liquidate its

investments within four to six years of the initial investment through a secondary public offering or sale to a strategic

investor.

The owners of CK are demanding a purchase price of $70 million. This is denoted on the balance sheet (see Table

13-15 at the end of the case) as a negative entry in additional paid-in capital. This price represents a multiple of 11.8

times 2003’s net income, almost twice the multiple for comparable publicly traded companies. Despite the “rich”

multiple, PI believes that it can finance the transaction through an equity investment of $25 million and $47 million in

debt. The equity investment consists of $3 million in common stock, with PI’s investors and CK’s management each

contributing $1.5 million. Debt consists of a $12 million revolving loan to meet immediate working capital

requirements, $20 million in senior bank debt secured by CK’s fixed assets, and $15 million in a subordinated loan

from a pension fund. The total cost of acquiring CK is $72 million, $70 million paid to the owners of CK and $2

million in legal and accounting fees.

The deal would appear to make sense from the standpoint of PI, since the projected average annual internal rates of

return (IRRs) for investors exceed PI’s minimum desired 30 percent rate of return in all scenarios considered between

2007 and 2009 (see Table 13-13). This is the period during which investors would like to “cash out.” The rates of return

scenarios are calculated assuming the business can be sold at different multiples of adjusted equity cash flow in the

year in which the business is assumed to be sold. Consequently, IRRs are calculated using the cash outflow (initial

equity investment in the business) in the first year offset by any positive equity cash flow from operations generated in

49

the first year, equity cash flows for each subsequent year, and the sum of equity cash flow in the year in which the

business is sold or taken public plus the estimated sale value (e.g., eight times equity cash flow) in that year. Adjusted

equity cash flow includes free cash flow generated from operations and the increase in “investments available for sale.”

Such investments represent cash generated in excess of normal operating requirements; and as such, this cash is

available to LBO investors.

Discussion Questions

1. What criteria did Pacific Investors (PI) use to select California Kool (CK) as a target for an LBO? Why

were these criteria employed?

Answer: PI has been able to realize attractive financial returns over the last decade because of their focus

2. Describe how PI financed the purchase price. Speculate as why each source of financing was selected?

How did CK pay for feels incurred in closing the transaction?

Answer: PI financed the purchase price through a modest $3 million equity contribution, one-half of

which was provided by PI investors and the remainder by CK management, $22 million in preferred

stock, and $47 million in debt. The debt consists of a $12 million revolving bank loan, $20 million in

3. What are the advantages and disadvantages of using enterprise cash flow in valuing CK? In what might

EBITDA been a superior (inferior) measure of cash flow for valuing CK?

Answer: Enterprise value includes cash from operating and investing activities but excludes cash from

financing activities. The use this measure requires that the analyst estimate depreciation expense, changes

in working capital, and capital expenditures. Consequently, it requires that the analyst project these

4. Compare and contrast the Cost of Capital Method and the Adjusted Present Value Method of valuation.

50

Answer: From Exhibits 13-1 and 13-2 we see that the APV method provides an estimate of total present

value that is about 7 percent higher than the Cost of Capital Method (CCM). The APV method is

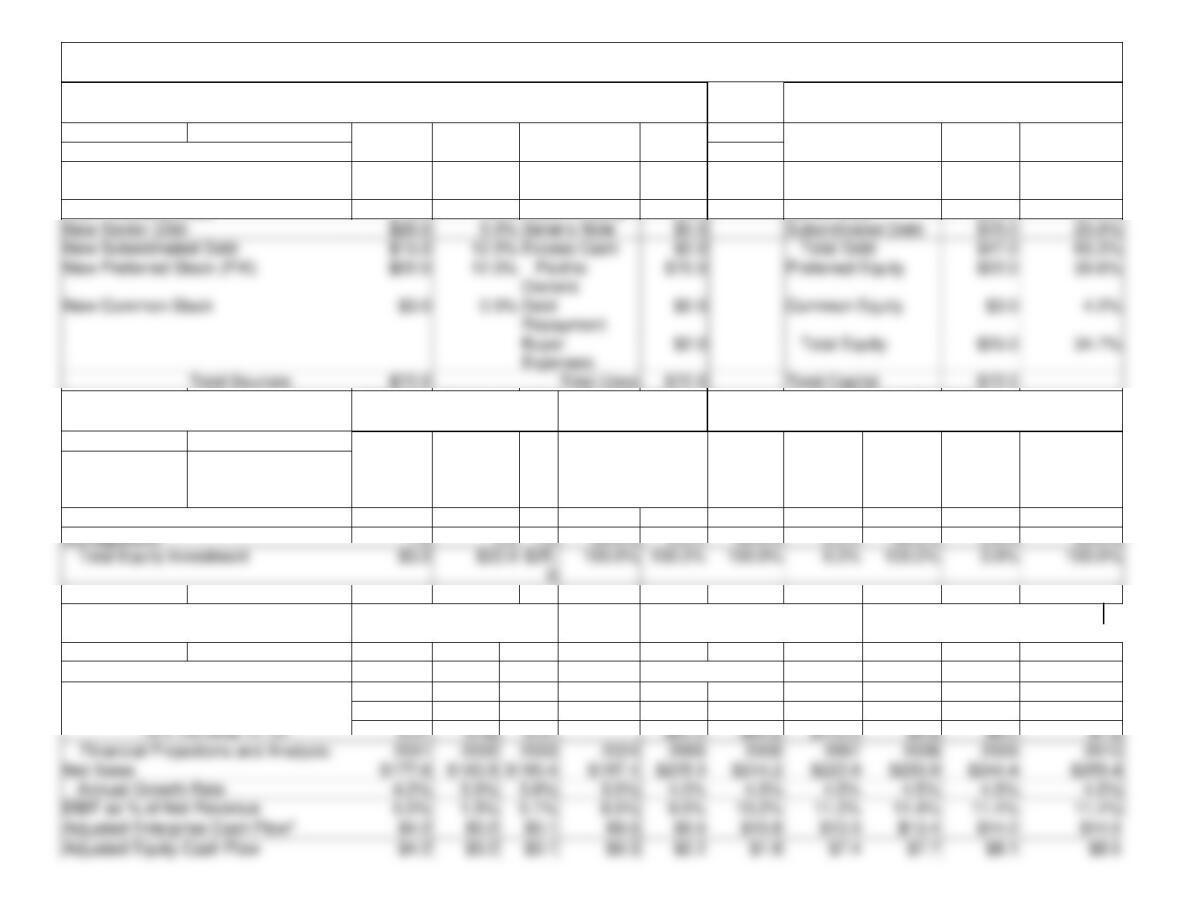

Table 13-11: California Kool Model Output Summary

Sources (Cash Inflows) and Uses (Cash Outflows) of Funds:

Pro Forma Capital Structure

Amount($

)

Interest

Rate (%)

Uses of Funds

Amount

($)

Form of Debt and

Equity

Market

Value

% of Total

Capital

Sources of Funds:

Cash From Balance Sheet

$0.0

0.0%

Cash to

Owners

$70.0

Revolving Loan

$12.0

16.7%

New Revolving Loan

$12.0

9.0%

Seller’s Equity

$0.0

Senior Debt

$20.0

27.8%

Equity Investment:

Ownership Distribution ($)

% Distribution

Fully Diluted Ownership

Distribution

Common

Preferred

Tota

l

Common

Preferre

d

Common

Warrants

Pre–

Option

Ownershi

p

Perform.

Options

Fully Dil.

Ownership

Equity Investor

1.5

22.0

23.5

50.0%

100.0%

50.0%

0.0%

50.0%

0.0%

50.0%

Management

1.5

1.5

50.0%

0.0%

50.0%

0.0%

50.0%

0.0%

50.0%

$3.0

100.0%

Internal Rates of Return:

Total Investor Return (%)

Equity Investor Investment

Gain ($)

Management Investment Gain ($)

2007

2008

2009

2007

2008

2009

2007

2008

2009

Multiple of Adjusted Equity Cash Flow1

0.51

0.42

0.37

$81.0

$94.2

$113.0

$5.2

$6.0

$7.2

2002

2003

2006

2007

2008

2009

8 x Terminal Yr. CF

9 x Terminal Yr. CF

0.42

0.35

0.33

$66.6

$78.9

$96.0

$4.3

$5.0

$6.1

0.46

0.39

0.35

$73.8

$86.6

$104.5

$4.7

$5.5

$6.7

New Senior Debt

$20.0

9.0%

Seller’s Note

$0.0

Subordinated Debt

$15.0

20.8%

New Subordinated Debt

$15.0

12.0%

Excess Cash

$0.0

$47.0

65.3%

New Preferred Stock (PIK)

$70.0

Preferred Equity

30.6%

New Common Stock

$3.0

0.0%

Debt

Repayment

Common Equity

Expenses

Total Sources

$72.0

Total Uses

$72.0

Total Capital

$72.0

52

Total Debt Outstanding

0

0

$47.0

$39.5

$31.5

$23.8

$19.2

$14.3

$8.8

$2.7

Total Debt/Adjusted Enterprise Cash

Flow

0.0

0.0

NA

4.1

3.3

2.2

1.5

1.1

0.6

0.2

EBIT/Interest Expense

0

0

10.1

13.3

18.6

30.9

Val

54

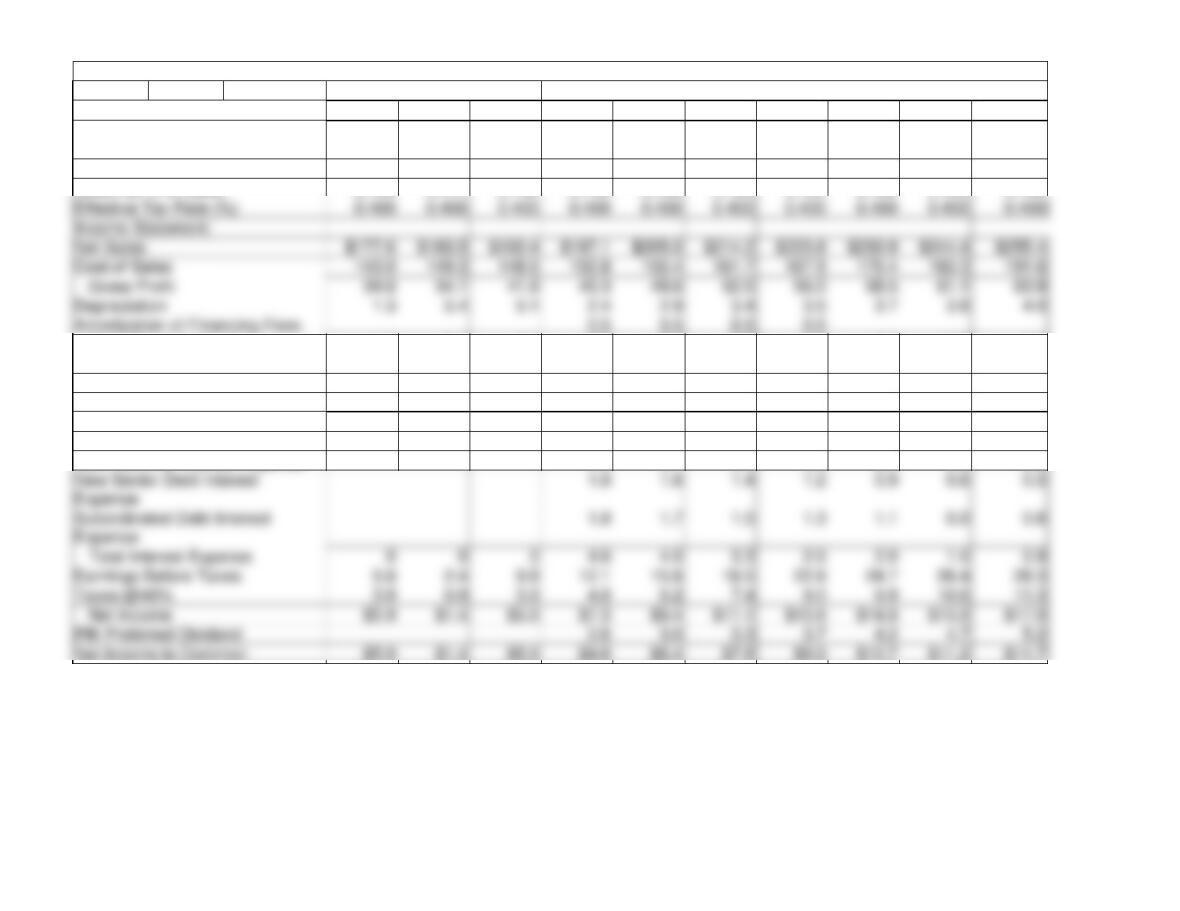

Table 13-12. California Kool Income Statement and Forecast Assumptions

Historical Period

Projections: Twelve Months Ending December 31,

Income Statement Assumptions:

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Net Sales Growth

(%)

0.042

0.033

0.038

0.035

0.040

0.045

0.045

0.045

0.045

0.045

Cost of Sales as % of Sales

0.805

0.814

0.780

0.765

0.758

0.755

0.750

0.750

0.750

0.750

SG&A as % of Sales

0.133

0.144

0.142

0.135

0.130

0.125

0.120

0.120

0.120

0.120

Total Depreciation &

Amortization

1.3

5.4

5.1

2.9

3.4

3.9

4.0

3.7

3.8

4.0

SG&A

23.6

26.4

27.0

26.6

26.6

26.8

26.9

28.1

29.3

30.7

Management Fee

0.1

0.1

0.1

0.1

0.1

0.1

0.1

Operating Income (EBIT)

9.7

2.3

9.7

16.7

19.5

21.7

25.0

26.6

27.8

29.1

(Interest Income)

0.1

0.1

0.1

0.0

0.1

0.1

0.1

0.1

0.1

0.1

New Revolver Interest Expense

1.0

0.7

0.4

0.0

0.0

0.0

0.0

1.8

1.6

1.4

1.2

0.9

0.6

0.3

Expense

4.6

4.0

3.3

2.5

2.0

1.5

0.9

Earnings Before Taxes

9.8

2.4

9.8

12.1

15.6

18.5

22.6

24.7

26.4

28.3

Taxes @40%

3.9

0.9

3.9

4.8

6.2

7.4

9.0

9.9

10.6

11.3

$5.9

$1.4

$5.9

$7.3

$9.4

$11.1

$13.6

$14.8

$15.9

$17.0

PIK Preferred Dividend

2.6

3.0

3.3

3.7

4.2

4.7

5.2

Net Income to Common

$5.9

$1.4

$5.9

$4.6

$6.4

$7.8

$9.9

$10.7

$11.2

$11.7

Effective Tax Rate (%)

0.400

0.400

0.400

0.400

0.400

0.400

0.400

0.400

0.400

0.400

Income Statement:

Net Sales

Cost of Sales

143.0

149.3

148.5

150.8

155.4

161.7

167.9

175.4

183.3

191.6

34.6

34.1

41.9

46.3

49.6

52.5

56.0

58.5

61.1

63.9

Depreciation

1.3

5.4

5.1

2.4

2.9

3.4

3.5

3.7

3.8

4.0

Amortization of Financing Fees

0.5

0.5

0.5

0.5

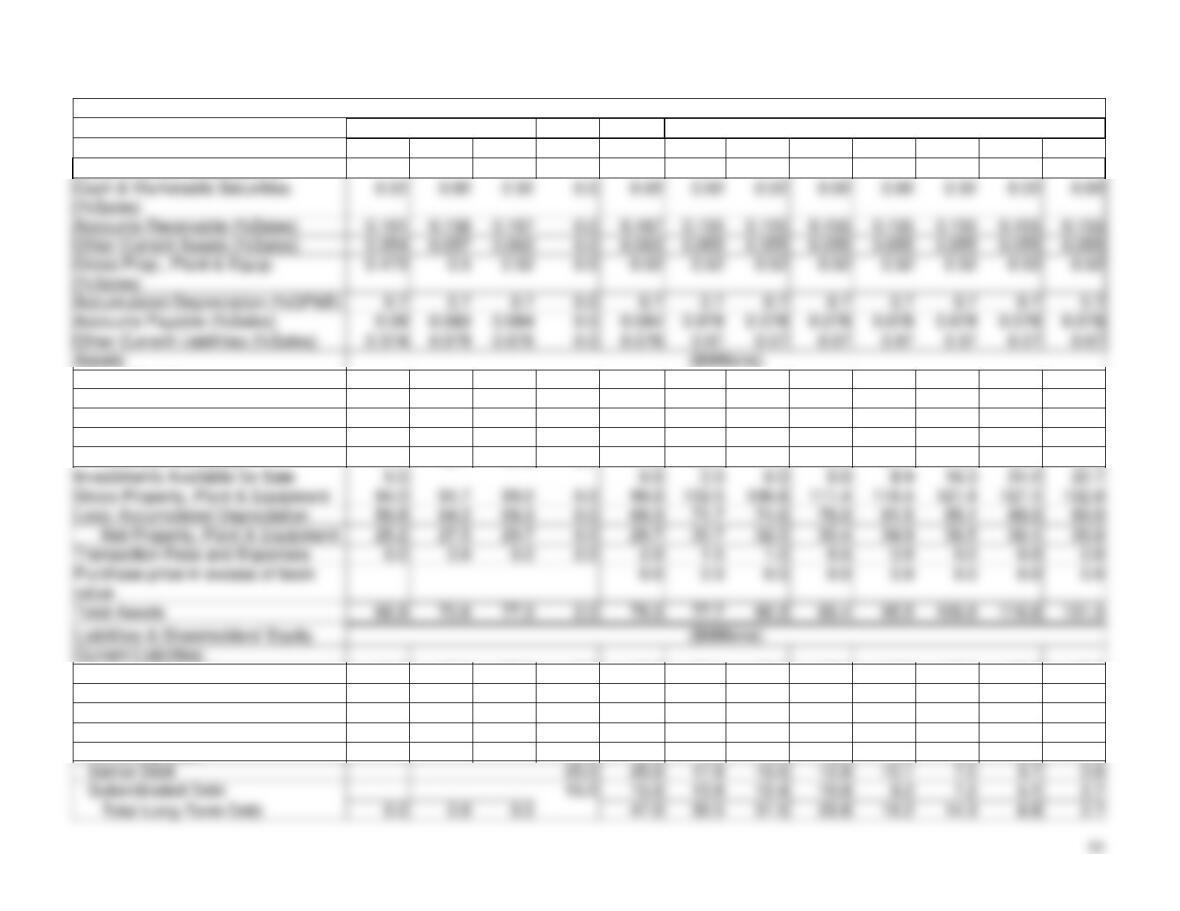

Table 13-13. California Kool Balance Sheet and Forecast Assumptions

Historical Period

Adjust.

Closing

Projections: Twelve Months Ended December,

2001

2002

2003

2003

2004

2005

2006

2007

2008

2009

2010

Balance Sheet Assumptions:

Accounts Receivable (%Sales)

0.0

0.167

Other Current Assets (%Sales)

0.0

0.063

Accumulated Depreciation (%GP&E)

0.7

0.7

0.7

0.0

0.7

0.7

0.7

0.7

0.7

0.7

0.7

0.7

Accounts Payable (%Sales)

0.08

0.0

0.084

Other Current Liabilities (%Sales)

0.0

0.076

0.07

0.07

0.07

0.07

0.07

0.07

0.07

Assets:

Current Assets

Cash and Marketable Securities

3.6

3.7

3.8

0.0

3.8

4.1

4.3

4.5

4.7

4.9

5.1

5.1

Accounts Receivable

28.6

29.0

31.8

0.0

31.8

30.6

31.8

33.2

34.7

36.3

37.9

39.6

Other Current Assets

9.6

10.5

12.0

0.0

12.0

10.8

11.3

11.8

12.3

12.9

13.4

14.0

Total Current Assets

41.7

43.1

47.6

0.0

47.6

45.5

47.3

49.5

51.7

54.0

56.4

58.8

Investments Available for Sale

0.0

0.0

0.0

0.0

8.9

16.3

24.2

32.7

Gross Property, Plant & Equipment

84.0

91.7

99.0

0.0

99.0

Less: Accumulated Depreciation

58.8

64.2

69.3

0.0

69.3

71.7

74.6

78.0

81.5

85.1

89.0

93.0

Net Property, Plant & Equipment

25.2

27.5

29.7

0.0

29.7

30.7

32.0

33.4

34.9

36.5

38.1

39.8

Transaction Fees and Expenses

0.0

0.0

0.0

2.0

2.0

1.5

1.0

0.5

0.0

0.0

0.0

0.0

value

Current Liabilities:

Accounts Payable

14.2

15.2

16.0

0.0

16.0

15.4

16.0

16.7

17.5

18.2

19.1

19.9

Other Current Liabilities

13.1

14.5

14.5

0.0

14.5

13.8

14.3

15.0

15.7

16.4

17.1

17.9

Total Current Liabilities

27.4

29.7

30.5

0.0

30.5

29.2

30.3

31.7

33.1

34.6

36.2

37.8

Long-Term Debt:

Revolving Loan

12.0

12.0

7.9

3.7

0.0

0.0

0.0

0.0

0.0

56

Total Liabilities & Shareholders’

Equity

66.9

70.6

77.3

2.0

79.3

77.7

80.3

85.0

95.5

106.8

118.8

131.3

Shareholders’ Equity

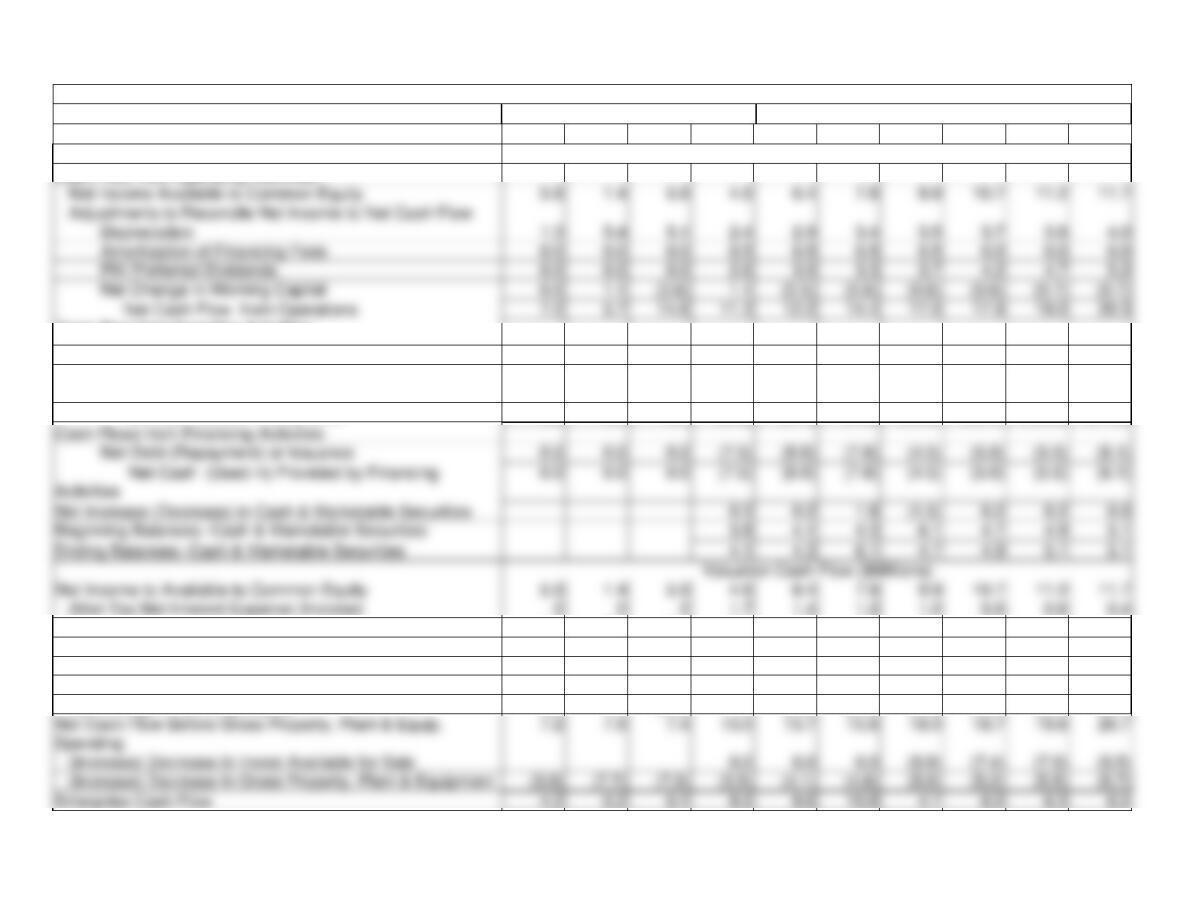

Table 13-14: California Kool Cash Flow Statement and Analysis

Historical Data

Projections: Twelve Months Ended December 31,

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

GAAP Cash Flow ($Millions)

Cash Flow from Operating Activities:

Cash Flow from Investing Activities:

(Increase) Decrease in Investments Available for Sale.

0.0

0.0

0.0

(8.9)

(7.4)

(7.9)

(8.5)

(Increase) Decrease in Gross Property, Plant &

Equipment

(3.5)

(4.1)

(4.8)

(5.0)

(5.2)

(5.5)

(5.7)

Net Cash Used in Investments

0.0

0.0

0.0

(3.5)

(4.1)

(4.8)

(13.9)

(12.7)

(13.3)

(14.2)

Cash Flows from Financing Activities:

Net Debt (Repayment) or Issuance

0.0

0.0

0.0

(7.5)

(8.0)

(7.8)

(4.5)

(5.0)

(5.5)

(6.1)

Net Cash (Used in) Provided by Financing

(7.5)

(8.0)

(7.8)

(4.5)

(5.0)

(5.5)

(6.1)

Net Increase (Decrease) in Cash & Marketable Securities

0.3

0.2

1.8

(1.5)

0.2

0.2

0.0

Beginning Balances—Cash & Marketable Securities

3.8

4.1

4.3

6.1

4.7

4.9

5.1

Ending Balances—Cash & Marketable Securities

4.1

4.3

6.1

4.7

4.9

5.1

5.1

Net Income to Available to Common Equity

5.9

1.4

5.9

4.6

6.4

7.8

9.9

10.7

11.2

11.7

After-Tax Net Interest Expense (Income)

0

0

0

1.7

1.4

1.2

1.0

0.8

0.6

0.4

Depreciation

1.3

5.4

5.1

2.4

2.9

3.4

3.5

3.7

3.8

4.0

Amortization of Financing Fees

0

0

0

0.5

0.5

0.5

0.5

0

0

0

PIK Preferred Dividend

0

0

0

2.6

3.0

3.3

3.7

4.2

4.7

5.2

Net Cash Flow Before Working Capital

7.2

6.8

11.0

11.9

14.2

16.1

18.6

19.3

20.3

21.3

Net Change in Working Capital

0.0

1.1

(3.6)

1.1

(0.5)

(0.6)

(0.6)

(0.6)

(0.7)

(0.7)

Net Income Available to Common Equity

5.9

1.4

5.9

4.6

6.4

7.8

9.9

10.7

11.2

11.7

Adjustments to Reconcile Net Income to Net Cash Flow

Depreciation

1.3

5.4

5.1

2.4

2.9

3.4

3.5

3.7

3.8

4.0

Amortization of Financing Fees

0.0

0.0

0.0

0.5

0.5

0.5

0.5

0.0

0.0

0.0

PIK Preferred Dividends

0.0

0.0

0.0

2.6

3.0

3.3

3.7

4.2

4.7

5.2

Net Change in Working Capital

0.0

1.1

(3.6)

1.1

(0.5)

(0.6)

(0.6)

(0.6)

(0.7)

(0.7)

Net Cash Flow from Operations

7.2

5.7

14.6

11.3

12.2

14.4

17.0

17.9

19.0

20.3

58

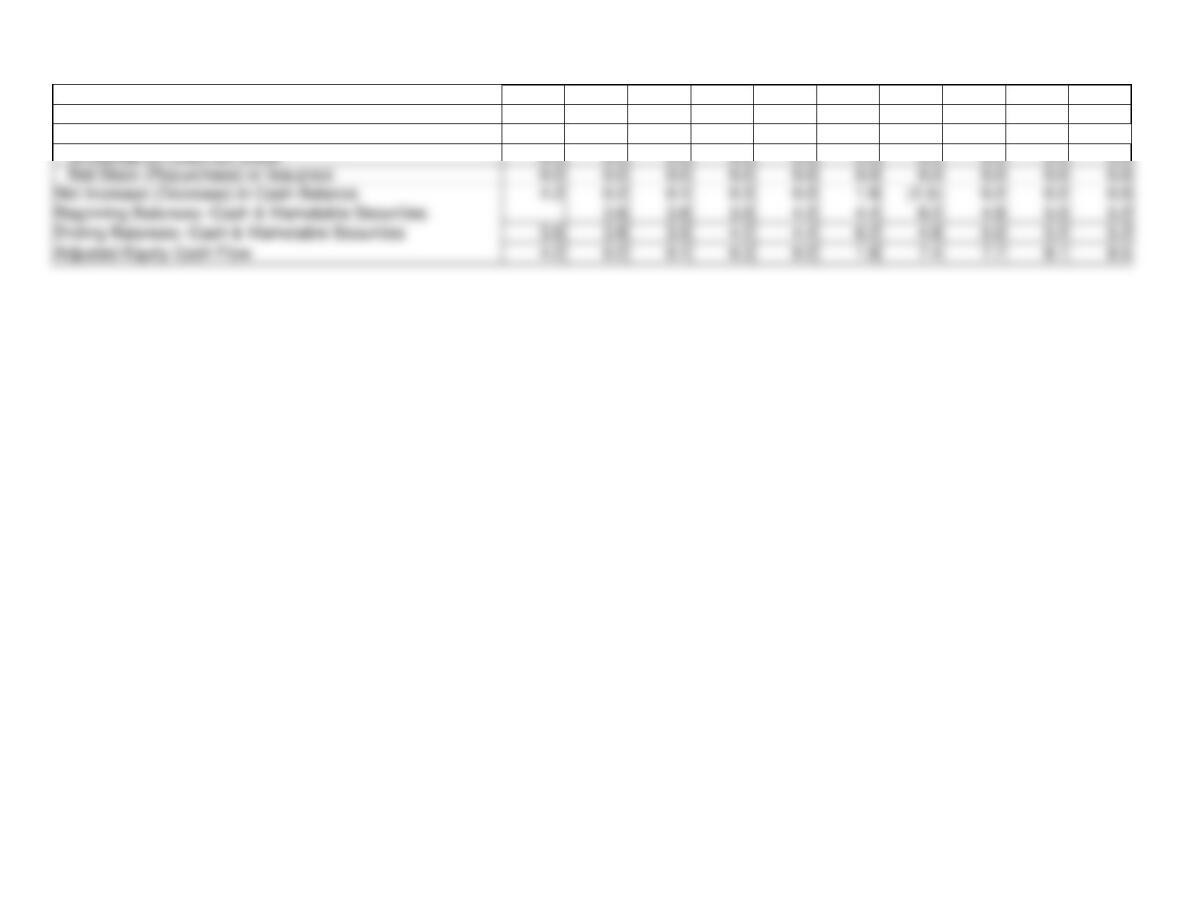

After-Tax Net Interest Expense (Income)

0.0

0.0

0.0

1.7

1.4

1.2

1.0

0.8

0.6

0.4

Net Debt (Repayments) or Issuance

0.0

0.0

0.0

(7.5)

(8.0)

(7.8)

(4.5)

(5.0)

(5.5)

(6.0)

Equity Cash Flow

4.2

0.2

0.1

0.3

0.2

1.8

(1.5)

0.2

0.2

0.0

Dividends on Common Stock

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Net Stock (Repurchase) or Issuance

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Net Increase (Decrease) in Cash Balance

4.2

0.2

0.1

0.3

0.2

1.8

(1.5)

0.2

0.2

0.0

Beginning Balances—Cash & Marketable Securities

3.6

3.8

3.9

4.2

4.4

6.2

4.8

5.0

5.2

Ending Balances—Cash & Marketable Securities

3.6

3.8

3.9

4.2

4.4

6.2

4.8

5.0

5.2

5.2