Accounting Information Systems, 10e 1

SOLUTIONS FOR CHAPTER 13

Each end-of-chapter question in the Solutions Manual is tagged to correspond with AACSB, AICPA

and CISA standards, allowing professors to more easily manage the task of reporting outcomes to these

professional and accrediting bodies. Please see the corresponding spreadsheet file for the tagging

information.

Discussion Questions

DQ 13-1 Refer to effectiveness goals A and B shown in the control matrix in Figure 13.11.

For each activity (accounts payable and cash disbursements), describe goals

other than the one discussed in the chapter.

ANS. Possible accounts payable effectiveness goals:

• (Contained in Figure 13.11.) Optimize cash discounts.

DQ 13-2 Explain why ambiguities and conflicts exist among operations process

(effectiveness) goals, and discuss potential ambiguities and conflicts relative to

the goals you described in DQ 13-1.

2 Solutions for Chapter 13

ANS. Conflicts exist because each organizational unit wants to do its best (or at least be

seen as doing its best). However, many (perhaps any) individual units cannot

possibly perform at their best because trade-offs must be made so that the

organization as a whole can do its best.

receiving and invoice verification processes may be sacrificed.

DQ 13-3 Without redrawing the figures, discuss how Figures 13.3, 13.4, and 13.6 would

change as a result of the following independent situations (be specific in

describing the changes):

a. Employing a voucher system that involved, among other things, establishing

vouchers payable that covered several vendor invoices.

ANS. In Figure 13.4, bubble 1.2, individual invoices would not be received from bubble

1.1 and the accounts payable master data would not be updated for individual

invoices. Rather, batches of invoices sorted by vendor identification code would

be accumulated between bubbles 1.1 and 1.2 and used by bubble 1.2 to update the

accounts payable master data.

Accounting Information Systems, 10e 3

ANS. In Figure 13.6, bubble 2.1 would be triggered on the fifth and the 25th of each

month. All discount dates reached between the last payment date and the current

payment date are considered available.

DQ 13-4 In terms of effectiveness and efficiency of operations, as well as of meeting the

generic information system control goals of validity, completeness, and accuracy,

what are the arguments for and against each of the following?

a. Sending a copy of the vendor invoice to the purchasing department for

approval of payment.

ANS. ● Purchasing personnel can review the invoice to ensure validity and accuracy

of the invoice (i.e., the items were ordered, price, terms, etc.).

ANS. ● Without the PO, the requisitioning department personnel cannot know what

was actually ordered on the PO versus what was requested on the purchase

requisition.

4 Solutions for Chapter 13

DQ 13-5 An electronic data interchange (EDI) system may present an organization with

opportunities and risks.

a. What opportunities might an EDI system present? Discuss your answer.

ANS. EDI facilitates the timely and efficient flow of data between trading partners. For

example, by enabling a just-in-time process, EDI can reduce the carrying costs of

ANS. Failure of the communications link threatens the ongoing operation of EDI. To

prevent this, the contract with the VAN should address the availability of the

communications link. An organization may contract with alternative VANs to be

used in the event of one VAN’s failure. Communication via the Internet might

DQ 13-6 In the physical implementation depicted in Figure 13.10, the payment order and

the RA were sent together through the banking system. We also described an

option of sending the RA directly to the vendor. Which is better? Discuss fully.

ANS. Each approach may have advantages. If the two items are sent together,

identification and validation of the payment may be more efficient. However, if

DQ 13-7 In the “Fraud and the Accounts Payable Function” section, we described a fraud

committed by Stanley and Phoebe and another by Veronica. For each fraud,

describe controls and technology that could reduce the risk of those frauds

occurring.

Accounting Information Systems, 10e 5

ANS. Controls and technology that might have reduced the risk of the fraud perpetrated

by Stanley and Phoebe include the following:

• Before opening the business account, the bank might have asked for

documentation regarding SRJ Enterprises.

Controls and technology that might have reduced the risk of the fraud perpetrated

by Veronica include the following:

• When the vendor invoice is entered, the invoice number should also be

entered, and the computer should be programmed to detect and preclude entry

of duplicate invoice numbers.

Short Problems

SP 13-1 ANS. We can discuss two categories of procedures and controls: business

process/application controls and entity-level/pervasive/IT general controls.

Business process/application controls:

6 Solutions for Chapter 13

Entity-level/pervasive/IT general controls:

SP 13-2 ANS. We can discuss two categories of procedures and controls: business

process/application controls and entity-level/pervasive/IT general controls.

Business process/application controls:

• The VAN or EDI translator should determine that the order was received from

a legitimate customer and not from an unauthorized source. A secure mailbox

Entity-level/pervasive/IT general controls:

• Physical and logical access controls should prevent unauthorized alteration of

the customer, sales order, and accounts receivable data—the data used to

validate the customer and perform the credit check.

• Program change controls must prevent unauthorized alteration of the program

that performs the validation and credit check.

Accounting Information Systems, 10e 7

SP 13-3 ANS. 1. B: Before invoices are accepted and recorded, Pownal Company must

validate the invoice by comparing it to the related purchase order and a

receiving report to ensure that the invoice is for items that were ordered and

received.

SP 13-4 ANS. 1. E: Samuel Company should compare incoming invoices to vendor master

data to determine that the invoices are from authorized vendors. The

invoices should also be compared to the related purchase order and

receiving report to reduce the possibility that the invoice is fraudulent.

2. D: Because the invoices are entered in batches, there is an opportunity for

personnel in the AP department to reconcile batch totals to ensure that all of

the invoices are recorded correctly.

8 Solutions for Chapter 13

SP 13-5 ANS.

Function

Risks

Controls and Technology

Finance

Nonoptimal cash balances (too

much, too little).

• Cash planning (from before or at the same time

that POs are issued). Requires that POs be

recorded so that we can plan for eventual

payments.

• Purchasing budgets.

Cash is lost.

• Electronic payments.

• Segregate controller and treasurer.

Inaccurate invoice (e.g.,

incorrect vendor, invoice

number, amount).

• Edit on input.

• Compare to vendor record, PO, and receiving

report.

Incomplete invoices.

Periodically examine open POs and open receiving

reports for invoices not received and/or not recorded

(tickler file).

Accounting Information Systems, 10e 9

Function

Risks

Controls and Technology

Discounts taken

(credit)

Inaccurate payment (e.g., wrong

vendor, wrong amount is paid).

• Electronic payments with digital signatures.

• Populate payment with vendor and invoice data.

• Match each payment with unpaid invoice.

(GR/IR).”

SP 13-6 ANS. While sometimes we think that the hand delivered signature is optimal, one has

to realize how easy it is to copy. No two signatures of an individual are identical. This can cause

a risk of error when verifying the signature. Because of the speed at which checks are processed,

it is nearly impossible to even do a cursory check for validity. From the other perspective,

Problems

Problems 1 and 2

Note: In the pages that follow, we provide solutions for problems 1 and 2 for both of the Case

Studies (Cases A and B) as applicable. Although the solution for each case study comprises

several pages, it is not necessarily comprehensive, nor does it represent the only acceptable

10 Solutions for Chapter 13

PureProducts Company (Accounts Payable and Cash Disbursements Processes) Solutions

(see the Note on pg. 9)

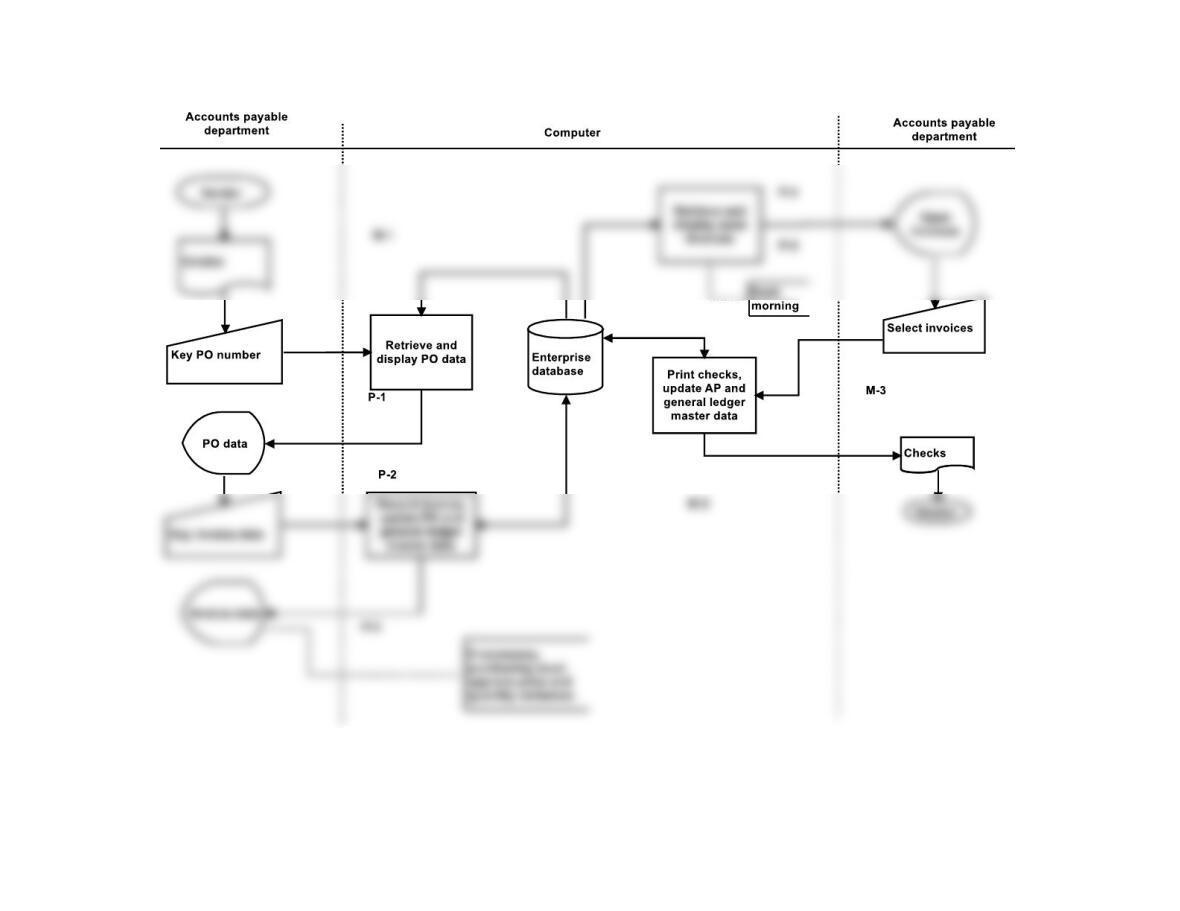

P 13-1 ANS. a. Table of Entities and Activities for PureProducts Company (Accounts Payable

and Cash Disbursements Processes)

Entities

Para

Activities

Accounts payable (AP)

2

1. Receive invoice from vendor.

2

2. Key PO number into computer.

Vendor

2

3

9. Read and display open invoices.

Accounts payable

3

10. Review open invoices.

3

11. Select invoices that should be paid.

Computer

3

12. Print checks, and update AP and general ledger master data.

Accounts payable

3

13. Mail check to vendor.

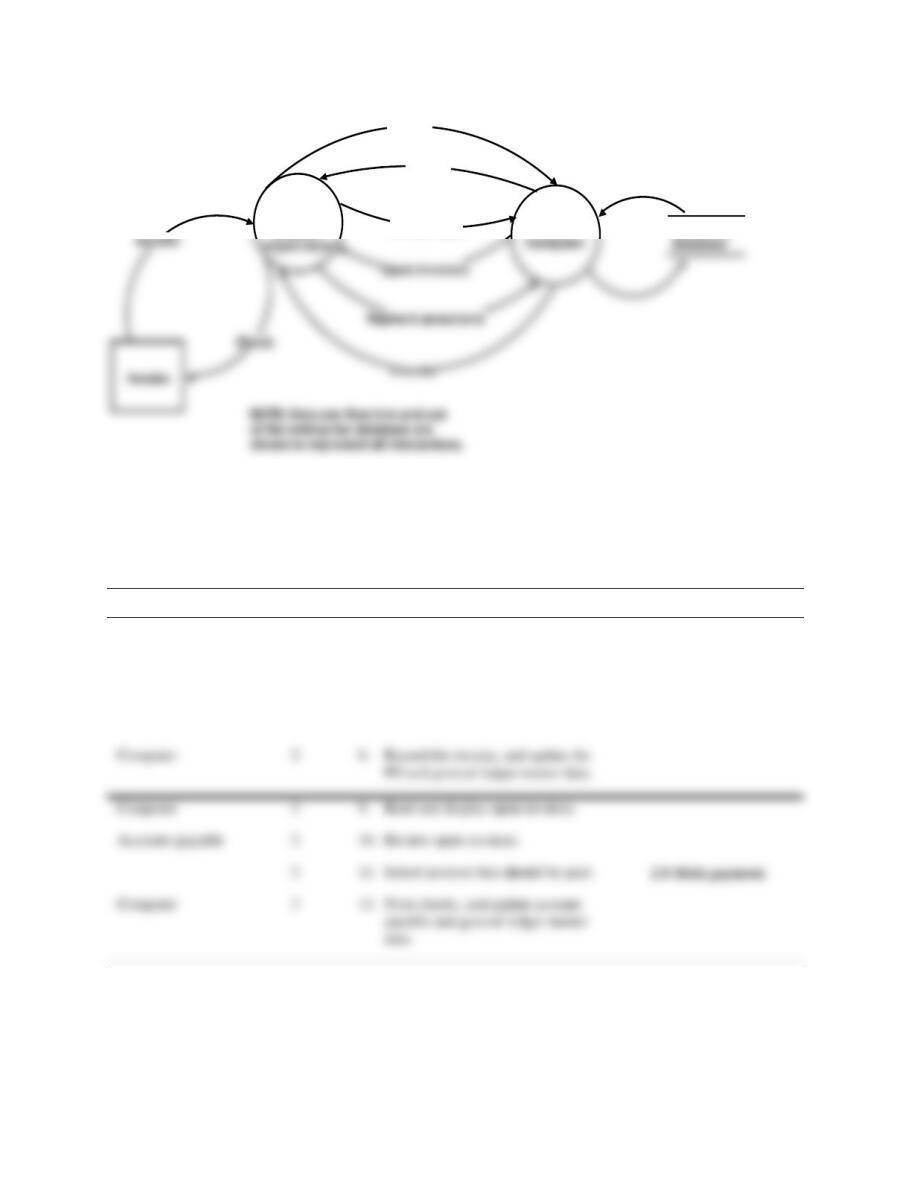

FIGURE SM-13.1 Problem 1, Part b Solution⎯Context Diagram for PureProducts Company

(Accounts Payable and Cash Disbursements Processes)

Computer

2

3. Display PO data.

AP

2

4. Key invoice data.

Computer

2

5. Match invoice with PO data.

2

6. If price or quantity variances exist, route to purchasing.

Purchasing

2

7. Approve variances.

Accounting Information Systems, 10e 11

1.0

Accounts

payable

2.0

Enterprise

PO data

PO

number

Invoice data

FIGURE SM-13.2 Problem 1, Part c Solution—Physical DFD for PureProducts Company

(Accounts Payable and Cash Disbursements Processes)

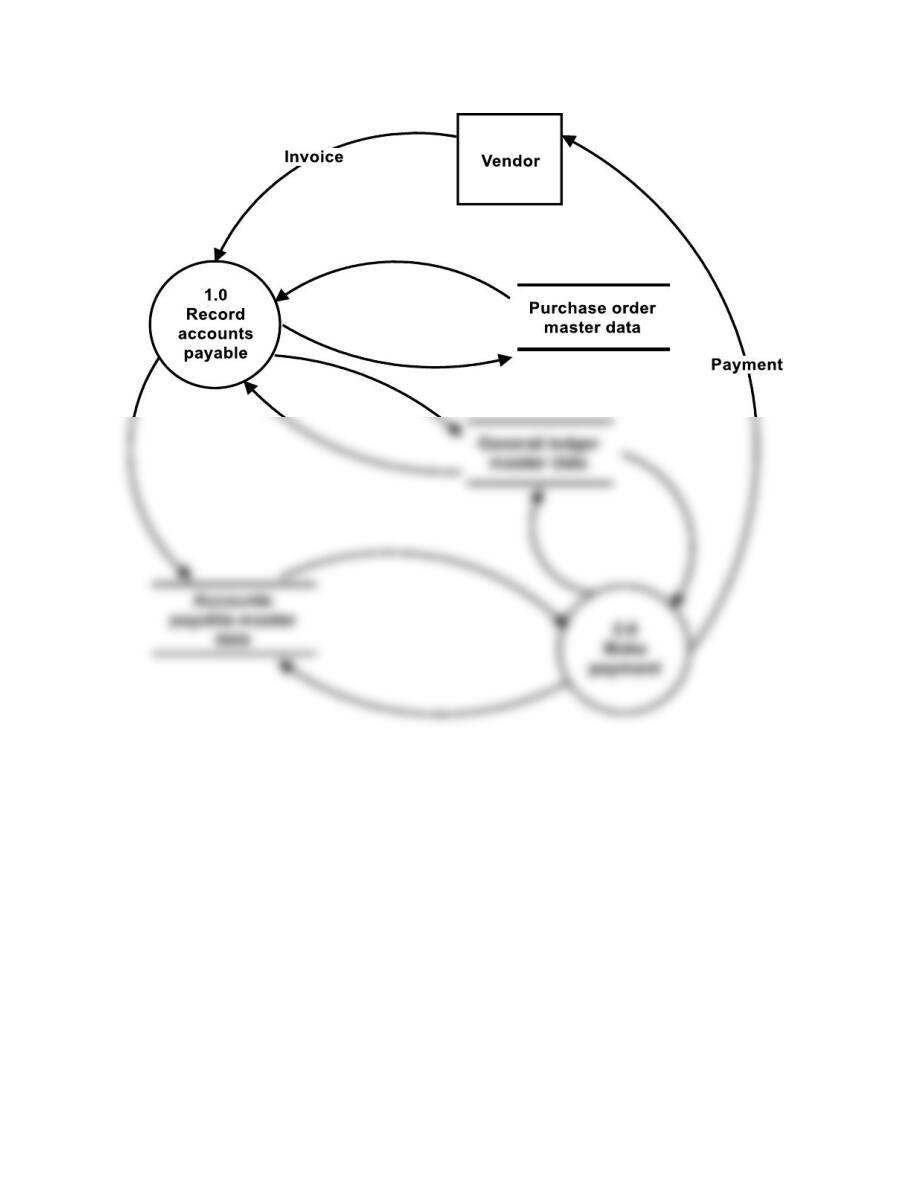

P 13-1 ANS. d. Table of Entities and Activities (Annotated) for PureProducts Company

(Accounts Payable and Cash Disbursements Processes)

Entities

Para

Activities

Process

Accounts payable (AP)

2

2. Key PO number into computer.

1.0 Record accounts

payable.

Computer

2

3. Display PO data.

AP

2

4. Key invoice data.

Computer

2

5. Match invoice with PO data.

Computer

3

9. Read and display open invoices.

3

10. Review open invoices.

3

11. Select invoices that should be paid.

12 Solutions for Chapter 13

FIGURE SM-13.3 Problem 1, Part e Solution—Logical DFD for PureProducts Company

(Accounts Payable and Cash Disbursements Processes)

Accounting Information Systems, 10e 13

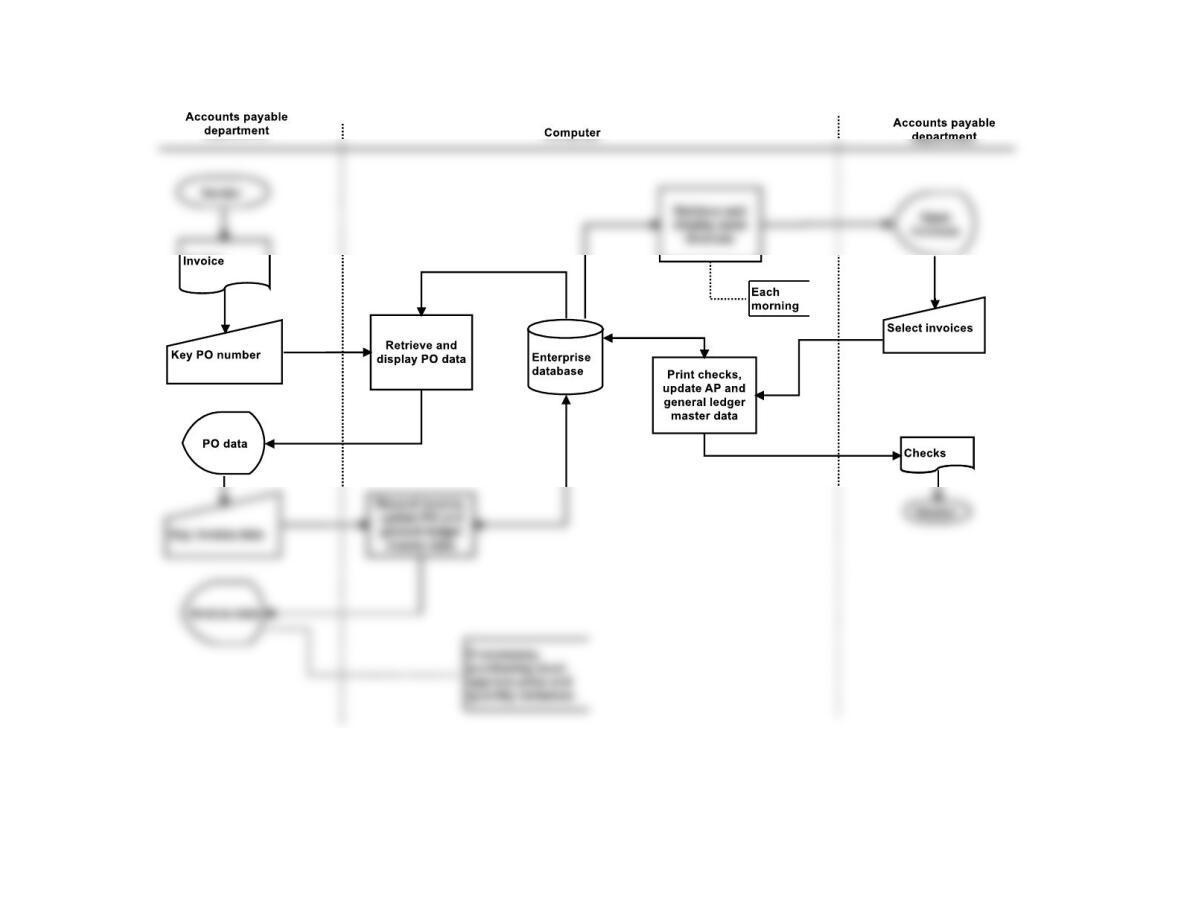

FIGURE SM-13.4 Problem 2, Part a Solution—Systems Flowchart for PureProducts Company

(Accounts Payable and Cash Disbursements Processes)

14 Solutions for Chapter 13

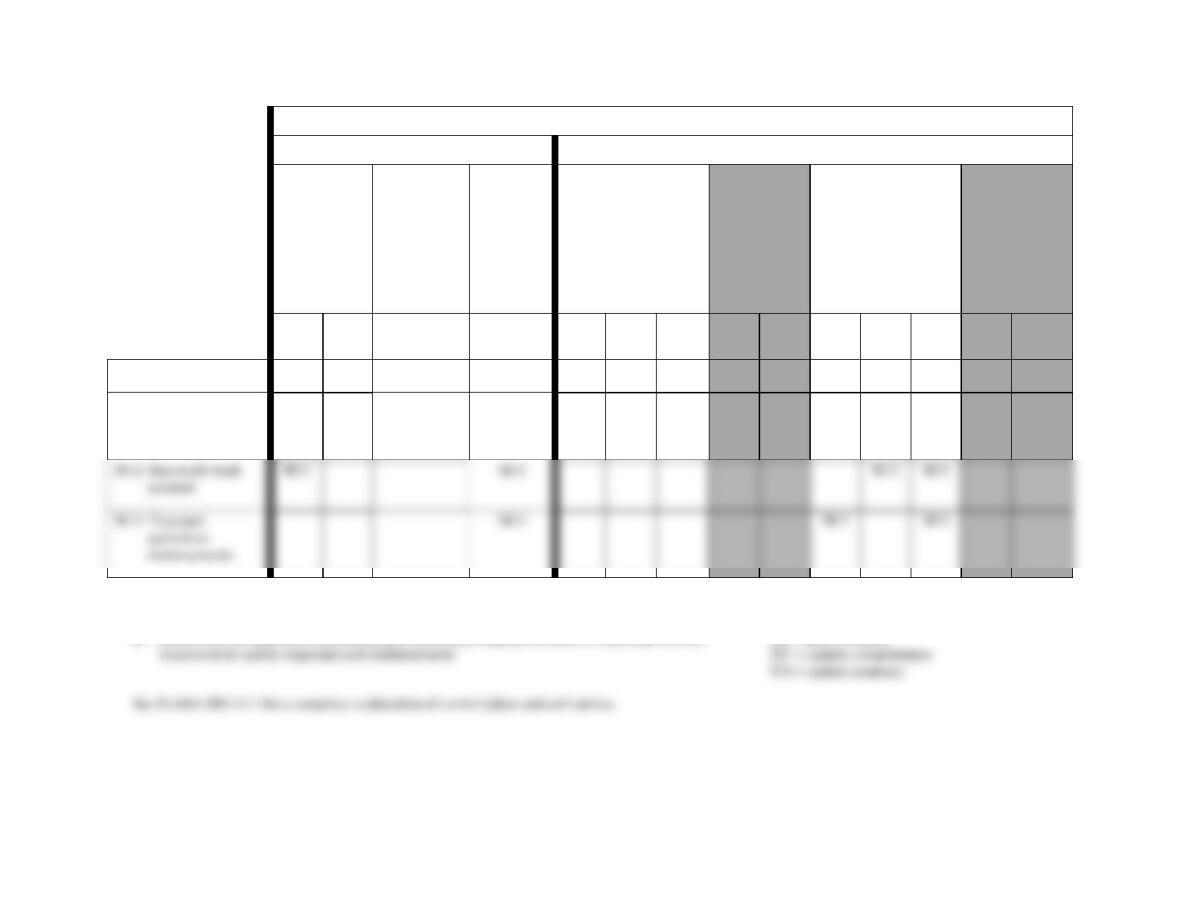

Control Goals of the PureProducts Company Accounts Payable and Cash Disbursements Business Processes

Control Goals of the Operations Process

Control Goals of the Information Process

Ensure

effectiveness

of operations

Ensure

efficient

employment

of resources

(people and

computers)

Ensure

security of

resources

(cash,

accounts

payable

master

data)

For vendor invoice

inputs, ensure:

For accounts

payable

master data,

ensure:

For payment

voucher inputs,

ensure:

For accounts

payable

master data,

ensure:

Recommended control

plans

A

B

IV

IC

IA

UC

UA

IV

IC

IA

UC

UA

Present controls

P-2: Match invoice to

PO and receiving

report

P-2

P-2

P-2

P-3: Authorize

variances

P-3

P-3

Accounting Information Systems, 10e 15

Control Goals of the PureProducts Company Accounts Payable and Cash Disbursements Business Processes

Control Goals of the Operations Process

Control Goals of the Information Process

Ensure

effectiveness

of operations

Ensure

efficient

employment

of resources

(people and

computers)

Ensure

security of

resources

(cash,

accounts

payable

master

data)

For vendor invoice

inputs, ensure:

For accounts

payable

master data,

ensure:

For payment

voucher inputs,

ensure:

For accounts

payable

master data,

ensure:

Recommended control

plans

A

B

IV

IC

IA

UC

UA

IV

IC

IA

UC

UA

Missing controls

M-1: Monitor open POs

and receiving

reports

M-1

M-1

Possible effectiveness goals include the following:

A – Optimize cash discounts

B – Ensure that the amount of cash maintained in demand deposit accounts is sufficient (but not

IV = input validity

IC = input completeness

IA = input accuracy

FIGURE SM-13.5 Problem 2, Part b Solution (Partial)—Control Matrix for PureProducts Company

(Accounts Payable and Cash Disbursements Processes)

M-3: Treasurer

authorizes

disbursements

16 Solutions for Chapter 13

Exhibit SM-13.1 Problem 2, Part b Solution (Partial)—explanation of cell entries for

control Matrix in Figure SM-13.5

Note: Vendor invoice and payment voucher inputs result in immediate updates to accounts

payable master data. Therefore, we do not show entries for UC or UA.

P-1: Independent validation of vendor invoice.

Ensure security of resources, vendor invoice input validity: The accounts payable

P-2: Match invoice with PO and receiving report.

Effectiveness goal A, vendor invoice input validity, and input accuracy: The

P-3: Authorize variances.

Vendor invoice input validity and input accuracy: Purchasing reviews the input

quantities and prices to determine that they are valid and accurate (within limits

prescribed by management).

Payment voucher input validity: The open invoice record is used to authorize

execution of a payment.

M-1: Monitor open POs and receiving reports.

Effectiveness goal A and vendor invoice input completeness: The database of open

M-2: Reconcile bank account.

Effectiveness goal A, security of resources, payment voucher input completeness,

M-3: Treasurer authorizes disbursements.

Security of resources, payment voucher input validity, and input accuracy:

Someone other than accounts payable, such as the treasurer, should authorize the

disbursements by comparing the disbursement to the invoice, PO, and receiving

report so that only authorized disbursements are made (security, validity), and that

all disbursements are accurate (accuracy).

• When there are programmed edit checks, manual comparisons, and

reconciliation of batch totals, we might find procedures for rejected inputs.

• Where paper documents are employed, we might find document design,

written approvals, and turnaround documents.

18 Solutions for Chapter 13

FIGURE SM-13.6 Problem 2, Part c Solution—Annotated Systems Flowchart for PureProducts Company

(Accounts Payable and Cash Disbursements Processes)

Accounting Information Systems, 10e 19

Internet Payment Platform (Accounts Payable and Cash Disbursements Processes)

Solutions (see the Note on pg. 9)

P 13-1 ANS. a. Table of Entities and Activities for Internet Payment Platform (Accounts

Payable and Cash Disbursements Processes)

Entities

Para

Activities

Supplier

2

1. Log on to IPP.

2

2. Flip PO to invoice.

BEPMIS

2

8. Post invoices to accounts payable database.

3

9. Perform three-way match of invoice, PO, receipt.

3

10. Extract and format invoice changes.

3

11. Send invoice changes to enterprise adapter.

Enterprise adapter

3

12. Convert changes from IDMS to XML.

3

13. Encrypt invoice changes.

3

14. Transmit invoice changes to IPP server.

IPP server

3

15. Post invoice changes to appreciating database.

Accounts payable accountant

4

16. Trigger payment process.

BEPMIS

4

17. Read and display invoices due for payment (assumed).

Accounts payable accountant

4

18. Review invoices.

4

19. Select invoices for payment.

BEPMIS

4

20. Extract and format payments.

4

21. Generate PIF file.

4

22. Transmit PIF to enterprise adapter.

4

24. E-mail CO, DO, and Boston Fed with PIF totals.

Enterprise adapter

4

25. Convert PIF from IDMS to XML.

IPP server

2

3. Post invoice to appreciating database.

2

4. Encrypt invoices.

2

5. Send invoices to the enterprise adapter.

Enterprise adapter

2

6. Translate invoices into XML.

2

7. Send translated invoices to BEPMIS (assumed).

20 Solutions for Chapter 13

Entities

Para

Activities

4

27. Transmit PIF to IPP server.

Disbursing officer (DO)

4

31. Log on to IPP.

4

32. Approve PIF.

IPP server

5

33. Generate ACH-formatted file from PIF.

5

34. Encrypt ACH-formatted file.

5

35. Send ACH-formatted file to Boston Fed.

5

37. E-mail supplier that a payment is coming.

Boston Fed

5

38. Transfer ACH file to FedACH system.

FedACH system

5

39. Settle payment (debit Treasury’s account and credit supplier’s

bank’s account).

5

40. Notify supplier’s bank of credits.

5

IPP server

4

28. Post PIF to appreciating database.

4

29. Log on to IPP.

4