SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Apr. 1

Equipment

56,000

Notes Payable

56,000

Purchased equipment by issuing an 7-year,

13% note.

Dec. 31

Interest Expense ($56,000 × 0.13 × 9/12)

Interest Payable

2017

Apr. 1

Interest Expense ($56,000 × 0.13 × 3/12)

Interest Payable

Notes Payable

Cash

15,280

Dec. 31

Interest Expense ($48,000 × 0.13 × 9/12)

Interest Payable

Requirement 2

Dec. 31, 2017

Interest Payable

Notes Payable

Total liabilities

E12-18 Preparing an amortization schedule and recording mortgages payable entries

Learning Objective 1

3. Interest Expense $4,333.33

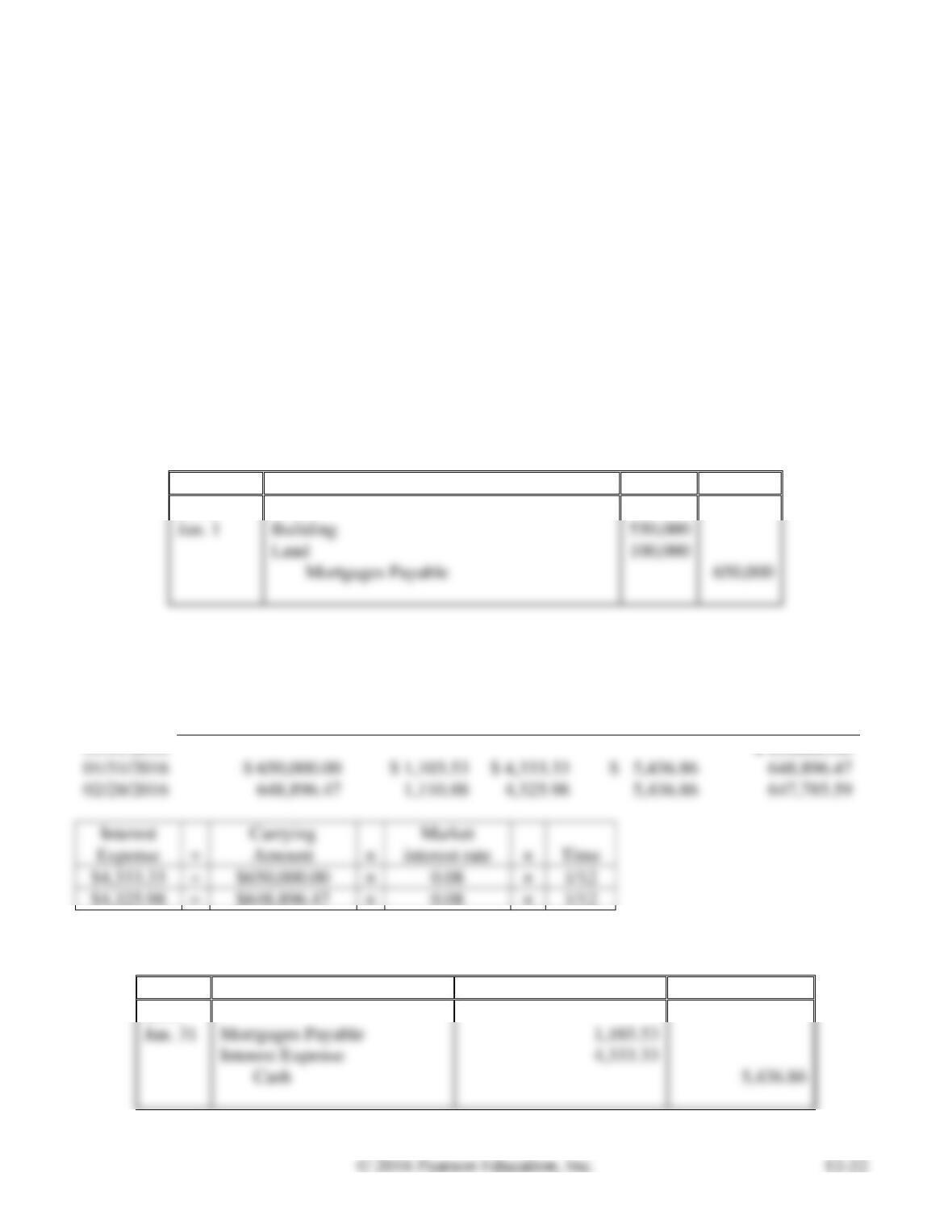

Keel Company purchased a building and land with a fair market value of $650,000 (building, $550,000,

and land, $100,000) on January 1, 2016. Keel signed a 20-year, 8% mortgage payable. Keel will make

monthly payments of $5,436.86.

Requirements

1. Journalize the mortgage payable issuance on January 1, 2016 (explanations are not required).

2. Prepare an amortization schedule for the first two payments.

3. Journalize the first payment on January 31, 2016 (round to two decimal places).

4. Journalize the second payment on February 29, 2016 (round to two decimal places).

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 1

Building

550,000

Land

100,000

Requirement 2

Beginning Balance

Principal

Payment

Interest

Expense

Total

Payment

Ending Balance

01/01/2016

$ 650,000.00

01/31/2016

02/28/2016

=

×

=

×

=

×

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 31

Mortgages Payable

1,103.53

Interest Expense

4,333.33

E12-18, cont.

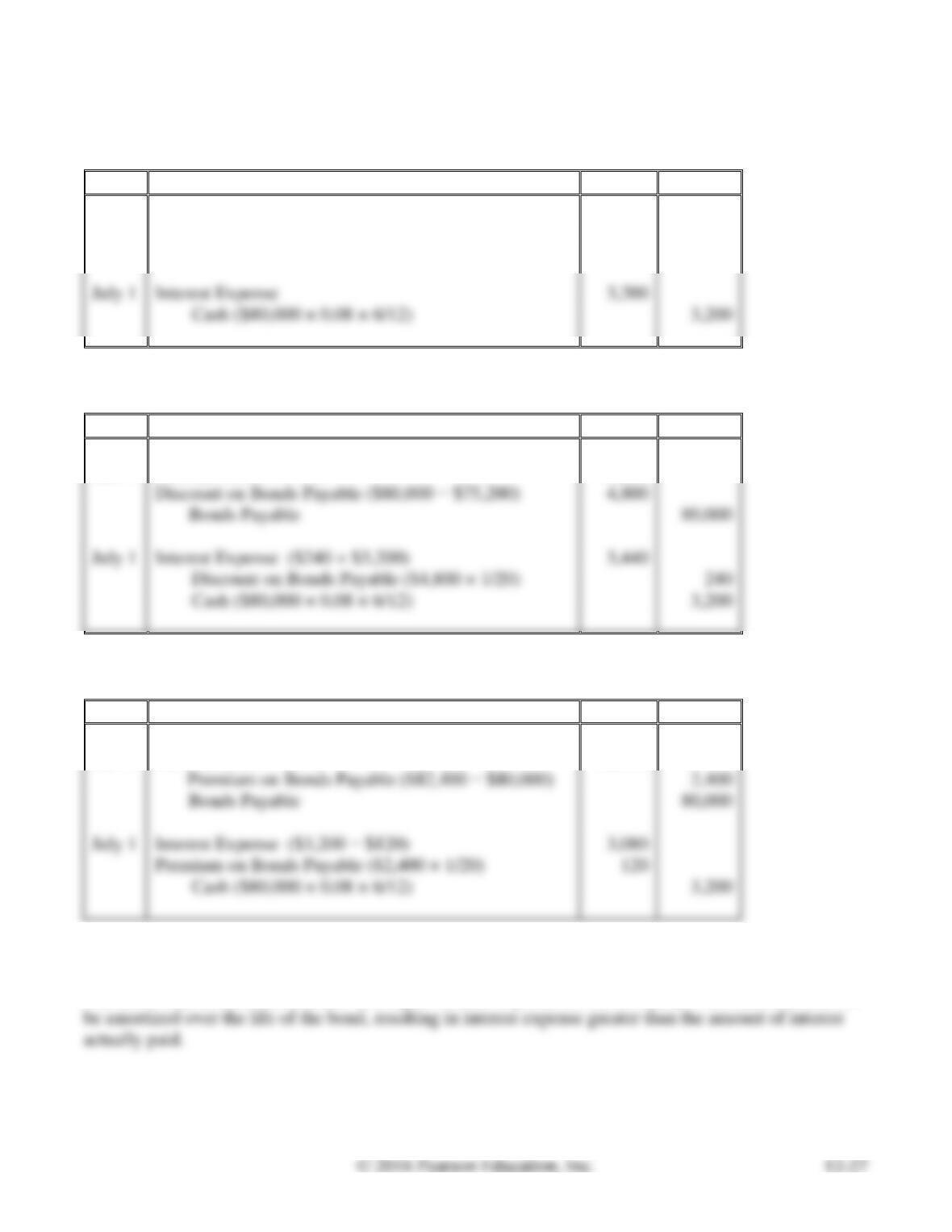

Requirement 4

Date

Accounts and Explanation

Debit

Credit

2016

Feb. 29

Mortgages Payable

1,110.88

Interest Expense

4,325.98

E12-19 Analyzing alternative plans to raise money

Learning Objective 2

AF Electronics is considering two plans for raising $3,000,000 to expand operations. Plan A is to issue

7% bonds payable, and plan B is to issue 100,000 shares of common stock. Before any new financing,

AF has net income of $250,000 and 200,000 shares of common stock outstanding. Management believes

the company can use the new funds to earn additional income of $500,000 before interest and taxes. The

income tax rate is 30%. Analyze the AF Electronics situation to determine which plan will result in

higher earnings per share. Use Exhibit 12-6 as a guide.

SOLUTION

Plan A:

Issue $3,000,000 of 7%

Bond Payable

Plan B:

Issue $3,000,000 of

Common Stock

E12-20 Determining bond prices and interest expense

Learning Objectives 2, 3

2. Market price $404,200

Nooks is planning to issue $470,000 of 5%, 10-year bonds payable to borrow for a major expansion. The

owner, Simon Nooks, asks your advice on some related matters.

Requirements

1. Answer the following questions:

a. At what type of bond price will Nooks have total interest expense equal to the cash interest

payments?

b. Under which type of bond price will Nooks’ total interest expense be greater than the cash

interest payments?

c. If the market interest rate is 7%, what type of bond price can Nooks expect for the bonds?

2. Compute the price of the bonds if the bonds are issued at 86.

3. How much will Nooks pay in interest each year? How much will Nooks’ interest expense be for the

first year?

SOLUTION

Requirement 1

a.

Face Value

Discount

c.

Discount

Requirement 2

Face value

×

Issue price

Market price or

Cash received

×

E12-21 Journalizing bond issuance and interest payments

Learning Objective 3

1. June 30 Bonds Payable CR $60,000

On June 30, Paulson Company issues 6%, 10-year bonds payable with a face value of $60,000. The

bonds are issued at face value and pay interest on June 30 and December 31.

Requirements

1. Journalize the issuance of the bonds on June 30.

2. Journalize the semiannual interest payment on December 31.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

June 30

Cash

Date

Debit

Credit

E12-22 Journalizing bond issuance and interest payments

Learning Objective 3

1. June 30 Discount DR $7,200

On June 30, Danver Limited issues 5%, 20-year bonds payable with a face value of $120,000. The

bonds are issued at 94 and pay interest on June 30 and December 31.

Requirements

1. Journalize the issuance of the bonds on June 30.

2. Journalize the semiannual interest payment and amortization of bond discount on December 31.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Date

Debit

Credit

E12-23 Journalizing bond transactions

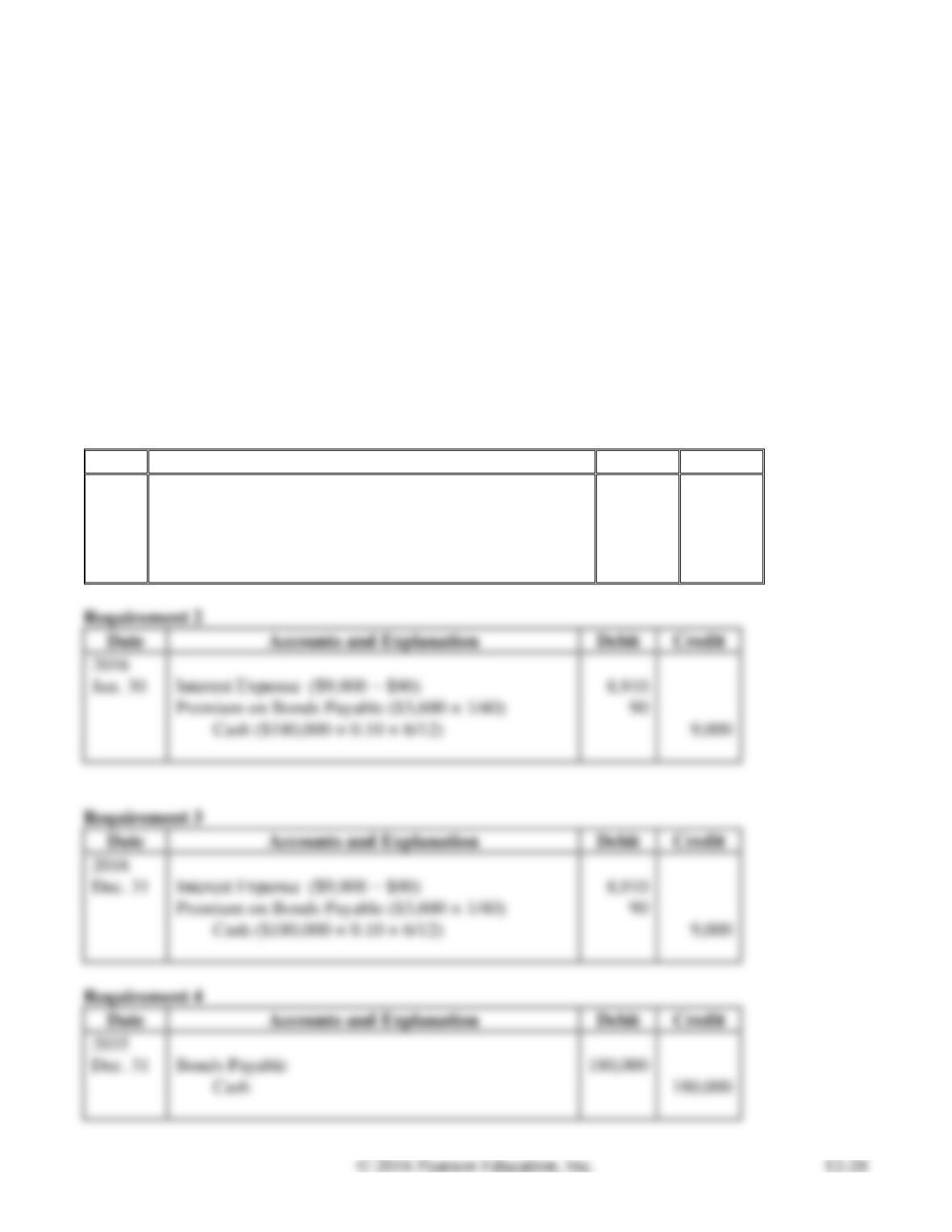

Learning Objective 3

2. Interest Expense DR $3,440

Franklin issued $80,000 of 10-year, 8% bonds payable on January 1, 2016. Franklin pays interest each

January 1 and July 1 and amortizes discount or premium by the straight-line amortization method. The

company can issue its bonds payable under various conditions.

Requirements

1. Journalize Franklin’s issuance of the bonds and first semiannual interest payment assuming the

bonds were issued at face value. Explanations are not required.

2. Journalize Franklin’s issuance of the bonds and first semiannual interest payment assuming the

bonds were issued at 94. Explanations are not required.

3. Journalize Franklin’s issuance of the bonds and first semiannual interest payment assuming the

bonds were issued at 103. Explanations are not required.

4. Which bond price results in the most interest expense for Franklin? Explain in detail.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 1

Cash

80,000

Bonds Payable

80,000

July 1

Interest Expense

Cash ($80,000 × 0.08 × 6/12)

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 1

Cash ($80,000 × 0.94)

75,200

Discount on Bonds Payable ($80,000 − $75,200)

Bonds Payable

80,000

July 1

Interest Expense ($240 + $3,200)

Discount on Bonds Payable ($4,800 × 1/20)

Cash ($80,000 × 0.08 × 6/12)

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 1

Cash ($80,000 × 1.03)

82,400

Premium on Bonds Payable ($82,400 − $80,000)

Bonds Payable

80,000

July 1

Interest Expense ($3,200 − $120)

Premium on Bonds Payable ($2,400 × 1/20)

Cash ($80,000 × 0.08 × 6/12)

Requirement 4

The bond issue at a discount results in a higher interest expense for the company. The discount needs to

E12-24 Journalizing bond issuance and interest payments

Learning Objectives 3, 4

1. Premium CR $3,600

On January 1, 2016, Dave Unlimited issues 10%, 20-year bonds payable with a face value of $180,000.

The bonds are issued at 102 and pay interest on June 30 and December 31.

Requirements

1. Journalize the issuance of the bonds on January 1, 2016.

2. Journalize the semiannual interest payment and amortization of bond premium on June 30, 2016.

3. Journalize the semiannual interest payment and amortization of bond premium on December 31,

2016.

4. Journalize the retirement of the bond at maturity. (Give the date.)

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 1

Cash ($180,000 × 1.02)

183,600

Premium on Bonds Payable ($183,600 − $180,000)

3,600

Bonds Payable

180,000

2016

Jun. 30

Premium on Bonds Payable ($3,600 × 1/40)

Cash ($180,000 × 0.10 × 6/12)

9,000

Credit

2016

Dec. 31

Premium on Bonds Payable ($3,600 × 1/40)

Cash ($180,000 × 0.10 × 6/12)

9,000

Credit

2035

Dec. 31

Bonds Payable

180,000

E12-25 Retiring bonds payable before maturity

Learning Objective 4

2. Cash CR $696,900

Parkview Magazine issued $690,000 of 15-year, 5% callable bonds payable on July 31, 2016, at 95. On

July 31, 2019, Parkview called the bonds at 101. Assume annual interest payments.

Requirements

1. Without making journal entries, compute the carrying amount of the bonds payable at July 31, 2019.

2. Assume all amortization has been recorded properly. Journalize the retirement of the bonds on July

31, 2019. No explanation is required.

SOLUTION

Requirement 1

Face value $690,000 – Carrying Value $655,500 ($690,000 × .95) = Discount $34,500

Discount $34,500 / 15 years = $2,300 amortized per year

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2019

July 31

Bonds Payable

690,000

Loss on Retirement of Bonds Payable

34,500

E12-26 Reporting current and long-term liabilities

Learning Objectives 2, 3, 5

Optical Dispensary borrowed $330,000 on January 2, 2016, by issuing a 15% serial bond payable that

must be paid in three equal annual installments plus interest for the year. The first payment of principal

and interest comes due January 2, 2017.Complete the missing information. Assume the bonds are issued

at face value.

SOLUTION

Requirement 1

December 31

2016

2017

2018

Current Liabilities:

Interest Payable

Long-term Liabilities:

Bonds Payable

Balance

Rate

Time

Interest Owed

2016

$330,000

×

0.15

×

12/12

=

2017

$220,000

×

0.15

×

12/12

=

2018

$110,000

×

0.15

×

12/12

=

E12-27 Reporting liabilities

Learning Objectives 2, 3, 5

Total Liabilities $358,000

At December 31, MediAssist Precision Instruments owes $51,000 on Accounts Payable, Salaries

Payable of $12,000, and Income Tax Payable of $10,000. MediAssist also has $280,000 of Bonds

Payable that were issued at face value that require payment of a $50,000 installment next year and the

remainder in later years. The bonds payable require an annual interest payment of $5,000, and

MediAssist still owes this interest for the current year. Report MediAssist’s liabilities on its classified

balance sheet.

SOLUTION

MEDIASSIST PRECISION INSTRUMENTS

Balance Sheet (Partial)

December 31

50,000

12,000

10,000

Total Liabilities

E12-28 Computing the debt to equity ratio

Learning Objective 6

Burkhart Corporation has the following data as of December 31, 2016:

Compute the debt to equity ratio at December 31, 2016.

SOLUTION

Assets:

Liabilities:

E12A-29 Determining the present value of bonds payable

Learning Objective 7

Appendix 12A

2. Present Value $71,329

Interest rates determine the present value of future amounts. (Round all numbers to the nearest whole

dollar.)

Requirements

1. Determine the present value of six-year bonds payable with face value of $84,000 and stated interest

rate of 12%, paid semiannually. The market rate of interest is 12% at issuance.

2. Same bonds payable as in Requirement 1, but the market interest rate is 16%.

3. Same bonds payable as in Requirement 1, but the market interest rate is 10%.

SOLUTION

Requirement 1

Present value = $84,000 because the stated rate of interest equals the market rate of interest.

E12A-29, cont.

Requirement 3

Present value of principal:

Present value

=

Future value

×

=

Present value of stated interest:

Present value

=

×

=

=

Present value

=

=

=

PV factor for

i = 5% (10% / 2),

E12B-30 Journalizing bond transactions using the effective-interest amortization method

Learning Objective 8

Appendix 12B

2. Interest Expense DR $6,208

Journalize issuance of the bond and the first semiannual interest payment under each of the following

three assumptions. The company amortizes bond premium and discount by the effective-interest

amortization method. Explanations are not required.

1. Ten-year bonds payable with face value of $86,000 and stated interest rate of 14%, paid

semiannually. The market rate of interest is 14% at issuance. The present value of the bonds at

issuance is $86,000.

2. Same bonds payable as in assumption 1, but the market interest rate is 16%. The present value of the

bonds at issuance is $77,594.

3. Same bonds payable as in assumption 1, but the market interest rate is 8%. The present value of the

bonds at issuance is $121,028.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

E12B-30, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Cash

77,594

Discount on Bonds Payable ($86,000 − $77,594)

Interest Expense

Discount on Bonds Payable

Cash

Cash Paid

Interest

Expense

Discount

Amortized

Carrying

Amount

E12B-30, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Cash

121,028

Premium on Bonds Payable ($121,028 − $86,000)

35,028

Bonds Payable

86,000

Interest Expense

Premium on Bonds Payable

Cash

Cash Paid

Interest

Expense

Premium

Amortized

Carrying

Amount

Beginning

$ 121,028

1st pmt

$ 6,020

$ 4,841

$ 1,179

Interest

=

×

=

×

119,849

Problems (Group A)

P12-31A Journalizing liability transactions and reporting them on the balance sheet

Learning Objectives 1, 5

1. Mar. 1, 2017, Mortgage Payable DR $4,710

2. Total Liabilities $345,998

The following transactions of Smith Pharmacies occurred during 2016 and 2017:

Requirements

1. Journalize the transactions in the Smith Pharmacies general journal. Round all answers to the nearest

dollar. Explanations are not required.

2. Prepare the liabilities section of the balance sheet for Smith Pharmacies on March 1, 2017 after all

the journal entries are recorded.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Mar. 1

Cash

240,000

Notes Payable

240,000

Dec. 1

Cash

150,000

Mortgages Payable

150,000

Dec. 31

Interest Expense ($240,000 × 0.07 × 10/12)

Interest Payable

Dec. 31

Interest Expense ($150,000 × 0.11 × 1/12)

1,375

Interest Payable

1,375

2017

Interest Payable

1,375

Jan. 1

Mortgages Payable ($6,000 − $1,375)

4,625

Cash

6,000

Feb. 1

Interest Expense

1,333

Mortgages Payable ($6,000 − $1,333)

4,667

Cash

6,000

Mar. 1

Interest Expense

1,290

Mortgages Payable ($6,000 − $1,290)

4,710

Cash

6,000

Mar. 1

Interest Payable

Interest Expense($240,000 × 0.07 × 2/12)

2,800

Notes Payable

Cash

P12-31A

Requirement 1, cont.

Sawyer Bank Interest Calculations

Beginning

Balance

Principal

Payment

Interest

Expense

Total

Payment

Ending

Balance

12/01/2016

$ 150,000

01/01/2017

$ 150,000

$ 4,625

1,375

$ 6,000

145,375

02/01/2017

145,375

1,333

140,708

03/01/2017

140,708

1,290

135,998

Interest

Expense

=

×

Market

=

×

=

×

=

×

Requirement 2

SMITH PHARMACIES

Balance Sheet (Partial)

March 1, 2017