P12-31A

Requirement 2, cont.

Beginning

Balance

Principal

Payment

Interest

Expense

Total

Payment

Ending

Balance

12/01/2016

$ 150,000

01/01/2017

$ 150,000

$ 4,625

1,375

$ 6,000

145,375

02/01/2017

145,375

4,667

1,333

6,000

140,708

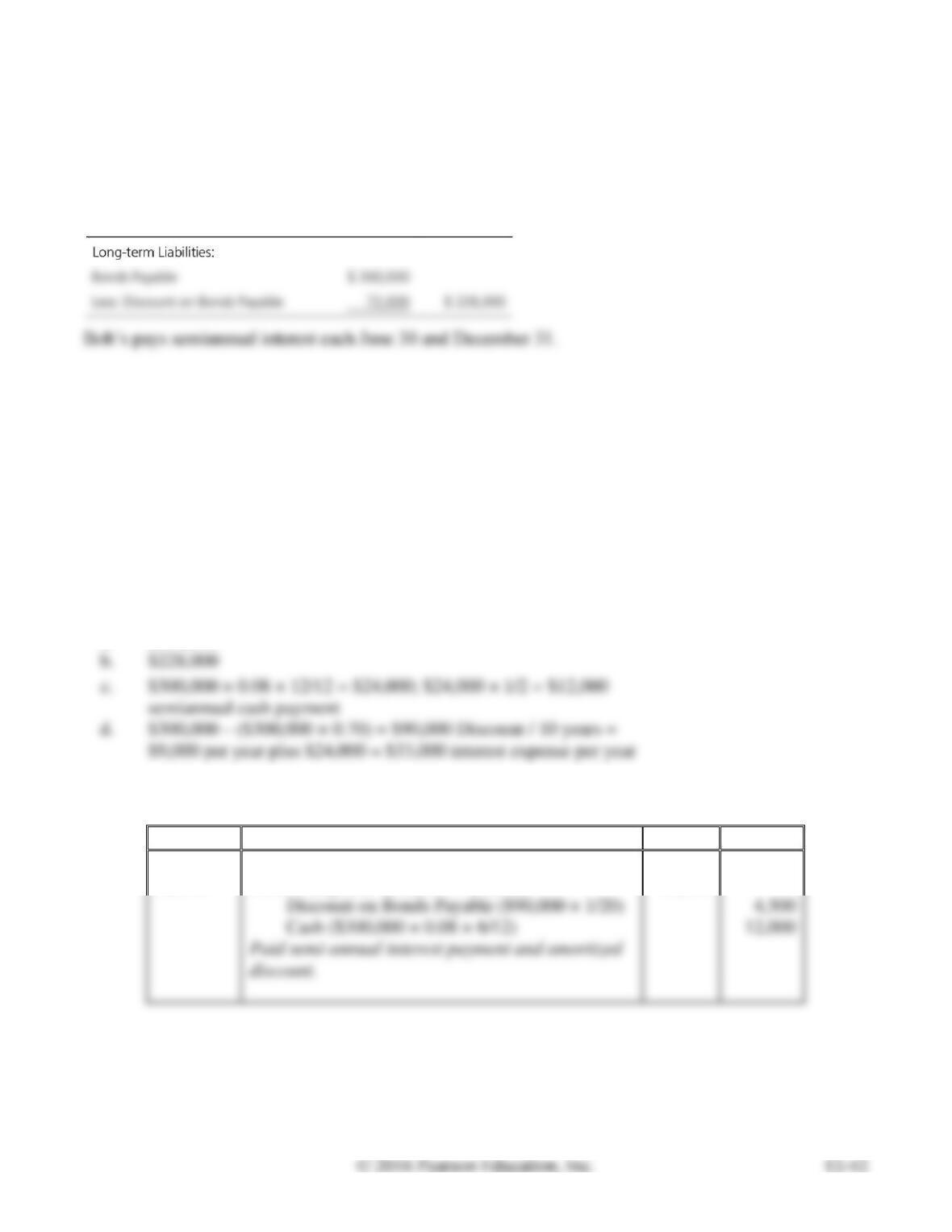

P12-32A Analyzing, journalizing, and reporting bond transactions

Learning Objectives 2, 3

2. Discount CR $4,500

Bob’s Hamburgers issued 8%, 10-year bonds payable at 70 on December 31, 2016. At December 31,

2018, Billy reported the bonds payable as follows:

Requirements

1. Answer the following questions about Bob’s bonds payable:

a. What is the maturity value of the bonds?

b. What is the carrying amount of the bonds at December 31, 2018?

c. What is the semiannual cash interest payment on the bonds?

d. How much interest expense should the company record each year?

2. Record the June 30, 2018, semiannual interest payment and amortization of discount.

SOLUTION

Requirement 1

a.

$300,000

$228,000

semiannual cash payment

$9,000 per year plus $24,000 = $33,000 interest expense per year

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2018

Jun. 30

Interest Expense ($12,000 + $4,500)

16,500

P12-33A Analyzing and journalizing bond transactions

Learning Objectives 2, 3, 4

3. June 30, 2016, Interest Expense DR $16,400

Requirements

1. If the market interest rate is 6% when TCU issues its bonds, will the bonds be priced at face value, at

a premium, or at a discount? Explain.

2. If the market interest rate is 9% when TCU issues its bonds, will the bonds be priced at face value, at

a premium, or at a discount? Explain.

3. The issue price of the bonds is 96. Journalize the following bond transactions:

a. Issuance of the bonds on January 1, 2016.

SOLUTION

Requirement 1

Requirement 2

The 8% bonds will be issued at a discount if the market interest rate is 9%. They are unattractive in this

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 1

Cash ($400,000 × 0.96)

384,000

Discount on Bonds Payable ($400,000 − $384,000)

16,000

Bonds Payable

400,000

Jun. 30

Interest Expense ($16,000 + $400)

16,400

Dec. 31

Interest Expense ($16,000 + $400)

16,400

2035

Dec. 31

Bonds Payable

400,000

400,000

P12-34A Analyzing and journalizing bond transactions

Learning Objectives 2, 3, 4

June 30, 2016, Interest Expense DR $20,400

On January 1, 2016, Agricultural Credit Union (ACU) issued 7%, 20-year bonds payable with face value

of $600,000. These bonds pay interest on June 30 and December 31. The issue price of the bonds is 104.

Journalize the following bond transactions:

a. Issuance of the bonds on January 1, 2016.

b. Payment of interest and amortization on June 30, 2016.

c. Payment of interest and amortization on December 31, 2016.

d. Retirement of the bond at maturity on December 31, 2035.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 1

Cash ($600,000 × 1.04)

624,000

Premium on Bonds Payable ($624,000 −

$600,000)

24,000

Jun. 30

Interest Expense ($21,000 − $600)

Premium on Bonds Payable ($24,000 × 1/40)

Cash ($600,000 × 0.07 × 6/12)

21,000

Dec. 31

Interest Expense ($21,000 − $600)

Premium on Bonds Payable ($24,000 × 1/40)

Cash ($600,000 × 0.07 × 6/12)

21,000

2035

Dec. 31

Bonds Payable

600,000

Cash

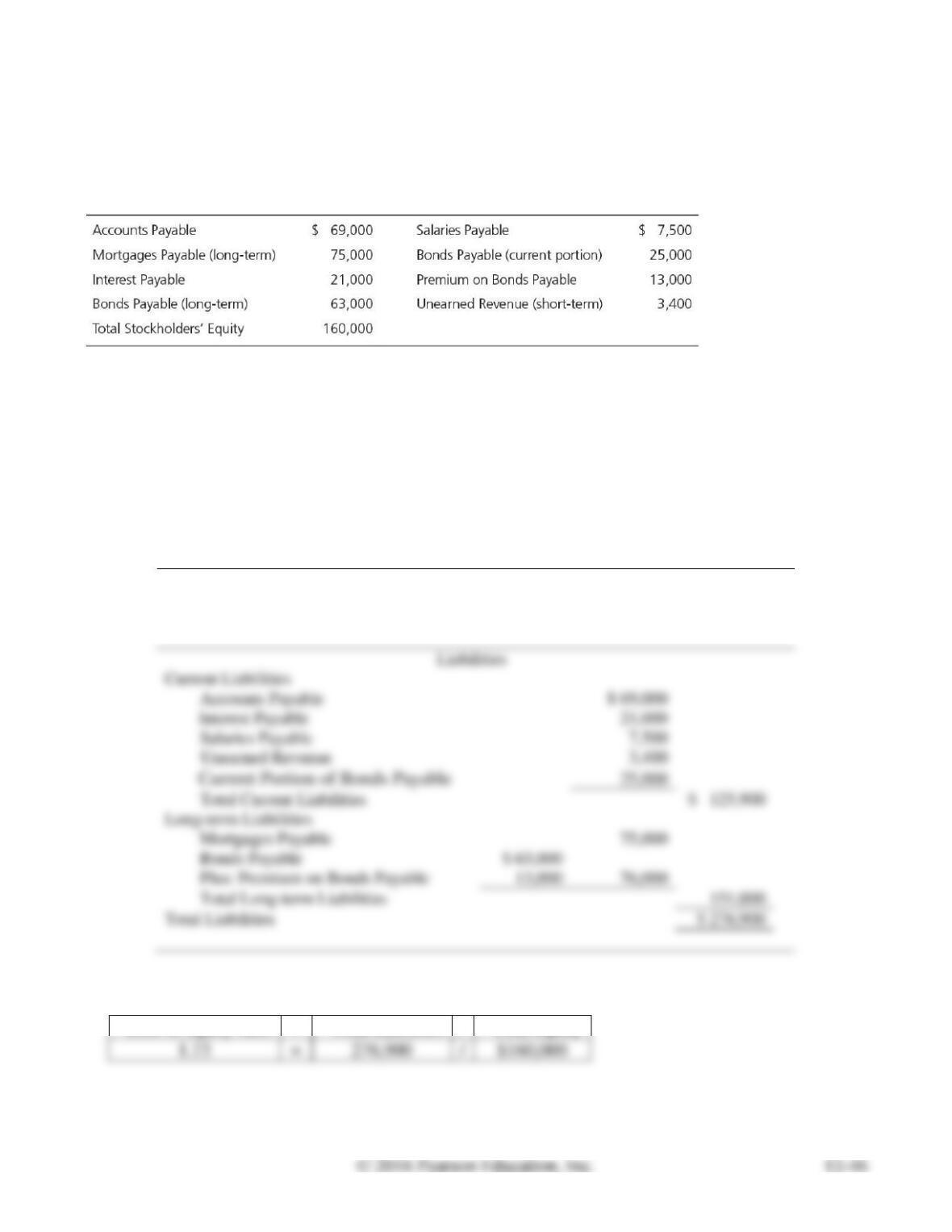

P12-35A Reporting liabilities on the balance sheet and computing debt to equity ratio

Learning Objectives 5, 6

1. Total Liabilities $276,900

The accounting records of Router Wireless include the following as of December 31, 2016:

Requirements

1. Report these liabilities on the Router Wireless balance sheet, including headings and totals for

current liabilities and long-term liabilities.

2. Compute Router Wireless’s debt to equity ratio at December 31, 2016.

SOLUTION

Requirement 1

ROUTER WIRELESS

Balance Sheet (Partial)

December 31, 2016

21,000

25,000

75,000

76,000

Requirement 2

Debt to equity ratio

=

Total liabilities

/

Total equity

=

/

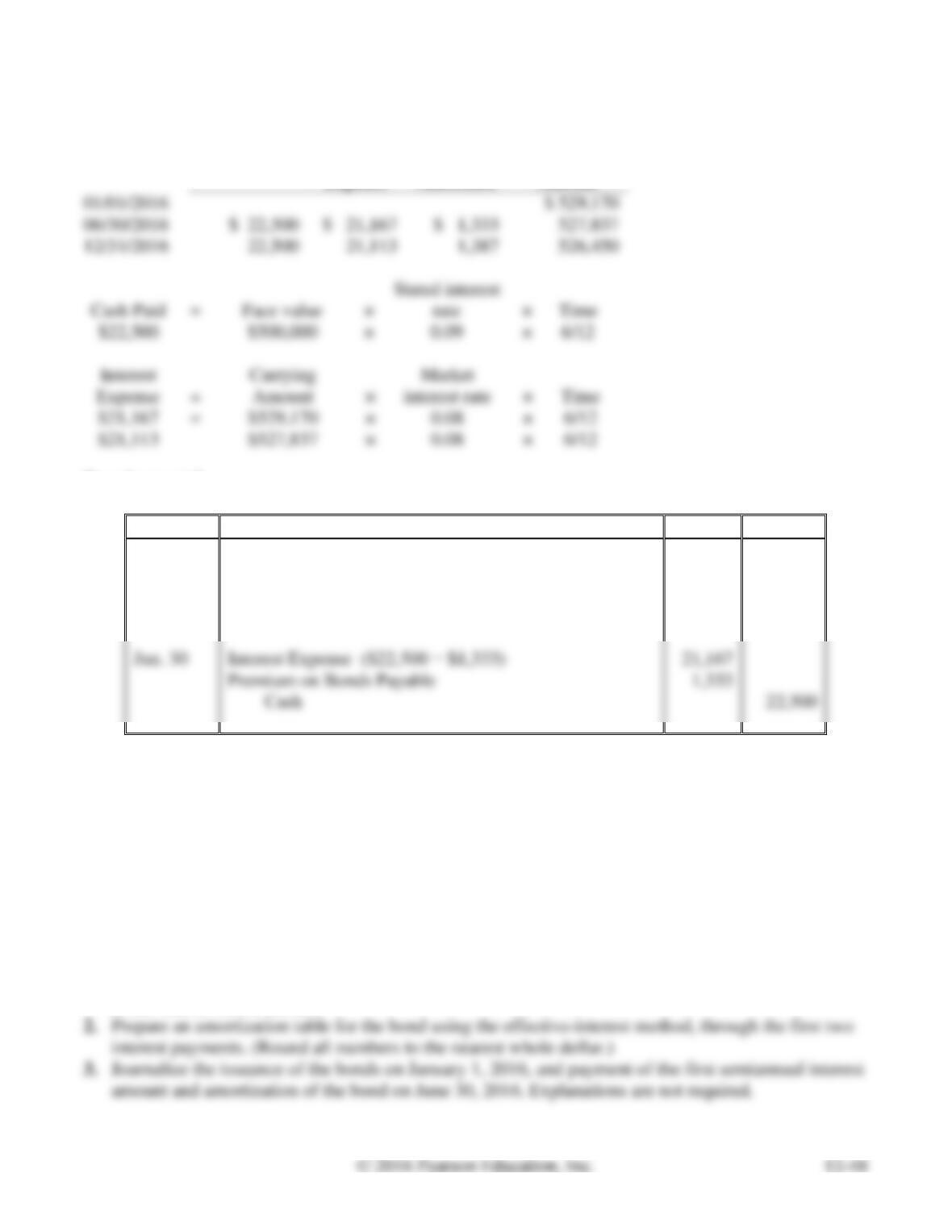

P12AB-36A Determining the present value of bonds payable and journalizing using the effective-

interest amortization method

Learning Objectives 7, 8

Appendixes 12A, 12B

3. Jan. 1, 2016, Cash DR $529,170

Ben Norton issued $500,000 of 9%, 8-year bonds payable on January 1, 2016. The market interest rate

at the date of issuance was 8%, and the bonds pay interest semiannually.

Requirements

1. How much cash did the company receive upon issuance of the bonds payable? (Round all numbers

to the nearest whole dollar.)

2. Prepare an amortization table for the bond using the effective-interest method, through the first two

interest payments. (Round all numbers to the nearest whole dollar.)

3. Journalize the issuance of the bonds on January 1, 2016, and payment of the first semiannual interest

amount and amortization of the bond on June 30, 2016. Explanations are not required.

SOLUTION

Requirement 1

Present value of principal:

Present value

=

Future value

×

=

Present value of stated interest:

Present value

=

×

=

=

=

Present value of bonds payable:

Present value

=

=

=

PV factor for

i = 4% (8% / 2),

P12AB-36A, cont.

Requirement 2

Cash Paid

Interest

Expense

Premium

Amortized

Carrying

Amount

×

$22,500

×

$21,167

$21,113

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 1

Cash

529,170

Premium on Bonds Payable ($529,170 − $500,000)

29,170

Bonds Payable

500,000

Jun. 30

Interest Expense ($22,500 − $1,333)

Premium on Bonds Payable

Cash

22,500

P12AB-37A Determining the present value of bonds payable and journalizing using the effective-

interest amortization method

Learning Objectives 7, 8

Appendixes 12A, 12B

3. Jan. 1, 2016, Cash DR $557,025

Serenity, Inc. is authorized to issue 5%, 10-year bonds payable. On January 1, 2016, when the market

interest rate is 8%, the company issues $700,000 of the bonds. The bonds pay interest semiannually.

Requirements

1. How much cash did the company receive upon issuance of the bonds payable? (Round all numbers

to the nearest whole dollar.)

SOLUTION

Requirement 1

Present value of principal:

Present value

=

Future value

×

=

Present value of stated interest:

=

=

=

Present value of bonds payable:

Present value

=

=

=

PV factor for

i = 4% (8% / 2),

Requirement 2

Cash Paid

Interest

Expense

Discount

Amortized

Carrying

Amount

01/01/2016

$ 557,025

06/30/2016

12/31/2016

=

Face value

×

×

=

×

=

×

=

×

P12AB-37A, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 1

Cash

557,025

$557,025)

Jun. 30

Interest Expense ($17,500 + $4,781)

Discount on Bonds Payable

Cash

Problems (Group B)

P12-38B Journalizing liability transactions and reporting them on the balance sheet

Learning Objectives 1, 5

1. Jan. 1, 2017, Interest Payable DR $3,000

2. Total Liabilities $853,895

The following transactions of Emergency Pharmacies occurred during 2016 and 2017:

Requirements

1. Journalize the transactions in the Emergency Pharmacies general journal. Round all answers to the

nearest dollar. Explanations are not required.

2. Prepare the liabilities section of the balance sheet for Emergency Pharmacies on March 1, 2017 after

all the journal entries are recorded.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Mar. 1

Cash

330,000

Notes Payable

330,000

Dec. 1

Cash

600,000

Mortgages Payable

600,000

Dec. 31

Interest Expense ($600,000 × 0.06 × 1/12)

Interest Payable

Dec. 31

Interest Expense ($330,000 × 0.13 × 10/12)

Interest Payable

2017

Interest Payable

Jan. 1

Mortgages Payable ($10,000 − $7,000)

Cash

Feb. 1

Interest Expense

Mortgages Payable ($10,000 − $2,965)

Cash

Mar. 1

Interest Expense

Mortgages Payable ($10,000 − $2,930)

Cash

Mar. 1

Interest Payable

Interest Expense($330,000 × 0.13 × 2/12)

Notes Payable

Cash

P12-38B, cont.

Requirement 1, cont.

Sawyer Bank Interest Calculations

Beginning

Balance

Principal

Payment

Interest

Expense

Total

Payment

Ending

Balance

12/01/2014

$ 600,000

01/01/2015

$ 600,000

$ 10,000

02/01/2015

03/01/2015

=

×

=

×

=

×

=

×

Requirement 2

EMERGENCY PHARMACIES

Balance Sheet (Partial)

March 1, 2017

Liabilities

Current Liabilities

Current Portion of Notes Payable

$ 55,000

Notes Payable

Total Long-term Liabilities

P12-38B, cont.

Requirement 2, cont.

Beginning

Balance

Principal

Payment

Interest

Expense

Total

Payment

Ending

Balance

12/01/2016

$ 600,000

01/01/2017

$ 600,000

$7,000

3,000

$ 10,000

593,000

02/01/2017

593,000

2,965

585,965

P12-39B Analyzing, journalizing, and reporting bond transactions

Learning Objectives 2, 3

2. Discount CR $2,000

George’s Hamburgers issued 8%, 10-year bonds payable at 80 on December 31, 2016. At December 31,

2018, George reported the bonds payable as follows:

Requirements

1. Answer the following questions about George’s bonds payable:

a. What is the maturity value of the bonds?

b. What is the carrying amount of the bonds at December 31, 2018?

c. What is the semiannual cash interest payment on the bonds?

d. How much interest expense should the company record each year?

2. Record the June 30, 2018, semiannual interest payment and amortization of discount.