CHAPTER 12

The Statement of Cash Flows

OVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated

Time in

Learning Objectives Exercises Minutes Level

Module 1

1. Explain the concept of cash flows and accrual accounting 25* 60 Diff

and the purpose of a statement of cash flows.

4. Describe the difference between the direct and indirect

methods of computing cash flow from operating activities.

Module 2

5. Use T accounts to prepare a statement of cash flows using the 6 5 Mod

direct method to determine cash flow from operating activities. 7 5 Mod

8 10 Mod

Module 3

6. Use T accounts to prepare a statement of cash flows using 16 10 Mod

the indirect method to determine cash flow from operating 17 10 Easy

activities. 18 15 Mod

12-2 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Estimated

Time in

Learning Objectives Exercises Minutes Level

Module 4

7. Use cash flow information to help analyze a company. 19 15 Mod

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-3

Problems Estimated

and Time in

Learning Objectives Alternates Minutes Level

Module 1

1. Explain the concept of cash flows and accrual accounting

and the purpose of a statement of cash flows.

Module 2

5. Use T accounts to prepare a statement of cash flows using the 3 45 Mod

direct method to determine cash flow from operating activities. 6 30 Mod

11* 30 Mod

13* 30 Diff

Module 3

6. Use T accounts to prepare a statement of cash flows using 1 30 Mod

the indirect method to determine cash flow from operating 4 45 Mod

activities. 7 30 Mod

9 45 Diff

12* 30 Mod

12-4 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Estimated

Time in

Learning Objectives Cases Minutes Level

Module 1

1. Explain the concept of cash flows and accrual accounting 4* 60 Diff

and the purpose of a statement of cash flows. 5* 25 Mod

6* 25 Mod

Module 2

5. Use T accounts to prepare a statement of cash flows using the 4* 60 Diff

direct method to determine cash flow from operating activities.

Module 3

Module 4

7. Use cash flow information to help analyze a company. 2 20 Mod

Module 5

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-5

EXERCISES

LO 2 EXERCISE 12-1 CASH EQUIVALENTS

Investments made during December 2016 that qualify as cash equivalents at

December 31, 2016:

LO 3 EXERCISE 12-2 CLASSIFICATION OF ACTIVITIES

1. F 6. O 10. I

LO 3 EXERCISE 12-3 RETIREMENT OF BONDS PAYABLE ON THE STATEMENT OF

CASH FLOWS—INDIRECT METHOD

1. Journal entry:

Journal 2016

Entry Dec. 31 Bonds Payable ……………………………………… 500,000

Analysis Loss on Retirement of Bonds …………………. 50,000

2. The $510,000 in cash paid to retire the bonds would be reported as a cash outflow in

the Financing Activities section. Assuming the company uses the indirect method,

the loss of $50,000 would be added back in the Operating Activities section.

12-6 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 3 EXERCISE 12-4 CLASSIFICATION OF ACTIVITIES FOR CARNIVAL CORPORATION

1. F 3. O 5. F

2. F 4. I 6. O

LO 5 EXERCISE 12-6 CASH COLLECTIONS—DIRECT METHOD

Cash collections to be reported in the Operating Activities section of Spencer’s 2016

statement of cash flows (direct method):

Accounts receivable, December 31, 2015 …………………………….. $28,000

LO 5 EXERCISE 12-7 CASH COLLECTIONS—DIRECT METHOD

Cash collections to be reported in the Operating Activities section of Stanley’s 2016

statement of cash flows (direct method):

Accounts receivable, December 31, 2015 …………………………….. $ 80,800

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-7

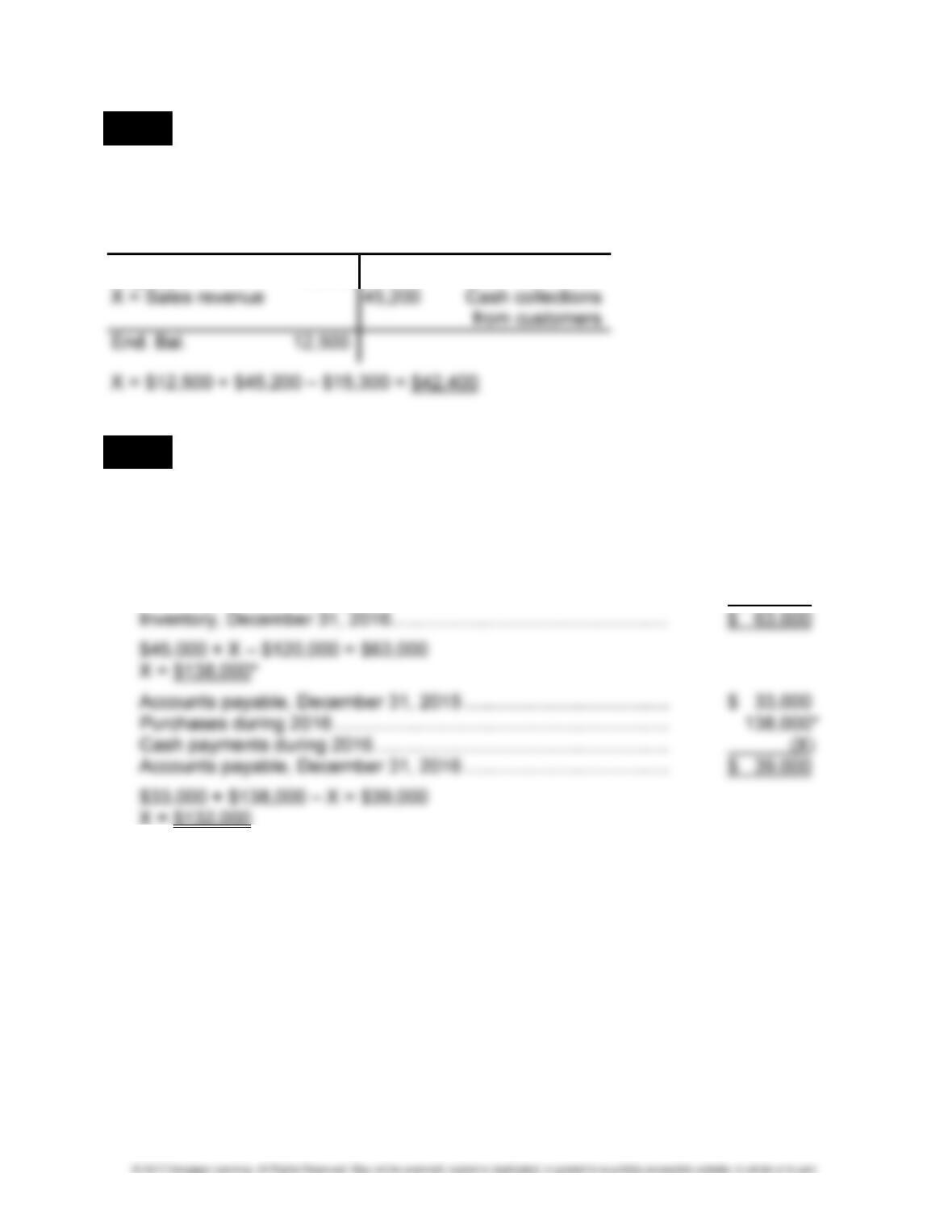

LO5 EXERCISE 12-8 WORKING BACKWARD: CASH COLLECTIONS—DIRECT METHOD

Sales revenue can be determined by analyzing the change in the Accounts Receivable

account:

Accounts Receivable

Beg. Bal. 15,300

LO 5 EXERCISE 12-9 CASH PAYMENTS—DIRECT METHOD

Cash payments for inventory to be reported in the Operating Activities section of Wolf’s

2016 statement of cash flows (direct method):

Inventory, December 31, 2015 …………………………………………….. $ 45,000

Purchases during 2016 ………………………………………………………. X

Cost of goods sold during 2016 …………………………………………… (120,000)

12-8 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

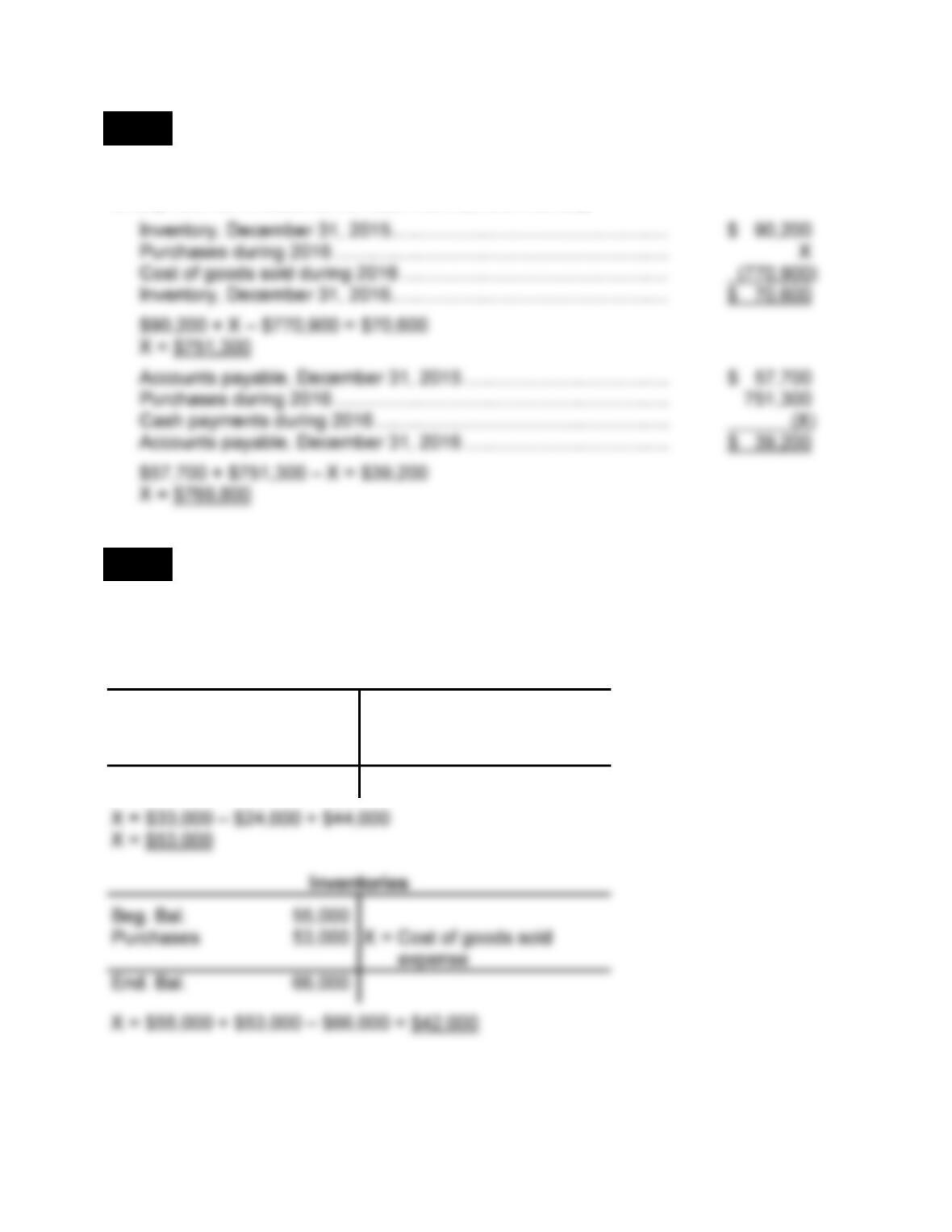

LO 5 EXERCISE 12-10 CASH PAYMENTS—DIRECT METHOD

Cash payments for inventory to be reported in the Operating Activities section of Lester

Enterprises’ 2016 statement of cash flows (direct method):

LO5 EXERCISE 12-11 WORKING BACKWARD: CASH PAYMENTS—DIRECT METHOD

Cost of goods sold expense can be determined by analyzing first the change in the Ac-

counts Payable account and then in the Inventories account:

Accounts Payable

Cash paid to

acquire Inventories 44,000

24,000 Beg. Bal.

X = Purchases

33,000 End. Bal.

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-9

LO 5 EXERCISE 12-12 OPERATING ACTIVITIES SECTION—DIRECT METHOD

1. Operating Activities section of the statement of cash flows:

LABRADOR COMPANY

PARTIAL STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

Cash Flows from Operating Activities

Cash collected from customers ……………………………………………. $102,0001

Cash payments for:

Footnotes:

1Cash collections from customers:

Sales revenue ………………………………………………………………. $100,000

Decrease in accounts receivable …………………………………….. 2,000

Cash collections …………………………………………………………… $ 102,000

4For interest:

Interest expense …………………………………………………………… $ 3,000

Decrease in interest payable ………………………………………….. 500

Cash payments …………………………………………………………….. $ 3,500

12-10 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 12-12 (Concluded)

2. The use of the direct method reveals the amounts collected from customers and the

amounts paid for inventory, interest, taxes, and other operating purposes. The indi-

rect method simply reconciles the net income of the period to the net cash flow from

operations. The direct method shows the reader of the statement the specific

amounts collected and paid for operating purposes.

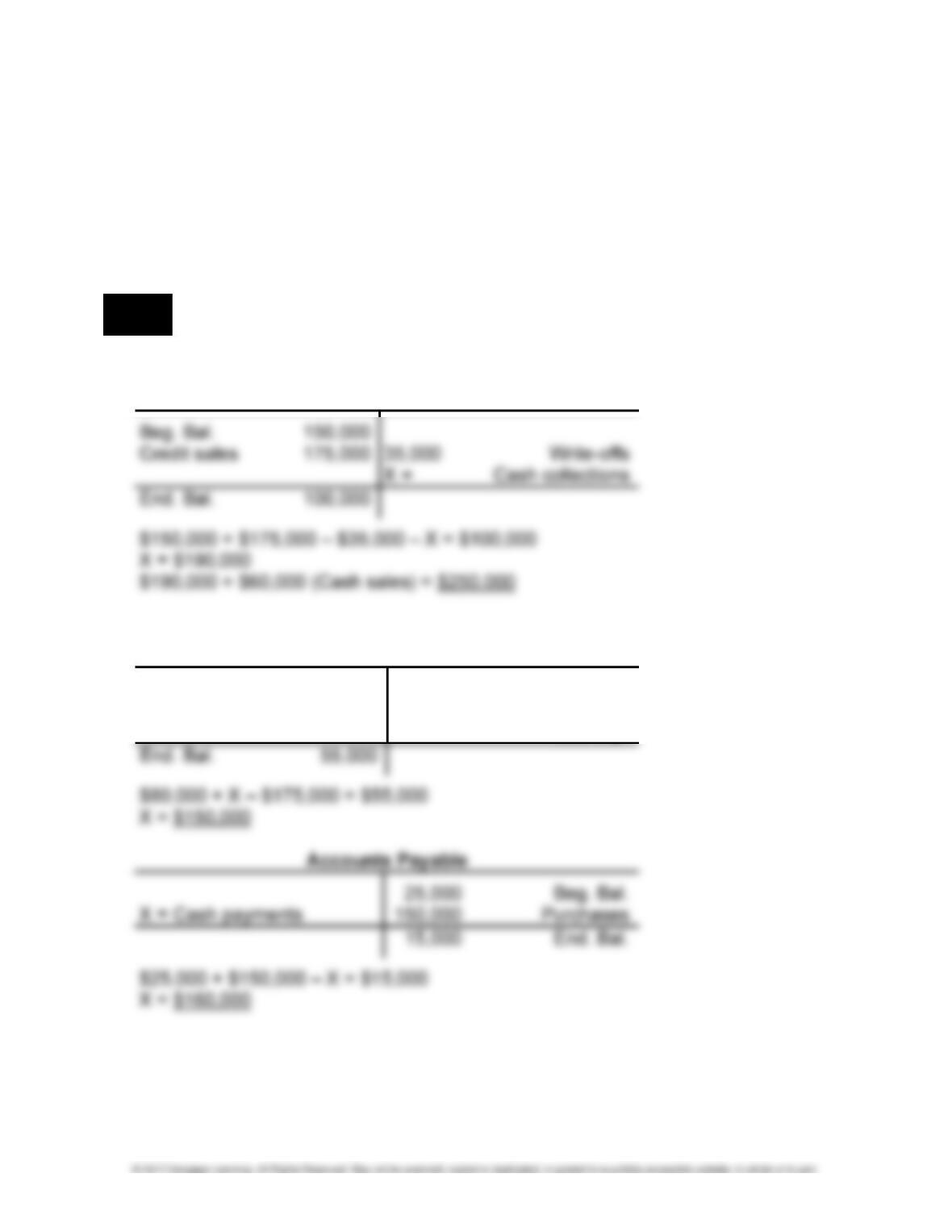

LO 5 EXERCISE 12-13 DETERMINATION OF MISSING AMOUNTS—CASH FLOW FROM

OPERATING ACTIVITIES

Case 1:

Accounts Receivable

Case 2:

Inventory

Beg. Bal. 80,000

X = Purchases

175,000 Cost of goods

sold exp.

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-11

EXERCISE 12-13 (Concluded)

Case 3:

Prepaid Insurance

Beg. Bal. 17,000

15,000 Insurance

Case 4:

Income Taxes Payable

95,000 Beg. Bal.

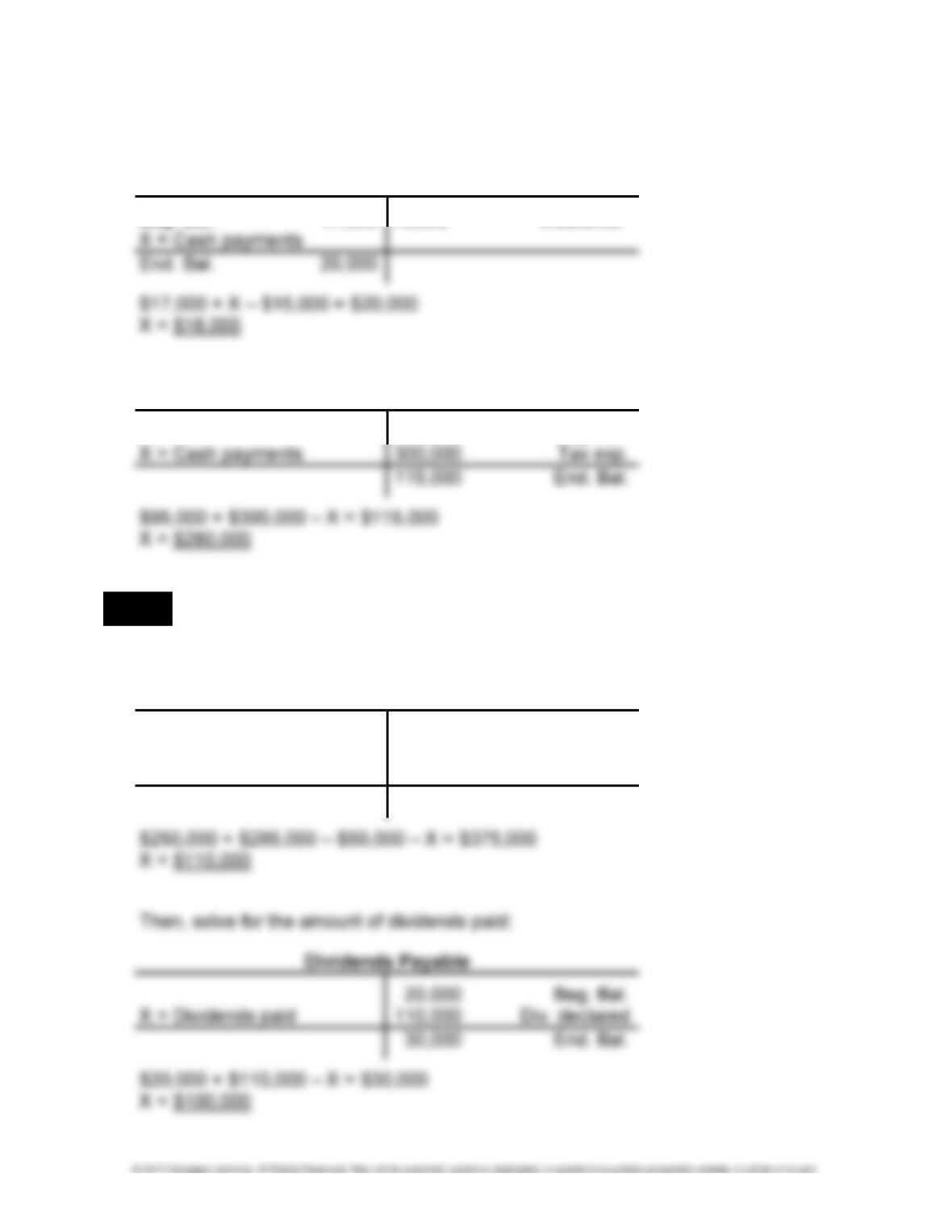

LO 5 EXERCISE 12-14 DIVIDENDS ON THE STATEMENT OF CASH FLOWS

1. First, determine the amount of dividends declared:

Retained Earnings

250,000 Beg. Bal.

Stock dividend 50,000

X = Dividends declared

285,000 Net income

375,000 End. Bal.

12-12 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 12-14 (Concluded)

2. Because a stock dividend does not involve cash, it is not reported on the statement

of cash flows. It is questionable whether or not a stock dividend is a significant non-

cash activity that should be reported on a supplemental schedule.

LO5 EXERCISE 12-15 WORKING BACKWARD: DIVIDENDS ON THE STATEMENT OF

CASH FLOWS

Since the company paid dividends during its first year of $160,000 and has a balance of

LO 6 EXERCISE 12-16 CASH PAYMENTS FOR INCOME TAXES—INDIRECT METHOD

Income Taxes Payable

Income tax paid

in cash 12,000

10,000 Beg. Bal.

X = Income taxes

accrued

15,000 End. Bal.

LO 6 EXERCISE 12-17 ADJUSTMENTS TO NET INCOME WITH THE INDIRECT METHOD

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-13

LO 6 EXERCISE 12-18 OPERATING ACTIVITIES SECTION—INDIRECT METHOD

1. Operating Activities section of the statement of cash flows:

SUFFOLK COMPANY

PARTIAL STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

Cash Provided by Operating Activities

Net income ……………………………………………………………………………. $40,000

2. The primary reason that net cash inflow from operating activities of $66,000 is more

than net income of $40,000 is depreciation of $20,000. It is deducted on the income

statement, but it does not require the use of cash. Other reasons for the higher

LO 7 EXERCISE 12-19 CASH FLOW ADEQUACY

1. Cash flow adequacy ratio:

(Net cash provided by operations – Capital expenditures)/Average annual debt

maturing over next five years

2. The cash flow adequacy ratio gives the user an indication of whether or not the

company is generating sufficient cash from its operations to repay its debts, after

12-14 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

MULTI-CONCEPT EXERCISES

LO 2,3 EXERCISE 12-20 CLASSIFICATION OF ACTIVITIES

LO 3,5 EXERCISE 12-21 CLASSIFICATION OF ACTIVITIES

1. IO 3. NR 5. IO 7. OO 9. OF 11. OF

2. OO 4. IF 6. NR 8. OI 10. NR 12. II

LO 3,6 EXERCISE 12-22 LONG-TERM ASSETS ON THE STATEMENT OF CASH

FLOWS—INDIRECT METHOD

First, determine the accumulated depreciation on the assets sold so that the book value

of those sold can be found:

Thus, the entry to record the sale would be as follows:

Journal Cash ………………………………………………………………… 64,000

Entry Accumulated Depreciation …………………………………… 90,000

Analysis Plant and Equipment …………………………………….. 150,000

Gain on Sale of Plant and Equipment ……………… 4,000

To record sale of plant and equipment at a gain.

Balance Sheet Income Statement

STOCKHOLDERS’

NET

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-15

EXERCISE 12-22 (Concluded)

Plant and Equipment

Beg. Bal. 500,000

X = Acquisitions

150,000 Sale of plant

and equipment

Similarly, acquisitions of new patents can be determined:

Patents

Beg. Bal. 80,000

These items would appear on the statement of cash flows as follows:

Cash Flows from Operating Activities

Net income ………………………………………………………………………………… $ 200,000

Adjustments to reconcile net income to net cash

12-16 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO3,6 EXERCISE 12-23 WORKING BACKWARD: INVESTING ACTIVITIES ON THE

STATEMENT OF CASH FLOWS

1. Both depreciation expense and the loss on sale of equipment are added in the

2. The cash received from the sale of the equipment will be added in the Investing

Activities section of the statement of cash flows. The book value of the equipment at

LO3,6 EXERCISE 12-24 WORKING BACKWARD: FINANCING ACTIVITIES ON THE

STATEMENT OF CASH FLOWS

1. The gain on the retirement of the bonds is deducted in the Operating Activities sec-

2. Since the company used cash of $95,000 to retire the bonds and reported a gain of

$5,000, the book value of the bonds was $95,000 + $5,000 = $100,000.

LO 1,5 EXERCISE 12-25 INCOME STATEMENT, STATEMENT OF CASH FLOWS

(DIRECT METHOD), AND BALANCE SHEET

1. Income statement:

HANDSOME HOUNDS GROOMING COMPANY

INCOME STATEMENT

FOR THE YEAR ENDED XX/XX/XX

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-17

EXERCISE 12-25 (Continued)

2. Statement of cash flows:

HANDSOME HOUNDS GROOMING COMPANY

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED XX/XX/XX

Cash Flows from Operating Activities

Cash receipts from:

Cash sales ……………………………………………………………………….. $110,0001

Cash Flows from Investing Activities

Down payment on patent ……………………………………………………. $ (20,000)4

Cash Flows from Financing Activities

Issuance of common stock …………………………………………………. $ 50,000

Supplemental Schedule of Noncash Activities

Acquisition of patent in exchange for four-year note ……………….. $ 80,000

3. The company generated slightly less cash flow from operations, $68,000, than it

earned in net income, $70,000. The differences between the two can be reconciled

as follows:

Net income ……………………………………………………………………………. $ 70,000

12-18 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 12-25 (Concluded)

4. Balance sheet:

HANDSOME HOUNDS GROOMING COMPANY

BALANCE SHEET

AS OF XX/XX/XX

Assets

Current assets:

Cash [from part (2)] …………………………………………….. $78,000

Liabilities and Stockholders’ Equity

Long-term liabilities:

Notes payable …………………………………………………….. $ 80,000

Stockholders’ equity:

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-19

PROBLEMS

LO 6 PROBLEM 12-1 STATEMENT OF CASH FLOWS—INDIRECT METHOD

1. Changes in account balances and explanations (in thousands of dollars):

Net Change

Dr. (Cr.) Explanation

Cash (2)

Accounts receivable 5

Inventory (10)

Prepaid rent 3

12-20 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 12-1 (Concluded)

Statement of cash flows:

CHRISMAN COMPANY

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

(IN THOUSANDS OF DOLLARS)

Cash Flows from Operating Activities

Net income ……………………………………………………………………………. $ 26

Adjustments to reconcile net income to net cash provided

by operating activities:

Cash Flows from Investing Activities

Acquisition of plant and equipment ………………………………………. $(100)

Cash Flows from Financing Activities

Retirement of bonds payable ………………………………………………. $ (25)

2. No, Chrisman did not generate enough cash from its operations to pay for its invest-

ing activities. Cash flow from operating activities amounted to only $63,000, while