CHAPTER 12

THE COST OF CAPITAL FOR LAYTON

MOTORS

NOTE: The example below shows the results during November 2015. The actual answer to the case

will change based on current market conditions.

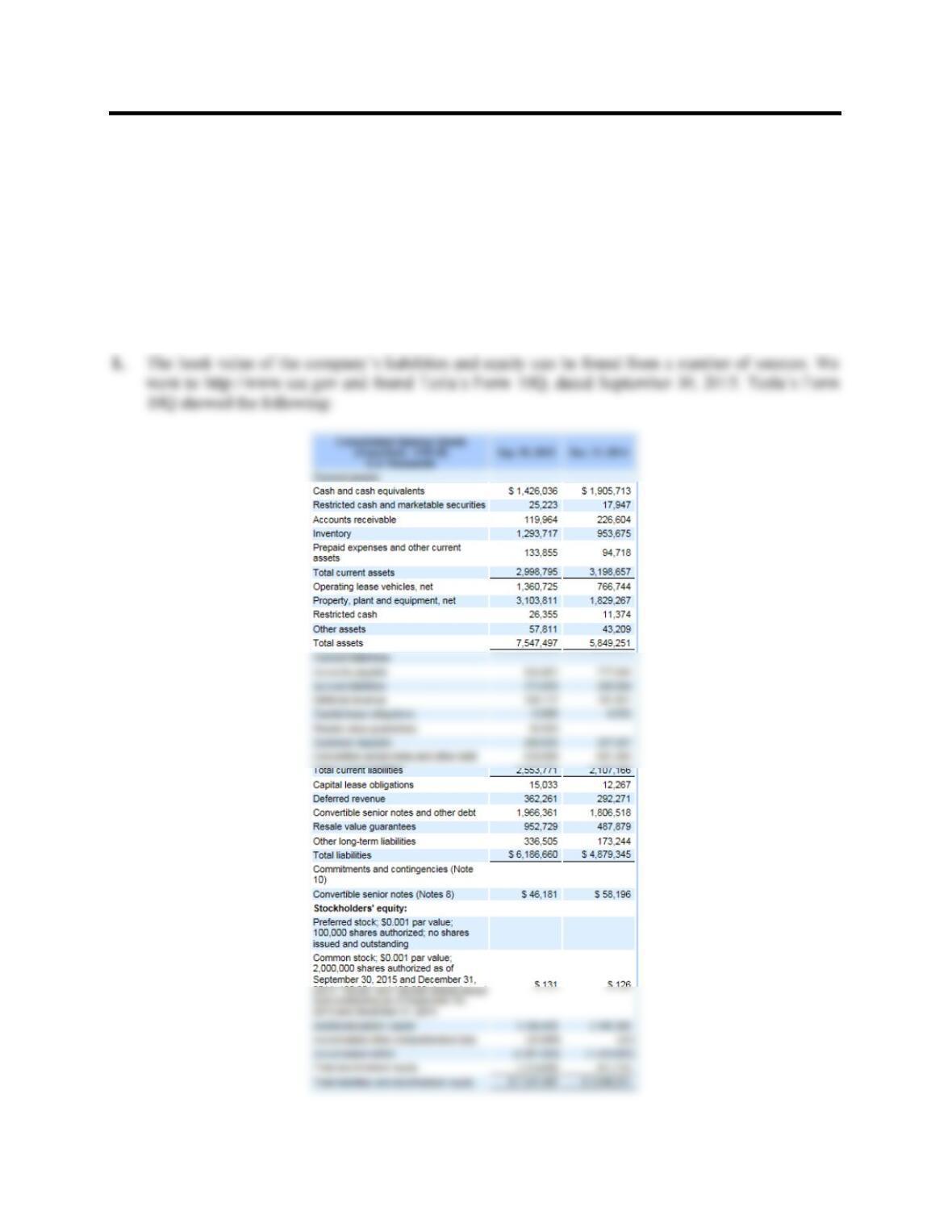

The book value of equity is $1,315 million on the balance sheet. However, for a more current book

value, we multiplied the number of shares outstanding by the book value per share on Yahoo!

Finance. For the book value of debt, we used the following note in the 10Q:

2. We need various pieces of information to estimate the cost of equity. We cannot use the dividend

growth model since Tesla does not pay a dividend, so we will use the CAPM. The following

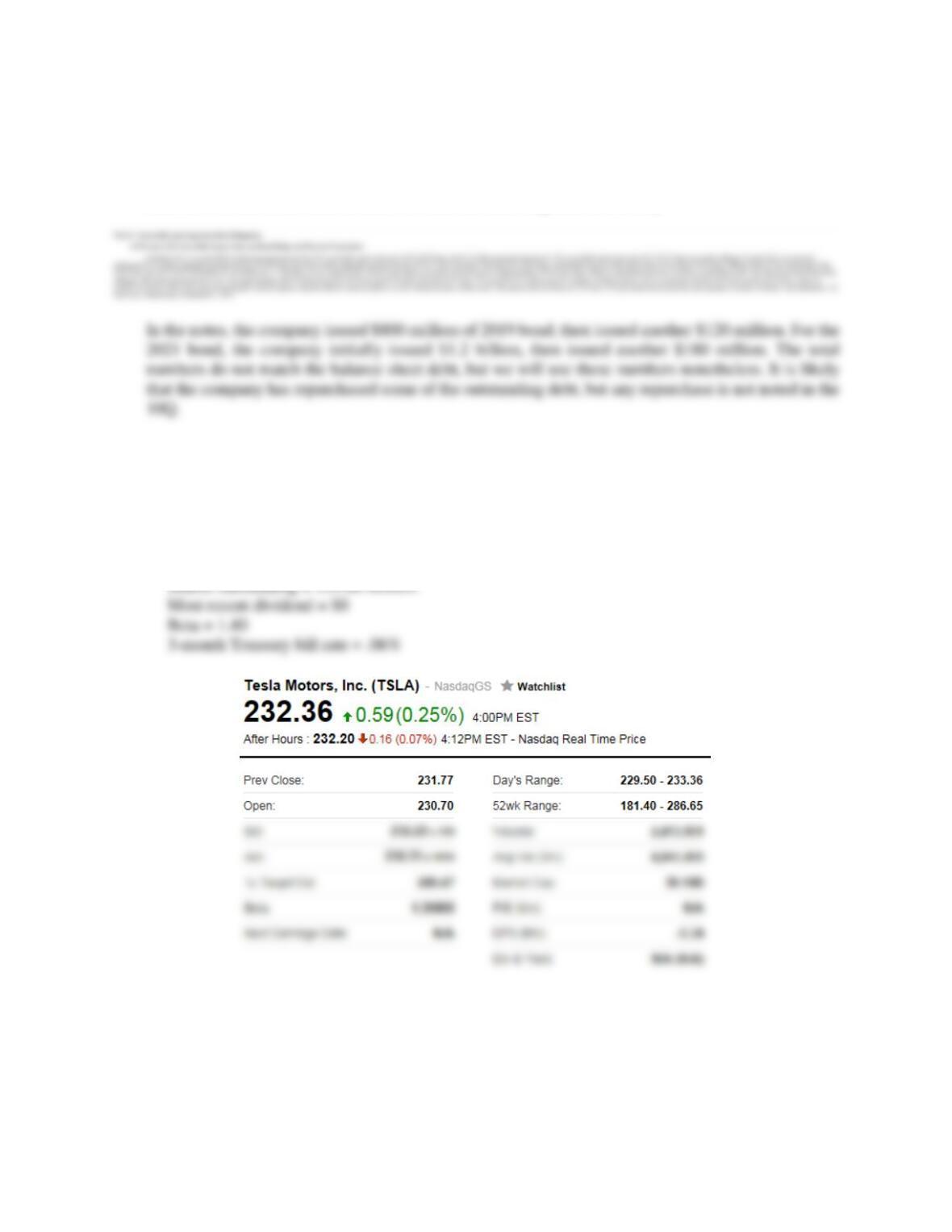

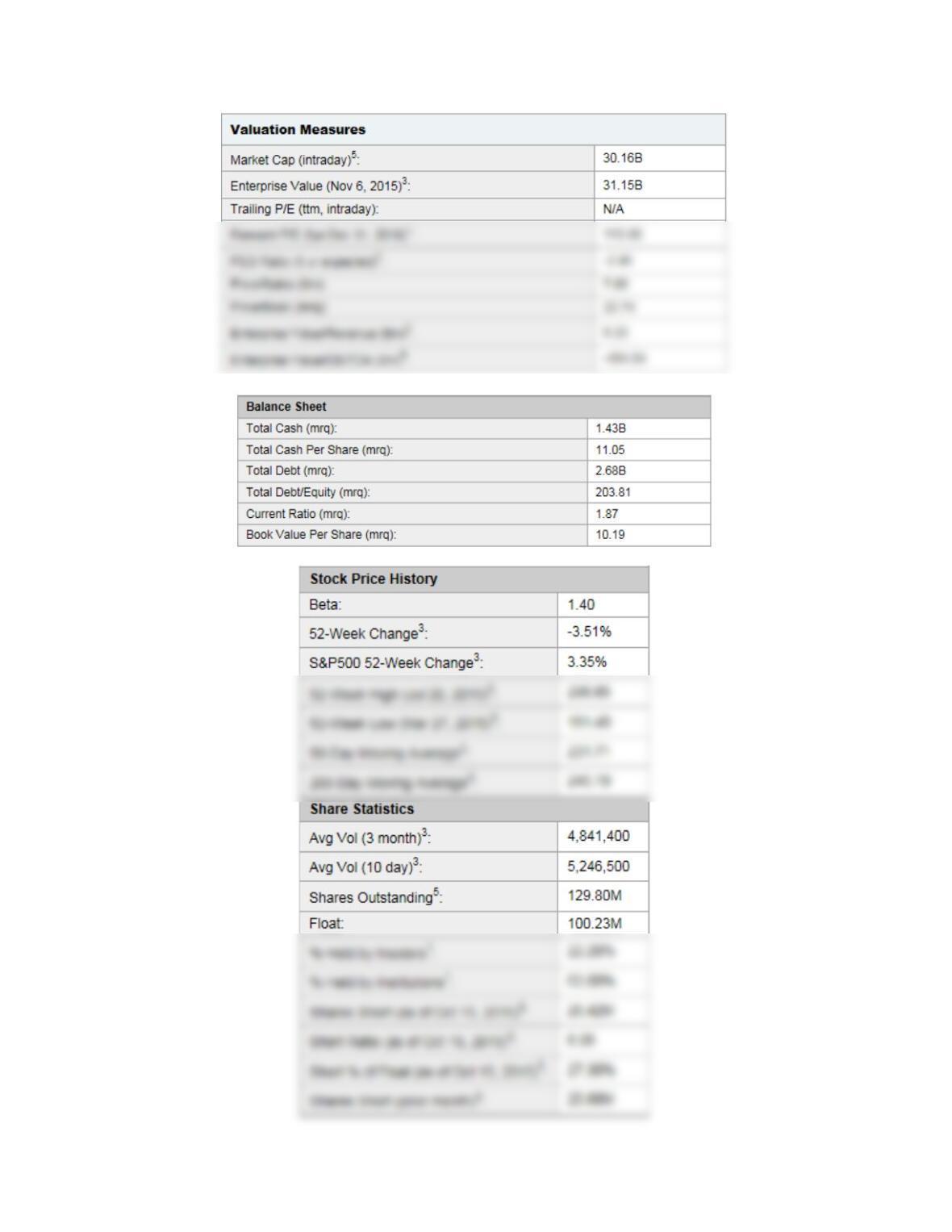

information is necessary for our calculations. We gathered all the information from

finance.yahoo.com. The screen shots below show this information.

Market price = $232.36

Market capitalization = $30.16 billion

Tesla has never paid a dividend so we cannot use the dividend growth model to estimate the cost of

equity. We do have the information to estimate the cost of equity with the CAPM. Using the market

risk premium of 7 percent from the textbook, we get:

RE = Rf + [E(RM) – Rf]

RE = .0006 + 1.40[.07]

RE = .0986, or 9.86%

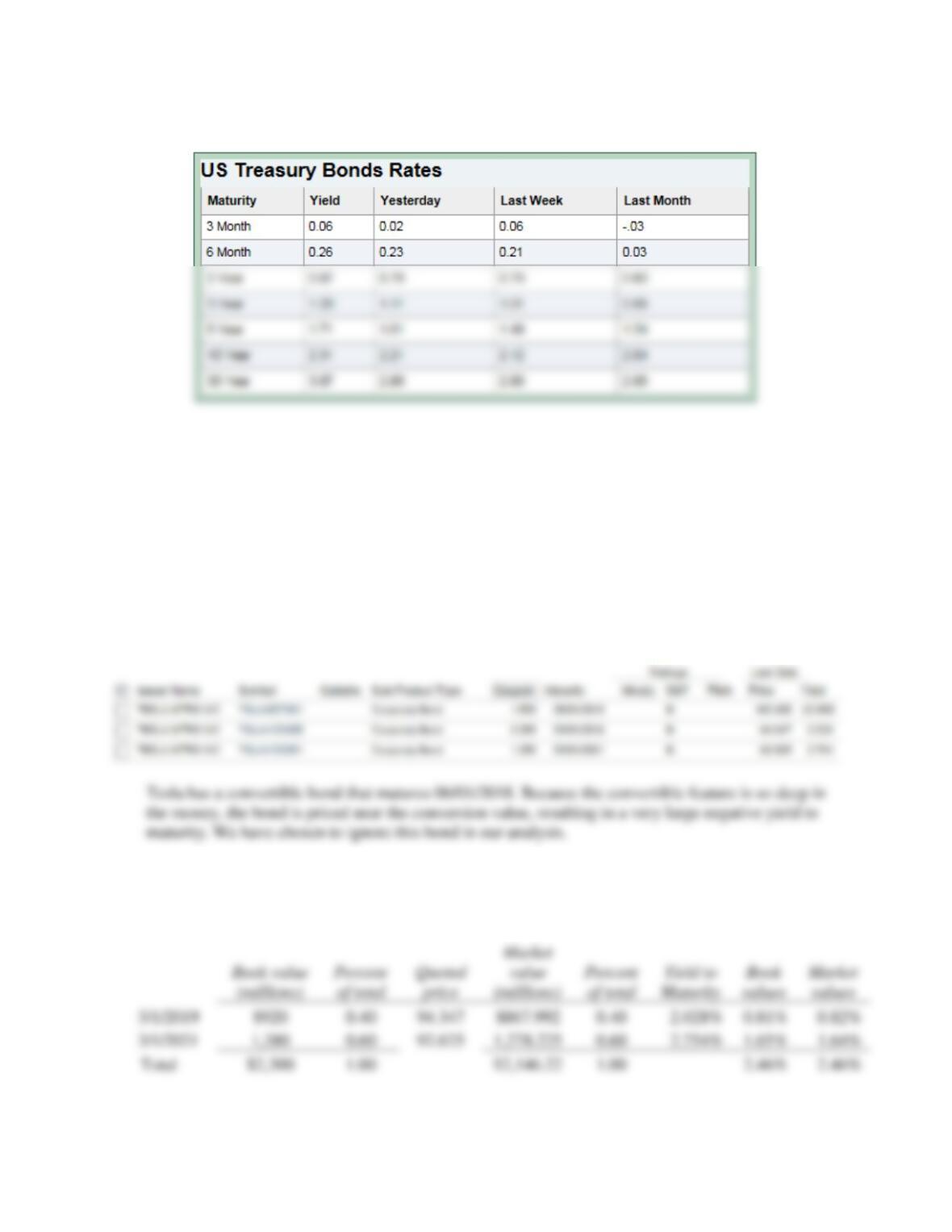

3. To get the yield to maturity on Tesla’s bonds, we went to finra-

markets.morningstar.com/BondCenter/. We gathered the following information:

If you click on the link for each bond, the website provides information concerning the bond, including

the face amount of the issue. So, the weighted average cost of debt for Tesla using both the book value

and the market value is:

4. Using book value weights, the total value of Tesla is:

V = $2,300,000,000 + $1,322,662,000

V = $3,622,662,000

So, the WACC based on book value weights is:

So, the WACC based on market value weights is:

WACC = RE(E/V) + RD(D/V)(1 – T)

WACC = (.0986)($30,160,328,000 /$32,306,545,400)

+ (.0246)($2,146,217,400 /$32,306,545,400)(1 – .35)

WACC = .0931, or 9.31%