CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-41

PROBLEM 12-10 (Concluded)

3. Statement of cash flows:

TERRIER COMPANY

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

(IN THOUSANDS OF DOLLARS)

Cash Flows from Operating Activities

Net income ……………………………………………………………………………. $ 70

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense ………………………………………………………… 20

Increase in accounts receivable ………………………………………….. (10)

Net cash provided by operating activities …………………………………… $ 80

4. In addition to the bonds issued in exchange for land, Terrier issued $150,000 of

bonds for cash. The money raised from this issuance was needed to help finance

the addition of $200,000 in plant and equipment.

12-42 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

MULTI-CONCEPT PROBLEMS

LO 4,5 PROBLEM 12-11 STATEMENT OF CASH FLOWS—DIRECT METHOD

1. Changes in account balances and explanations (in thousands of dollars):

Net Change

Dr. (Cr.) Explanation

Cash (9)

Accounts receivable 15

Accounts payable (7)

Other accrued liabilities (6)

Income taxes payable 2

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-43

PROBLEM 12-11 (Continued)

Conversion of income statement items to a cash basis (in thousands of dollars):

Income Statement Amount Adjustment Cash Flows

Sales revenue $550 $550

– Increase in accounts receivable (15)

Cash collected $535

Cost of goods sold 350 $350

– Decrease in inventory (15)

– Increase in accounts payable (7)

Cash payments $328

General and

12-44 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 12-11 (Concluded)

Statement of cash flows:

GLENDIVE CORP.

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED JUNE 30, 2016

(IN THOUSANDS OF DOLLARS)

Cash Flows from Operating Activities

Cash collections from customers ……………………………………………… $ 535

Cash payments for:

Inventory ………………………………………………………………………….. $(328)

General and administrative …………………………………………………. (45)

Interest ……………………………………………………………………………. (15)

Cash Flows from Financing Activities

Repayment of long-term loan ……………………………………………… $ (30)

Issuance of additional stock ……………………………………………….. 150

Payment of cash dividends …………………………………………………. (7)

Net cash provided by financing activities …………………………………… $ 113

Net decrease in cash ……………………………………………………………… $ (9)

Cash balance, June 30, 2015 ………………………………………………….. 40

Cash balance, June 30, 2016 ………………………………………………….. $ 31

2. It is true that the amount of cash flow from operating activities is the same regard-

less of which method (direct or indirect) is used. The two methods, however, differ in

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-45

LO 4,6 PROBLEM 12-12 STATEMENT OF CASH FLOWS—INDIRECT METHOD

1. Changes in account balances and explanations (in thousands of dollars):

Net Change

Dr. (Cr.) Explanation

Cash (9)

Accounts receivable 15

Inventory (15)

12-46 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 12-12 (Concluded)

Statement of cash flows:

GLENDIVE CORP.

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED JUNE 30, 2016

Increase in accounts payable ……………………………………………… 7

Increase in other accrued liabilities ………………………………………. 6

Decrease in income taxes payable ………………………………………. (2)

Net cash provided by operating activities …………………………………… $ 128

*Book value $30 – proceeds $25

2. It is true that the amount of cash flow from operating activities is the same regard-

less of which method (direct or indirect) is used. The two methods, however, differ in

the information reported to the reader of the statement of cash flows. The direct me-

thod shows the actual inflows and outflows of cash, while the indirect method arrives

at the same amount by reconciling net income to cash flow from operating activities.

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-47

LO 2,5 PROBLEM 12-13 STATEMENT OF CASH FLOWS—DIRECT METHOD

1. No, the U.S. Treasury bills are not cash equivalents, because they have a maturity in

2. Changes in account balances and explanations (in thousands of dollars):

Net Change

Dr. (Cr.) Explanation

Cash (40)

12-48 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 12-13 (Continued)

Conversion of income statement items to a cash basis (in thousands of dollars):

Income Statement Amount Adjustment Cash Flows

Sales revenue $2,408 $2,408

– Increase in accounts receivable (110)

Cash collected $2,298

Cost of goods sold 1,100 $1,100

+ Increase in inventory 120

– Increase in accounts payable (60)

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-49

PROBLEM 12-13 (Concluded)

Statement of cash flows:

LANG COMPANY

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

(IN THOUSANDS OF DOLLARS)

Cash Flows from Operating Activities

Cash collections from customers ……………………………………………… $ 2,298

Cash payments for:

Inventory ………………………………………………………………………….. $(1,160)

Salaries and benefits …………………………………………………………. (850)

Cash Flows from Investing Activities

Sale of U.S. Treasury bills ………………………………………………….. $ 50

Acquisition of land …………………………………………………………….. (10)

Acquisition of buildings and equipment ………………………………… (110)

Net cash used by investing activities ………………………………………… $ (70)

12-50 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

ALTERNATE PROBLEMS

LO 6 PROBLEM 12-1A STATEMENT OF CASH FLOWS—INDIRECT METHOD

1. Changes in account balances and explanations:

Net Change

Dr. (Cr.) Explanation

Cash 2,000

Accounts receivable (2,000)

Inventory 1,000

Prepaid rent 200

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-51

PROBLEM 12-1A (Concluded)

Statement of cash flows:

MADISON COMPANY

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

Cash Flows from Operating Activities

Net loss ………………………………………………………………………………… $(21,800)

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense ………………………………………………………… 50,000

Cash Flows from Investing Activities

Acquisition of plant and equipment ………………………………………. $(50,000)

Cash Flows from Financing Activities

Issuance of bonds payable …………………………………………………. $ 25,000

Repayment of short-term notes payable ……………………………….. (2,500)

2. Madison was able to increase its cash balance even though it incurred a net loss

primarily because it had one very large expense that did not require the use of any

cash: depreciation of $50,000. This one adjustment is the major difference between

the net loss of $21,800 and the net cash flow from operating activities of $29,500.

12-52 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 8 PROBLEM 12-2A STATEMENT OF CASH FLOWS USING A WORK SHEET—

INDIRECT METHOD (APPENDIX)

1. Statement of cash flows work sheet (all amounts are in thousands of dollars)

Balances Cash Inflows (Outflows)

Accounts 12/31/16 12/31/15 Changes Operating Investing Financing

Cash 12.0 10.0 2.0

Accounts Receivable 10.0 12.0 (2.0) 2.0

Inventory 8.0 7.0 1.0 (1.0)

Prepaid Rent 1.2 1.0 0.2 (0.2)

Land 75.0 75.0 0.0

1

Purchase of equipment.

2

Depreciation expense.

3

Retirement of note.

4

Issuance of bonds.

5

Net loss.

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-53

PROBLEM 12-2A (Concluded)

2. Statement of cash flows:

MADISON COMPANY

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

Cash Flows from Operating Activities

Net loss ………………………………………………………………………………… $(21,800)

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense ………………………………………………………… 50,000

Decrease in accounts receivable …………………………………………. 2,000

Cash Flows from Investing Activities

Acquisition of plant and equipment ………………………………………. $(50,000)

Cash Flows from Financing Activities

Issuance of bonds payable …………………………………………………. $ 25,000

Repayment of short-term notes payable ……………………………….. (2,500)

Net cash provided by financing activities …………………………………… $ 22,500

12-54 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 PROBLEM 12-3A STATEMENT OF CASH FLOWS—DIRECT METHOD

1. Changes in account balances and explanations (in thousands of dollars):

Net Change

Dr. (Cr.) Explanation

Cash (70)

Accounts receivable (85)

Inventory 20

(350) Net income

Total 0

Conversion of income statement items to a cash basis (in thousands of dollars):

Income Statement Amount Adjustment Cash Flows

Sales revenue $2,460 $2,460

+ Decrease in accounts receivable 85

Cash collected $2,545

Cost of goods sold 1,400 $1,400

+ Increase in inventory 20

– Increase in accounts payable (20)

Cash payments $1,400

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-55

PROBLEM 12-3A (Continued)

Statement of cash flows:

WABASH CORP.

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

(IN THOUSANDS OF DOLLARS)

Cash Flows from Operating Activities

Cash collections from customers ……………………………………………… $ 2,545

Cash payments for:

Cash Flows from Investing Activities

Sale of land………………………………………………………………………. $ 100

Acquisition of plant and equipment ………………………………………. (250)

Net cash used by investing activities ………………………………………… $ (150)

Cash Flows from Financing Activities

Repayment of long-term borrowings …………………………………….. $ (50)

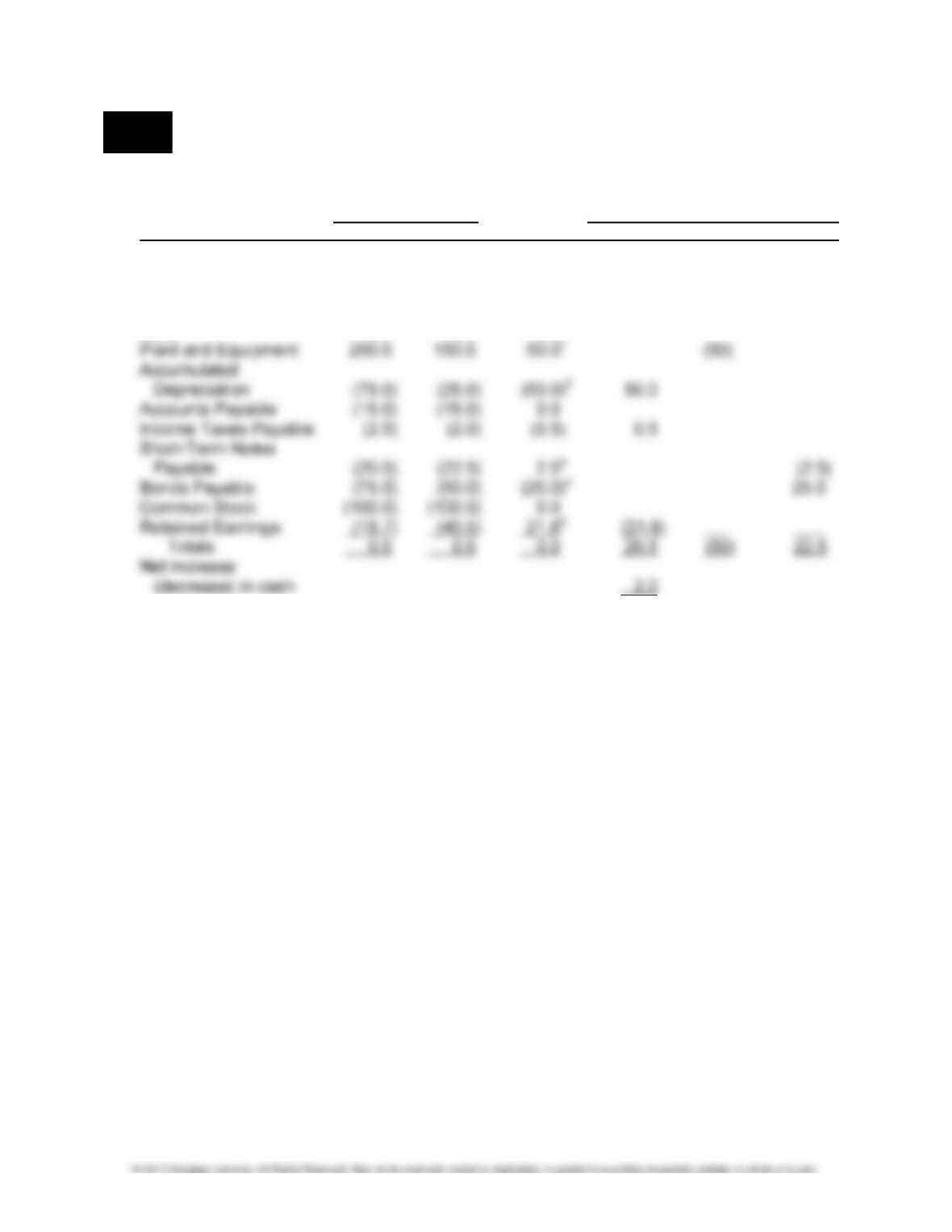

2. Memorandum to the president:

TO: President of Wabash Corp.

FROM: Student’s name

DATE: January 20, 2017

SUBJECT: Cash flows

12-56 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 12-3A (Concluded)

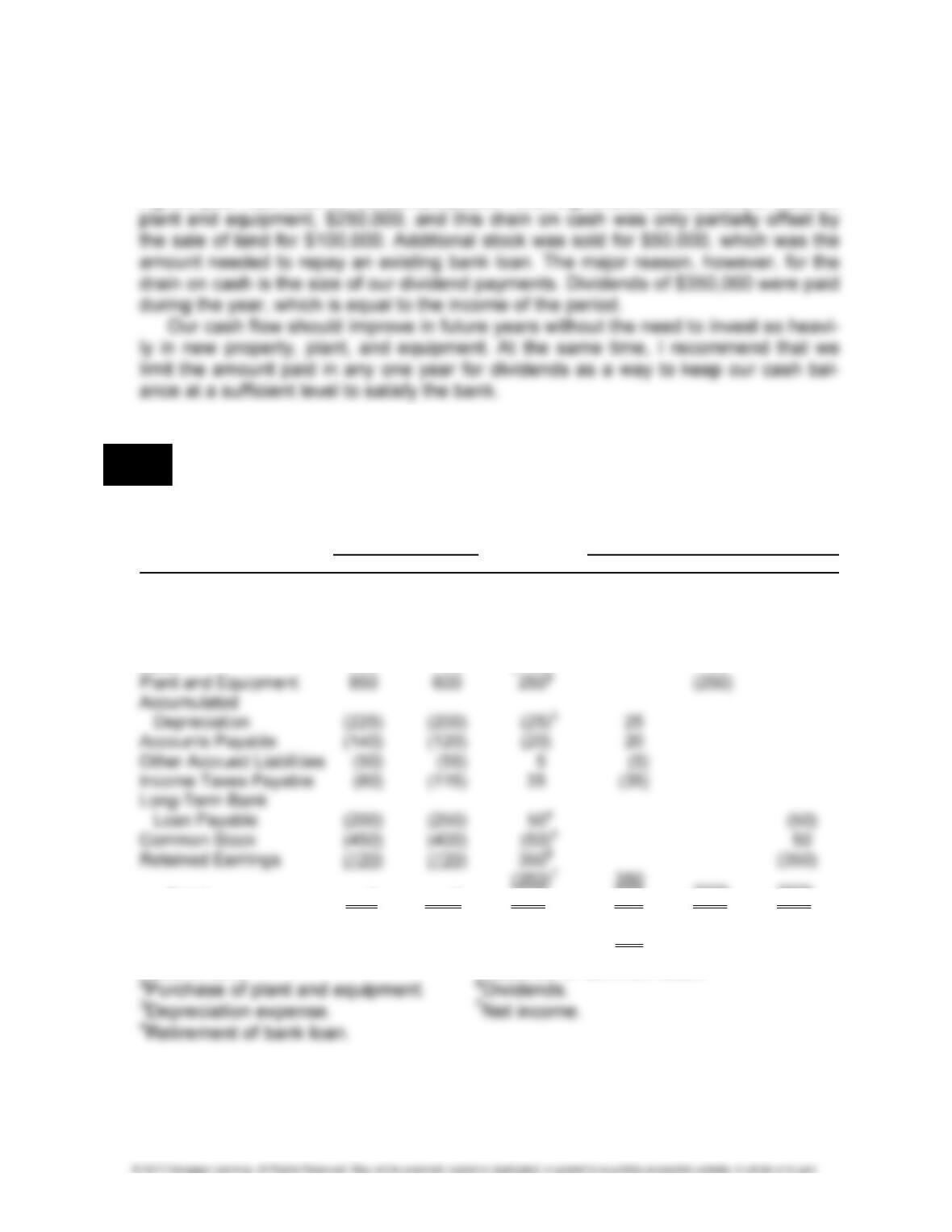

Although net income on an accrual basis was $350,000, net cash flow from op-

erating activities was even higher, $430,000. However, the favorable cash flow dur-

ing the year was used for various purposes. First, significant additions were made to

LO 6 PROBLEM 12-4A STATEMENT OF CASH FLOWS—INDIRECT METHOD

1. Changes in account balances and explanations (in thousands of dollars):

Net Change

Dr. (Cr.) Explanation

Cash (70)

Accounts receivable (85)

Inventory 20

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-57

PROBLEM 12-4A (Continued)

Statement of cash flows:

WABASH CORP.

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

(IN THOUSANDS OF DOLLARS)

Cash Flows from Operating Activities

Net income ……………………………………………………………………………. $ 350

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense ………………………………………………………… 25

Decrease in accounts receivable …………………………………………. 85

Cash Flows from Investing Activities

Sale of land………………………………………………………………………. $ 100

Acquisition of plant and equipment ………………………………………. (250)

Net cash used by investing activities ………………………………………… $(150)

Cash Flows from Financing Activities

Repayment of long-term borrowings …………………………………….. $ (50)

2. Memorandum to the president:

TO: President of Wabash Corp.

FROM: Student’s name

DATE: January 20, 2017

SUBJECT: Cash flows

You recently expressed concern to me regarding the decrease in cash during 2016

12-58 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 12-4A (Concluded)

Although net income on an accrual basis was $350,000, net cash flow from op-

erating activities was even higher, $430,000. However, the favorable cash flow dur-

ing the year was used for various purposes. First, significant additions were made to

LO 8 PROBLEM 12-5A STATEMENT OF CASH FLOWS USING A WORK SHEET—

INDIRECT METHOD (APPENDIX)

1. Statement of cash flows work sheet (all amounts are in thousands of dollars):

Balances Cash Inflows (Outflows)

Accounts 12/31/16 12/31/15 Changes Operating Investing Financing

Cash 140 210 (70)

Accounts Receivable 60 145 (85) 85

Inventory 200 180 20 (20)

Prepayments 15 25 (10) 10

Land 600 700 (100)1 100

Totals 0 0 0 430 (150) (350)

Net increase

(decrease) in cash (70)

1

Sale of land. 5Issuance of common stock.

CHAPTER 12 • THE STATEMENT OF CASH FLOWS 12-59

PROBLEM 12-5A (Continued)

2. Statement of cash flows:

WABASH CORP.

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

(IN THOUSANDS OF DOLLARS)

Cash Flows from Operating Activities

Net income ……………………………………………………………………………. $ 350

Adjustments to reconcile net income to net cash provided

by operating activities:

Depreciation expense ………………………………………………………… 25

Cash Flows from Investing Activities

Sale of land………………………………………………………………………. $ 100

Acquisition of plant and equipment ………………………………………. (250)

Net cash used by investing activities ………………………………………… $(150)

Cash Flows from Financing Activities

Repayment of long-term borrowings …………………………………….. $ (50)

3. Memorandum to the president:

TO: President of Wabash Corp.

FROM: Student’s name

12-60 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 12-5A (Concluded)

Although net income on an accrual basis was $350,000, net cash flow from op-

erating activities was even higher, $430,000. However, the favorable cash flow dur-

ing the year was used for various purposes. First, significant additions were made to

LO 5 PROBLEM 12-6A STATEMENT OF CASH FLOWS—DIRECT METHOD

1. Changes in account balances and explanations (in thousands of dollars):

Net Change

Dr. (Cr.) Explanation

Cash 15

Accounts receivable (50)

Inventory 0

Prepayments 1

Land 100 Purchase (c)