Accounting Information Systems, 10e 41

Factory floor

Order

Key items and

quantities

Shipment

data

Display

shipment data

Sales order

master data

invoice

Invoice

Invoice

1

2 3

Invoices

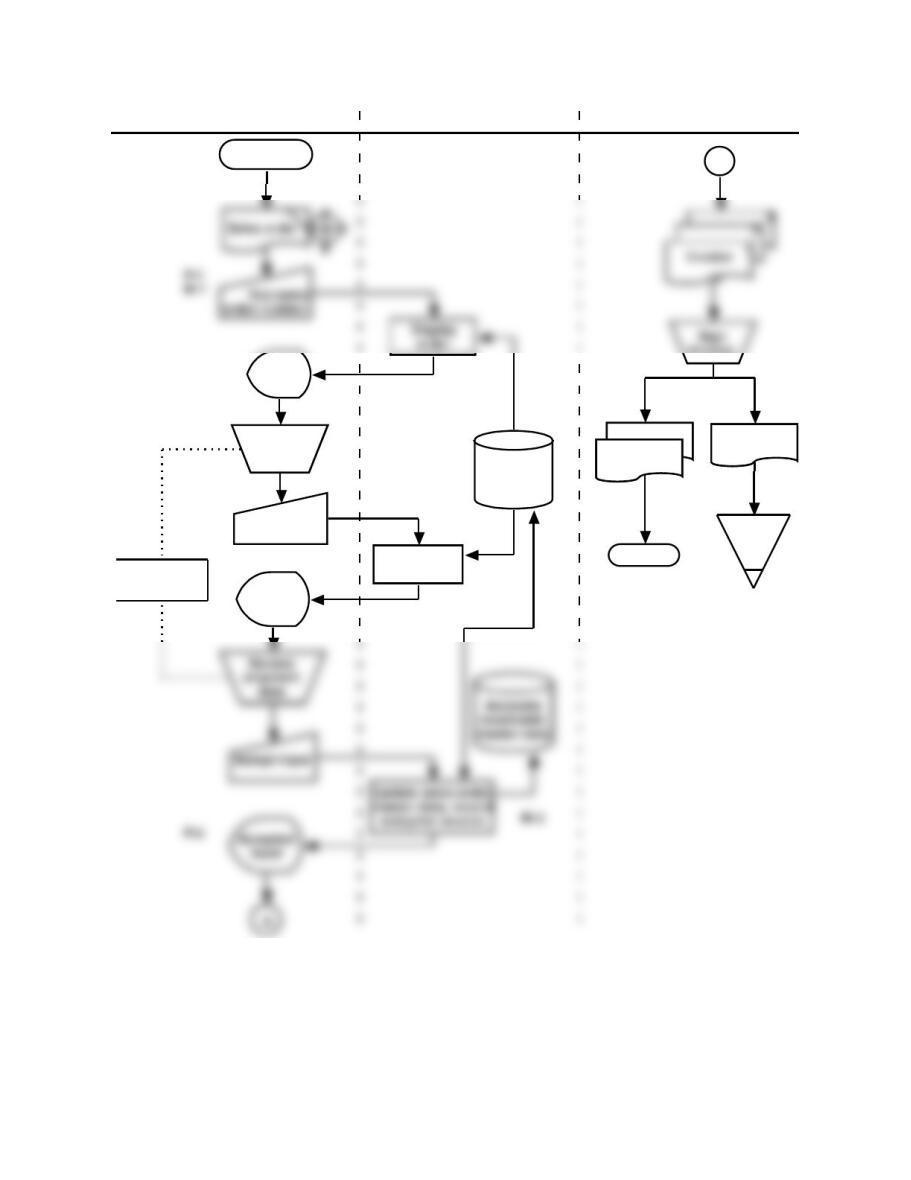

A

Customer

Review order

screen

Error routine

not shown

Shipping department Computer Billing office

A

P-2

P-3

P-4

M-2

FIGURE SM-11.20 Problem 2, Part c Solution—Annotated Systems Flowchart for Impulse

Accessories, Inc. (Billing Process)

42 Solutions for Chapter 11

Impulse Accessories, Inc. (Cash Receipts Process) Solutions (see Note on pg. 8)

P 11-1 ANS. a. Table of Entities and Activities for Impulse Accessories, Inc. (Cash Receipts

Process)

Entities

Para

Activities

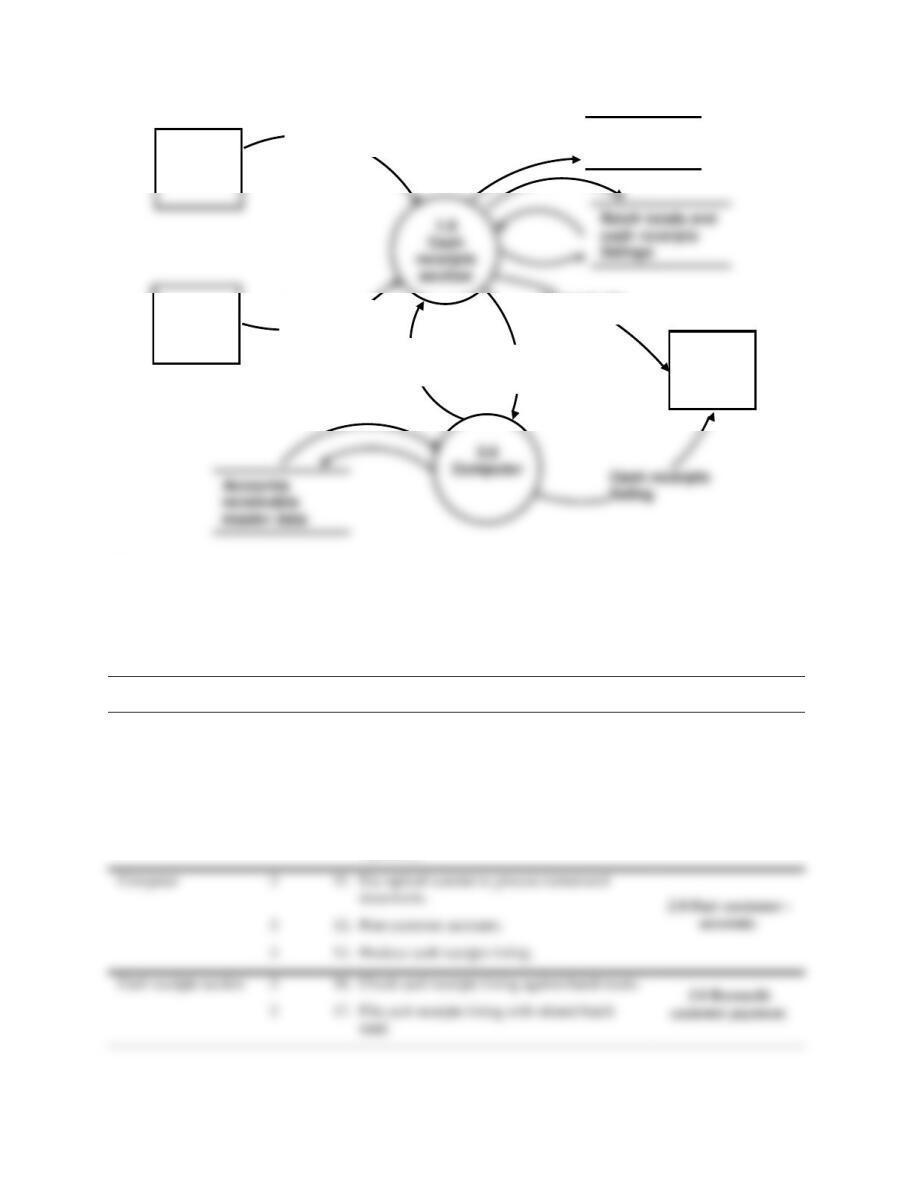

Customer

1

1. Send check and invoice copy 3 (remittance advice [RA]).

Cash receipts section

1

2. Receive payment (check and RA) from customers.

1

3. Compare check amount to RA.

2

9. File batch totals and copy 2 of deposit slip separately.

2

10. Send copy 3 of the deposit slip to Treasurer.

Bank

2

Treasurer

2

IT/Computer

3

11. Use optical scanner to process RAs.

3

12. Post customer accounts.

3

3

3

16. Check cash receipts listing against batch totals.

Customer

Deposit

notice

Payment

FIGURE SM-11.21 Problem 1, Part b Solution—Context Diagram for Impulse Accessories,

Inc. (Cash Receipts Process)

1

4. Enter amount received on RA.

2

5. Batch checks and RAs.

2

7. Prepare deposit slip.

2

8. Deposit checks.

Accounting Information Systems, 10e 43

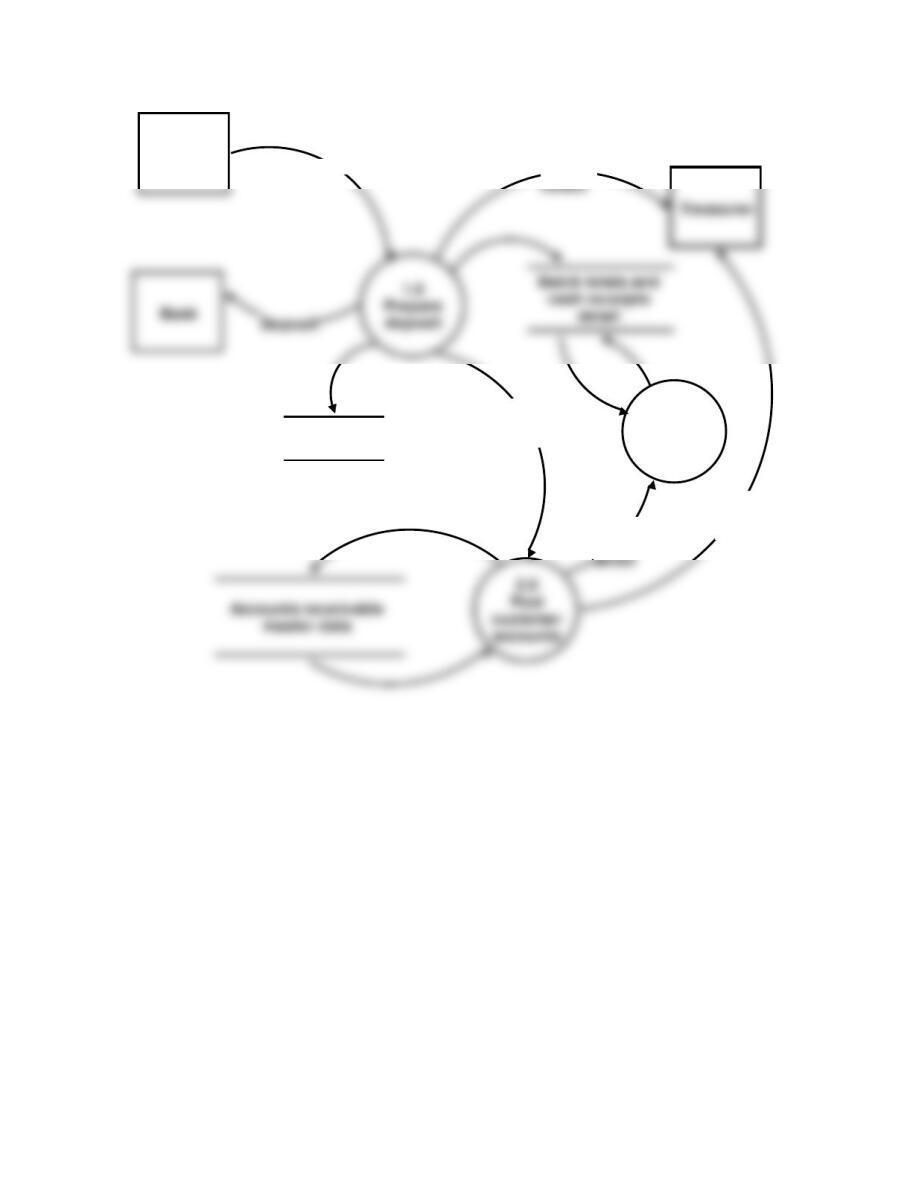

Bank

Customer

Treasurer

Deposit slips

(copy 2)

Deposit slip

(copy 3)

Batched

turnaround

documents

Cash

receipts

listing

Check and

invoice copy 3

Deposit slip

(copy 1)

and checks

FIGURE SM-11.22 Problem 1, Part c Solution—Physical DFD for Impulse Accessories, Inc.

(Cash Receipts Process)

P 11-1 ANS. d. Table of Entities and Activities (Annotated) for Impulse Accessories, Inc.

(Cash Receipts Process)

Entities

Para

Activities

Process

Cash receipts section

1

3. Compare check to RA.

1.0 Prepare deposit.

1

4. Enter amount received on RA.

2

5. Batch checks and RAs.

2

6. Prepare deposit slip.

2

9. File batch totals and copy 2 of deposit slip

separately.

Computer

3

11. Use optical scanner to process turnaround

documents.

3

12. Post customer accounts.

3

16. Check cash receipts listing against batch totals.

44 Solutions for Chapter 11

Customer

3.0

Reconcile

customer

payment

Deposit

record

Deposit

Batched

remittance

advices

Cash

receipts

Cash

receipts

detail

Payment

FIGURE SM-11.23 Problem 1, Part e Solution—Logical DFD for Impulse Accessories, Inc.

(Cash Receipts Process)

Accounting Information Systems, 10e 45

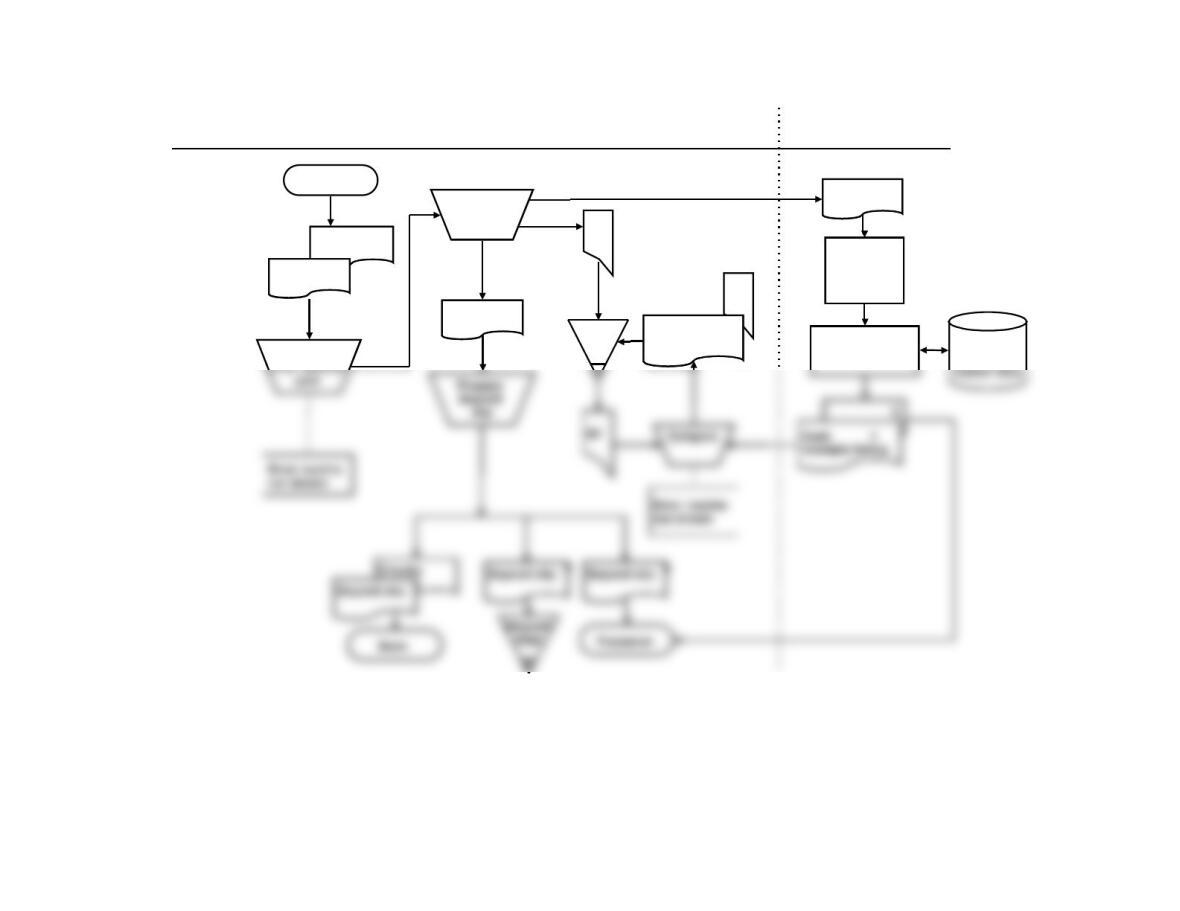

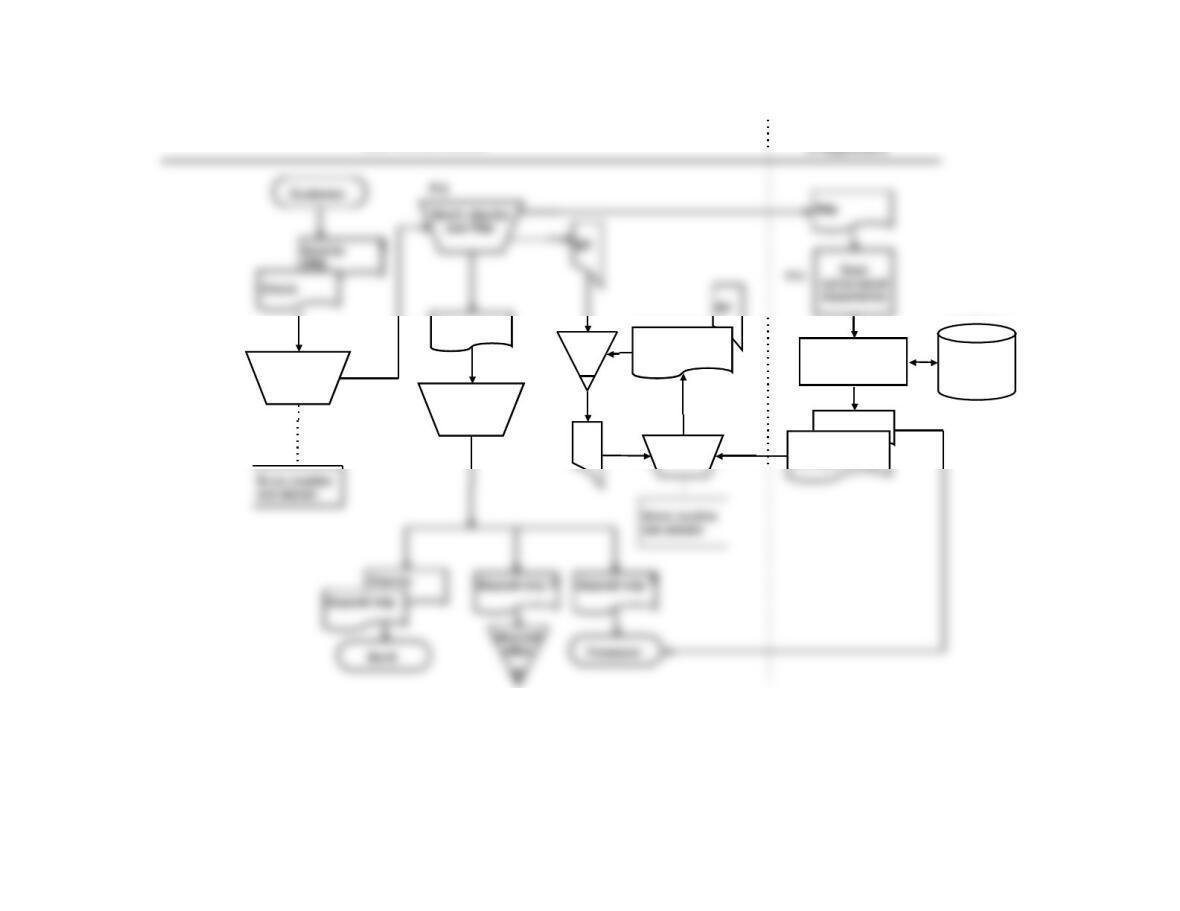

FIGURE SM-11.24 Problem 2, Part a Solution—Systems Flowchart for Impulse Accessories, Inc. (Cash Receipts Process)

Cash receipts section IT Department

Customer

Invoice

(RA)

Check

Compare and

Batch checks

and RAs

Checks

BT

Batch

totals

Cash 1

receipts listing

BT

RAs

Post to customer

accounts Accounts

receivable

Scan

turnaround

documents

3

46 Solutions for Chapter 11

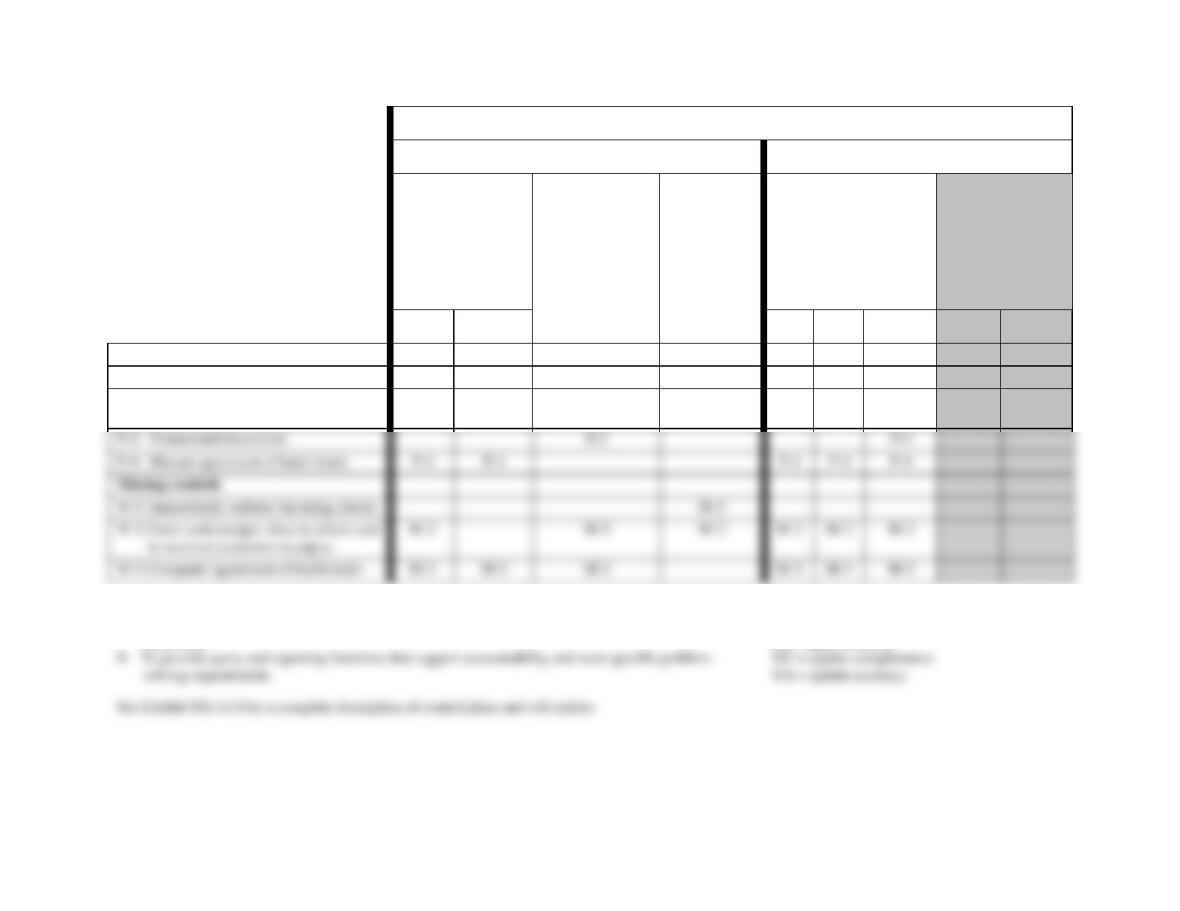

Control Goals of the Fairfield Novelty, Inc. Cash Receipts Business Process

Control Goals of the Operations Process

Control Goals of the Information Process

Ensure

effectiveness of

operations:

Ensure efficient

employment of

resources

(people and

computers)

Ensure

security of

resources

(cash,

accounts

receivable

master data)

For the remittance

advice inputs (i.e., cash

receipts), ensure:

For accounts

receivable master

data, ensure:

Recommended control plans

A

B

IV

IC

IA

UC

UA

Present controls

P-1: Compare check and RA

P-1

P-1

P-1

P-1

P-1

P-2: Immediately separate checks and

remittance advices

P-2

P-2

Possible effectiveness goals include the following:

A – To optimize cash flows by minimizing overdue accounts and reducing the investment in accounts

receivable.

IV = input validity

IC = input completeness

IA = input accuracy

FIGURE SM-11.25 Problem 2, Part b Solution—Control Matrix for Impulse Accessories, Inc. (Cash Receipts Process)

P-3: Turnaround documents

P-3

P-3

P-4: Manual agreement of batch totals

P-4

P-4

P-4

P-4

Missing controls

M-2: Enter cash receipts close to where cash

is received (customer receipts)

M-3

Accounting Information Systems, 10e 47

Exhibit SM-11.4 Problem 2, Part b Solution (Partial)—Explanation of Cell entries for

Control Matrix in Figure SM-11.25

Note: Remittance advice inputs result in immediate updates to accounts receivable master data.

Therefore, we do not show entries for UC or UA.

P-1: Compare check and RA.

Effectiveness goals A and B: This comparison will ensure that, when the RA is

input, the correct account will be updated (goal A) and that the AR data used for

P-2: Immediately separate checks and remittance advices.

Effectiveness goal A: Quick deposit of checks allows for faster investment of

cash.

Security of resources: The checks are separated from the remittance advices and

the checks are deposited quickly. The less time that the RA and the check are

together and the faster the checks are deposited results in less chance that the cash

can be diverted or that lapping can occur.

P-3: Turnaround documents.

Efficient employment of resources: An invoice document, printed by the computer,

is used to capture and input the data for the cash receipt. This is more efficient

than having someone rekey the data.

48 Solutions for Chapter 11

Remittance advice input validity, input completeness, and input accuracy: This

reconciliation of the batch totals will ensure that only legitimate source

documents were input (validity), that all of the batched data was recorded once

and only once (completeness), and that the data was recorded correctly

(accuracy).

M-1: Immediately endorse incoming checks.

M-2: Enter cash receipts close to where cash is received (customer receipts).

Note: We categorize this as missing because the customer payments are sent to the

cash receipts section and then to IT

Effectiveness goal A: The customer payments are not sent directly to the bank, nor

are they entered at cash receipts, which would greatly accelerate cash flow by

eliminating the time required to process those receipts through the Fairfield office

and to the bank.

M-3: Computer agreement of batch totals.

Effectiveness goals A and B: This reconciliation of batch totals will ensure that

when the RA was input, it was for the correct account (goal A) and that the AR

data used for decision making is accurate (goal B).

Accounting Information Systems, 10e 49

Remittance advice input validity, input completeness, and input accuracy: This

reconciliation of the batch totals will ensure that only legitimate source

documents were input (validity), that all of the batched data was recorded once

and only once (completeness), and that the data was recorded correctly

(accuracy).

• As data is entered into the system, we might find programmed edit checks,

populate input screens with master data, and compare input data with master

data. For example, there should be a comparison of the input RA with the

open AR as it is posted to the customer accounts.

• When there are programmed edit checks, manual comparisons, and

reconciliation of batch totals, we might find procedures for rejected inputs.

50 Solutions for Chapter 11

Cash re ceipts section IT Department

Compare and

enter amount

paid

Checks

Prepare

deposit

slip

Batch

totals

C

Cash 1

receipts listing

BT Compare

Post to customer

accounts Accounts

receivable

master data

2

Cash 1

receipts listing

P-1

M-1

M-2

P-4 M-3

FIGURE SM-11.26 Problem 2, Part c Solution—Annotated Systems Flowchart for Impulse Accessories, Inc. (Cash Receipts

Process)

P 11-3 ANS.

1. H: Bank reconciliation can only be effective in detecting fraud if the one who

reconciles does not also handle cash receipts or disbursements. Therefore, the

treasurer and cashier must be segregated (i.e., two different people).

4. B: Selection, hiring, and supervision of billing clerks to ensure that they select

all shipments for billing in a timely manner.

5. K: Plans for physical and logical access to sales order master data to prevent

unauthorized changes to sales order data such as indicating that a shipment

has been billed when it has not.

6. F: Segregate marketing and billing to ensure that processes are authorized by

marketing, a function that is separated from the billing function.

maintenance to ensure the accurate capture of remittance advice data.

P11-4 Output formats may vary by student and package used for the calculations. Below

is a summary of the totals that are expected.

Cycleocity, Inc

Accounts Receivable Aging Report

As of June 30, 20XX

Days Outstanding

Customer Name

Total

0-30

31–60

61–90

>90

Bikes Et Cetera

$6,156.04

$1,920.27

$1,566.51

$0.00

$2,669.26

International Bicycle Sales

2,917.93

1,255.91

363.60

400.69

897.73

Rodebyke & Mopeds

1,174.71

870.24

541.40

Wheelaway Cycle Center

3,478.50

819.55

Total All Customers

$3,838.49