Chapter 11

International Debt Financing

QUESTIONS

1. What are the three main sources of financing for any firm?

2. What is the difference between a centralized and decentralized debt denomination

for a MNC?

Answer: Under a decentralized debt-denomination model, MNCs issue debt in different

3. Will a MNC issuing debt in low–interest rate currencies necessarily lower its cost of

funds? Why?

4. Should a MNC borrow primarily short term when short-term interest rates are

lower than long-term interest rates? Or should it keep the maturity the same but use

a floating-rate loan rather than a fixed-rate loan? Explain.

Answer: First, if short-term interest rates are lower than long-term interest rates, this may

be an indication of impending increases in interest rates. In fact, if the expectations

5. What is financial disintermediation?

6. What are the two main segments of the international bond market, and what types

of regulations apply to them?

7. What is the difference between a foreign bond and a Eurobond?

8. Why might U.S. investors continue to purchase Eurobonds, despite the fact that the

U.S. corporate bond market is well developed?

9. What is a global bond, and what role does the global bond market play in the

blurring of the distinctions in the international bond market?

Chapter 11: International Debt Financing

3

10. What are the differences between a straight bond, a floating-rate note, and a

convertible bond?

11. What is a dual-currency bond?

12. What kind of activities do international banks engage in?

Answer: International banks typically develop a complete line of financial services to

and foreign bonds, which are investment-banking activities.

13. Why is there a need for international banking regulation?

Answer: First, central banks are concerned that without an international regulatory

framework to ensure that an adequate level of capital is maintained in the international

14. What are the differences between credit risk, market risk, and operational risk?

15. What is systemic risk?

16. Which activity would require the largest capital charge under the 1988 Basel

Accord: a loan to another bank or a loan to a large MNC? Would this necessarily be

true under the Basel II rules?

Answer: Under Basel I, claims on other banks received only a 20% weighting, meaning

17. What is VaR?

18. What is the difference between a foreign branch and a subsidiary bank?

19. What is an offshore center?

20. What is the difference between an Edge Act bank and an international banking

facility?

Answer: Edge Act banks are federally chartered subsidiaries of U.S. banks that are

physically located in the United States but are allowed to engage in a full range of

21. What is the difference between a Eurocredit, a Euronote, and a Euro-medium-term

note?

Answer: Eurocredits are typically very large international loans extended by a consortium

or syndicate of banks that share the risk of the loan. Eurocredits are typically issued at

22. Why are Eurocredits not extended by one bank but by a large syndicate of banks?

23. What is the all-in cost of a 5-year loan? What are its main components?

Answer: The all-in-cost (AIC) is the internal rate of return that sets the proceeds from the

24. What is a credit rating? What is a credit spread?

Answer: For credit spread, see the answer to Question 23. The credit spread a company

25. Should corporations issue bonds in countries where they face the lowest credit

spreads? Be very specific about the concept of credit spread you use.

Chapter 11: International Debt Financing

7

PROBLEMS

1. In 1985, R.J. Reynolds (RJR for short) acquired Nabisco Brands and financed the

deal with a variety of financial instruments, including three dual-currency

Eurobonds. The first dual-currency bond, lead-managed by Nikko, raised JPY25

billion (which was equivalent to USD105.5 million at the time of issue). Coupons

were paid in yen, but the required final principal payment was not JPY25 billion

but USD115.956 million. The coupon was 7.75%, even though a comparable fixed–

rate Euroyen bond at that time carried only a 6.375% coupon. The actual 5-year

forward rate at the time was around JPY200/USD.

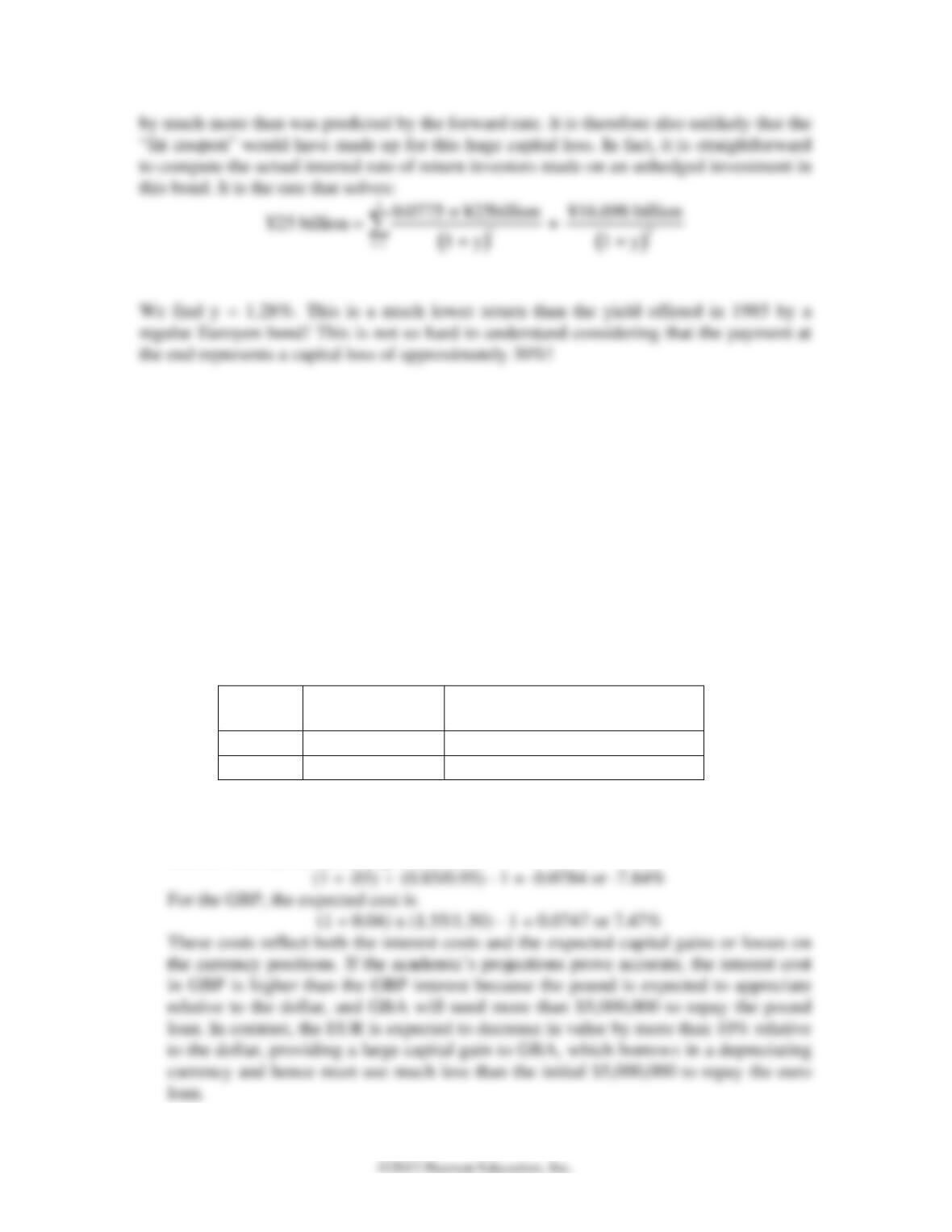

a. Given the “fat” coupon, is this bond necessarily a great deal for the investors?

Answer: No, it isn’t a particularly great deal for the investor because the payment at the

end is worth substantially less than the face amount of the bond. To see this, note that the

b. At maturity, in August 1990, the exchange rate was actually JPY144/USD. Was

the bond a good deal for investors?

Answer: We need to calculate the return to investors if the investors were unhedged.

Investors received

Chapter 11: International Debt Financing

8

2. GBA Company wishes to raise $5,000,000 with debt financing. The funds will be

repaid with interest in 1 year. The treasurer of GBA Company is considering three

sources:

i. Borrow USD from Citibank at 1.50%

ii. Borrow EUR from Deutsche Bank at 3.00%

iii. Borrow GBP from Barclays at 4.00%

If the company borrows in euros or British pounds, it will not cover the foreign

exchange risk; that is, it will change foreign currency for dollars at today’s spot rate

and buy foreign currency back 1 year later at the spot rate prevailing then. The

GBA Company has no operations in Europe.

A representative of GBA contacts a local academic to provide projections of the spot

rates 1 year in the future. The academic comes up with the following table:

Currency

Spot Rate

Projected Rate 1 Year in the

Future

USD/GBP

1.5

1.55

USD/EUR

0.95

0.85

a. What is the expected interest rate cost for the loans in EUR and GBP?

Answer: For the EUR, the expected cost is

Chapter 11: International Debt Financing

9

b. What are the projected USD/GBP rate and USD/EUR rate for which the

expected interest costs would be the same for the three loans?

Answer: These are the exchange rates that satisfy Uncovered Interest Rate Parity,

c. Should the company borrow in the currency with the lowest interest rate cost?

Why or why not? Would your answer change if GBA did generate cash flows in

the United Kingdom and continental Europe?

Answer: When using the forecasts of the academic, the lowest interest cost occurs in

EUR. However, the academic’s forecast is quite far away from the “break–even” rates

3. FE Company wishes to raise $1,000,000 with debt financing. The treasurer of FE

Company considers two possible instruments:

i. A 2-year floating-rate note at 1% above 1-year dollar LIBOR on which interest

is paid once a year

ii. A 2-year bond with an interest rate of 5%

Currently, the dollar LIBOR is 1.50%.

a. Is it obvious which security the Treasurer should pick?

4.50%. Which security has the lowest expected AIC if borrowing fees are similar

for the two instruments?

4. K3 Company wants to borrow $100 million for 5 years. Investment bankers propose

to either do a syndicated Eurocredit or issue a Eurobond. The Eurocredit would be

denominated in dollars, but the Eurobond would be denominated in different

currencies for different markets (these issues are called tranches):

Terms:

Syndicated Eurocredit

Amount:

USD100 million

Upfront fees:

USD1.25%

Interest rate:

Interest payable every 6 months; LIBOR plus 1.00%

Terms:

Eurobond

Tranche 1:

USD 50 million, Interest rate: 3.50%

Tranche 2:

¥ 5,952 million (equivalent of USD50 million), Interest rate 1.5%

a. What are the net proceeds in USD for K3 for the Eurocredit loan?

b. Assuming that the 6-month LIBOR in USD is currently at 2.00%, what is the

effective annual interest cost for K3 for the first 6 months of the loan?

Chapter 11: International Debt Financing

11

c. Compute an effective annualized interest rate cost (all-in cost) for the USD

tranche of the Eurobond.

d. What information would you need to obtain the dollar all-in cost of the yen

tranche?

e. What elements would you take into account to choose between the two

possibilities?

Answer: With all the information given above (interest rate costs, loan issuance costs,

and information on yen conversion rates); we can compute the AICs on the two

5. Suppose Intel wishes to raise USD1 billion and is deciding between a domestic dollar

bond issue and a Eurobond issue. The U.S. bond can be issued at a 5-year maturity

with a coupon of 4.50%, paid semiannually. The underwriting, registration, and

other fees total 1.00% of the issue size. The Eurobond carries a lower annual coupon

of 4.25%, but the total costs of issuing the bond runs to 1.25% of the issue size.

Which loan has the lowest all-in cost?

Chapter 11: International Debt Financing

12

The U.S. bond is special as it features semi-annual coupon payments (of 4.5% / 2 =

1. US Bond

Half-Year

Dollar Cash Flows

0

100 – 1.00 = 99.00

1

2

9

1

2

3

4

5

For the Eurobond, the computations are more standard:

6. Web Question: In 2010, Coca-Cola FEMSA, a bottler in Mexico, issued a $500

million 10-year bond. Look up more details about this issue. What type of bond is

it? How was it rated? What is the credit spread associated with the bond?

The FEMSA Web site, www.femsa.com/en/assets/007/18878.pdf, provides the following

2. Eurobond

Year

Euro Cash Flows

0

100 – 1.25 = 98.75