CHAPTER 11 • STOCKHOLDERS’ EQUITY 11-21

PROBLEM 11-5 (Concluded)

2. The Stockholders’ Equity category as of December 31, 2016, would appear as

follows:

FREDERIKSEN INC.

PARTIAL BALANCE SHEET

DECEMBER 31, 2016

Stockholders’ Equity

Preferred stock, $80 par, 7%, 3,000 shares issued

and outstanding ………………………………………………………………… $ 240,000

3. A stock dividend results in the capitalization of part of the Retained Earnings ac-

count. The value of the shares issued in the stock dividend is deducted from the Re-

tained Earnings account and added to the Capital Stock account (and the Additional

Paid-In Capital account for small stock dividends). The number of outstanding

11-22 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 8 PROBLEM 11-6 STATEMENT OF STOCKHOLDERS’ EQUITY

Preferred Common Paid-In Treasury Retained

Stock Stock Capital Stock Earnings

Balance, January 1 $ 0 $ 0 $ 0 $ 0 $ 0

Sale of preferred stock 50,000 10,000

Sale of common stock 20,000 300,000

Issuance of common

Explanations:

1/10 Preferred stock: 500 × $100 par = $50,000 increase

Additional paid-in capital: 500 × ($120 – $100) = $10,000 increase

1/10 Common stock: 4,000 × $5 = $20,000 increase

Additional paid-in capital: 4,000 × ($80 – $5) = $300,000 increase

1/20 Common stock: 1,000 × $5 par = $5,000 increase

Additional paid-in capital: 1,000 × ($70 – $5) = $65,000 increase

CHAPTER 11 • STOCKHOLDERS’ EQUITY 11-23

LO 8 PROBLEM 11-7 SOUTHWEST AIRLINES’ COMPREHENSIVE INCOME

1. Southwest Airlines has several items that were not included in the net income

amount but are included on the statement of comprehensive income. The effect of

2. While comprehensive income would show all sources of income for the period, these

numbers could lead readers to believe this is an ordinary result of operations. Some

items are considered to be “paper” gains or losses; these adjustments are not pre-

sented on the income statement because they are unrealized. These adjustments

LO 10 PROBLEM 11-8 EFFECTS OF STOCKHOLDERS’ EQUITY TRANSACTIONS ON

STATEMENT OF CASH FLOWS

Cash flows from financing activities:

Issuance of preferred stock (500 × $120) ………………………………….. $ 60,000

Issuance of common stock (4,000 × $80) ………………………………….. 320,000

Purchase of treasury stock (500 × $60) …………………………………….. (30,000)

Reissuance of treasury stock (100 × $65)………………………………….. 6,500

Net cash flow from financing activities ………………………………………. $356,500

The following transactions would not appear in the Financing Activities section of the

11-24 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

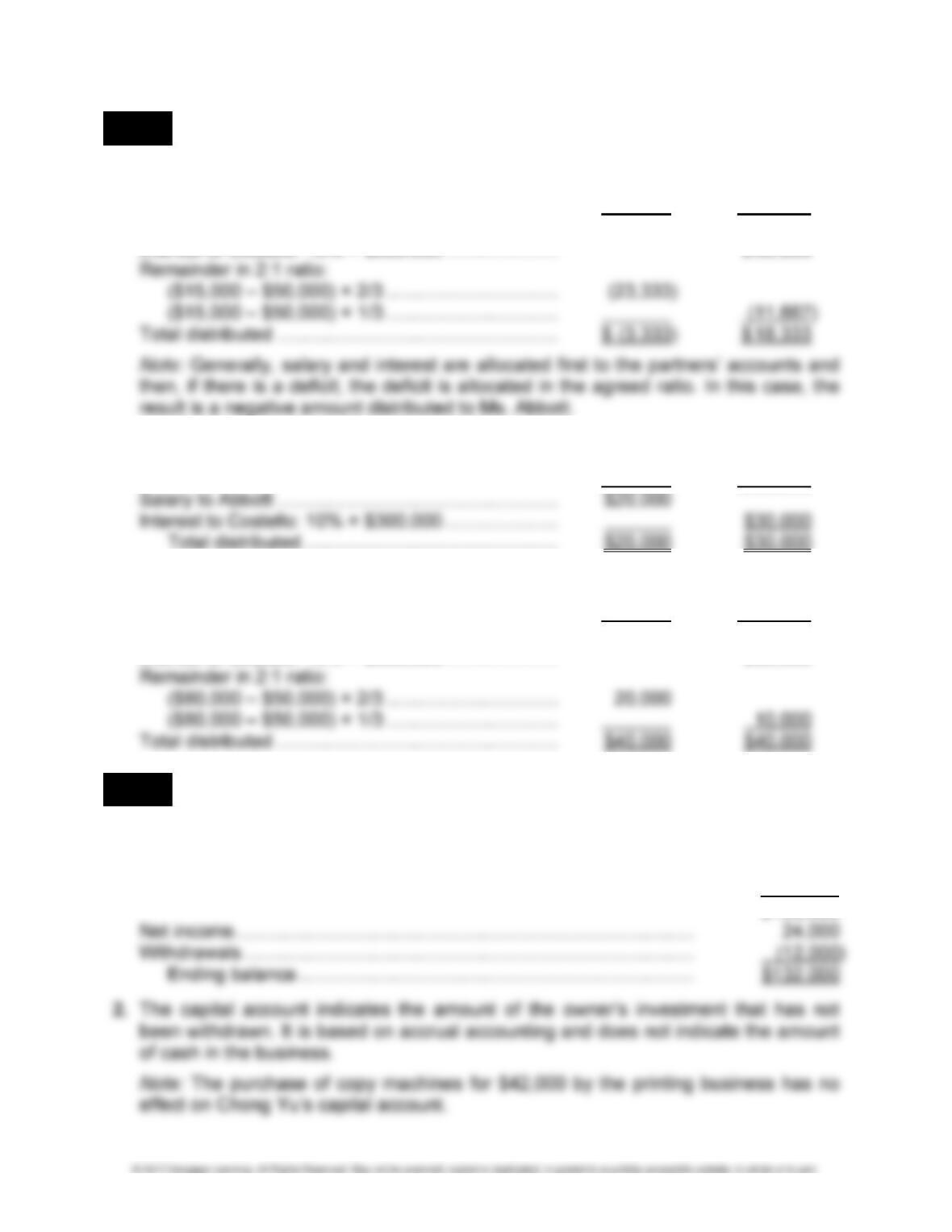

LO 11 PROBLEM 11-9 INCOME DISTRIBUTION OF A PARTNERSHIP (APPENDIX)

1. If income is $15,000, it should be distributed as follows:

Abbott

Costello

Salary to Abbott ……………………………………………… $ 20,000

Interest to Costello: 10% × $300,000 …………………. $ 30,000

2. If income is $50,000, it should be distributed as follows:

Abbott

Costello

3. If income is $80,000, it should be distributed as follows:

Abbott

Costello

Salary to Abbott ……………………………………………… $20,000

Interest to Costello: 10% × $300,000 …………………. $30,000

LO 11 PROBLEM 11-10 SOLE PROPRIETORSHIPS (APPENDIX)

1. The balance of the owner’s capital account can be calculated as follows:

Beginning balance …………………………………………………………………. $ 0

Investments by owner …………………………………………………………….. 120,000

$ 120,000

CHAPTER 11 • STOCKHOLDERS’ EQUITY 11-25

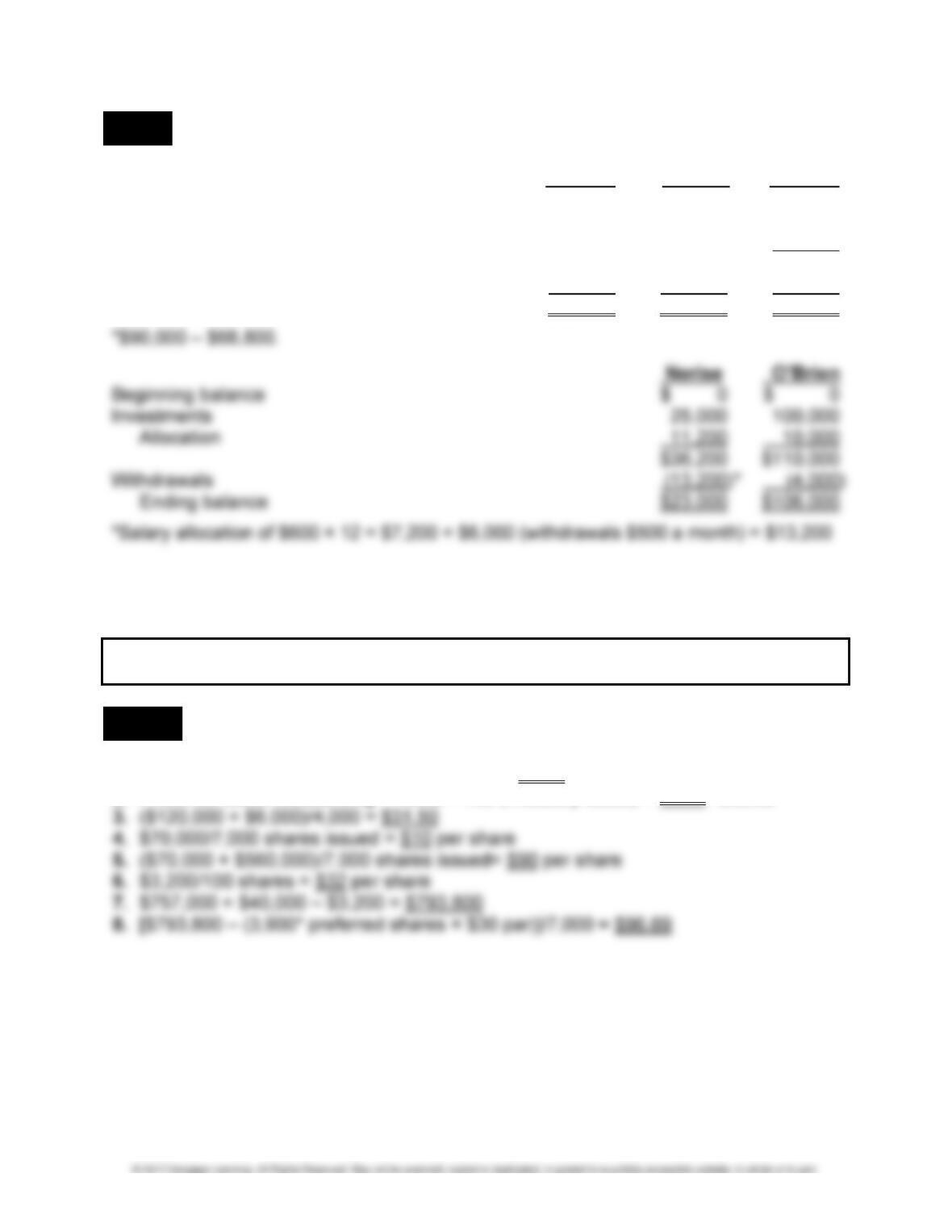

LO 11 PROBLEM 11-11 PARTNERSHIPS (APPENDIX)

Allocation: Nerise

O’Brien Total

Amount to be allocated $21,200*

Salary $ 7,200

Interest ($100,000 × 6%) $ 6,000 13,200

Remainder to allocate $ 8,000

Balance of equity 4,000 4,000 8,000

$11,200 $10,000 $ 0

MULTI-CONCEPT PROBLEMS

LO 1,4 PROBLEM 11-12 ANALYSIS OF STOCKHOLDERS’ EQUITY

1. Preferred Stock Issued = $120,000/$30 par = 4,000 shares issued

2. Preferred Stock Outstanding = 4,000 – 100 (Treasury Stock) = 3,900* shares

11-26 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 3,4,7 PROBLEM 11-13 EFFECTS OF STOCKHOLDERS’ EQUITY TRANSACTIONS ON

THE BALANCE SHEET

1. Assets = Liabilities + Stockholders’ Equity

a. +500,000 +100,000

+400,000

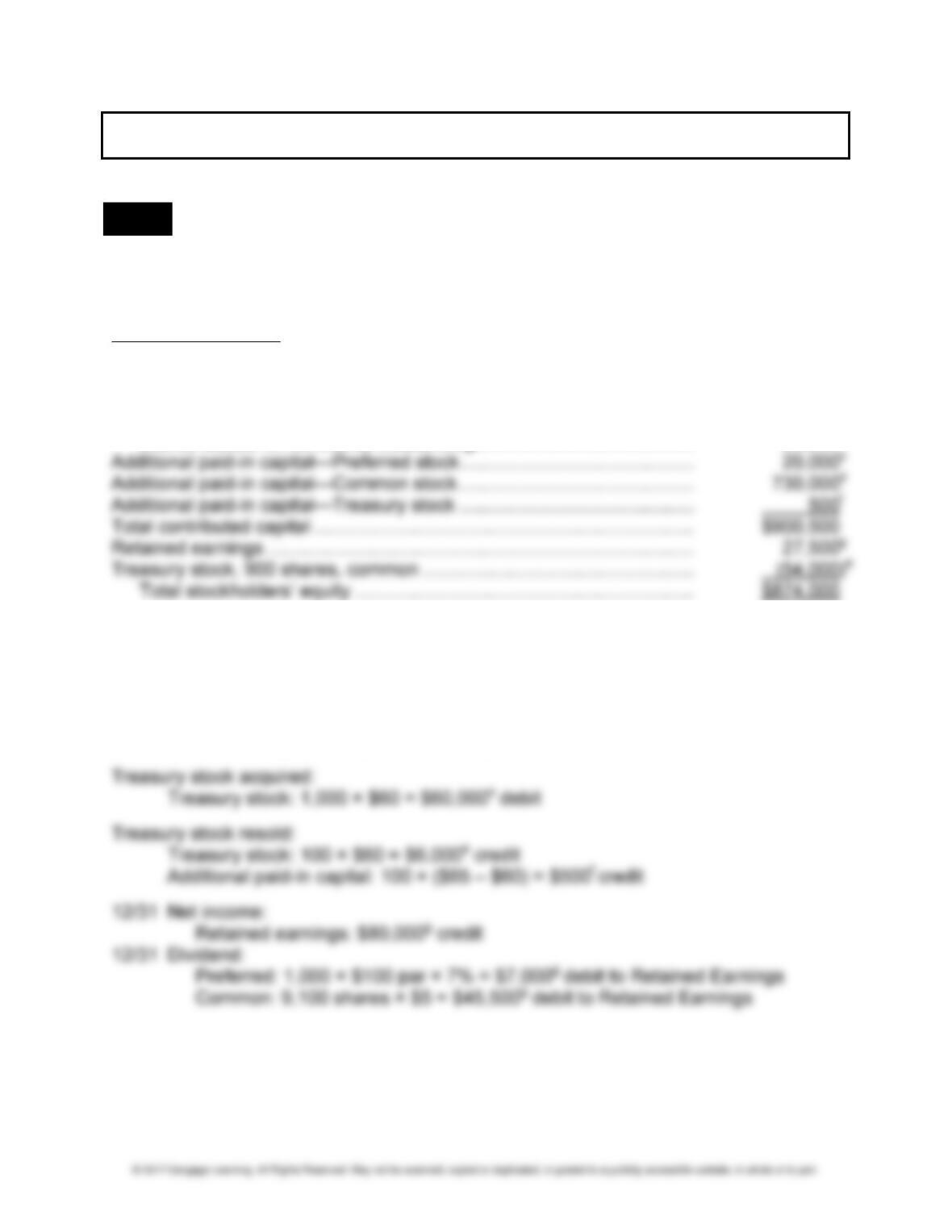

2. HORTON INC.

PARTIAL BALANCE SHEET

DECEMBER 31, XXXX

Stockholders’ Equity

Common stock, 2,000,000 authorized, 220,000 issued,

3. Note: The company is authorized to issue 2,000,000 shares of common stock, $0.50

par value. At the end of the year, 220,000 shares are issued; however, only 218,000

CHAPTER 11 • STOCKHOLDERS’ EQUITY 11-27

LO 1,4 PROBLEM 11-14 STOCKHOLDERS’ EQUITY SECTION OF THE BALANCE SHEET

1. IVES INC.

BALANCE SHEET

AS OF XXXX

Assets

Cash ……………………………………………………………………………………. $ 3,500

Account receivable …………………………………………………………………. 5,000

Plant, property, and equipment ………………………………………………… 108,000

Total assets ……………………………………………………………………… $116,500

2. The Retained Earnings account has a debit balance because the accumulated earn-

ings of the company represent a net loss and/or dividends paid out have exceeded

the cumulative earnings.

11-28 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

ALTERNATE PROBLEMS

LO 1 PROBLEM 11-1A STOCKHOLDERS’ EQUITY CATEGORY

KEBLER COMPANY

PARTIAL BALANCE SHEET

DECEMBER 31, 2016

Stockholders’ Equity

Preferred stock, $100 par, 7%, 2,000 shares authorized,

1,000 shares issued ……………………………………………………………….. $100,000a

Common stock, $5 par, 20,000 shares authorized, 10,000

shares issued, 9,100 shares outstanding …………………………………… 50,000b

1/10 Preferred stock: 1,000 × $100 par = $100,000a credit

Additional paid-in capital: 1,000 × ($120 – $100) = $20,000c credit

1/10 Common stock: 8,000 × $5 = $40,000 creditb

Additional paid-in capital: 8,000 × ($80 – $5) = $600,000d credit

1/20 Common stock: 2,000 × $5 par = $10,000 creditb

Additional paid-in capital: 2,000 × ($70 – $5) = $130,000d credit

CHAPTER 11 • STOCKHOLDERS’ EQUITY 11-29

LO 2 PROBLEM 11-2A EVALUATING ALTERNATIVE INVESTMENTS

1. Common stock—dividends become an obligation of the company after they are de-

clared. Prior to the declaration, the company is not obligated to pay dividends to

common shareholders.

2. Rob should invest in the common stock because the return is greatest. Rob must be

aware, however, that the risk is also the greatest. If the company fails to perform as

LO 5 PROBLEM 11-3A DIVIDENDS FOR PREFERRED AND COMMON STOCK

1. Preferred Stock Common Stock

$200,000 × 8% = $16,000 $118,000 – $16,000 = $102,000

Per share: $16,000/2,000 = $8.00 $102,000/40,000 = $2.55

LO 6 PROBLEM 11-4A EFFECT OF STOCK DIVIDEND

1. The statement should include the following points:

a. A stock dividend does not change the total stockholders’ equity amount.

11-30 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 11-4A (Concluded)

2. The statement to the stockholders should stress the following points:

a. Each stockholder has the same proportionate ownership of the company after

the dividend as before the dividend.

LO 7 PROBLEM 11-5A DIVIDENDS AND STOCK SPLITS

1. Mar. 1 Cash dividends increase (or Retained Earnings decreases) and total

stockholders’ equity decreases.

Apr. 1 Total stockholders’ equity remains unchanged.

Sept. 1 Retained Earnings and total stockholders’ equity decrease by $7,560

[(10,000 + 800) × $0.70].

Oct. 1 Total stockholders’ equity does not change.

CHAPTER 11 • STOCKHOLDERS’ EQUITY 11-31

PROBLEM 11-5A (Concluded)

2. SVENBERG INC.

PARTIAL BALANCE SHEET

DECEMBER 31, 2016

Stockholders’ Equity

Preferred stock, $80 par, 8%, 1,000 shares issued

and outstanding ………………………………………………………………… $ 80,000

Common stock, $3.33 par, 32,400a shares issued

and outstanding ………………………………………………………………… 108,000b

3. A stock dividend results in the capitalization of part of the Retained Earnings ac-

count. The value of the shares issued in the stock dividend is deducted from the Re-

tained Earnings account and added to the Capital Stock account (and the Additional

11-32 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

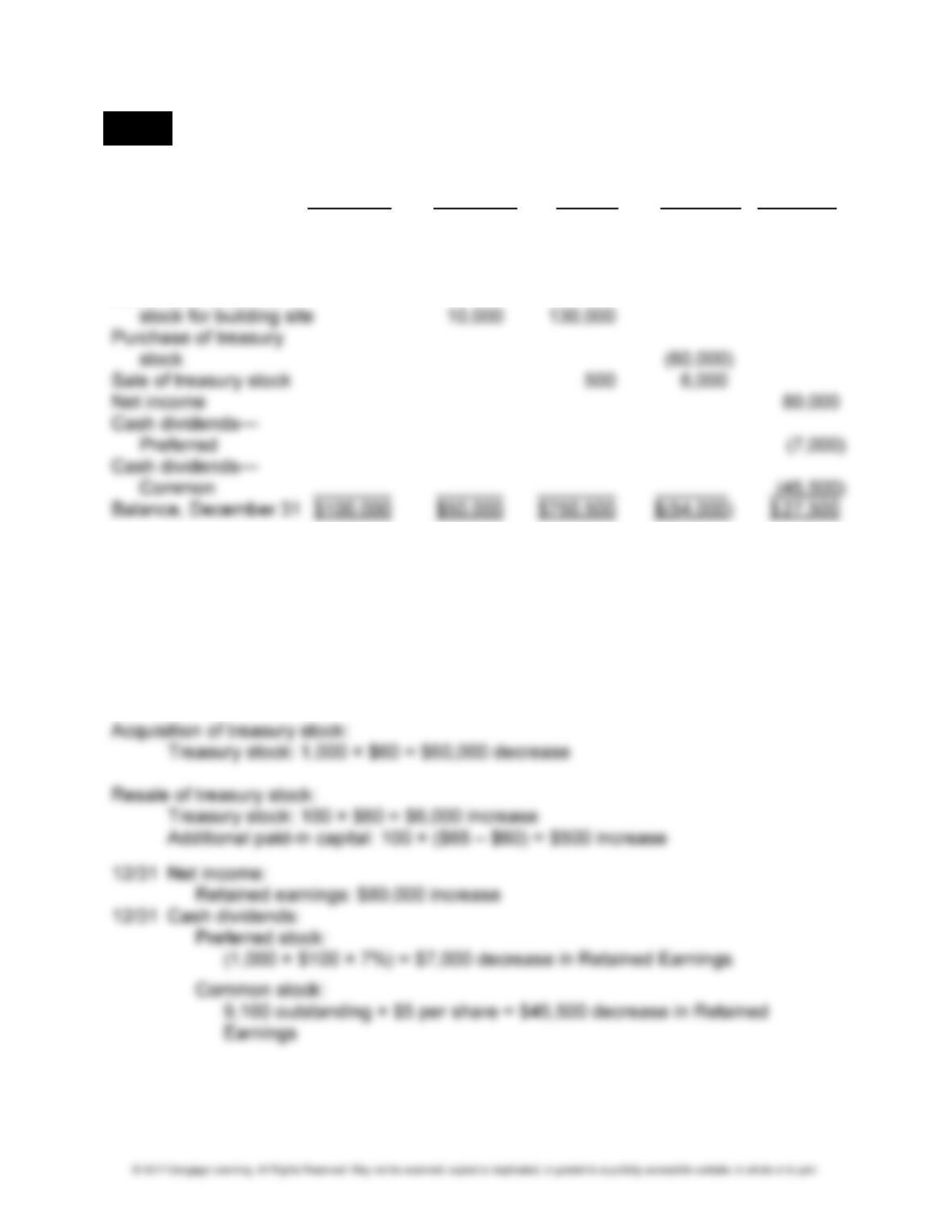

LO 8 PROBLEM 11-6A STATEMENT OF STOCKHOLDERS’ EQUITY

Preferred Common Paid-In Treasury Retained

Stock Stock Capital Stock Earnings

Balance, January 1 $ 0 $ 0 $ 0 $ 0 $ 0

Sale of preferred stock 100,000 20,000

Sale of common stock 40,000 600,000

Issuance of common

Explanations:

1/10 Preferred stock: 1,000 × $100 par = $100,000 increase

Additional paid-in capital: 1,000 × ($120 – $100) = $20,000 increase

1/10 Common stock: 8,000 × $5 = $40,000 increase

Additional paid-in capital: 8,000 × ($80 – $5) = $600,000 increase

1/20 Common stock: 2,000 × $5 par = $10,000 increase

Additional paid-in capital: 2,000 × ($70 – $5) = $130,000 increase