Chapter 11

Current Liabilities and Payroll

Review Questions

1. What are the three main characteristics of liabilities?

The three main characteristics of liabilities are:

2. What is a current liability? Provide some examples of current liabilities.

Current liabilities must be paid with cash or with goods and services within one year or within the

3. How is sales tax recorded? Is it considered an expense of a business? Why or why not?

Sales tax is recorded as a liability when it is charged to the customer; it is usually calculated as a

4. How do unearned revenues arise?

Unearned revenue arises when a business has received cash in advance of providing goods or

5. What do short-term notes payable represent?

6. Coltrane Company has a $5,000 note payable that is paid in $1,000 installments over five years.

How would the portion that must be paid within the next year be reported on the balance sheet?

The principal amount that will be paid within one year will be reported in the current liabilities as

current portion of notes payable.

7. What is the difference between gross pay and net pay?

Gross pay is the total amount of salary, wages, commissions, and bonuses earned by the employee

8. List the required employee payroll withholding deductions, and provide the tax rate for each.

Required payroll withholding deductions are:

Withholding Deductions

Tax Rate

Federal, State and Local Income Tax

The amount withheld depends on the

employee’s gross pay and the

number of withholding allowances

9. How might a business use a payroll register?

Many companies use a payroll register to help summarize the earnings, withholdings, and net pay for

each employee.

10. What payroll taxes is the employer responsible for paying?

11. What are the two main controls for payroll? Provide an example of each.

There are two main controls for payroll: controls for efficiency and controls to safeguard payroll

disbursements.

12. When do businesses record warranty expense, and why?

13. What is a contingent liability? Provide some examples of contingencies.

14. Curtis Company is facing a potential lawsuit. Curtis’s lawyers think that it is reason- ably possible

that it will lose the lawsuit. How should Curtis report this lawsuit?

Contingencies that are reasonably possible have more chance of occurring but are not likely. A

reasonably possible contingency should be described in the notes to the financial statements.

15. How is the times-interest-earned ratio calculated, and what does it evaluate?

The times-interest-earned ratio is calculated as earnings before interest and taxes or EBIT (Net

Short Exercises

For all payroll calculations, use the following tax rates and round amounts to the nearest cent.

Employee: OASDI: 6.2% on first $117,000 earned; Medicare: 1.45% up to $200,000, 2.35% on

earnings above $200,000.

Employer: OASDI: 6.2% on first $117,000 earned; Medicare: 1.45%; FUTA: 0.6% on first

$7,000 earned; SUTA: 5.4% on first $7,000 earned.

S11-1 Determining current versus long-term liabilities

Learning Objective 1

Rios Raft Company had the following liabilities.

a. Accounts Payable

b. Note Payable due in 3 years

c. Salaries Payable

d. Note Payable due in 6 months

e. Sales Tax Payable

f. Unearned Revenue due in 8 months

g. Income Tax Payable

Determine whether each liability would be considered a current liability (CL) or a long-term liability

(LTL).

SOLUTION

a.

current liability (CL)

long-term liability (LTL)

c.

current liability (CL)

current liability (CL)

e.

current liability (CL)

current liability (CL)

current liability (CL)

S11-2 Recording sales tax

Learning Objective 1

On July 5, Feather Company recorded sales of merchandise inventory on account, $20,000. The sales

were subject to sales tax of 9%. On August 15, Feather Company paid $1,200 of sales tax to the state.

Requirements

1. Journalize the transaction to record the sale on July 5. Ignore cost of goods sold.

2. Journalize the transaction to record the payment of sales tax to the state.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

July 5

Accounts Receivable

21,800

Accounts and Explanation

Debit

Credit

S11-3 Recording unearned revenue

Learning Objective 1

On June 1, Guitar Magazine collected cash of $51,000 on future annual subscriptions starting on July 1.

Requirements

1. Journalize the transaction to record the collection of cash on June 1.

2. Journalize the transaction required at December 31, the magazine’s year-end, assuming no revenue

earned has been recorded. (Round adjustment to the nearest whole dollar.)

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

June 1

Cash

51,000

Date

Debit

Credit

Dec. 31

Unearned Revenue

25,500

S11-4 Accounting for a note payable

Learning Objective 1

On December 31, 2015, Franklin purchased $7,000 of merchandise inventory on a one-year, 11% note

payable. Franklin uses a perpetual inventory system.

Requirements

1. Journalize the company’s purchase of merchandise inventory on December 31, 2015.

2. Journalize the company’s accrual of interest expense on June 30, 2016, its fiscal year-end.

3. Journalize the company’s payment of the note plus interest on December 31, 2016.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2015

Dec. 31

Merchandise Inventory

7,000

Date

Debit

Credit

Jun. 30

Interest Expense ($7,000 × 0.11 × 6/12)

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2016

Dec. 31

Notes Payable

7,000

Interest Expense ($7,000 × 0.11 × 6/12)

Interest Payable

S11-5 Determining current portion of long-term note payable

Learning Objective 1

On January 1, Garland Company purchased equipment of $120,000 with a long-term note payable. The

debt is payable in annual installments of $24,000 due on December 31 of each year. At the date of

purchase, how will Garland Company report the note payable?

SOLUTION

S11-6 Computing and journalizing an employee’s total pay

Learning Objective 2

Jenna Lindsay works at College of Boston and is paid $40 per hour for a 40-hour workweek and time-

and-a-half for hours above 40.

Requirements

1. Compute Lindsay’s gross pay for working 54 hours during the first week of February.

2. Lindsay is single, and her income tax withholding is 10% of total pay. Lindsay’s only payroll

deductions are payroll taxes. Compute Lindsay’s net (take-home) pay for the week. Assume

Lindsay’s earnings to date are less than the OASDI limit.

3. Journalize the accrual of salaries and wages expense and the payments related to the employment of

Jenna Lindsay.

SOLUTION

Requirement 1

Straight-time pay for 40 hours ($40 × 40 hours)

$ 1,600

Overtime pay for 14 hours: 14 × $40 × 1.5

Gross Pay

$ 2,440

Gross pay

Withholding deductions:

Employee income tax (10%)

Employee OASDI tax (6.2%)

Employee Medicare tax (1.45%)

Total withholdings

Net (take-home) pay

S11-6, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Wages Expense

2,440.00

Employee Income Taxes Payable

244.00

151.28

Wages Payable

2,009.34

S11-7 Computing payroll amounts considering FICA tax ceilings

Learning Objective 2

Lori Waverly works for MRK all year and earns a monthly salary of $11,700. There is no overtime pay.

Lori’s income tax withholding rate is 20% of gross pay. In addition to payroll taxes, Lori elects to

contribute 4% monthly to United Way. MRK also deducts $125 monthly for co-payment of the health

insurance premium. As of September 30, Lori had $114,900 of cumulative earnings.

Requirements

1. Compute Lori’s net pay for October.

2. Journalize the accrual of salaries expense and the payments related to the employment of Lori

Waverly.

SOLUTION

Requirement 1

Gross pay

$ 12,000.00

Withholding deductions:

Employee income tax (20%)

Employee OASDI tax (6.2%)*

Employee Medicare tax (1.45%)

Employee health insurance

Employee contribution to United Way (4%)

Total withholdings

Net (take-home) pay

*Calculation of tax for OASDI

Employee earnings subject to tax

Employee earnings prior to the current month

Current pay subject to tax

Tax rate

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Oct. 31

Salaries Expense

12,000.00

Employee Income Taxes Payable

2,400.00

8,263.00

8,263.00

S11-8 Computing and journalizing the payroll expense of an employer

Learning Objective 2

Orchard Company has monthly salaries of $10,000. Assume Orchard pays all the standard payroll taxes

and no employees have reached the payroll tax limits. Journalize the accrual and payment of employer

payroll taxes for Orchard Company.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Payroll Tax Expense

1,365

FICA—OASDI Taxes Payable

(6.2% × $10,000)

620

(0.6% × $10,000)

540

Federal Unemployment Taxes Payable

State Unemployment Taxes Payable

Payment of payroll taxes

S11-9 Computing bonus payable

Learning Objective 3

On December 31, Peterson Company estimates that it will pay its employees a 3% bonus on $62,000 of

net income after deducting the bonus. The bonus will be paid on January 15 of the next year.

Requirements

1. Journalize the December 31 transaction for Peterson.

2. Journalize the payment of the bonus on January 15.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Employee Bonus Expense

1,805.83

Employee Bonus Payable

S11-9, cont.

Requirement 2

S11-10 Journalizing vacation benefits

Learning Objective 3

Roy Industries has eight employees. Each employee earns two vacation days a month. Roy pays each

employee a weekly salary of $1,000 for a five-day workweek.

Requirements

1. Determine the amount of vacation expense for one month.

2. Journalize the entry to accrue the vacation expense for the month.

SOLUTION

Requirement 1

Employees

8

Weekly salary

$1,000

Total amount to accrue 16 days times $200 per day = $3,200 for one month

Requirement 2

S11-11 Accounting for warranty expense and warranty payable

Learning Objective 3

Hipster Corrector guarantees its snowmobiles for three years. Company experience indicates that

warranty costs will be approximately 3% of sales.

Assume that the Hipster dealer in Colorado Springs made sales totaling $350,000 during 2016. The

company received cash for 20% of the sales and notes receivable for the remainder. Warranty payments

totaled $8,000 during 2016.

Requirements

1. Record the sales, warranty expense, and warranty payments for the company. Ignore cost of goods

sold.

2. Post to the Estimated Warranty Payable T-account. At the end of 2016, how much in Estimated

Warranty Payable does the company owe? Assume the Estimated Warranty Payable is $0 on January

1, 2016.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Cash (20% × $350,000)

70,000

Notes Receivable (80% × $350,000)

280,000

Warranty Expense (3% × $350,000)

10,500

Estimated Warranty Payable

10,500 Accrual

2,500 Bal.

S11-12 Accounting treatment for contingencies

Learning Objective 4

Fernandez Motors, a motorcycle manufacturer, had the following contingencies.

a. Fernandez estimates that it is reasonably possible but not likely that it will lose a current lawsuit.

Fernandez’s attorneys estimate the potential loss will be $3,200,000.

b. Fernandez received notice that it was being sued. Fernandez considers this lawsuit to be frivolous.

c. Fernandez is currently the defendant in a lawsuit. Fernandez believes it is likely that it will lose the

lawsuit and estimates the damages to be paid will be $60,000.

Determine the appropriate accounting treatment for each of the situations Fernandez is facing.

SOLUTION

Situation

Appropriate accounting treatment

S11-13 Computing times-interest-earned ratio

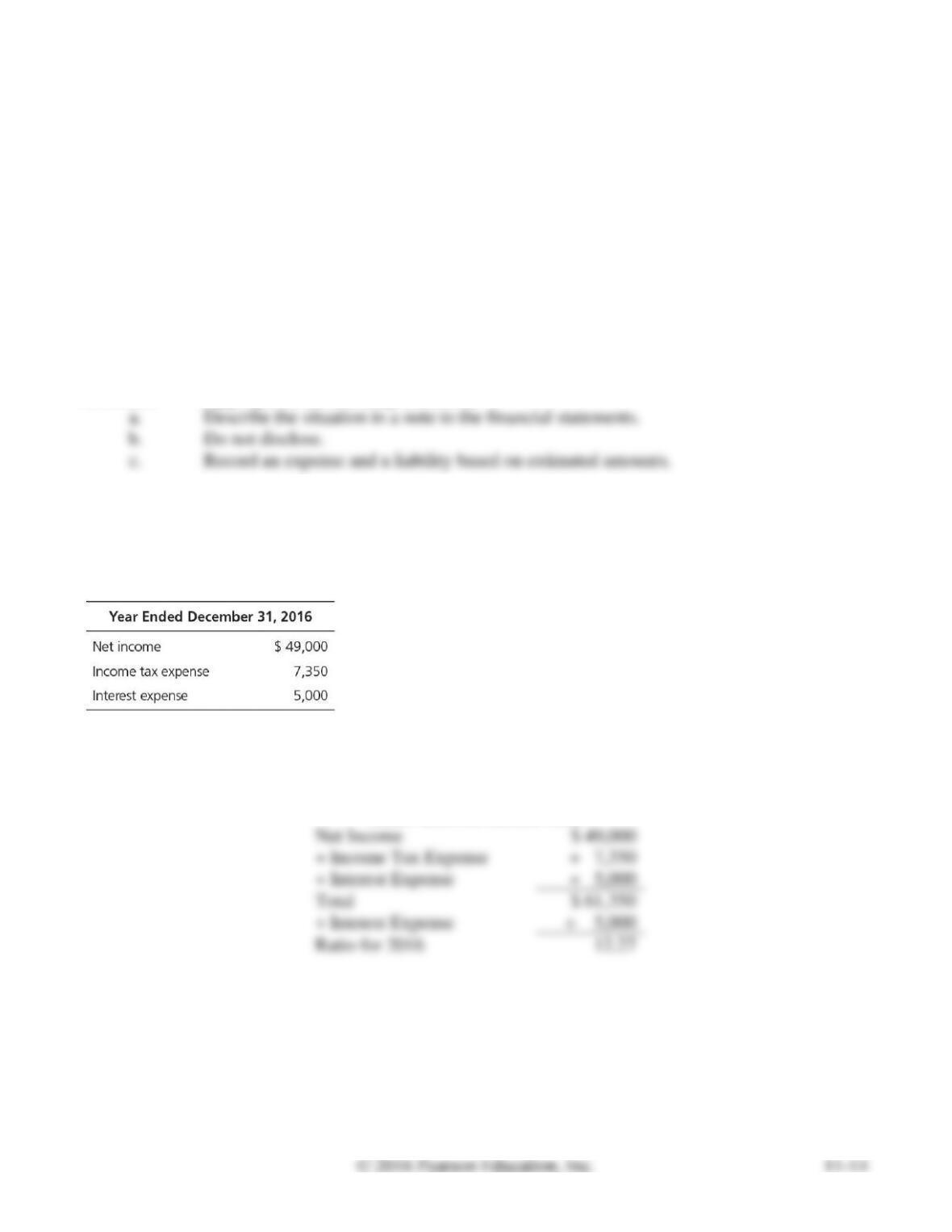

Learning Objective 5

Arnold Electronics reported the following amounts on its 2016 income statement:

What is Arnold’s times-interest-earned ratio for 2016? (Round the answer to two decimals.)

SOLUTION

Times-interest-earned ratio

Exercises

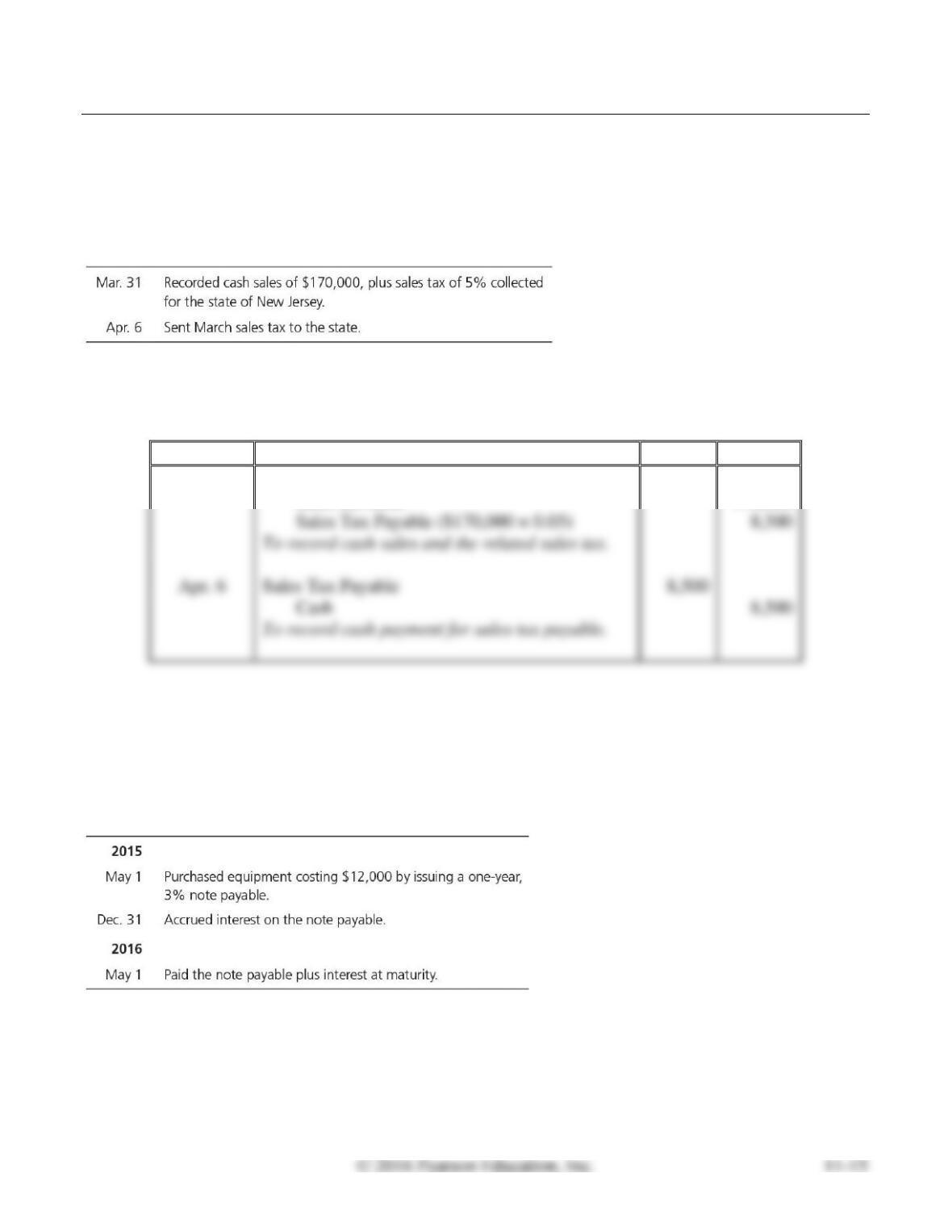

E11-14 Recording sales tax

Learning Objective 1

Sales Tax Payable $8,500

Consider the following transactions of Moore Software:

Journalize the transactions for the company. Ignore cost of goods sold.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Mar. 31

Cash

178,500

Sales Revenue

170,000

Sales Tax Payable ($170,000 × 0.05)

Sales Tax Payable

Cash

E11-15 Recording note payable transactions

Learning Objective 1

May 1, 2016 Interest Expense $120

Consider the following note payable transactions of Concert Video Productions.

Journalize the transactions for the company.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2015

May 1

Equipment

12,000

Notes Payable

12,000

Interest Expense ($12,000 × 0.03 × 8/12)

Interest Payable

2016

May 1

Notes Payable

12,000

Interest Payable

Cash

12,360

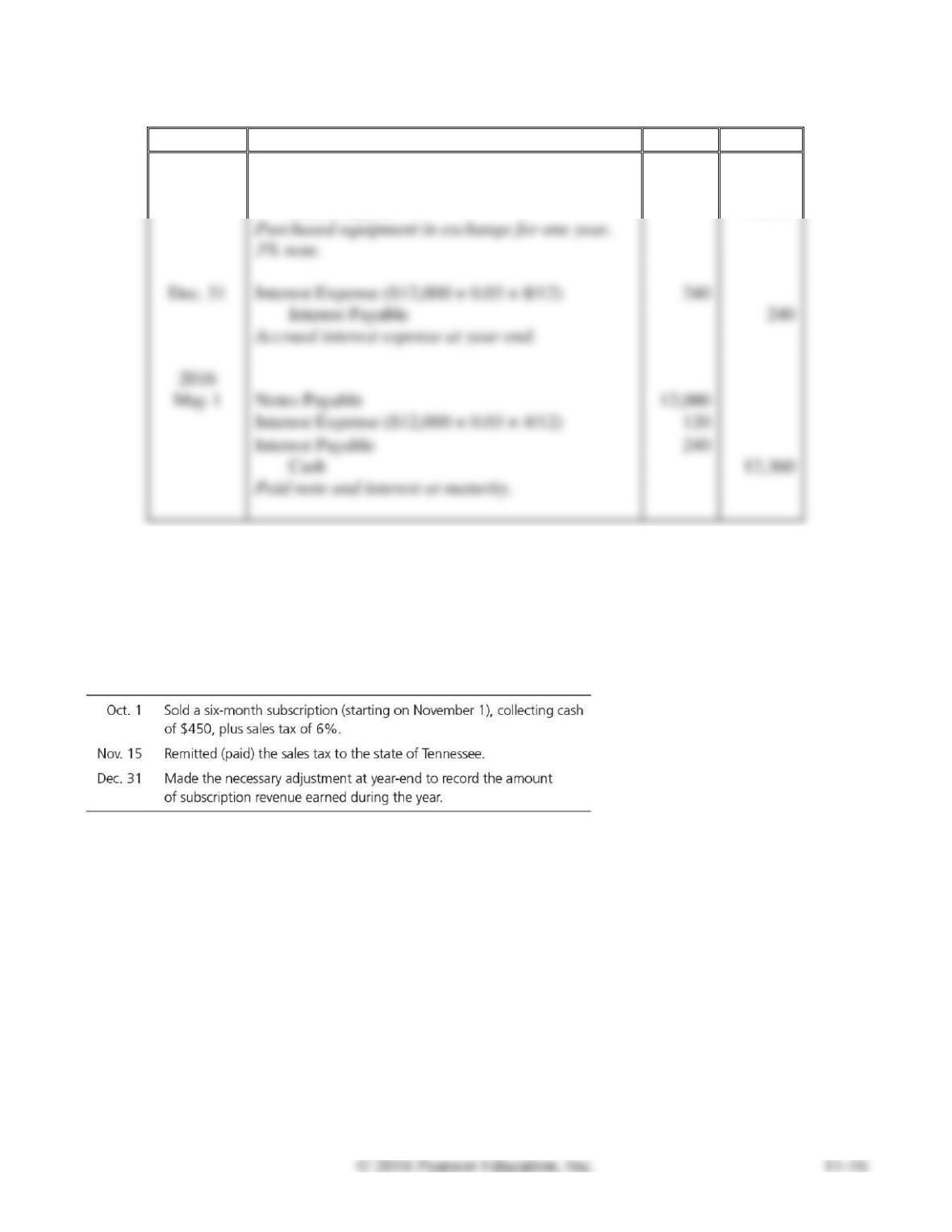

E11-16 Recording and reporting current liabilities

Learning Objective 1

Dec. 31 Subscription Revenue $150

Worldly Publishing completed the following transactions during 2016:

Journalize the transactions (explanations are not required).

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2016

Oct. 1

Cash

477

Unearned Revenue

450

Sales Tax Payable ($450 × 6%)

27

sales tax.

Sales Tax Payable

27

Cash

27

payable.

Unearned Revenue

150

Subscription Revenue

150

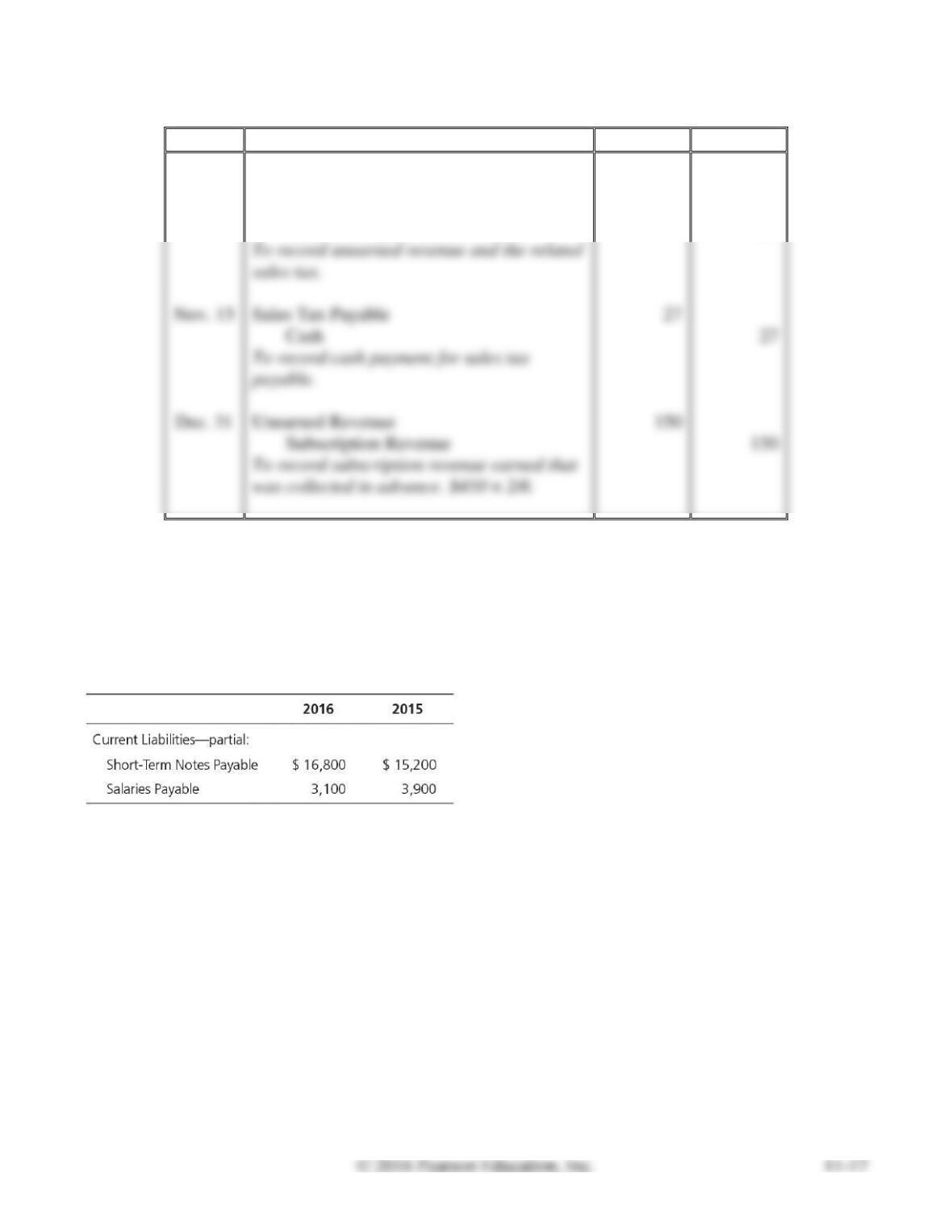

E11-17 Journalizing current liabilities

Learning Objectives 1, 2

Salaries Expense $3,100

Erik O’Hern Associates reported short-term notes payable and salaries payable as follows:

During 2016, O’Hern paid off both current liabilities that were left over from 2015, borrowed money on

short-term notes payable, and accrued salaries expense. Journalize all four of these transactions for

O’Hern during 2016. Assume no interest on short-term notes payable of $15,200.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2016

Short-Term Notes Payable

15,200

Cash

15,200

Salaries Payable

Cash

Cash

16,800

Short-Term Notes Payable

16,800

Salaries Expense

Salaries Payable

E11-18 Computing and recording gross and net pay

Learning Objective 2

1. Net Pay $362.44

Hubert Sollenberger manages a Dairy House drive-in. His straight-time pay is $8 per hour, with time-

and-a-half for hours in excess of 40 per week. Sollenberger’s payroll deductions include withheld

income tax of 20%, FICA tax, and a weekly deduction of $8 for a charitable contribution to United Way.

Sollenberger worked 56 hours during the week.

Requirements

1. Compute Sollenberger’s gross pay and net pay for the week. Assume earnings to date are $11,000.

2. Journalize Dairy House wages expense accrual for Sollenberger’s work. An explanation is not

required.

3. Journalize the subsequent payment of wages to Sollenberger.

SOLUTION

Requirement 1

Straight-time pay for 40 hours ($8 × 40 hours)

$ 320.00

Overtime pay for 16 hours: (16 × $8 × 1.5)

Gross Pay

$ 512.00

Gross pay

Withholding deductions:

Employee income tax (20%)

Employee OASDI tax (6.2%)

Employee Medicare tax (1.45%)

Employee contribution to United Way

Total withholdings

Net (take-home) pay

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Wages Expense

512.00

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Wages Payable

362.44

E11-19 Recording employer payroll taxes and employee benefits

Learning Objective 2

Payroll Tax Expense $6,135.00

Diego’s Mexican Restaurant incurred salaries expense of $70,000 for 2016. The pay– roll expense

includes employer FICA tax, in addition to state unemployment tax and federal unemployment tax. Of

the total salaries, $13,000 is subject to unemployment tax. Also, the company provides the following

benefits for employees: health insurance (cost to the company, $2,700), life insurance (cost to the

company, $380), and retirement benefits (cost to the company, 10% of salaries expense). Journalize

Diego’s expenses for employee benefits and for payroll taxes. Explanations are not required.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Payroll Tax Expense

6,135

FICA—OASDI Taxes Payable (6.2% × $70,000)

4,340

FICA—Medicare Taxes Payable (1.45% × $70,000)

1,015

Employee Benefits Expense

7,000