CHAPTER 11

THE BETA FOR FLIR SYSYTEMS

NOTE: The example below shows the results from January 2015. The actual answer to the case will

change based on current market conditions

1. The information used for the analysis is presented below. Note that the risk-free rate is an annual rate.

It is necessary to find the monthly rate, so this rate is divided by 12.

3 month

Risk-free

1 month

risk-free

Stock

price

Return

S&P 500

S&P 500

return

Stock

risk

premium

Market

risk

premium

Dec–10

$27.99

1257.64

Jan-11

0.15

0.0125

$29.21

0.0434

1286.12

0.0226

0.0309

0.0101

Feb-11

0.13

0.01083

$30.45

0.0425

1327.22

0.0320

0.0317

0.0211

Mar–11

0.10

0.00833

$32.63

0.0715

1325.83

-0.0010

0.0632

-0.0094

Sep-11

0.01

0.00083

$23.71

-0.0317

1131.42

-0.0718

-0.0325

-0.0726

Oct–11

0.02

0.00167

$24.90

0.0499

1253.30

0.1077

0.0482

0.1061

Nov-11

0.01

0.00083

$25.49

0.0237

1246.96

-0.0051

0.0228

-0.0059

Dec–11

0.01

0.00083

$23.79

-0.0666

1257.60

0.0085

-0.0675

0.0077

Jan-12

0.03

0.0025

$24.43

0.0271

1312.41

0.0436

0.0246

0.0411

Feb-12

0.09

0.0075

$24.90

0.0192

1365.68

0.0406

0.0117

0.0331

Mar–12

0.08

0.00667

$24.08

-0.0329

1408.47

0.0313

-0.0395

0.0247

Apr-12

0.08

0.00667

$21.37

-0.1126

1397.91

-0.0075

-0.1193

-0.0142

0.09

0.0075

$20.36

-0.0471

1310.33

-0.0627

-0.0546

-0.0702

0.09

0.0075

$18.62

-0.0858

1362.16

0.0396

-0.0933

0.0321

0.10

0.00833

$19.52

0.0487

1379.32

0.0126

0.0404

0.0043

Sep-12

0.11

0.00917

$19.14

0.0091

1440.67

0.0242

-0.0001

0.0151

Oct–12

0.10

0.00833

$18.61

-0.0275

1412.16

-0.0198

-0.0359

-0.0281

Nov-12

0.09

0.0075

$19.61

0.0538

1416.18

0.0028

0.0463

-0.0047

Dec–12

0.07

0.00583

$21.46

0.0941

1426.19

0.0071

0.0883

0.0012

Jan-13

0.07

0.00583

$22.85

0.0650

1498.11

0.0504

0.0591

0.0446

Feb-13

0.10

0.00833

$25.40

0.1114

1514.68

0.0111

0.1031

0.0027

Apr-13

0.06

0.005

$23.45

-0.0654

1597.57

0.0181

-0.0704

0.0131

Apr-11

0.06

0.005

$33.20

0.0176

1363.61

0.0285

0.0126

0.0235

0.04

0.00333

$34.13

0.0281

1345.20

-0.0135

0.0248

-0.0168

0.04

0.00333

$31.83

-0.0675

1320.64

-0.0183

-0.0708

-0.0216

0.04

0.00333

$25.93

-0.1854

1292.28

-0.0215

-0.1887

-0.0248

Aug-11

0.02

0.00167

$24.49

-0.0555

1218.89

-0.0568

-0.0572

-0.0585

May–13

0.04

0.00333

$23.58

0.0057

1630.74

0.0208

0.0024

0.0174

Jun-13

0.05

0.00417

$26.11

0.1071

1606.28

-0.0150

0.1030

-0.0192

Jul-13

0.04

0.00333

$31.44

0.2039

1685.73

0.0495

0.2006

0.0461

Aug-13

0.04

0.00333

$30.37

-0.0340

1632.97

-0.0313

-0.0373

-0.0346

Feb-14

0.05

0.00417

$33.35

0.0798

1859.45

0.0431

0.0756

0.0390

Mar–14

0.05

0.00417

$35.17

0.0545

1872.34

0.0069

0.0503

0.0028

Apr-14

0.03

0.0025

$33.26

-0.0544

1883.95

0.0062

-0.0569

0.0037

May–14

0.03

0.0025

$34.21

0.0286

1923.57

0.0210

0.0261

0.0185

Jun-14

0.04

0.00333

$34.03

-0.0052

1960.23

0.0191

-0.0085

0.0157

Jul-14

0.03

0.0025

$32.61

-0.0418

1930.67

-0.0151

-0.0443

-0.0176

Aug-14

0.03

0.0025

$33.21

0.0183

2003.37

0.0377

0.0158

0.0352

Sep-14

0.02

0.00167

$30.80

-0.0725

1972.29

-0.0155

-0.0742

-0.0172

0.02

0.00167

$32.95

0.0699

2018.05

0.0232

0.0682

0.0215

Nov-14

0.02

0.00167

$31.28

-0.0508

2067.56

0.0245

-0.0524

0.0229

Dec–14

0.03

0.0025

$31.85

0.0183

2058.90

-0.0042

0.0158

-0.0067

Jan-15

0.03

0.0025

$29.77

-0.0653

1994.99

-0.0310

-0.0678

-0.0335

Feb-15

0.02

0.00167

$31.93

0.0725

2104.50

0.0549

0.0708

0.0532

Mar–15

0.03

0.0025

$30.94

-0.0310

2067.89

-0.0174

-0.0335

-0.0199

Apr-15

0.02

0.00167

$30.56

-0.0125

2085.51

0.0085

-0.0141

0.0069

May–15

0.02

0.00167

$30.32

-0.0076

2107.39

0.0105

-0.0092

0.0088

Jun-15

0.02

0.00167

$30.59

0.0088

2063.11

-0.0210

0.0072

-0.0227

Jul-15

0.03

0.0025

$30.56

-0.0010

2103.84

0.0197

-0.0035

0.0172

Aug-15

0.07

0.00583

$28.52

-0.0668

1972.18

-0.0626

-0.0726

-0.0684

Sep-15

0.02

0.00167

$27.88

-0.0224

1920.03

-0.0264

-0.0240

-0.0281

0.02

0.00167

$26.57

-0.0472

2079.36

0.0830

-0.0488

0.0813

Nov-15

0.13

0.01083

$30.56

0.1502

2080.41

0.0005

0.1394

-0.0103

Dec–15

0.23

0.01917

$28.07

-0.0815

2043.94

-0.0175

-0.1006

-0.0367

Using the Excel functions for the average return and standard deviation, the table below shows the

averages and standard deviations for each of the series.

Risk-free

Stock

S&P 500

Average return

.0047%

.22%

.87%

Standard deviation

.0034%

6.70%

3.38%

Sep-13

0.02

0.00167

$30.48

0.0038

1681.55

0.0297

0.0022

0.0281

0.05

0.00417

$27.65

-0.0930

1756.54

0.0446

-0.0972

0.0404

Nov-13

0.07

0.00583

$28.89

0.0450

1805.81

0.0280

0.0391

0.0222

Dec–13

0.07

0.00583

$29.31

0.0145

1848.36

0.0236

0.0087

0.0177

Jan-14

0.04

0.00333

$30.89

0.0538

1782.59

-0.0356

0.0505

-0.0389

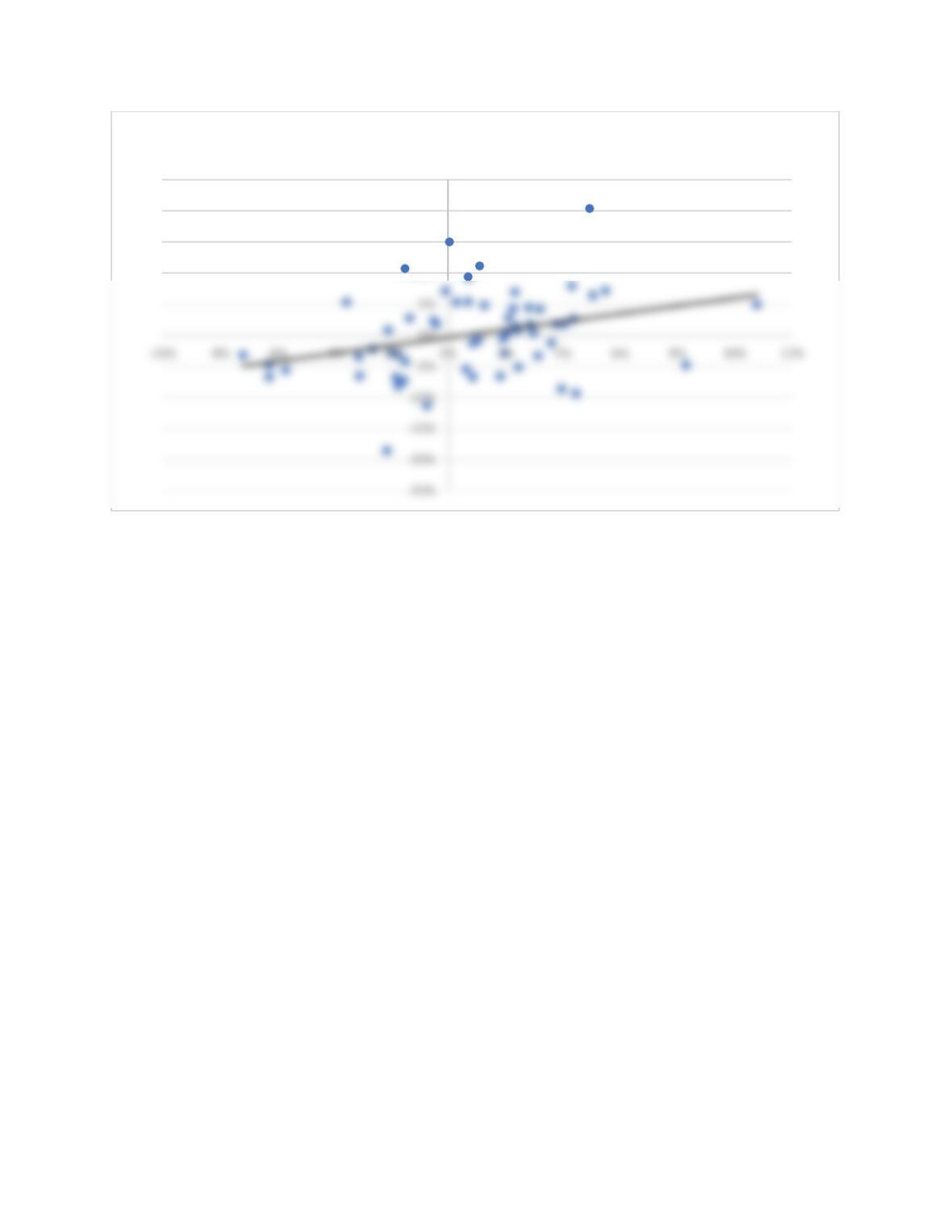

2. Jensen’s alpha represents the excess return not explained by the beta of the stock. A positive alpha

plots above the Security Market Line and has a return in excess of its systematic risk.

3. The relevant output from the Excel regression is:

SUMMARY OUTPUT

Regression Statistics

Multiple R

0.321776363

R Square

0.103540028

Adjusted R Square

0.088083821

Standard Error

0.063980181

Observations

60

Regression

Residual

58

Total

Intercept

X Variable 1

0.638388418

4. The beta for FLIR Systems on Yahoo! Finance at the time was .53, which is similar to this estimate.

Possible reasons for the difference could be different data, for example Yahoo! Finance could use a

longer or shorter period, or use daily data, a different risk-free rate, or a different market risk premium.

10%

15%

20%

25%

FLIR Monthly Returns vs. S&P 500 Returns