P11-30B Journalizing and posting liabilities

Learning Objectives 1, 2

1d. Rent Revenue $2,625

The general ledger of U-R-Shipping at June 30, 2016, the end of the company’s fiscal year, includes the

following account balances before payroll and adjusting entries.

The additional data needed to develop the payroll and adjusting entries at June 30 are as follows:

a. The long-term debt is payable in annual installments of $60,000, with the next installment due on

July 31. On that date, U-R-Shipping will also pay one year’s interest at 8%. Interest was paid on July

31 of the preceding year. Make the adjusting entry to accrue interest expense at year-end.

Requirements

1. Using T-accounts, open the listed accounts and insert the unadjusted June 30 balances.

2. Journalize and post the June 30 payroll and adjusting entries to the accounts that you opened.

Identify each adjusting entry by letter.

3. Prepare the current liabilities section of the balance sheet at June 30, 2016.

SOLUTION

Requirements 1 and 2

Date

Accounts and Explanation

Debit

Credit

2016

Jun. 30

a.

Interest Expense

22,000.00

Interest Payable ($300,000 × 8 % × 11/12)

22,000.00

a.

Salary Expense

Employee Income Taxes Payable

Salaries Payable

c.

Payroll Tax Expense

Unearned Rent Revenue

Rent Revenue ($6,300 × 5/12)

Accounts Payable

115,000 Beg. Bal.

115,000 End Bal.

22,000 a.

22,000 End Bal.

P11-30B, cont.

Requirements 1 and 2, cont.

Employee Income Taxes Payable

0 Beg. Bal.

820 b.

820 End Bal.

0 Beg. Bal.

0 Beg. Bal.

Unearned Rent Revenue

6,300 Beg. Bal.

d. 2,625

3,675 End Bal.

300,000 Beg. Bal.

P11-30B, cont.

Requirement 3

U-R-SHIPPING

Balance Sheet (Partial)

June 30, 2016

Liabilities

Current Liabilities:

Accounts Payable

$

115,000.00

Current Portion of Notes Payable

Interest Payable

Salaries Payable

Unearned Rent Revenue

Total Current Liabilities

$

205,088.65

P11-31B Computing and journalizing payroll amounts

Learning Objective 2

1. Net Pay $156,895

Len Wilson is general manager of Crossroad Salons. During 2016, Wilson worked for the company all

year at a $14,200 monthly salary. He also earned a year-end bonus equal to 10% of his annual salary.

Requirements

1. Compute Wilson’s gross pay, payroll deductions, and net pay for the full year 2016. Round all

amounts to the nearest dollar.

2. Compute Crossroad’s total 2016 payroll tax expense for Wilson.

3. Make the journal entry to record Crossroad’s expense for Wilson’s total earnings for the year, his

SOLUTION

Requirement 1

Len Wilson

Payroll for the year ended December 31, 2016

Calculation

Annual

Gross Pay:

Salary

$14,200 × 12

$ 170,400

Bonus

Total Gross Pay

Deductions:

Federal Income Tax

State Income Tax

Charity Fund

Life Insurance

Total Deductions

Net Pay

$ 156,895

Requirement 2

Len Wilson

Employer Payroll Expense for the year ended December 31, 2016

Calculation

Annual

Gross Pay

$ 187,440

Employer Payroll Taxes:

FUTA

SUTA

Total Employer Payroll Tax

P11-31B, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2016

Dec. 31

Salaries Expense

170,400

Bonus Expense

17,040

1,630

7,254

2,718

5,623

Requirement 4

Date

Accounts and Explanation

Debit

Credit

2016

Dec. 31

Payroll Tax Expense

10,392

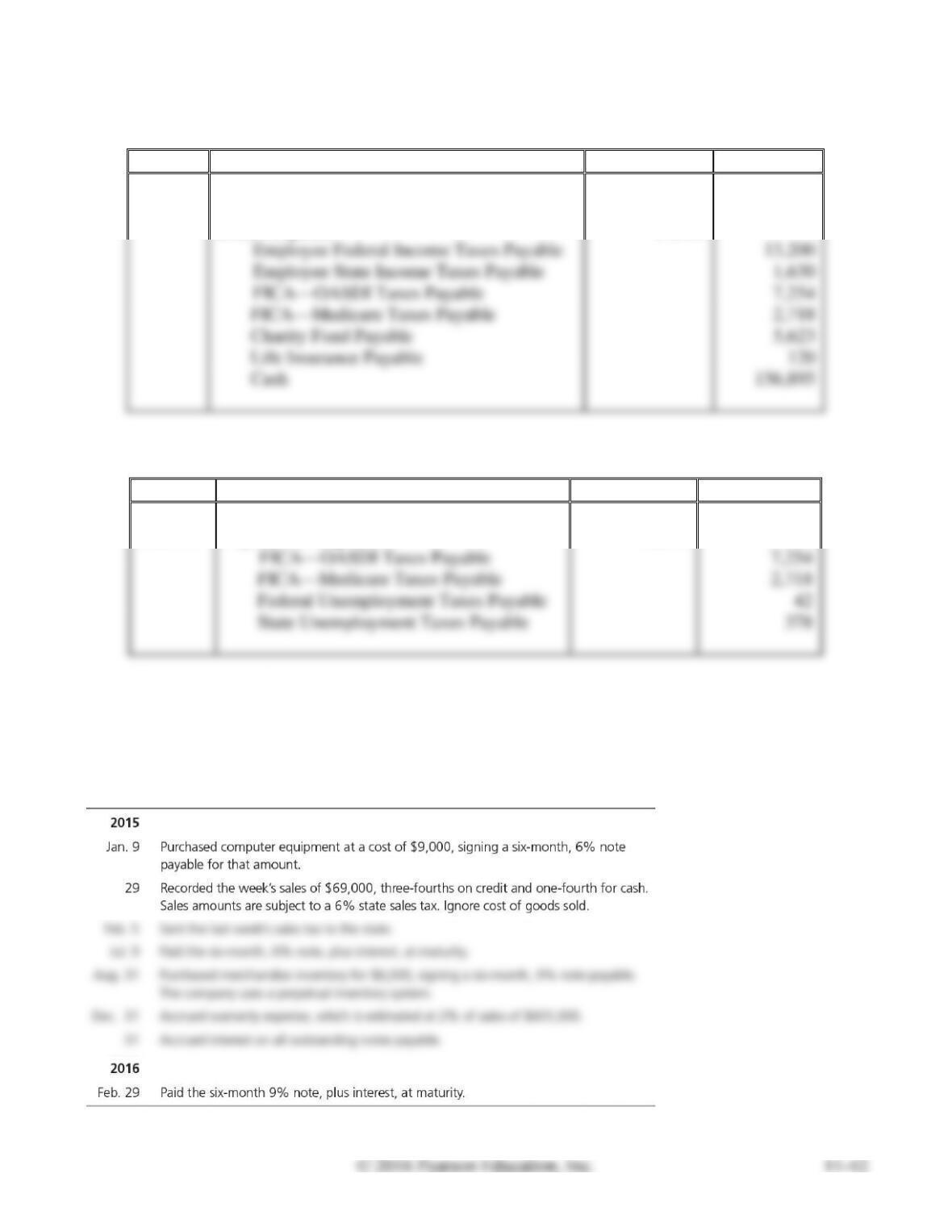

P11-32B Journalizing liability transactions

Learning Objectives 1, 3

Jan. 29 Cash $18,285

The following transactions of San Francisco Pharmacies occurred during 2015 and 2016:

Journalize the transactions in San Francisco’s general journal. Explanations are not required.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2015

Jan. 9

Computer Equipment

9,000

Short-term Notes Payable

9,000

Cash ($69,000 × ¼) + ($17,250 × 6%)

Accounts Receivable ($69,000 × ¾) + (51,750 × 6%)

4,140

Sales Tax Payable

4,140

4,140

Short-term Notes Payable

9,000

9,270

Merchandise Inventory

6,000

6,000

Warranty Expense (2% × $601,000)

Interest Expense ($6,000 × 9% × 4/12)

Short-term Notes Payable

6,000

Interest Payable

Interest Expense ($6,000 × 9% × 2/12)

6,270

P11-33B Journalizing liability transactions

Learning Objectives 3, 4

1. June 30 Warranty Expense $18,000

The following transactions of Percy Bowes occurred during 2016:

Requirements

1. Journalize required transactions, if any, in Bowes’s general journal. Explanations are not required.

2. What is the balance in Estimated Warranty Payable assuming a beginning balance of $0?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Apr. 30

No entry required

Warranty Expense (4% × $450,000)

18,000

Estimated Warranty Payable

Estimated Loss from Lawsuit

120,000

Dec. 31

Warranty Expense (4% × $480,000)

19,200

Requirement 2

Estimated Warranty Payable

18,000 Jun. 30

Jul. 28 6,300

19,200 Dec. 31

30,900 End Bal.

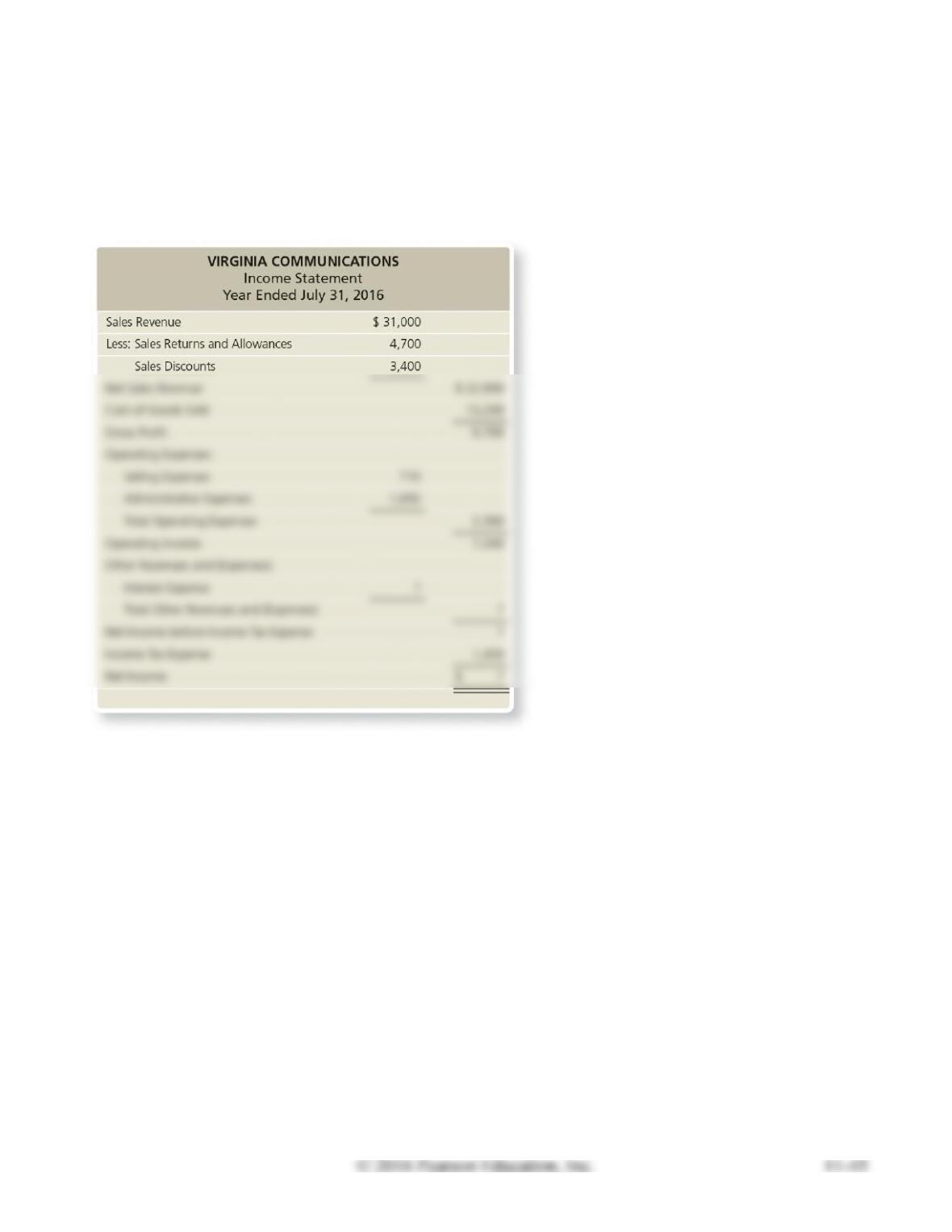

P11-34B Computing times-interest-earned ratio

Learning Objective 5

1. Net Income $5,790

The income statement for Virginia Communications follows. Assume Virginia Communications signed

a 120-day, 6%, $10,000 note on June 1, 2016, and that this was the only note payable for the company.

Requirements

1. Fill in the missing information for Virginia’s year ended July 31, 2016, income statement.

2. Compute the times-interest-earned ratio for the company.

SOLUTION

Requirement 1

VIRGINIA COMMUNICATIONS

Income Statement

Year Ended July 31, 2016

Sales Revenue

$ 31,000

Less: Sales Returns and Allowances

(4,700)

(3,400)

$ 22,900

Gross Profit

9,700

Operating Expenses:

(2,360)

Operating Income

7,340

Other Revenues and (Expenses):

Net Income before Income Tax Expense

7,240

Income Tax Expense

(1,450)

Net Income

Interest Expense = $10,000 × 6% × 60/360 = $100

Requirement 2

Times-interest-earned ratio

Net Income

$ 5,790

+ Income Tax Expense

+ 1,450

+ Interest Expense

Total

$ 7,340

÷ Interest Expense

Ratio for 2016

Continuing Problem

P11-35 Accounting for liabilities of a known amount

This problem continues the Daniels Consulting situation from Problem P10-23 of Chapter 10. Daniels

Consulting believes the company will need to borrow $300,000 in order to expand operations. Daniels

consults the bank and secures a 6%, five-year note on March 1, 2017. Daniels must pay the bank

principal in five equal installments plus interest annually on March 1.

Requirements

1. Record the $300,000 note payable on March 1, 2017.

SOLUTION

Requirements 1, 2, 3

Date

Accounts and Explanation

Debit

Credit

2017

Mar. 1

Cash

300,000

Long-Term Notes Payable

300,000

Interest Expense (300,000 × 6% × 10/12)

Interest Payable

2018

Mar. 1

Long-Term Notes Payable

Interest Payable

Interest Expense ($300,000 × 6% × 2/12)

Critical Thinking

Decision Case 11-1

Golden Bear Construction operates throughout California. The owner, Gaylan Beavers, employs 15

work crews. Construction supervisors report directly to Beavers, and the supervisors are trusted

employees. The home office staff consists of an accountant and an office manager.

Because employee turnover is high in the construction industry, supervisors hire and fire their own

crews. Supervisors notify the office of all personnel changes. Also, supervisors forward the employee

W-4 forms to the home office. Each Thursday, the supervisors submit weekly time sheets for their

crews, and the accountant prepares the payroll. At noon on Friday, the supervisors come to the office to

get paychecks for distribution to the workers at 5 p.m.

The company accountant prepares the payroll, including the paychecks. Beavers signs all paychecks.

To verify that each construction worker is a bona fide employee, the accountant matches the employee’s

endorsement signature on the back of the canceled paycheck with the signature on that employee’s W-4

form.

Requirements

1. Identify one way that a supervisor can defraud Golden Bear Construction under the present system.

2. Discuss a control feature that the company can use to safeguard against the fraud you identified in

Requirement 1.

SOLUTION

Requirement 1

A supervisor can enter a fictitious employee on a weekly time sheet, submit the time sheet to the

Requirement 2

To safeguard against the company fraud identified in Requirement 1, Beavers (or a home office

employee) should make unscheduled visits to construction sites and distribute payroll checks. If a

paycheck is payable to an employee not present to receive it, Beavers can ask other workers if the absent

person has been working on that job. If the workers say no, Beavers will have uncovered a possible

fraud.

Decision Case 11-2

Sell-Soft is the defendant in numerous lawsuits claiming unfair trade practices. Sell-Soft has strong

incentives not to disclose these contingent liabilities. However, GAAP requires that companies report

their contingent liabilities.

Requirements

1. Why would a company prefer not to disclose its contingent liabilities?

2. Describe how a bank could be harmed if a company seeking a loan did not disclose its contingent

liabilities.

3. What ethical tightrope must companies walk when they report contingent liabilities?

SOLUTION

Requirement 1

A company would prefer not to disclose its contingent liabilities because they cast a shadow on the

Requirement 2

A contingent liability creates risk for a company. If the contingent liability is not reported, the bank may

Requirement 3

Reporting of contingent liabilities often depends on subjective judgment about whether an outcome is

Ethical Issue 11-1

Many small businesses have to squeeze down costs any way they can just to survive. One way many

businesses do this is by hiring workers as “independent contractors” rather than as regular employees.

Unlike rules for regular employees, a business does not have to pay Social Security (FICA) taxes and

unemployment insurance payments for independent contractors. Similarly, it does not have to withhold

federal, state, or local income taxes or the employee’s share of FICA taxes. The IRS has a “20 factor

test” that determines whether a worker should be considered an employee or a con- tractor, but many

businesses ignore those rules or interpret them loosely in their favor. When workers are treated as

independent contractors, they do not get a W-2 form at tax time (they get a 1099 instead), they do not

have any income taxes withheld, and they find themselves subject to “self–employment” taxes, by which

they bear the brunt of both the employee’s and the employer’s shares of FICA taxes.

Requirements

1. When a business abuses this issue, how is the independent contractor hurt?

2. If a business takes an aggressive position—that is, interprets the law in a very slanted way—is there

an ethical issue involved? Who is hurt?

SOLUTION

Requirement 1

The contractor must pay “self–employment tax” which represents both the employer’s and the

Requirement 2

Businesses may take aggressive positions on tax issues, and those positions may be tested in court. It is

Financial Statement Case 11-1

Requirements

1. Give the breakdown of Starbucks’s current liabilities at September 29, 2013.

2. Calculate Starbucks’s times-interest-earned ratio for the year ending September 30, 2012.

SOLUTION

Requirement 1

STARBUCKS

Balance Sheet (partial)

September 29, 2013 (In millions)

Liabilities

Current Liabilities:

Accounts payable

Accrued litigation charge

Accrued liabilities

Insurance reserves

Deferred revenue

Total current liabilities

Requirement 2

Times-Interest-Earned Ratio

September

30, 2012

Net Income

$ 1,383.8

+ Income Tax Expense

+ Interest Expense

Total

$ 2,090.9

÷ Interest Expense

Communication Activity 11-1

In 150 words or fewer, explain how contingent liabilities are accounted for.

SOLUTION

How businesses record or don’t record contingent liabilities is based on one of three likelihoods of the

event occurring in the future: remote, reasonably possible, or probable.