CEC also announced that it had introduced a poison pill defense intended to prevent others from acquiring more than

10% of its outstanding shares. The adoption of the poison pill makes it less likely that others will seek to block the deal and

push for a higher purchase price. Another bidder buying more than 10% of CEC’s outstanding shares would allow the firm

to issue additional shares thereby increasing the overall cost to acquire CEC. Existing investors such as Fidelity

Investments and Wellington Management, who already own at least 10 % of the firm as of March 31, 2013, are exempt

from the pill.

T-Mobile and MetroPCS Complete a Multibillion Dollar Merger

_____________________________________________________________________________

Case Study Objectives: To illustrate

• How deal structures reflect the primary needs of the parties to the negotiations

• How reverse mergers enable private firms or wholly owned subsidiaries of parent firms to go public and

• Their use as a corporate restructuring strategy.

______________________________________________________________________________

Background

T-Mobile Chief Executive Officer John Legere has always been considered a maverick in the wireless telecommunications

industry. At an interview at the Consumer Electronics Show in Las Vegas in 2014 he discussed how T-Mobile had all the

momentum in the industry. “The firm,” he said,” has presented itself as the antithesis of what most people do not like about

their carriers.” Reflecting growing market acceptance of its new marketing campaign, the firm added 4.4 million new

customers, including prepaid, during 2013.

22

After U.S. regulators nixed a $39 billion merger between T-Mobile and AT&T in late 2011 due to antitrust concerns, the

outlook for T-Mobile, the nation’s fourth largest cellular phone carrier, looked bleak. The firm was hemorrhaging

customers to Verizon and AT&T once their contracts ended. Rene Obermann, CEO of T-Mobile’s parent firm Deutsche–

Telekom, made it clear that he was unwilling to increase significantly its investment in T-Mobile. Without a 4G LTE

network and the ability to offer high-end smartphones like its competitors because of its lack of clout with handset vendors,

the firm appeared destined to shrink amid an industry in flux.

Not to be outdone, T-Mobile merged with MetroPCS on May 1, 2013 in a complex deal structure designed to allow T-

Mobile’s parent Deutsche-Telekom to exit T-Mobile over time, satisfy T-Mobile’s and MetroPCS’s need for additional

spectrum, realize substantial cost synergies, and to provide a significant takeover premium for MetroPCS shareholders as

an incentive to approve the deal. Although its geographic coverage is less than its larger competitors, this deal gave T-

Mobile the fastest network in the U.S. For Obermann, who after seven years as CEO was succeeded by Chief Financial

Officer Timotheus Hoettges at the end of 2013, the deal was probably his last chance to find a solution to the U.S. business

that had long eluded him. What follows is a discussion of how reverse mergers can be used as part of a complex

restructuring strategy to achieve these diverse strategic objectives for each of the three parties involved: Deutsche-Telekom,

T-Mobile, and MetroPCS.

The Shareholders’ Dilemma

In late 2012, T-Mobile announced that it had reached an agreement to merge with MetroPCS. Dallas-based MetroPCS is a

low-cost, no-contract provider of prepaid data plans and inexpensive phones targeted at Americans who could not afford

Verizon and AT&T’s more expensive offerings. At the time, it was the fifth largest wireless carrier in the U.S. based on the

number of subscribers. According to Roger Linquist, Chairman and CEO of MetroPCS, the deal addresses the firm’s need

for additional spectrum and allows for expansion into underserved markets. The firm’s shareholders in assessing the

proposed deal were confronted with the usual dilemma: Do the proposed benefits of the combination represent a better

alternative to remaining a standalone company?

23

A recapitalization is viewed as a financial reorganization in which Deutsche-Telekom would have a substantial

continuing interest in Newco as a result of its exchange of T-Mobile shares for MetroPCS shares. T-Mobile’s operations

are unaffected; and, as such, a recapitalization is not considered an actual sale of the business. Consequently, the deal is tax-

free to Deutsche-Telekom. See Chapter 12 for a more detailed discussion of this matter.

The Newco shares held by MetroPCS shareholders would trade on a public stock exchange. While not impacting

Newco’s market value, the reverse stock split would reduce the number of Newco shares outstanding following the

exchange of 74% of MetroPCS post-split shares for all of T-Mobile shares. The 26% of the Newco shares held by former

MetroPCS shareholders would be publicly traded. Thus, the intent of the reverse split may have been to support the value of

the publicly traded Newco shares by boosting earnings per share to mitigate any selling pressure on the stock. That is, for a

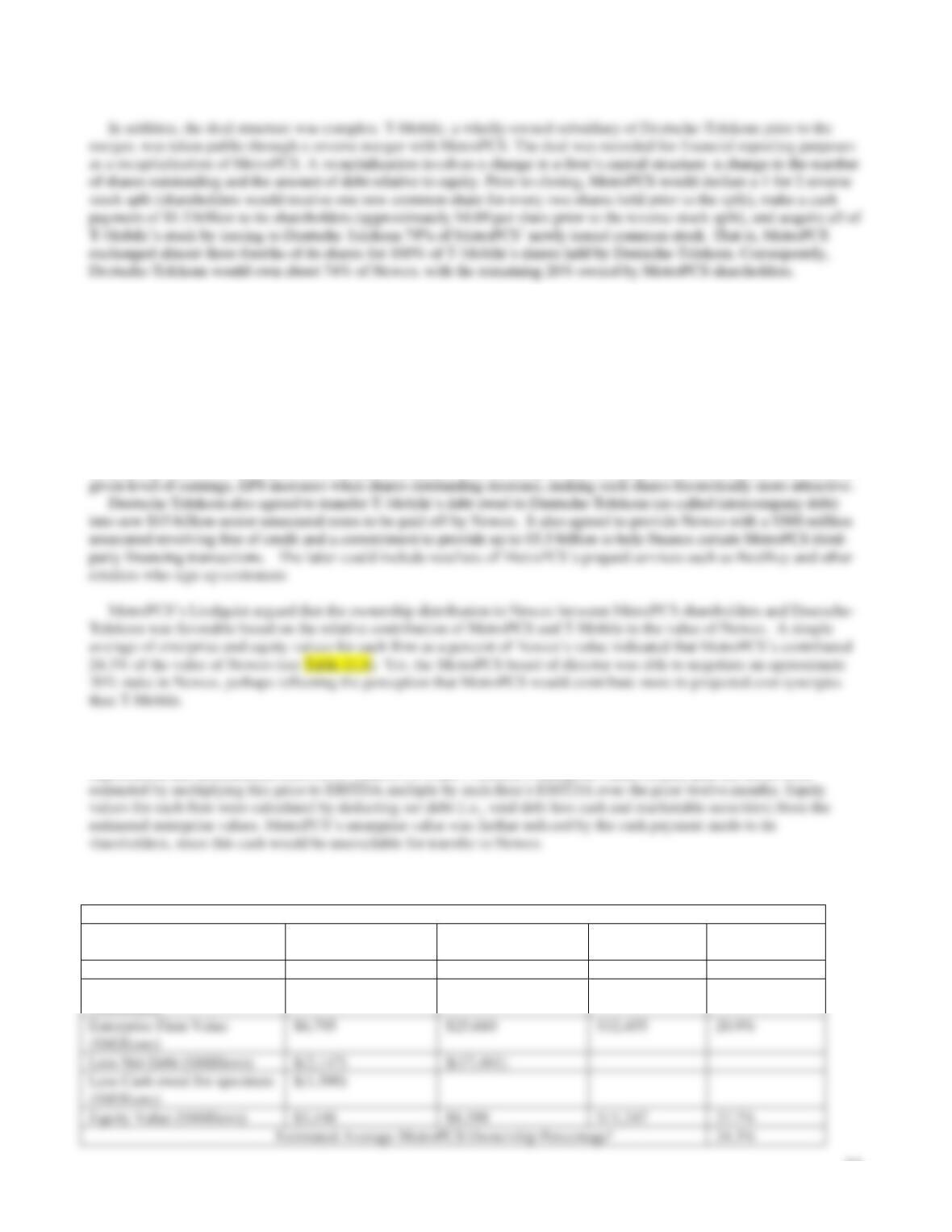

Newco’s valuation depended on the assumption that industry average valuation multiples could be applied to valuing the

combined firms. At the time, wireless carriers were trading at an average of five times earnings before interest, taxes,

depreciation and amortization (EBITDA). MetroPCS’s and T–Mobile’s enterprise values (equity plus net debt) were

Table 11.6 MetroPCS Ownership Analysis

MetroPCS

T-Mobile

Newco

MetroPCS as %

Newco

Firm Value/EBITDA

5x

5x

NA

NA

2013 Estimated EBITDA

($Millions)

$1,359

$5,132

$6,491

NA

24

NA: Not applicable.

aCalculated as a simple average of MetroPCS as a percent of Newco ‘s enterprise and equity values.

Critics of the proposed deal raised concerns about the amount of leverage Newco would have following closing.

However, as shown in Table 11.7, MetroPCS’s financial leverage following closing was in line with its peers. In addition,

its S&P credit rating of BB was higher than its peers. Note that net debt is gross or total debt less cash and marketable

securities.

Table 11.7 Comparison of Newco Peers Leverage and Credit Ratings

Based on Last Twelve Months EBITDA

Leap

Sprint

Newco

MetroPCS

(Post-

Merger)

T-Mobile

(Pre-Merger)

Gross Leverage

(Total Debt/EBITDA)

5.5x

5.5x

3.6x

3.1x

3.6x

Selecting a Restructuring Strategy

The reverse merger was undertaken in lieu of a direct sale of T-Mobile to a strategic buyer or an initial public offering.

Why? Since regulators had disallowed the proposed AT&T takeover of T-Mobile, it was unlikely that there would be a

strategic buyer big enough to buy the firm. IPOs could be administratively cumbersome and expensive.8 Furthermore, since

Deutsche-Telekom was unwilling to invest additional capital into T-Mobile to achieve the necessary size to be competitive

with Verizon and AT&T, it was unlikely that an IPO would attract much investor interest. Consequently, a reverse merger

seemed to be a reasonable option, since it would enable the creation of a new wireless company with the scale to make it

competitive without Deutsche-Telekom investing additional funds. In time, the combined firms could become more

attractive to potential investors enabling Deutsche-Telekom to exit the business at a much higher price than could be

achieved at that time.

Prologue

T-Mobile US, the fourth biggest U.S. wireless company, rose 6% in its first day of trading as a public company to $16.52.

T-Mobile’s Chief Executive Officer John Legere noted “It will be fun to have people voting on the stock every day.” True

to his word, T-Mobile has been shaking up the industry. Late last year, the firm started allowing customers to upgrade their

phones twice a year and introduced no-money down plans for new phones, such as the popular IPhone, forcing competitors

to introduce similar programs.

In early 2014, T-Mobile announced that it would pay termination fees of up to $350 for Verizon, Sprint or AT&T

customers dropping their contracts with these carriers and switching to T-Mobile. Furthermore, T-Mobile offered a credit of

Net Leverage

4.4x

3.0x

3.4x

2.4x

3.6x

25

Discussion Questions

1. The Deutsche-Telekom board decided against a divestiture of T-Mobile or an initial public offering to pursue a reverse

merger. What other alternatives to merging its wholly-owned subsidiary T-Mobile with another firm could Deutsche-

Telekom have pursued? Be specific. What are the advantages and disadvantages of the other options?

16.

A spin-off involves the payment of the stock of T-Mobile held by Deutsche-Telekom to its shareholders as a

dividend. Procedurally, it is relatively straight forward as the board of directors has the sole right to declare the type

(cash or stock) and timing of dividends. Properly structured the dividend would be tax-free to Deutsche-Telekom’s

shareholders. The distribution would have the added advantage of giving the receiving shareholder the right to

determine what to do with the shares: hold or sell. Spin-offs can be complicated by significant amounts of

intercompany loans between the parent and the subsidiary. If the parent burdens the subsidiary with excessive amounts

of debt before spinning off the unit, the spun-off unit may be forced into bankruptcy. Under fraudulent conveyance

laws, the parent may be forced to take back the unit and to pay-off its creditors.

2. What are the primary disadvantages and advantages of a reverse merger strategy?

Answer: As with any merger, the acquirer is taking responsibility for the known and unknown legal and financial

liabilities of the other party. Thus, extensive due diligence is required. As with an equity carve-out, the merged firms

will have minority shareholders. The existence of the public shareholders requires periodically filing reports with the

Securities and Exchange Commission and the administrative costs associated with doing so. More significantly, the

26

3. In what way might the use of the T-Mobile/MetroPCS impact value?

Answer: The use of a reverse merger has all of the advantages (and disadvantages) of a conventional statutory merger.

That is, all assets and liabilities known and unknown automatically transfer by rule of law to the merged firms. The

4. What are the key assumptions implicit in the Deutsche-Telekom restructuring strategy for T-Mobile?

Answer: Deutsche-Telekom sees this deal as an exit strategy from T-Mobil. The objective is to undertake an IPO at

5. What is the form of payment used in this deal? Why might this form have been selected? What are the advantages and

disadvantages of the form of payment used in this deal?

Answer: The form of payment for MetroPCS is a combination of cash and stock. This combination may have been

used because an all-cash deal would have required a substantial increase in borrowing further burdening Newco; using

only stock may not have attracted enough MetroPCS shareholders to vote to approve the deal due to the uncertain

6. What is the form of acquisition used in this deal? Why might this form have been chosen? What are the advantages and

disadvantages of the form of acquisition used in this case study?

Answer: The form of acquisition reflects what is being acquired (stock or assets) and how ownership is conveyed. In

this deal, the form of acquisition was a purchase of all of T-Mobile’s stock held by Deutsche-Telekom. As such, all

Sanofi Acquires Genzyme in a Test of Wills

Key Points

Contingent value rights help bridge price differences between buyers and sellers when the target’s future earnings

performance is dependent on the realization of a specific event.

They are most appropriate when the target firm is a large publicly traded firm with numerous shareholders.

______________________________________________________________________________

27

The acquisition represented the end of a nine-month effort that began on May 23, 2010, when Sanofi CEO Chris

Viehbacher first approached Genzyme’s Henri Termeer, the firm’s founder and CEO. Sanofi expressed interest in Genzyme

at a time when debt was cheap and when Genzyme’s share price was depressed, having fallen from a 2008 peak of $83.25

to $47.16 in June 2010. Genzyme’s depressed share price reflected manufacturing problems that had lowered sales of its

best-selling products. Genzyme continued to recover from the manufacturing challenges that had temporarily shut down

operations at its main site in 2009. The plant is the sole source of Genzyme’s top-selling products, Gaucher’s disease

treatment Cerezyme and Fabry disease drug Fabrazyme. Both were in short supply throughout 2010 due to the plant’s

shutdown. By yearend, the supply shortages were less acute. Sanofi was convinced that other potential bidders were too

occupied with integrating recent deals to enter into a bidding war.

In a letter made public on August 29, 2010, Sanofi indicated that it had been trying to engage Genzyme in acquisition

talks for months and that its formal bid had been rejected by Genzyme without any further discussion on August 11, 2010.

The letter concludes with a thinly disguised threat that “all alternatives to complete the transaction” would be considered

and that “Sanofi is confident that Genzyme shareholders will support the proposal.” In responding to the public disclosure

of the letter, the Genzyme board said it was not prepared to engage in merger negotiations with Sanofi based on an

opportunistic proposal with an unrealistic starting price that dramatically undervalued the company. Termeer said publicly

that the firm was worth at least $80 per share. He based this value on the improvement in the firm’s manufacturing

The CVR helped to allay fears that Sanofi would overpay and that the drug Lemtrada would not be approved by the

FDA. Under the terms of the CVR, Genzyme shareholders would receive $1 per share if Genzyme were able to meet

certain production targets in 2011 for Cerezyme and Fabrazyme, whose output had been sharply curtailed by viral

contamination at its plant in 2009. Each right would yield an additional $1 if Lemtrada wins FDA approval. Additional

payments will be made if Lemtrada hits certain other annual revenue targets. The CVR, which runs until the end of 2020,

entitles holders to a series of payments that could cumulatively be worth up to $14 per share if Lemtrada reaches $2.8

billion in annual sales.

Discussion Questions

1. The deal was structured as a tender offer coupled with a “top up” option to be followed by a backend short

form merger. Why might this structure be preferable to a more common statutory merger deal or a tender offer

followed by a backend merger requiring a shareholder vote?

Answer: Merger deals require target firm shareholder approvals which might delay the closing significantly,

giving rise to the potential for another bidder to appear, a dissident shareholder to gain support, or in an share

2. Speculate as to the purpose of the dual track model in which the bidder initiates a tender offer and

simultaneously files a prospectus to hold a shareholders meeting and vote on a merger

3. Describe the takeover tactics employed by Sanofi. Discuss why each one might have been used.

Answer: Sanofi was opportunistic in its approach to Genzyme. Timing was critical. Debt financing was

cheap, Genzyme’s share price was depressed, and its major competitors were too preoccupied to participate in

an auction for Genzyme. Sanofi wanted a friendly takeover to minimize disrupting efforts to improve the

firm’s manufacturing operations and to minimize the loss of key employees, customers, and suppliers that

often accompany vitriolic hostile takeover battles.

4. Describe the antitakeover strategy employed by Genzyme. Discuss why each may have been employed. In

your opinion, did the Genzyme strategy work?

29

5. What alternatives could Sanofi used instead of the CVR to bridge the difference in how the parties valued

Genzyme? Discuss the advantages and disadvantages of each.

Answer: A CVR is a specific type of an earnout. Under an earnout, a portion of the purchase price is deferred

and dependent on future events. It is used to bridge the gap between buyer and seller purchase price

expectations. A CVR is an increasingly popular version of an earnout in public company sales, especially the

pharmaceutical industry. CVRs are usually shorter in duration than earnouts and tied to the objectively

6. How might both the target and bidding firm benefit from the top-up option?

7. How might the existence of a CVR limit Sanofi’s ability to realize certain types of synergies? Be specific.

Answer: As is true with earnouts, the CVR may limit Sanofi’s ability to integrate the two firms in order to

realize certain cost reductions and operating efficiencies because the two firms must be operated separately. If

Swiss Pharmaceutical Giant Novartis Takes Control of Alcon

_________________________________________________________________________________________________

30

Key Points

Parent firms frequently find it appropriate to buy out minority shareholders to reduce costs and to simplify future decision

making.

Acquirers may negotiate call options with the target firm after securing a minority position to implement so-called

“creeping takeovers.”

_________________________________________________________________________________________________

In December 2010, Swiss pharmaceutical company Novartis AG completed its effort to acquire, for $12.9 billion, the

remaining 23% of U.S.-listed eye care group Alcon Incorporated (Alcon) that it did not already own. This brought the total

purchase price for 100% of Alcon to $52.2 billion. Novartis had been trying to purchase Alcon’s remaining publicly traded

shares since January 2010, but its original offer of 2.8 Novartis shares, valued at $153 per Alcon share, met stiff resistance

In 2008, with global financial markets in turmoil, Novartis acquired, for cash, a minority position in food giant Nestlé’s

wholly owned subsidiary Alcon. Nestlé had acquired 100% of Alcon in 1978 and retained that position until 2002, when it

undertook an IPO of 23% of its shares. In April 2008, Novartis acquired 25% of Alcon for $143 per share from Nestlé. As

part of this transaction, Novartis and Nestlé received a call and a put option, respectively, which could be exercised at $181

While the Nestlé deal seemed likely to receive regulatory approval, the offer to the minority shareholders was assailed

immediately as too low. At $153 per share, the offer was well below the Alcon closing price on January 4, 2010, of

$164.35. The Alcon publicly traded share price may have been elevated by investors’ anticipating a higher bid. Novartis

argued that without this speculation, the publicly traded Alcon share price would have been $137, and the $153 per share

price Novartis offered the minority shareholders would have represented an approximate 12% premium to that price. The

minority shareholders, who included several large hedge funds, argued that they were entitled to $181 per share, the amount

paid to Nestlé. Alcon’s publicly traded shares dropped 5% to $156.97 on the news of the Novartis takeover. Novartis’

shares also lost 3%, falling to $52.81. On August 9, 2010, Novartis received approval from European Union regulators to

buy the stake in Alcon, making it easier for it to take full control of Alcon.

With the buyout of Nestlé’s stake in Alcon completed, Novartis was now faced with acquiring the remaining 23% of the

outstanding shares of Alcon stock held by the public. Under Swiss takeover law, Novartis needed a majority of Alcon board

members and two-thirds of shareholders to approve the terms for the merger to take effect and for Alcon shares to convert

automatically into Novartis shares. Once it owned 77% of Alcon’s stock, Novartis only needed to place five of its own

31

Novartis’ patience appears to have worn thin. While not always the case, the resistance of the independent directors paid off

for those investors holding publicly traded shares.

Discussion Questions

1. Speculate as to why Novartis acquired only a 25 percent stake in Alcon in 2008.

Answer: Nestle may have been unwilling to sell more Alcon shares because of the depressed state of the

2. Why was the price ($181 per share) at which Novartis exercised its call option in 2010 to increase its stake in

Alcon to 77 so much higher than what it paid ($143 per share) for an approximate 25 percent stake in Alcon in

early 2008?

Answer: Novartis went from buying a 25 percent minority stake, subject to a minority discount from the

3. Alcon and Novartis shares dropped by 5 percent and 3 percent, respectively, immediately following the

announcement that Novartis would exercise its option to buy Nestle’s majority holdings of Alcon shares.

Explain why this happened.

4. How do Swiss takeover laws compare to comparable U.S. laws. Which are more appropriate and why?

Answer: U.S. law enables an acquirer owning more than 50.1 percent of another firm to force the minority

shareholders to sell their shares, often in exchange for preferred shares or debt. This is done to prevent a

6. Discuss how Novartis may have arrived at the estimate of $137 per share as the intrinsic value of

Alcon.

What are the key underlying assumptions? Do you believe that the minority shareholders should receive the

same price as Nestle?

Answer: Novartis argued that the $164 price of publicly traded Alcon stock prior to Novartis exercising its

call option reflected speculation that the eventual buyout of the minority shareholders of Alcon would take

32

Illustrating How Deal Structure Affects Value—The FaceBook / Instagram Deal

_________________________________________________________________________________________________

Key Points:

Deal structures affect value by limiting risk to the parties involved or exposing them to risk.

The value of cash received at closing is certain, whereas the value of stock is not.

Mechanisms exist to limit such risk; however, they often come with a cost to the party seeking risk mitigation.

_________________________________________________________________________________________________

While we always look smarter after the fact, social networking giant Facebook’s acquisition of Instagram, a popular photo–

sharing service, highlights risk common to such deals. Instagram’s user base was exploding; Facebook viewed it as a

potential competitor and as a means of extending its own product offering to photo sharing on smartphones and tablet

The purchase price consisted of $300 million in cash and 23 million shares of common stock for all of the outstanding

Instagram shares. The combination of cash and stock is usually offered to give selling-firm shareholders the favorable tax

advantages of acquirer stock, the certainty of cash, and the opportunity to participate in any potential appreciation of the

acquiring firm’s shares. The deal value was predicated on a Facebook share price of $31 per share, giving Facebook a

market value at the time of $75 billion. What is perhaps most remarkable about this transaction is the price paid, the speed

with which it was negotiated, and the absence of protections for the Instagram shareholders. These issues are discussed

next.

Called an important milestone by Facebook founder and CEO Mark Zuckerberg, the deal reflected the dangers of

valuing a firm primarily on its potential. This is an issue that Facebook tackled following its IPO on May 18, 2012.

Originally offered at $38 per share, the stock soon plummeted to less than half that value as investors doubted the firm’s

long-term profitability.

Facebook’s dual class shareholder structure gives Mr. Zuckerberg effective control of the firm, despite owning only

28.4% of outstanding class B shares. This control made it possible for the lofty valuation to be placed on Instagram and for

the deal to be negotiated so rapidly. Indeed, the Instagram offer price may have reflected the euphoria preceding the

Boston Scientific Overcomes Johnson & Johnson to Acquire Guidant—A Lesson in Bidding Strategy

Johnson & Johnson, the behemoth American pharmaceutical company, announced an agreement in December 2004 to

acquire Guidant for $76 per share for a combination of cash and stock. Guidant is a leading manufacturer of implantable

heart defibrillators and other products used in angioplasty procedures. The defibrillator market has been growing at 20

percent annually, and J&J desired to reenergize its slowing growth rate by diversifying into this rapidly growing market.

33

Soon after the agreement was signed, Guidant’s defibrillators became embroiled in a regulatory scandal over failure to

inform doctors about rare malfunctions. Guidant suffered a serious erosion of market share when it recalled five models of

its defibrillators.

The subsequent erosion in the market value of Guidant prompted J&J to renegotiate the deal under a material adverse

change clause common in most M&A agreements. J&J was able to get Guidant to accept a lower price of $63 a share in

Boston Scientific realized that it would be able to acquire Guidant only if it made an offer that Guidant could not refuse

without risking major shareholder lawsuits. Boston Scientific reasoned that if J&J hoped to match an improved bid, it

would have to be at least $77, slightly higher than the $76 J&J had initially offered Guidant in December 2004. With its

greater borrowing capacity, Boston Scientific knew that J&J also had the option of converting its combination stock and

cash bid to an all-cash offer. Such an offer could be made a few dollars lower than Boston Scientific’s bid, since Guidant

investors might view such an offer more favorably than one consisting of both stock and cash, whose value could fluctuate

between the signing of the agreement and the actual closing. This was indeed a possibility, since the J&J offer did not

include a collar arrangement.

Table 1

Boston Scientific and Johnson & Johnson Bidding Chronology

Date

Comments

December 15, 2004

J&J reaches agreement to buy Guidant for $25.4 billion in stock and cash.

November 15, 2005

Value of J&J deal is revised downward to $21.5 billion.

December 5, 2005

Boston Scientific offers $25 billion.

January 11, 2006

Guidant accepts a J&J counteroffer valued at $23.2 billion.

January 17, 2006

Boston Scientific submits a new bid valued at $27 billion.

January 25, 2006

A side deal with Abbott Labs made the lofty Boston Scientific offer possible. The firm entered into an agreement with

Abbott Laboratories in which Boston Scientific would divest Guidant’s stent business while retaining the rights to Guidant’s

stent technology. In return, Boston Scientific received $6.4 billion in cash on the closing date, consisting of $4.1 billion for

34

Between December 2004, the date of Guidant’s original agreement with J&J, and January 25, 2006, the date of its

agreement with Boston Scientific, Guidant’s stock rose by 16 percent, reflecting the bidding process. During the same

period, J&J’s stock dropped by a modest 3 percent, while Boston Scientific’s shares plummeted by 32 percent.

Discussion Questions

1. What were the key differences between J&J’s and Boston Scientific’s bidding strategy? Be specific.

Answer: J&J’s style could be characterized as self–assured and reactive and Boston Scientific’s as

opportunistic and nimble. J&J was willing to reopen their bid for Guidant by executing the material adverse

change clause in the agreement of purchase and sale and to renegotiate aggressively a much lower offer price.

While they had contractual right to do so, the nearly 21 percent reduction in the offer price demanded by J&J

appears to have been overly aggressive, perhaps with little regard for the possibility of attracting other

2. What might J&J have done differently to avoid igniting a bidding war?

Answer: Immediately following its announcement that it had reached an agreement to be acquired by Johnson

and Johnson (J&J), Guidant defibrillators became embroiled in a regulatory scandal over failure to inform

3. What evidence is given that J&J may not have taken Boston Scientific as a serious bidder?

Answer: J&J announced publicly that Guidant was fully valued at its cash and stock bid of $76 per Guidant

share. The firm refused to raise its bid to the higher Boston Scientific bid of $80, possibly believing that the

35

7. Explain how differing assumptions about market growth, potential synergies, and the size of the potential liability

related to product recalls affected the bidding?

Answer: The potential product related liability initiated the bidding war as it provided Boston Scientific with

an opportunity to intervene in what had been a signed agreement. J&J and Boston Scientific simply had

Buyer Consortium Wins Control of ABN Amro

The biggest banking deal on record was announced on October 9, 2007, resulting in the dismemberment of one of Europe’s

largest and oldest financial services firms, ABN Amro (ABN). A buyer consortium consisting of The Royal Bank of

Scotland (RBS), Spain’s Banco Santander (Santander), and Belgium’s Fortis Bank (Fortis) won control of ABN, the largest

bank in the Netherlands, in a buyout valued at $101 billion.

European banks had been under pressure to grow through acquisitions and compete with larger American rivals to avoid

becoming takeover targets themselves. ABN had been viewed for years as a target because of its relatively low share price.

However, rival banks were deterred by its diverse mixture of businesses, which was unattractive to any single buyer. Under

pressure from shareholders, ABN announced that it had agreed, on April 23, 2007, to be acquired by Barclay’s Bank of

Discussion Questions:

1. In your judgment, what are likely to be some of the major challenges in assembling a buyer consortium to acquire

and subsequently dismember a target firm such as ABN Amro? In what way do you thing the use of a single

investment advisor might have addressed some of these issues?

Answer: Finding willing and financially able partners with a synergistic fit to a specific target firm is difficult.

Multiple investment banking advisors for each consortium participant having different agendas could imperil the

2. The ABN Amro transaction was completed at a time when the availability of credit was limited due to the sub-

prime mortgage loan problem originating in the United States. How might the use of a group rather than a single

buyer have facilitated the purchase of ABN Amro?

36

3. The same outcome could have been achieved if a single buyer had reached agreement with other banks to acquire

selected pieces of ABN before completing the transaction. The pieces could then have been sold at the closing.

Why might the use of the consortium been a superior alternative?

Answer: Pre-selling businesses before closing is a technique that makes sense mostly for target firms whose assets

are managed largely independently. Consequently, such assets can be easily divested upon closing to other parties

Pfizer Acquires Wyeth Labs Despite Tight Credit Markets

Pfizer and Wyeth began joint operations on October 22, 2009, when Wyeth shares stopped trading and each Wyeth share

was converted to $33 in cash and 0.985 of a Pfizer share. Valued at $68 billion, the cash and stock deal was first announced

in late January of 2009. The purchase price represented a 12.6 percent premium over Wyeth’s closing share price the day

before the announcement. Investors from both firms celebrated as Wyeth’s shares rose 12.6 percent and Pfizer’s 1.4 percent

on the news. The announcement seemed to offer the potential for profit growth, despite storm clouds on the horizon.

As is true of other large pharmaceutical companies, Pfizer expects to experience serious erosion in revenue due to

expiring patent protection on a number of its major drugs. Pfizer faced the expiration of patent rights in 2011 to the

Pfizer’s strategy appears to have been to acquire Wyeth at a time when transaction prices were depressed because of the

recession and tight credit markets. Pfizer anticipates saving more than $4 billion annually by combining the two businesses,

with the savings being phased in over three years. Pfizer also hopes to offset revenue erosion due to patent expirations by

diversifying into vaccines and arthritis treatments.

By the end of 2008, Pfizer already had a $22.5 billion commitment letter in order to obtain temporary or “bridge”

financing and $26 billion in cash and marketable securities. Pfizer also announced plans to cut its quarterly dividend in half

to $0.16 per share to help finance the transaction. However, there were still questions about the firm’s ability to complete

the transaction in view of the turmoil in the credit markets.

Many transactions that were announced during 2008 were never closed because buyers were unable to arrange financing

and would later claim that the purchase agreement had been breached due to material adverse changes in the business

climate. Such circumstances, they would argue, would force them to renege on their contracts. Usually, such contracts