37

attempt to find alternative financing or terminate the agreement. If Wyeth had terminated the agreement, Pfizer would have

been obligated to pay the termination fee.

Using Form of Payment as a Takeover Strategy:

Chevron’s Acquisition of Unocal

Unocal ceased to exist as an independent company on August 11, 2005 and its shares were de-listed from the New York

Stock Exchange. The new firm is known as Chevron. In a highly politicized transaction, Chevron battled Chinese oil-

producer, CNOOC, for almost four months for ownership of Unocal. A cash and stock bid by Chevron, the nation’s second

largest oil producer, made in April valued at $61 per share was accepted by the Unocal board when it appeared that

CNOOC would not counter-bid. However, CNOOC soon followed with an all-cash bid of $67 per share. Chevron amended

the merger agreement with a new cash and stock bid valued at $63 per share in late July. Despite the significant difference

in the value of the two bids, the Unocal board recommended to its shareholders that they accept the amended Chevron bid

in view of the growing doubt that U.S. regulatory authorities would approve a takeover by CNOOC.

This mix of cash and stock implied that Chevron would pay approximately $7.5 billion (i.e., $27.60 x 272 million

Unocal shares outstanding) in cash and issue approximately 168 million shares of Chevron common stock (i.e., .618 x 272

million of Unocal shares) valued at $57.28 per share as of July 22, 2005. The implied value of the merger on that date was

$17.1 billion (i.e., $27.60 x 272 million Unocal common shares outstanding plus $57.28 x 168 million Chevron common

shares). An increase in Chevron’s share price to $63.15 on August 10, 2005, the day of the Unocal shareholders’ meeting,

boosted the value of the deal to $18.1 billion.

The agreement of purchase and sale between Chevron and Unocal contained a “proration clause.” This clause enabled

Chevron to limit the amount of total cash it would payout under those options involving cash that it had offered to Unocal

shareholders and to maintain the “blended” rate of $63 it would pay for each share of Unocal stock. Approximately 242

million Unocal shareholders elected to receive all cash for their shares, 22.1 million opted for the all-stock alternative, and

10.1 million elected the cash and stock combination. No election was made for approximately .3 million shares. Based on

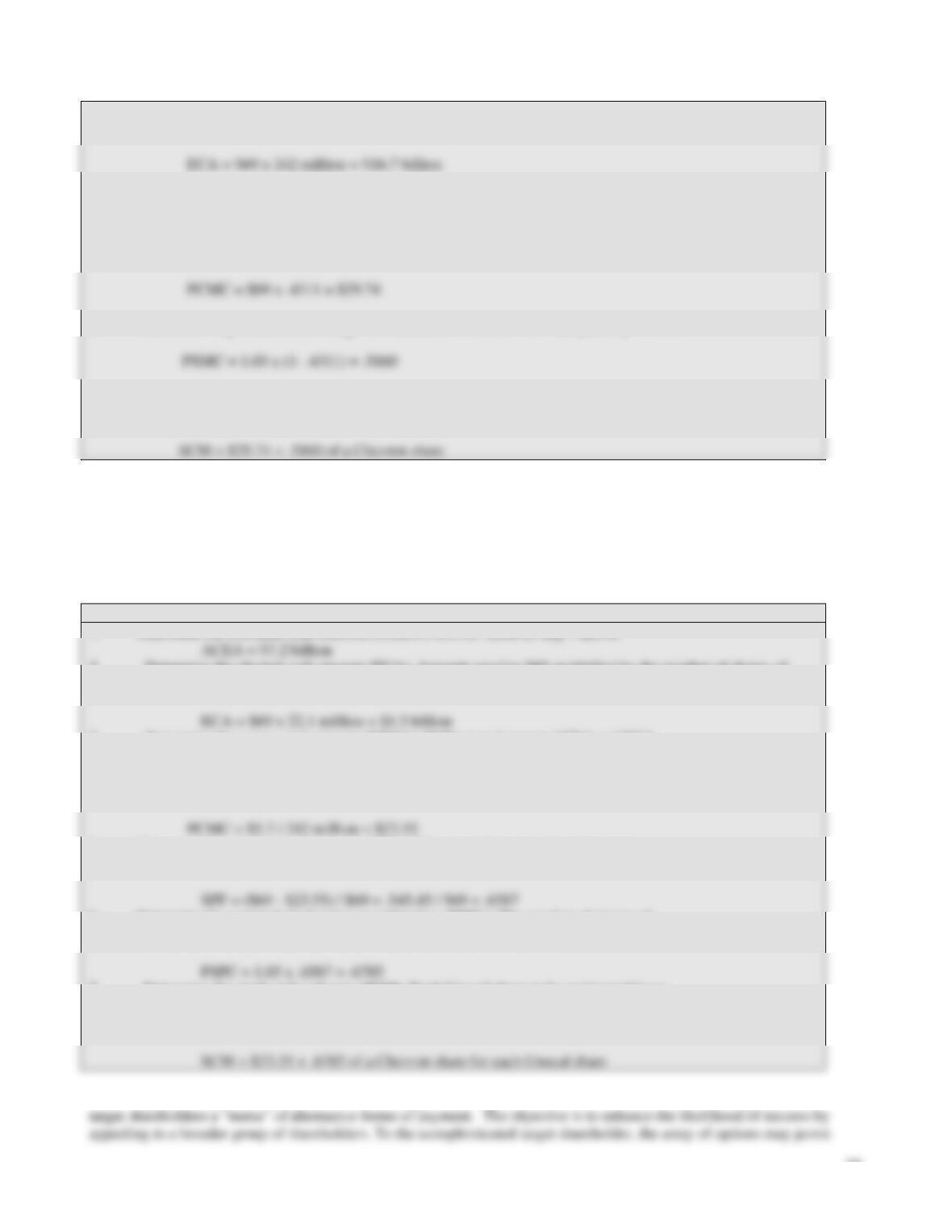

Exhibit 1. Prorating All-Cash Elections

1. Determine the available cash election amount (ACEA): Aggregate cash amount minus the amount of cash

to be paid to Unocal shareholders selecting the combination of cash and stock (i.e., Option 3).

ACEA = $27.60 x 272 million (Unocal shares outstanding) – 10.1

million (shares electing cash and stock option) x $27.60

38

2. Determine the elected cash amount (ECA): Amount equal to $69 multiplied by the

number of shares of Unocal common stock electing the all-cash option.

3. Determine the cash proration factor (CPF): ACEA/ECA

CPF = $7.2 / $16.7 = .4311

4. Determine the prorated cash merger consideration (PCMC): An amount in cash equal

to $69 multiplied by the cash proration factor.

5. Determine the prorated stock merger consideration (PSMC): 1.03 multiplied by 1 – CPF.

6. Determine the stock and cash mix (SCM): Sum of the prorated cash (PCMC) and stock

(PSMC) merger considerations exchanged for each share of Unocal common stock.

If too many Unocal shareholders had elected to receive Chevron stock, those making the all-stock election would not

have received 1.03 shares of Chevron stock for each share of Unocal stock. Rather, they would have received a mix of

stock and cash to help preserve the approximate 56 percent stock and 44 percent cash composition of the purchase price

desired by Chevron. For illustration only, assume the number of Unocal shares to be exchanged for the all-cash and all-

stock options are 22.1 and 242 million, respectively. This is the reverse of what actually happened. The mix of stock and

cash would have been prorated as shown in Exhibit 2.

Exhibit 12. Prorating All-Stock Elections

1. Determine the available cash election amount (ACEA): Same as step 1 above.

2. Determine the elected cash amount (ECA): Amount equal to $69 multiplied by the number of shares of

Unocal common stock electing the all-cash option.

3. Determine the excess cash amount (EXCA): Difference between ACEA and ECA.

EXCA = $7.2 – $1.5 = $5.7

4. Determine the prorated cash merger consideration (PCMC): EXCA divided by number of Unocal shares

elected the all-stock option.

5. Determine the stock proration factor (SPF): $69 minus the prorated cash merger

consideration divided by $69.

6. Determine the prorated stock price consideration (PSPC): The number of shares of

Chevron stock equal to 1.03 multiplied by the stock proration factor.

7. Determine the stock and cash mix (SCM): Each Unocal share to be exchanged in an

all-stock election is converted into the right to receive the prorated cash merger

consideration and the prorated stock merger consideration.

It is typical of large transactions in which the target has a large, diverse shareholder base that acquiring firms offer

39

appealing. However, it is likely that those electing all-cash or all-stock purchases are likely to be disappointed due to

probable proration clauses in merger contracts. Such clauses enable the acquirer to maintain an overall mix of cash and

stock in completing the transaction. This enables the acquirer to limit the amount of cash they must borrow or the number

of new shares they must issue to levels they find acceptable.

Discussion Questions

1. What was the form of payment employed by both bidders for Unocal? In your judgment, why were they

different? Be specific.

Answer: Chevron offered Unocal shareholders three options including all cash, all stock, and a combination of

both. CNOOC countered with an all-cash bid. CNOOC tried to appeal to those Unocal shareholders who wanted

2. How did Chevron use the form of payment as a potential takeover strategy?

3. Is the “proration clause” found in most merger agreements in which target shareholders are given several ways in

which they can choose to be paid for their shares in the best interests of the target shareholders? In the best

interests of the acquirer? Explain your answer.

Answer: While proration clauses are common in transactions involving multiple forms of payment, one could

argue that they are deceptive for unsophisticated target shareholders choosing an all-cash or all-stock bid. Such

Blackstone Outmaneuvers Vornado to Buy Equity Office Properties

Reflecting the wave of capital flooding into commercial real estate and the growing power of private equity investors, the

Blackstone Group (Blackstone) succeeded in acquiring Equity Office Properties (EOP) following a bidding war with

Vornado Realty Trust (Vornado). On February 8, 2007, Blackstone Group closed the purchase of EOP for $39 billion,

consisting of about $23 billion in cash and $16 billion in assumed debt.

EOP was established in 1976 by Sam Zell, a veteran property investor known for his ability to acquire distressed

properties. Blackstone, one of the nation’s largest private equity buyout firms, entered the commercial real estate market for

the first time in 2005. In contrast, Vornado, a publicly traded real estate investment trust, had a long-standing reputation for

savvy investing in the commercial real estate market. EOP’s management had been under fire from investors for failing to

sell properties fast enough and distribute the proceeds to shareholders.

40

Discussion Questions:

1. Describe Blackstone’s negotiating strategy with EOP in its effort to counter Vornado’s bids. Be specific.

Answer: Blackstone continued to increase its offer price in response to Vornado’s offers. However, each

Blackstone counteroffer was always less than the Vornado offer. Blackstone was relying on an all-cash price

2. What could Vornado have done to assuage EOP’s concerns about the certainty of the value of the stock

portion of its offer?

Answer: Vornado could have offered EOP shareholders a collar arrangement in which it would offer more

Vornado shares for each share of EOP if Vornado shares declined in value between the time of signing of a

3. Explain the reaction of EOP’s and Vornado’s share prices to the news that Blackstone was the winning bidder.

What does the movement in Vornado’s share price tell you about the likelihood that the firm’s shareholders

would have approved the takeover of EOP?

Answer: EOP’s share price dropped to just below the Blackstone offer price, reflecting the potential risk that

the deal would not close. Vornado’s share price rose sharply possibly as a result of investor relief that

Vivendi Universal and GE Combine Entertainment Assets to Form NBC Universal

Ending a four-month-long auction process, Vivendi Universal SA agreed on October 5, 2003, to sell its Vivendi Universal

Entertainment (VUE) businesses, consisting of film and television assets, to General Electric Corporation’s wholly owned

NBC subsidiary. Vivendi received a combination of GE stock and stock in the combined company valued at approximately

$14 billion. Vivendi would combine the Universal Pictures movie studio, its television production group, three cable

networks, and the Universal theme parks with NBC. The new company would have annual revenues of $13 billion based on

2003 pro forma statements.

Applying a multiple of 14 times estimated 2003 EBITDA of $3 billion, the combined company had an estimated value

of approximately $42 billion. This multiple is well within the range of comparable transactions and is consistent with the

share price multiples of television media companies at that time. Of the $3 billion in 2003 EBITDA, GE would provide $2

billion and Vivendi $1 billion. This values GE’s assets at $28 billion and Vivendi’s at $14 billion. This implies that GE

assets contribute two thirds and Vivendi’s one third of the total market value of the combined company.

41

Discussion Questions:

1. From a legal standpoint, identify the acquirer and the target firms?

2. What is the form of acquisition? Why might the parties involved in the transaction have agreed to this form?

Answer: Purchase of assets. The purchase of assets allows GE/NBC to acquire only assets it finds most attractive.

3. What is the form of acquisition vehicle and the post-closing organization? Why do you think the legal entities you

have identified were selected?

4. What is the form of payment or total consideration? Why do you think this form of payment may have been

selected by the parties involved?

5. Is this transaction likely to be non-taxable, wholly taxable, or partially taxable to Vivendi? Explain your answer.

6. Based on a total valuation of $42 billion, Vivendi’s assets contributed one–third and GE’s two-thirds of the total

value of NBC Universal. However, after the closing, Vivendi would only own a 20% equity position in the

combined business. Why?

Answer: Vivendi’s contribution to the $42 billion was estimated to be $14 billion or approximately one-third of

the total value. However, Vivendi choose to receive a liquidity infusion at closing totaling $5.4 billion, while

News Corp.’s Power Play in Satellite Broadcasting

The share prices of Rupert Murdoch’s News Corp., Fox Entertainment Group Inc., and Hughes Electronics

Corp. (a subsidiary of General Motors Corporation) tumbled immediately following the announcement that

News Corp had reached an agreement to take a controlling interest in Hughes on April 10, 2003.

News Corp.’s Chairman Rupert Murdoch, had pursued control of Hughes, the parent company of

DirecTV, for several years. News Corp.’s bid valued at about $6.6 billion to acquire control of Hughes

Electronics Corp. and its DirecTV unit gives News Corp a U.S. presence to augment its satellite TV

operations in Britain and Asia. In one bold move, News Corp became the second largest provider of pay-

TV service to U.S. homes, second only to Comcast. By transferring News Corp.’s stake in Hughes to Fox,

Fox gained control over 11 million subscribers. It gives Fox more leverage for its cable networks when

negotiating rights fees with cable operators that compete with DirecTV. In negotiating with film studios or

sports companies over pay television rights, News Corp. is now the only global customer, with satellite

News Corp. financed its purchase of a 34.1% stake in Hughes (i.e., GM’s 20% ownership and 14.1%

from public shareholders) by paying $3.1 billion in cash to GM, plus 34.3 million in nonvoting American

depository receipts (ADRs) in News Corp. shares. Hughes’ public shareholders will be paid with 122.2

million nonvoting ADRs in News Corp. Each ADR is equivalent to four News Corp. shares. The resulting

issue of 156.5 million shares would dilute News Corp. shareholders by about 13%. Immediately following

closing, News Corp.’s ownership interest was transferred to Fox in exchange for a $4.5 billion promissory

Discussion Questions:

1. Why did the share prices of News Corp., Fox, and Hughes fall precipitously following the

announcement? Explain your answer.

43

2. How did News Corp.’s proposed deal structure better satisfy GM’s needs than those of other

bidders?

3. How can it be said that News Corp. obtained a controlling interest in Hughes when its stake

amounted to only about one-third of Hughes outstanding voting shares? Explain your answer.

Answer: News Corp acquired GM’s 20% block and 14.1% of the public shareholders’ stock. The

Determining Deal Structuring Components

BigCo has decided to acquire Upstart Corporation, a leading supplier of a new technology believed to be crucial to the

successful implementation of BigCo’s business strategy. Upstart is a relatively recent start-up firm, consisting of about 200

employees averaging about 24 years of age. HiTech has a reputation for developing highly practical solutions to complex

technical problems and getting the resulting products to market very rapidly. HiTech employees are accustomed to a very

informal work environment with highly flexible hours and compensation schemes. Decision-making tends to be fast and

casual, without the rigorous review process often found in larger firms. This culture is quite different from BigCo’s more

highly structured and disciplined environment. Moreover, BigCo’s decision making tends to be highly centralized.

While Upstart’s stock is publicly traded, its six co-founders and senior managers jointly own about 60 percent of the

outstanding stock. In the four years since the firm went public, Upstart stock has appreciated from $5 per share to its

current price of $100 per share. Although they desire to sell the firm, the co-founders are interested in remaining with the

Discussion Questions:

1. What is the acquisition vehicle used to acquire the target company, Upstart Corporation? Why was this legal

structure used?

44

2. How would you characterize the post-closing organization? Why was this organizational structure used?

Answer: The post closing organization is a holding company framework. This post closing structure was chosen

3. What is the form of payment? Why was it used?

Answer: The form of payment is a combination of cash and stock for the Upstart’s outstanding stock. This form of

4. What was the form of acquisition? How does this form of acquisition protect the acquiring company’s rights to

HiTech’s proprietary technology?

Answer: The form of acquisition was a purchase of stock. This is preferable in this instance because of the

5. How would the use of purchase accounting affect the balance sheets of the combined companies?

Answer: Assuming the acquirer adopted a Section 338 election, Upstart’s assets would have been revalued with a

portion of purchase price being allocated to its tangible and intangible assets. Any unallocated portion of the

6. Was the transaction non-taxable, partially taxable, or wholly taxable to HiTech shareholders? Why?

Consolidation in the Wireless Communications Industry: Vodafone Acquires AirTouch

.

Deregulation of the telecommunications industry has resulted in increased consolidation. In Europe, rising competition is

the catalyst driving mergers. In the United States, the break up of AT&T in the mid-1980s and the subsequent deregulation

of the industry has led to key alliances, JVs, and mergers, which have created cellular powerhouses capable of providing

nationwide coverage. Such coverage is being achieved by roaming agreements between carriers and acquisitions by other

carriers. Although competition has been heightened as a result of deregulation, the telecommunications industry continues

to be characterized by substantial barriers to entry. These include the requirement to obtain licenses and the need for an

extensive network infrastructure. Wireless communications continue to grow largely at the expense of traditional landline

services as cellular service pricing continues to decrease. Although the market is likely to continue to grow rapidly, success

is expected to go to those with the financial muscle to satisfy increasingly sophisticated customer demands. What follows is

a brief discussion of the motivations for the merger between Vodafone and AirTouch Communications. This discussion

includes a description of the key elements of the deal structure that made the Vodafone offer more attractive than a

competing offer from Bell Atlantic.

Vodafone

Company History

Vodafone is a wireless communications company based in the United Kingdom. The company is located in 13 countries in

Europe, Africa, and Australia/New Zealand. Vodafone reaches more than 9.5 million subscribers. It has been the market

45

leader in the United Kingdom since 1986 and as of 1998 had more than 5 million subscribers in the United Kingdom alone.

Strategic Intent

Vodafone’s focus is on global expansion. They are expanding through partnerships and by purchasing licenses. Notably,

Vodafone lacked a significant presence in the United States, the largest mobile phone market in the world. For Vodafone to

Company Structure

The company is very decentralized. The responsibilities of the corporate headquarters in the United Kingdom lie in

AirTouch

Company History

AirTouch Communications launched its first cellular service network in 1984 in Los Angeles during the opening

ceremonies at the 1984 Olympics. The original company was run under the name PacTel Cellular, a subsidiary of Pacific

Strategic Intent

AirTouch has chosen to differentiate itself in its domestic regions based on the concept of “Superior Service Delivery.” The

company’s focus is on being available to its customers 24 hours a day, 7 days a week and on delivering pricing options that

Company Structure

AirTouch is decentralized. Regions have been developed in the U.S. market and are run autonomously with respect to

pricing decisions, marketing campaigns, and customer care operations. Each region is run as a profit center. Its European

Merger Highlights

Vodafone began exploratory talks with AirTouch as early as 1996 on a variety of options ranging from partnerships to a

merger. Merger talks continued informally until late 1998 when they were formally broken off. Bell Atlantic, interested in

Motivation for the Merger

Shared Vision

The merger would create a more competitive, global wireless telecommunications company than either company could

achieve separately. Moreover, both firms shared the same vision of the telecommunications industry. Mobile

Complementary Assets

Scale, operating strength, and complementary assets were given as compelling reasons for the merger. The combination of

AirTouch and Vodafone would create the largest mobile telecommunication company at the time, with significant presence

in the United Kingdom, United States, continental Europe, and Asian Pacific region. The scale and scope of the operations

Synergy

Anticipated synergies include after-tax cost savings of $340 million annually by the fiscal year ending March 31, 2002. The

estimated net present value of these synergies is $3.6 billion discounted at 9%. The cost savings arise from global

AirTouch’s Board Analyzes Options

Morgan Stanley, AirTouch’s investment banker, provided analyses of the current prices of the Vodafone and Bell Atlantic

stocks, their historical trading ranges, and the anticipated trading prices of both companies’ stock on completion of the

merger and on redistribution of the stock to the general public. Both offers were structured so as to constitute essentially

Table 1. Comparison of Form of Payment/Total Consideration

Vodafone

Bell Atlantic

5 shares of Vodafone common plus $9 for each

share of AirTouch common

1.54 shares of Bell Atlantic for each share of AirTouch common

subject to the transaction being treated as a pooling of interest under

47

Morgan Stanley’s primary conclusions were as follows:

1. Bell Atlantic had a current market value of $83 per share of AirTouch stock based on the $53.81 closing price of Bell

2. The Vodafone proposal had a current market value of $97 per share of AirTouch stock based on Vodafone’s ordinary

shares (i.e., common) on January 17, 1999.

3. Following the merger, the market value of the Vodafone American Depository Shares (ADSs) to be received by

AirTouch shareholders under the Vodafone proposal could decrease.

4. Following the merger, the market value of Bell Atlantic’s stock also could decrease, particularly in light of the

expectation that the proposed transaction would dilute Bell Atlantic’s EPS by more than 10% through 2002.

In addition to Vodafone’s higher value, the board tended to favor the Vodafone offer because it involved less regulatory

uncertainty. As U.S. corporations, a merger between AirTouch and Bell Atlantic was likely to receive substantial scrutiny

from the U.S. Justice Department, the Federal Trade Commission, and the FCC. Moreover, although both proposals could

Acquisition Vehicle and Post Closing Organization

In the merger, AirTouch became a wholly owned subsidiary of Vodafone. Vodafone issued common shares valued at $52.4

billion based on the closing Vodafone ADS on April 20, 1999. In addition, Vodafone paid AirTouch shareholders $5.5

billion in cash. On completion of the merger, Vodafone changed its name to Vodafone AirTouch Public Limited Company.

Vodafone created a wholly owned subsidiary, Appollo Merger Incorporated, as the acquisition vehicle. Using a reverse

Discussion Questions:

48

1. Did the AirTouch board make the right decision? Why or why not?

2. How valid are the reasons for the proposed merger?

Answer: Vodafone was intent on becoming a global carrier. To achieve this goal, it was necessary for the firm to

achieve substantial coverage in the U.S. By acquiring AirTouch, Vodafone was able to obtain a substantial

3. What are the potential risk factors related to the merger?

Answer: The risks include the potential for having overpaid and for not being able to earn Vodafone’s cost of

capital on the acquired assets. Moreover, the acquisition was made with the understanding that the global market

4. Is this merger likely to be tax free, partially tax free, or taxable? Explain your answer.

5. What are some of the challenges the two companies are likely to face while integrating the businesses?

Answer: While no integration is ever easy, the two companies are compatible in many ways. They are managed

on a decentralized basis, have a shared vision of how to grow the cellular business, and have relatively young

workforces. However, both firms have employed the use of partnering arrangements to extend their cellular

JDS Uniphase–SDL Merger Results in Huge Write-Off

What started out as the biggest technology merger in history up to that point saw its value plummet in line with the

declining stock market, a weakening economy, and concerns about the cash-flow impact of actions the acquirer would have

to take to gain regulatory approve. The $41 billion mega-merger, proposed on July 10, 2000, consisted of JDS Uniphase

(JDSU) offering 3.8 shares of its stock for each share of SDL’s outstanding stock. This constituted an approximate 43%

premium over the price of SDL’s stock on the announcement date. The challenge facing JDSU was to get Department of

Given the size of the premium, JDSU’s management was unwilling to protect SDL’s shareholders from this possibility

by providing a “collar” within which the exchange ratio could fluctuate. The absence of a collar proved particularly

The Participants

JDSU manufactures and distributes fiber-optic components and modules to telecommunication and cable systems providers

worldwide. The company is the dominant supplier in its market for fiber-optic components. In 1999, the firm focused on

making only certain subsystems needed in fiber-optic networks, but a flurry of acquisitions has enabled the company to

offer complementary products. JDSU’s strategy is to package entire systems into a single integrated unit, thereby reducing

the number of vendors that fiber network firms must deal with when purchasing systems that produce the light that is

As of July 10, 2000, JDSU had a market value of $74 billion with 958 million shares outstanding. Annual 2000 revenues

amounted to $1.43 billion. The firm had $800 million in cash and virtually no long-term debt. Including one-time merger-

related charges, the firm recorded a loss of $905 million. With its price-to-earnings (excluding merger-related charges) ratio

at a meteoric 440, the firm sought to use stock to acquire SDL, a strategy that it had used successfully in eleven previous

acquisitions. JDSU believed that a merger with SDL would provide two major benefits. First, it would add a line of lasers

to the JDSU product offering that strengthened signals beamed across fiber-optic networks. Second, it would bolster

JDSU’s capacity to package multiple components into a single product line.

The Deal Structure

On July 9, 2000, the boards of both JDSU and SDL unanimously approved an agreement to merge SDL with a newly

formed, wholly owned subsidiary of JDS Uniphase, K2 Acquisition, Inc. K2 Acquisition, Inc. was created by JDSU as the

acquisition vehicle to complete the merger. In a reverse triangular merger, K2 Acquisition Inc. was merged into SDL,

with SDL as the surviving entity. The postclosing organization consisted of SDL as a wholly owned subsidiary of JDS

Uniphase. The form of payment consisted of exchanging JDSU common stock for SDL common shares. The share

exchange ratio was 3.8 shares of JDSU stock for each SDL common share outstanding. Instead of a fraction of a share,

each SDL stockholder received cash, without interest, equal to dollar value of the fractional share at the average of the

closing prices for a share of JDSU common stock for the 5 trading days before the completion of the merger.

50

The Aftermath of Overpaying

Despite dramatic cost-cutting efforts, the company reported a loss of $7.9 billion for the quarter ending June 31, 2001 and

$50.6 billion for the 12 months ending June 31, 2001. This compares to the projected pro forma loss reported in the

September 9, 2000 S4 filing of $12.1 billion. The actual loss was the largest annual loss ever reported by a U.S. firm up to

that time. The fiscal year 2000 loss included a reduction in the value of goodwill carried on the balance sheet of $38.7

Discussion Questions:

1. What is goodwill? How is it estimated? Why did JDS Uniphase write down the value of its goodwill in 2001?

Why does this reflect a series of poor management decisions with respect to mergers completed between 1999 and

early 2001?

Answer: In theory, goodwill represents the value of the acquired firm’s intangible value including brand,

intellectual property, good customer relations, and high employee morale. Goodwill is calculated as the excess of

the purchase price over the target’s net book assets (i.e., the sum of the book value of equity of the acquired

2. How might the use of stock, as an acquisition “currency,” have contributed to the sustained decline in JDS

Uniphase’s stock through mid-2001? In your judgment what is the likely impact of the glut of JDS Uniphase

shares in the market on the future appreciation of the firm’s share price? Explain your answer.

Answer: The lofty JDSU share price in 1999 and early 2000 made it a very attractive acquisition “currency.”

3. What are the primary differences between a forward and a reverse triangular merger? Why might JDS Uniphase

have chosen to merge its K2 Acquisition Inc. subsidiary with SDL in a reverse triangular merger? Explain your

answer.

51

Answer: Forward triangular mergers are used in tax-free asset acquisitions, no more than 50% of the purchase

price can be cash, and either voting or non-voting stock may be used. A reverse triangular merger is used in tax-

free stock acquisitions, only 20% of the purchase price may be cash, and only voting stock may be used in the

4. Discuss various methodologies you might use to value assets acquired from SDL such as existing technologies,

“core” technologies, trademarks and trade names, assembled workforce, and deferred compensation?

Answer: The value of intellectual property may be estimated by looking at recent comparable sales, by estimating

the cost of replacing such assets, by computing the present value of royalties generated if such assets were

5. Why do boards of directors of both acquiring and target companies often obtain so-called “fairness opinions” from

outside investment advisors or accounting firms? What valuation methodologies might be employed in

constructing these opinions? Should stockholders have confidence in such opinions? Why/why not?

Answer: Fairness opinions are often obtained to minimize potential liability from shareholder lawsuits which

might ensue if it is later determined that the acquirer “overpaid” for the target firm or that the target firm’s