Accounting Information Systems, 10e 1

SOLUTIONS FOR CHAPTER 11

Each end-of-chapter question in the Solutions Manual is tagged to correspond with AACSB, AICPA

and CISA standards, allowing professors to more easily manage the task of reporting outcomes to these

professional and accrediting bodies. Please see the corresponding spreadsheet file for the tagging

information.

Discussion Questions

DQ 11-1 Develop several examples of possible goal conflicts among the various managers

and supervisors depicted in Figure 11.1.

ANS. Some examples might include the following:

• Accounts receivable wanting to record only a good check, delays recording

DQ 11-2 Based upon the definition of float presented in the chapter, discuss several

possibilities for improving the cash float for your company, assuming you are the

cashier.

ANS. Float is defined as “the time between the customer’s tendering payment and the

availability of good funds, where goods funds are funds on deposit and available

2 Solutions for Chapter 11

DQ 11-3 Using Figure 11.6, speculate about the kinds of data that might be running along

the data flow that comes from the accounts receivable master data to bubble 2.1.

Be specific and be prepared to defend your answer by discussing the use(s) to

which each of those data elements could be put.

ANS. The data flow might indicate the following:

• That the customer had been billed for the item being returned. A customer

should only be permitted to return items actually purchased. However, if the

DQ 11-4 Discuss the information content of Figure 11.7. How might this report be used by

the credit manager or by the accounts receivable manager? If you were either of

these managers, what other reports concerning accounts receivable might you

find useful and how would you use them? Be specific.

ANS. The report portrays an aging of the open accounts receivables. The credit manager

Accounting Information Systems, 10e 3

DQ 11-5 Consult the systems flowcharts of Figures 11.11 and 11.13. Discuss how each of

these processes implements the concept of segregation of duties discussed in

Chapter 8. For each of the two processes, be specific as to which entity (or

entities) performs each of the four data processing functions mentioned in

Chapter 8 (assuming that all four functions are illustrated by the process).

ANS.

Function

Entity in Figure 11.11

Entity in Figure 11.13

Authorizing events.

Accounts receivable (billing

section) selects the

shipments to be billed.

Recording events.

Computer updates the

accounts receivable, sales,

and general ledger data.

Computer updates the cash

receipts, accounts

receivable, and general

Accounts receivable

(payment applications)

authorizes the updates to AR

4 Solutions for Chapter 11

DQ 11-6 a. Discuss the conditions under which each of the following billing processes are

most appropriate: (1) pre-billing system, and (2) post-billing system.

ANS. A pre-billing process is appropriate if:

• The shipping cost can be determined at the time that the order is entered.

ANS. The seller may prefer pre-billing because the invoice-preparation process is a

simple, one-step process: The bill is sent quickly, and cash receipts should be

DQ 11-7 “Pre–billing sounds like the type of process used for catalog and Internet sales.”

Do you agree? Discuss fully.

ANS. Not exactly. Catalog and Internet sales are typically paid for with a credit or debit

card, precluding the need for an invoice. So, while there is a “billing” to the card

Short Problems

SP 11-1

Accounting Information Systems, 10e 5

ANS. EBPP systems reduce the time between billing and cash receipt and reduce float

for the payee (the time between the tendering of payment and the availability of

cash). Because the bill is electronically presented and then electronically paid, the

SP 11-2 ANS. We can suggest the following changes to the Otis Company cash receipts process:

• The check log should be compared—either one-for-one or batch totals—to

validated deposit slips (returned from the bank indicating validity and

SP 11-3 ANS.

6 Solutions for Chapter 11

Function

Risks

Controls and Technology

Marketing

Lose customers (poor customer

service)

• Accurate and timely billing and payments

processing

• Monitor customer service

Collections

Cash (debit)

AR (credit)

Late collections

• Monitor open receivables

• Electronic payments

• Lockbox

Post payment to incorrect

account or with wrong amount

• Electronic payments (reduces data entry

• Electronic payments

• Confirm customer accounts

SP 11-4 ANS. See Figures SM-11.1 and SM-11.2. Figure SM-11.1 shows how bubble 3.0

in Figure 11.3 would be shown to reflect the fact that customers make their

Accounting Information Systems, 10e 7

FIGURE SM–11.1 Short Problem 4, Solution—Changes for Figure 11.3

FIGURE SM-11.2 Short Problem 4, Solution—Lower-Level View of Figure SM-11.1

8 Solutions for Chapter 11

SP 11-5 ANS.

1. C

SP 11-6 ANS.

1. F

2. E

Problems

Problems 1 and 2

Note: In the pages that follow, we provide solutions for problems 1 and 2 for all of the Case

Studies (Cases A through D). Case A is a cash receipts process with paper checks; Case B an

electronic billing and cash receipts process; Case C a billing process with paper invoices; and

Case D a cash receipts process with paper checks. Although the solution for each case study

comprises several pages, it is not necessarily comprehensive, nor does it represent the only

acceptable answers. Your or your students’ answers easily may vary in two areas. First, the

Accounting Information Systems, 10e 9

Fred’s Electrical, Inc. (Cash Receipts) Solutions (see Note on pg. 8)

P 11-1 ANS. a. Table of Entities and Activities for Fred’s (Cash Receipts)

Entities

Para

Activities

Customers

1

1. Mail payment to Fred’s.

Accounts receivable

1

2. Compare check to RA.

1

3. Prepare batch totals.

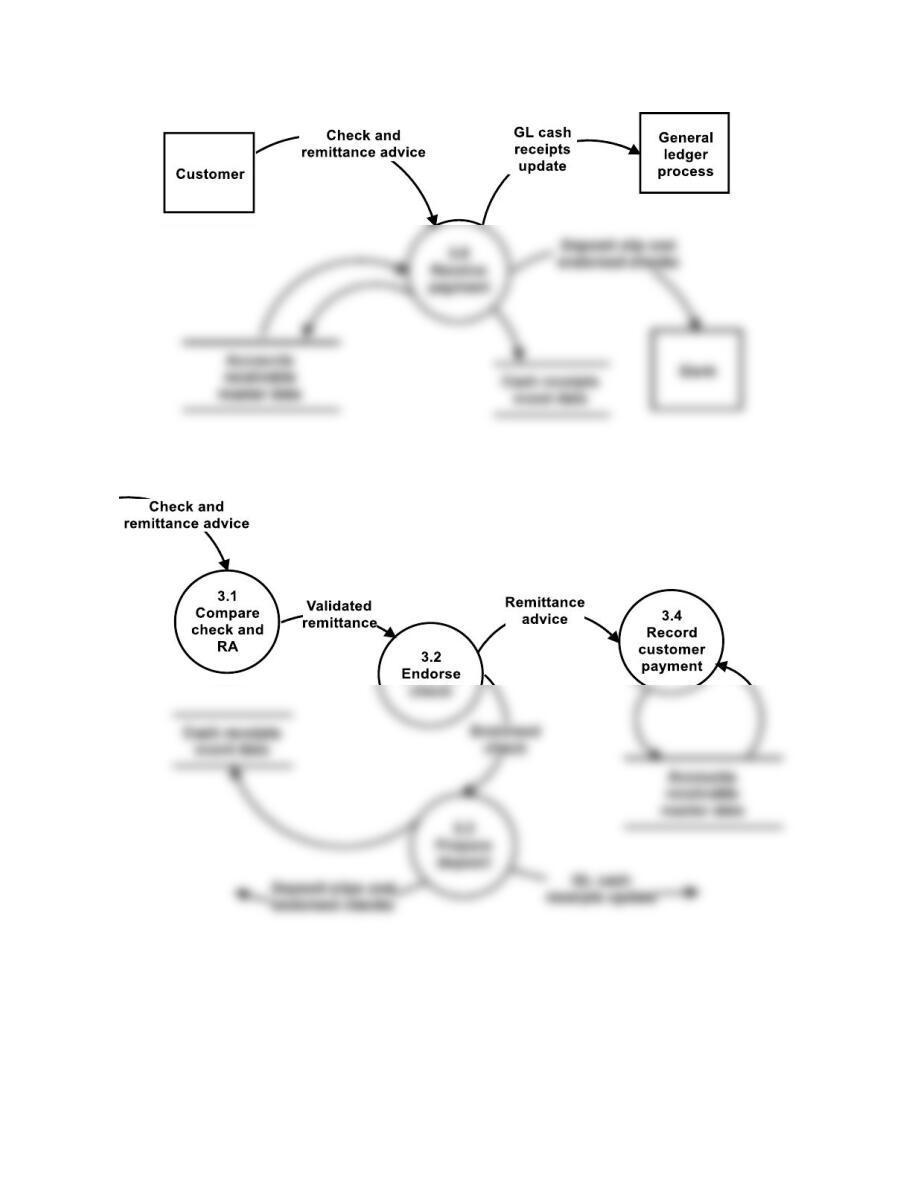

FIGURE SM-11.3 Problem 1, Part b Solution—Context Diagram for Fred’s Electrical, Inc.

(Cash Receipts)

1

1

5. Enter batch totals and payments.

Cashier

1

Computer

1

6. Update AR master data.

1

7. Reconcile batch totals.

1

1

9. Report discrepancies.

10 Solutions for Chapter 11

FIGURE SM-11.4 Problem 1, Part c Solution—Physical DFD for Fred’s Electrical, Inc.

(Cash Receipts)

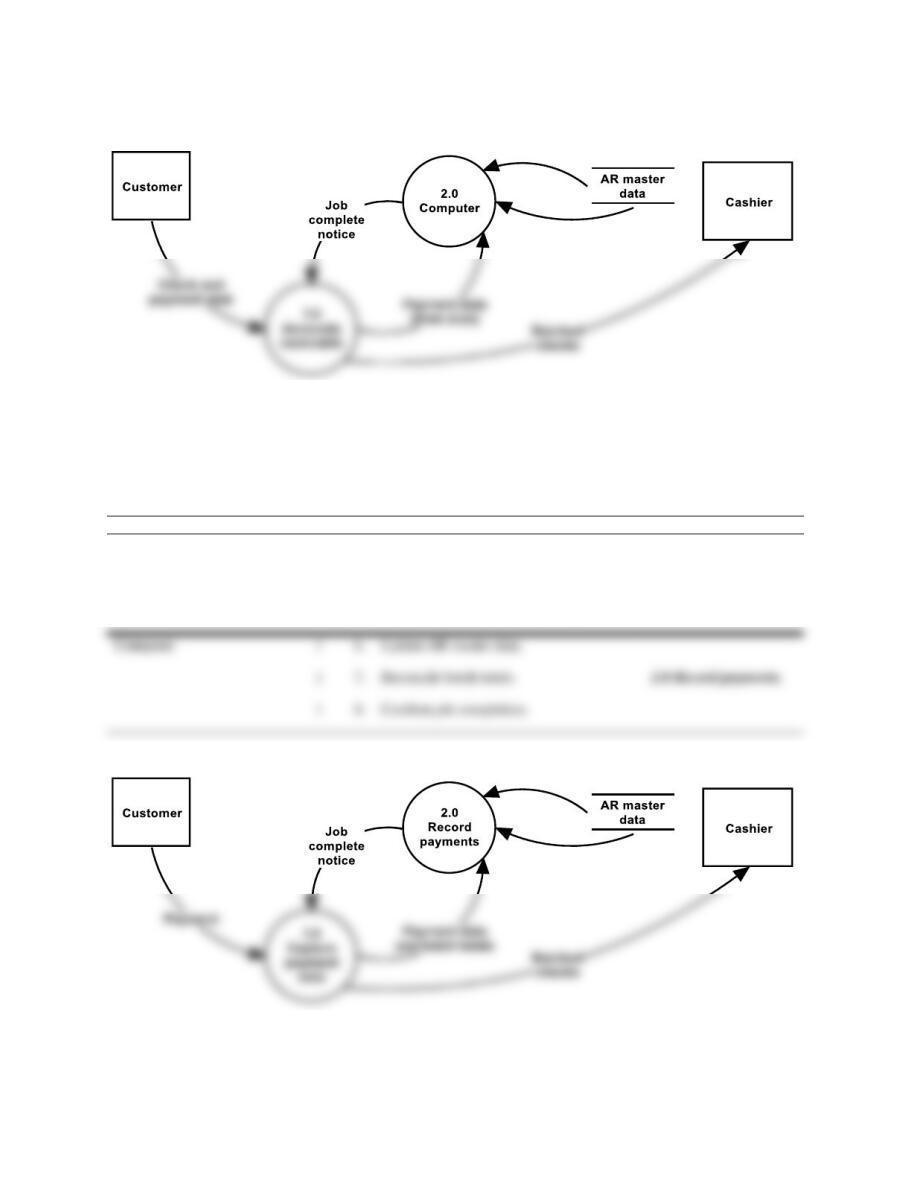

d. Table of Entities and Activities (Annotated) for Fred’s Electrical, Inc. (Billing and Cash

Receipts)

Entities

Para

Activities

Process

Accounts receivable

1

2. Compare check to RA

1.0 Capture payment-

data.

1

3. Prepare batch totals.

1

5. Enter batch totals and payments.

FIGURE SM-11.5 Problem 1, Part e Solution—Logical DFD for Fred’s Electrical, Inc. (Cash

Receipts)

Computer

1

6. Update AR master data.

1

8. Confirm job completion.

Accounting Information Systems, 10e 11

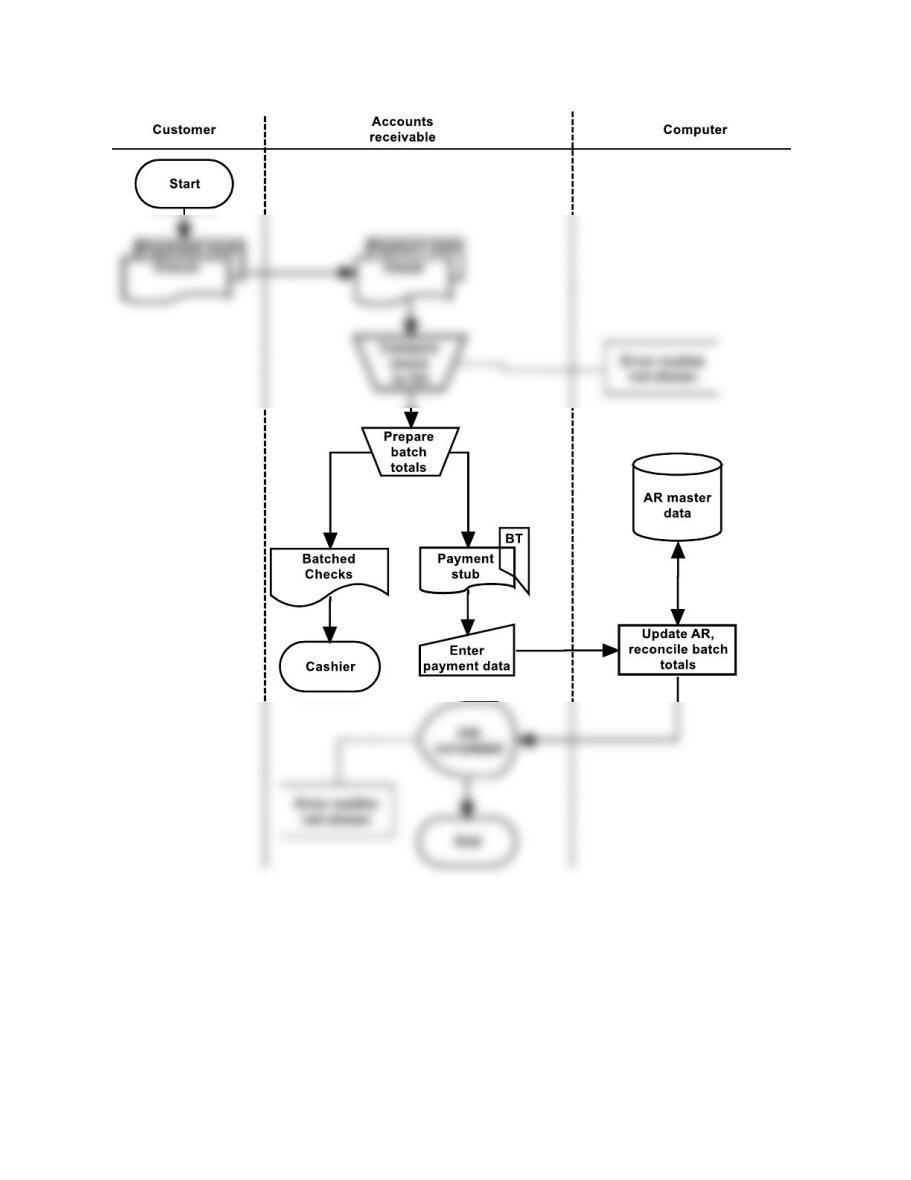

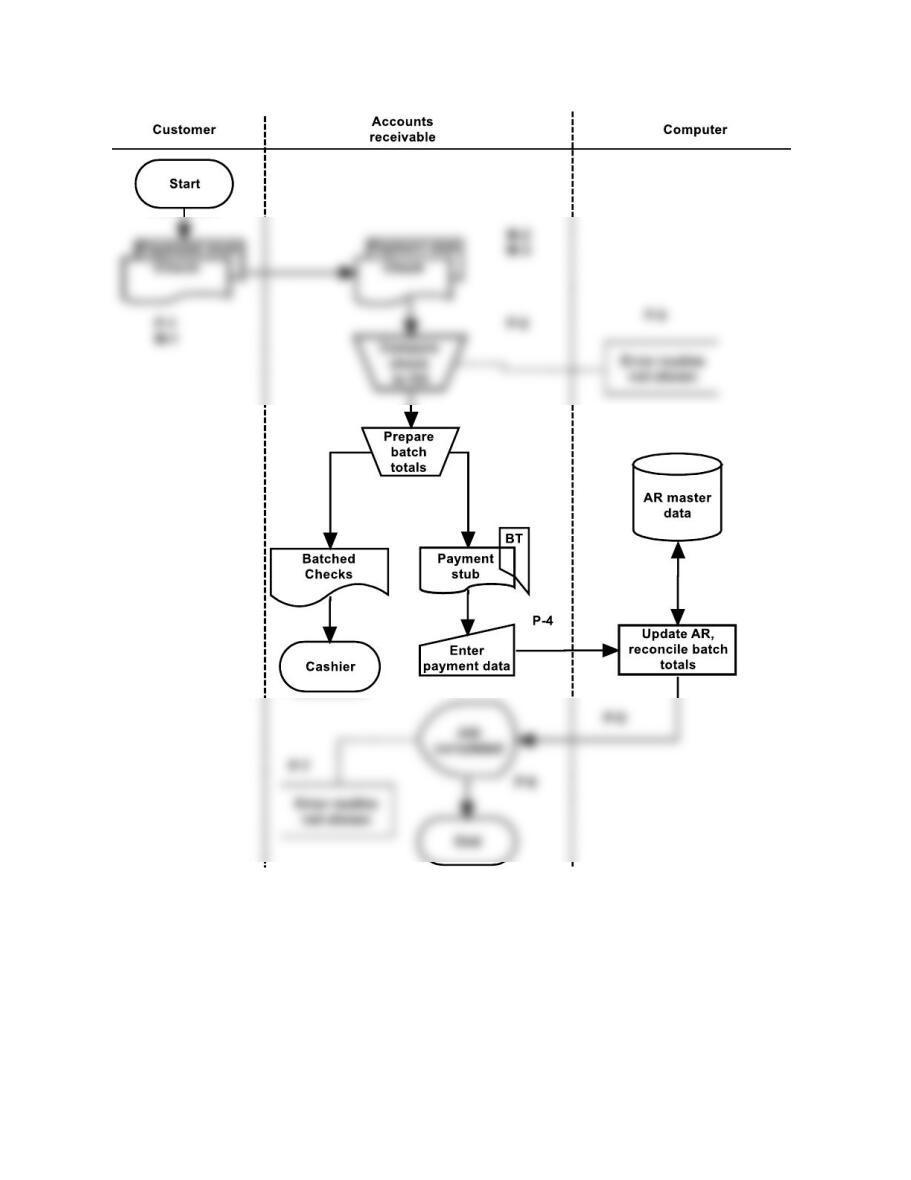

FIGURE SM-11.6 Problem 2, Part a Solution—Systems Flowchart for Fred’s Electrical, Inc.

(Cash Receipts)

12 Solutions for Chapter 11

Control Goals of the Fred’s Electrical, Inc. Cash Receipts Business Process

Control Goals of the Operations Process

Control Goals of the Information Process

Recommended control

plans

Ensure

effectiveness of

operations

Ensure

efficient

employ-

ment of

resources

(e.g., people

and

computers)

Ensure

security of

resources

(e.g., cash,

accounts

receivable

master

data)

For the remittance advice

inputs (i.e., cash receipts),

ensure:

For the accounts

receivable master

data, ensure:

A

B

C

IV

IC

IA

UC

UA

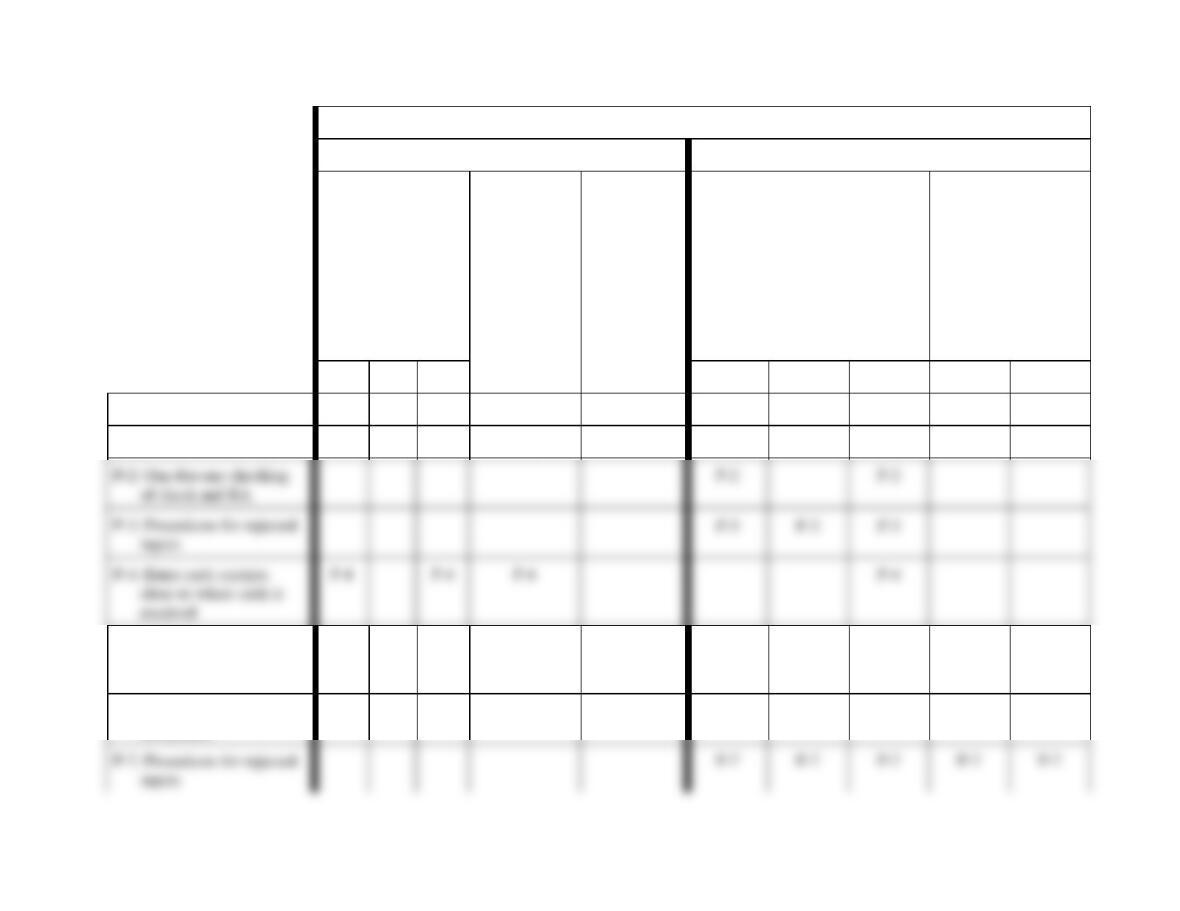

Present controls

P-1: Turnaround document

P-1

P-1

P-5: Computer agreement of

input and output batch

totals

P-5

P-5

P-5

P-5

P-5

P-5

P-6: Confirm input

acceptance

P-6

P-6

P-3: Procedures for rejected

P-3

P-3

Accounting Information Systems, 10e 13

Control Goals of the Fred’s Electrical, Inc. Cash Receipts Business Process

Control Goals of the Operations Process

Control Goals of the Information Process

Recommended control

plans

Ensure

effectiveness of

operations

Ensure

efficient

employ-

ment of

resources

(e.g., people

and

computers)

Ensure

security of

resources

(e.g., cash,

accounts

receivable

master

data)

For the remittance advice

inputs (i.e., cash receipts),

ensure:

For the accounts

receivable master

data, ensure:

A

B

C

IV

IC

IA

UC

UA

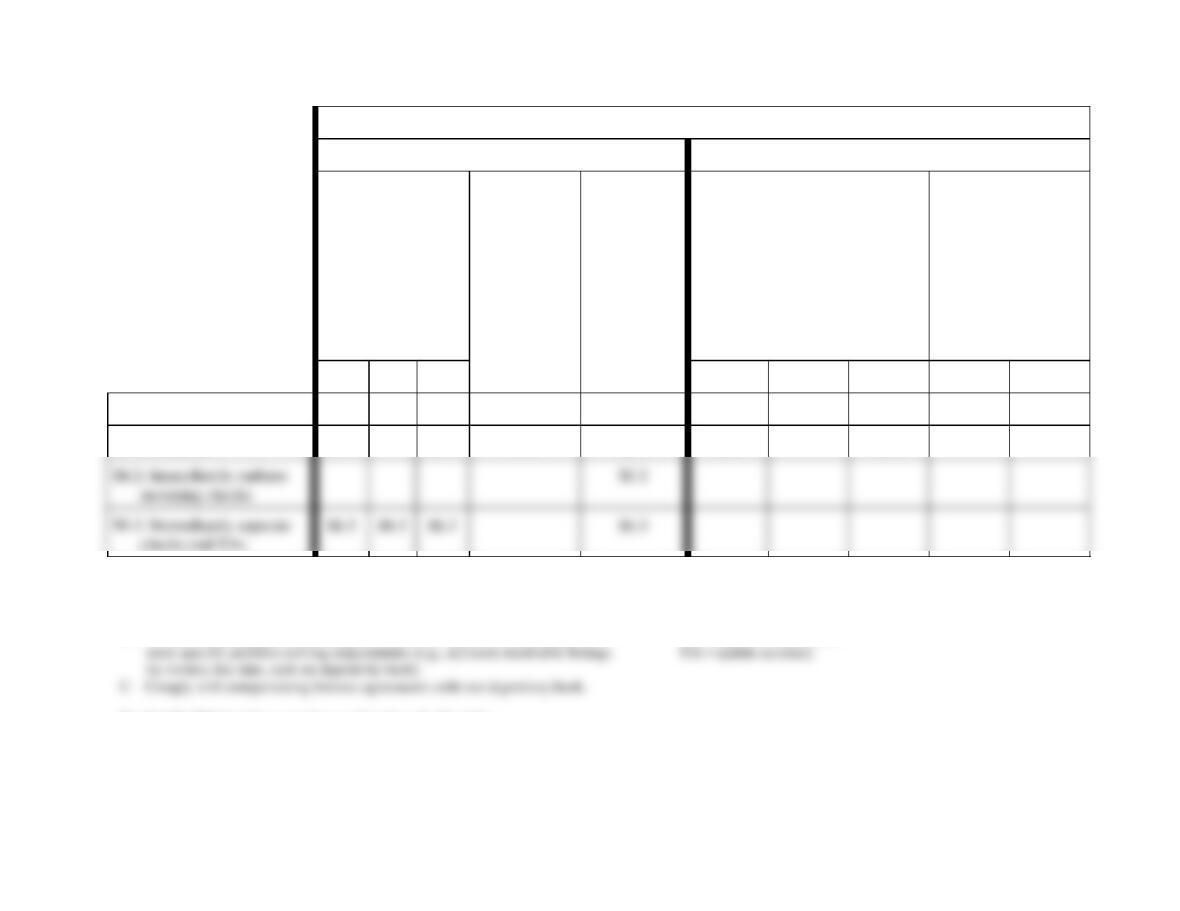

Missing controls

M-1: Lockbox

M-1

M-1

M-1

M-1

M-1

M-1

Effectiveness goals include:

A – Optimize cash flow by minimizing overdue accounts and reducing the

investment in accounts receivable.

B – Provide for querying and reporting functions that support accountability and

See Exhibit SM-11.1 for a complete explanation of cell entries.

IV = input validity

IC = input completeness

IA = input accuracy

UC = update completeness

FIGURE SM-11.7 Problem 2, Part b Solution (Partial)—Control Matrix for Fred’s Electrical, Inc. (Cash Receipts)

14 Solutions for Chapter 11

Exhibit SM-11.1 Explanation of Cell Entries for Control Matrix in Figure SM-11.7

P-1 Turnaround document.

Efficient employment of resources, remittance advice input accuracy: The

payment stub, printed by the computer, is used as the source document. This is

more efficient and less error-prone than would be manually preparing an RA.

Remittance advice input completeness: This procedure should ensure that all

inputs are corrected and input.

P-4: Enter cash receipts close to where cash is received.

Effectiveness goals A and C: By entering the RAs in accounts receivable, and not

sending them on to another data entry function, RAs will be input in a more

timely manner.

P-5: Computer agreement of input and output batch totals.

Efficient employment of resources: The computer comparison of batch totals can

detect errors much more efficiently than can a comparison of the detailed data.

Also, the computer agreement process is more efficient than would be a manual

process.

Accounting Information Systems, 10e 15

P-6: Confirm input acceptance:

Remittance advice input completeness, accounts receivable update completeness:

The computer tells the accounts receivable clerk that the inputs have been

accepted and that the updates have taken place once and only once.

P-7: Procedures for rejected inputs.

Remittance advice input validity, input completeness, and input accuracy: We

presume that corrective action will be taken to investigate all rejected items,

M-1: Lockbox.

Effectiveness goals A and C and security of resources: By having the payments

sent directly to the bank, Fred’s ensures a more timely deposit (goals A and C) and

reduces the possibility that payments will be diverted by their own employees

(security).

M-2: Immediately endorse incoming checks.

Security of resources: The checks should be restrictively endorsed to prevent them

from being fraudulently misappropriated.

M-3: Immediately separate checks and RAs.

16 Solutions for Chapter 11

Effectiveness goals A, B, and C: The checks should be separated from the RAs

and the checks deposited as quickly as possible. This helps to optimize cash flow

and to ensure that the organization complies with compensating balance

opportunities for lapping.

Solution Note: Several controls not described in the preceding list could be

included in the solution to this problem, as present or missing, depending on

assumptions made. For example:

• At the data entry location, we could include preformatted screens and online

Accounting Information Systems, 10e 17

FIGURE SM-11.8 Problem 2, Part c Solution—Annotated Systems Flowchart for Fred’s

Electrical, Inc. (Cash Receipts)

18 Solutions for Chapter 11

Bondstreet Company (Billing and Cash Receipts) Solutions

P 11-1 ANS. a. Table of Entities and Activities for Bondstreet Company (Billing and Cash

Receipts)

Entities

Para

Activities

Billing clerk

2

1. Requests billing due list display.

ERP system

2

2. Display billing due list.

2

3. Display totals for billing due list.

4

9. Accept invoice batch.

ERP system

4

10. Update sales order, close billing due list, create AR, update

GL, send electronic invoice, and display job completed.

Customer

4

Lockbox

5

11. Send remittance file.

5

12. E-mail totals.

ERP system

13. Save remittance file.

Cash application clerk (CA

5

14. Request display of remittance totals.

ERP system

5

15. Display remittance file totals.

CA clerk

5

16. Compare e-mail and remittance file totals.

6

17. Request application of payments.

ERP system

6

18. Examine terms, calculate amount due, and record payment.

6

19. Display total AR, discounts, and amount paid.

CA clerk

6

20. Compare payment totals to e-mail and remittance file totals.

6

21. Request update of GL.

ERP system

6

22. Update GL.

Billing clerk

2

4. Record billing due list totals on batch total sheet.

3

5. Request execution of billing program.

ERP system

3

6. Prepare invoice records (access customer, inventory, sales

3

7. Calculate and display invoice totals.

Clerk

4

8. Reconcile billing due and invoice totals.

Accounting Information Systems, 10e 19

Customer Billing/Cash

receipts

Lockbox

Invoice

Remittance data

FIGURE SM-11.9 Problem 1, Part b Solution—Context Diagram for Bondstreet Company

(Billing and Cash Receipts)

20 Solutions for Chapter 11

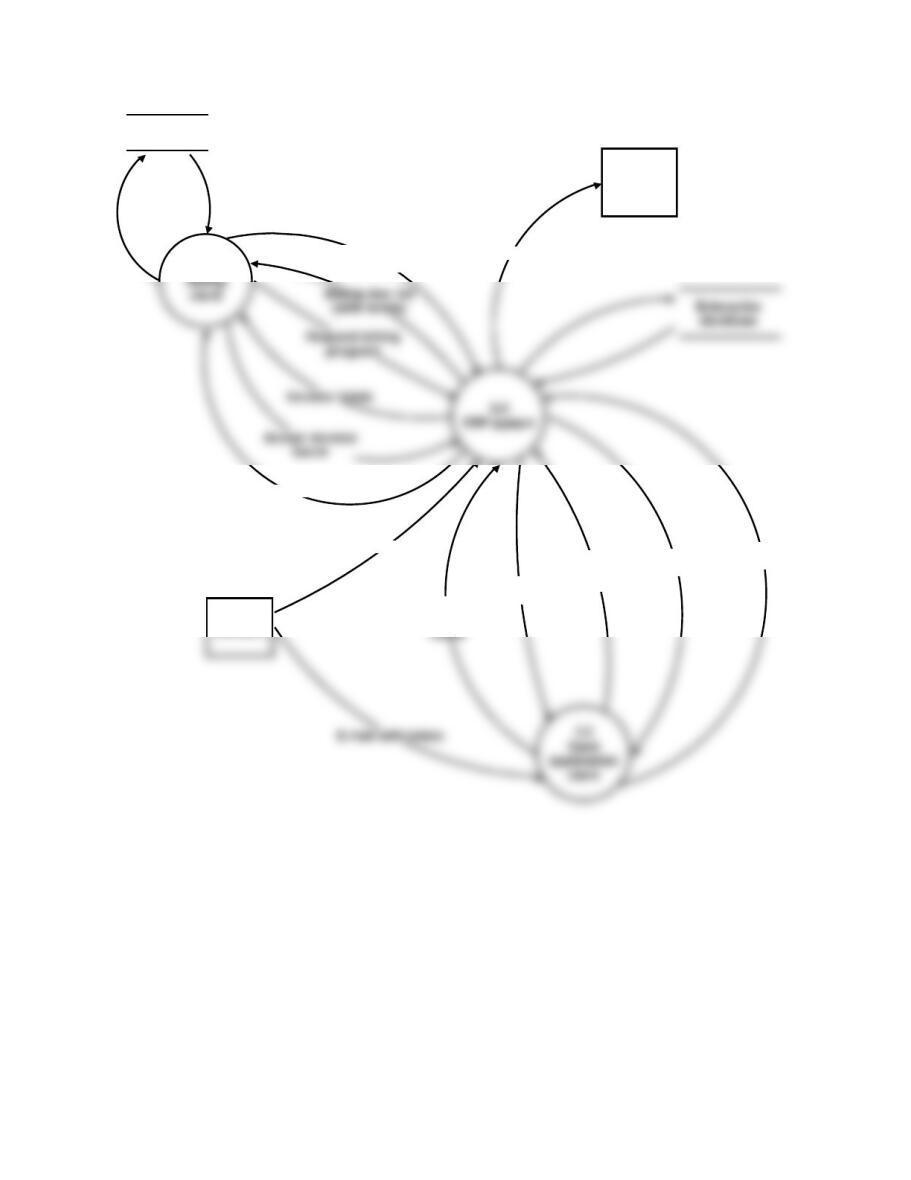

1.0

Lockbox

AR, discounts

paid

Request

payments

application

Request

remittance

NOTE: See the logical DFD for details regarding flows into and out of the enterprise database.

Request billing

due list

Batch total

she et

Job completed

Customer

Invoice

Remittance file

Remittance

totals

Request

GL update

FIGURE SM-11.10 Problem 1, Part c Solution—Physical DFD for Bondstreet Company

(Billing and Cash Receipts)