Chapter 10: Analysis and Valuation

of Privately Held Companies

Answers to End of Chapter Discussion Questions

10.1 What is a capitalization rate? When is it used and why?

Answer: The capitalization rate, or simply the “cap rate,” represents the ratio of net operating income divided

by asset value. Net operating income is total revenue less operating expenses. It is before taxes and excludes

10.2 What are the common ways of estimating capitalization multiples?

Answer: Capitalization multiples can be calculated as the reciprocal of the “cap rate” (analogous to a price

10.3 What is the marketability discount and what are common ways of estimating this discount?

Answer: The risk associated with an illiquid market for the specific stock is often referred to as the

10.4 Give examples of private company costs that might be understated and explain why.

Answer: Examples may include employee training and the cost of complying with government regulation such

10.5 How can an analyst determine if the target firm’s costs and revenues are understated or overstated?

Answer: The analyst may determine that revenues have been overstated by comparing the accounting practices

10.6 Why might shell corporations have value?

Answer: Merging with an existing corporate shell of a formerly publicly traded company may be a reasonable

10.7 Why might succession planning be more challenging for family owned firms?

10.8 What are some of the reasons a family-owned or privately-owned business may want to go public? What are

some of the reasons that discourage such firms from going public?

Answer: Private or family owned firms are more likely to go public when valuations are high or are

10.9 Why are family owned firms often attractive to private equity investors?

Answer: Family-owned firms often encounter succession problems. The founder wants to retire but either

lacks confidence in existing family members as successors or cannot find a family member with the right

10.10 Rank from the highest to the lowest the liquidity discount you would apply if you as a business appraiser had

been asked to value the following businesses: a) a local, profitable hardware store, b) a money losing

laundry, c) a large privately owned but marginally profitable firm with significant excess cash balances and

other liquid short-term investments, and d) a pool cleaning service whose primary tangible assets consist of

a 2-year old truck and miscellaneous equipment. Explain your ranking.

Answer: In descending order of magnitude, the liquidity discounts associated with these businesses would be

Practice Problems and Answers

10.11 An analyst constructs a privately held firm’s cost of equity using the “build–up” method. The 10-year Treasury

bond rate is 4% and the historical equity risk premium for the S&P 500 stock index is 5.5%. The risk

premium associated with firms of this size is 3.8% and for firms within this industry is 2.4%. Based on due

diligence, the analyst estimates the risk premium specific to this firm to be 2.5%. What is the firm’s cost of

equity based on this information?

10.12 An investor is interested in making a minority equity investment in a small privately held firm. Because of the

nature of the business, she concludes that it would be difficult to sell her interest in the business quickly.

Therefore, she believes that the discount for the lack of marketability to be 25%. She also estimates that if

she were to acquire a controlling interest in the business, the control premium would be 15%. Based on this

information, what should be the discount rate for making a minority investment in this firm? What should

she pay for 20% of the business if she believes the value of the entire business to be $1 million. Answer:

Discount rate = 9.78% and Purchase price for a 20% interest = $180,440

3

10.13 Based on its growth prospects, a private investor values a local bakery at $750,000. She believes that cost

savings having a present value of $50,000 can be achieved by changing staffing levels and store hours.

Based on recent empirical studies, she believes the appropriate liquidity discount is 20 percent. A recent

transaction in the same city required the buyer to pay a 5 percent premium to the asking price to gain a

controlling interest in a similar business. What is the most she should be willing to pay for a 50.1

percent stake in the bakery?

10.14 You have been asked by an investor to value a restaurant. Last year, the restaurant earned pretax operating

income of $300,000. Income has grown 4% annually during the last five years, and it is expected to

continue growing at that rate into the foreseeable future. The annual change in working capital is $20,000,

and capital spending for maintenance exceeded depreciation in the prior year by $15,000. Both working

capital and the excess of capital spending over depreciation are projected to grow at the same rate as

operating income. By introducing modern management methods, you believe the pretax operating income

growth rate can be increased to 6% beyond the second year and sustained at that rate into the foreseeable

future.

The ten-year Treasury bond rate is 5%, the equity risk premium is 5.5%, and the marginal federal, state,

and

local tax rate is 40%. The beta and debt-to-equity ratio for publicly traded firms in the restaurant industry

are 2 and 1.5, respectively. The business’s target debt-to-equity ratio is 1, and its pretax cost of borrowing,

based on its recent borrowing activities, is 7%. The business-specific risk premium for firms of this size is

estimated to be 6%. The liquidity risk premium is believed to be 15%, relatively low for firms of this type

due to the excellent reputation of the restaurant. Since the current chef and the staff are expected to remain

after the business is sold, the quality of the restaurant is expected to be maintained. The investor is willing

to pay a 10% premium to reflect the value of control.

a. What is free cash flow to the firm in year 1?

b. What is free cash flow to the firm in year 2?

c. What is the firm’s cost of equity?

Industry’s unleveraged beta = 2 / (1 + .6 x 1.5) = 1.05

d. What is the firm’s after-tax cost of debt?

e. What is the firm’s target debt–to-total capital ratio?

4

g. What is the business worth?

PV = $150,800 + $156,832 + ($156,832 x 1.06)/(.1222 – .06) =

(1.1222) (1.1222)2 (1.1222)2

Solutions to End of Chapter Case Study Questions

Going Public—Reverse Merger or IPO?

Discussion Questions:

1. What are common reasons for a private firm to go public? What are the advantages and

disadvantages of doing so? Be specific.

Answer: Common reasons for a firm to go public include the ability to obtain capital, to obtain an

acquisition currency, to liquidate some portion of the founder’s share holdings, and to offer

2. Discuss the pros and cons of a reverse merger versus an IPO.

Answer: Many small businesses fail each year. In a number of cases, all that remains is a business

with no significant assets or operations. Such companies are referred to as shell corporations.

5

3. Discuss why Versartis and Aravive may have chosen a reverse merger over an IPO.

Answer: When firms are interested in going public, they usually want to undertake an IPO in a

surging stock market increasing the likelihood that the shares will increase in value once issued.

Reverse mergers are not about raising money but rather about transferring ownership from a

4. What is the purpose of private firm in wanting to be listed on a major stock exchange such as

NASDAQ?

Answer: Larger public stock exchanges offer substantially larger trading volumes than the Pink

Sheets and OTC Bulletin Board. Therefore, they are likely to provide greater liquidity for

5. What is a shell corporation? Which firm is the shell corporation (Versartis or Aravive) in the

case study? Why is it misleading to call Versartis the acquirer and Aravive the target firm?

Answer: A shell corporation is a firm without significant business operations or operating assets.

6. What are the auditing challenges associated with reverse mergers? How can investors protect

themselves from the liabilities that may be contained in corporate shells?

Answer: Auditing challenges could include the following: collusion between local bank branches

and company executives in confirming the firm’s bank cash balances; collusion between vendors

Examination Questions and Answers

True/False Questions: Answer true or false to the following questions:

1. Both public and private firms always attempt to maximize earnings growth. True or False

2. Financial information for both public and private firms is equally reliable because their statements are

audited by outside accounting firms to ensure that are developed in a manner consistent with GAAP.

True or False

3. For privately held firms, firm specific risk may include lack of product, industry, and geographic

diversification; limited management depth, volatile stock markets, and unionized workforces.

True or False

4. Private firms are likely to understate revenue and understate costs in order to minimize their tax liabilities.

True or False

5. Revenue may be inflated by booking as revenue products shipped to resellers without adequately

adjusting for probable returns. True or False

6. If a buyer expects that the target firm’s revenue has been overstated, the buyer can reconstruct revenue by

examining usage levels of the key inputs required to produce the product or service. True or False

7. The purpose of adjusting the target’s income statement is to provide an accurate estimate of the

current year’s reported operating income or operating cash flow. True or False

8. Employee benefit levels in private firms are almost always mandated by state or federal law and

therefore cannot be changed. True or False

9. An increase in the target firm’s reserves for doubtful accounts increases taxable income, while a

decrease reduces the firm’s taxable income. True or False

10. It is easier to obtain the fair market value of private companies than for public companies because of the

absence of volatile stock markets. True or False

11. Methodologies employed to value private firms are substantially different from those employed to value

public firms. True or False

12. Asset valuation includes specific business risks but ignores any adjustment for liquidity risk. True or False

13. The risk associated with an illiquid market for a specific stock is referred to as the liquidity or marketability

risk. True or False

14. Shell corporations may have significant value to acquiring firms. True or False

15. Empirical evidence suggests that discounts have declined in recent years. True or False

16. Private businesses may need to be valued to settle shareholder disputes, court cases, divorce, or the

payment of gift or estate taxes. True or False

17. The availability and reliability of data for public companies tends to be much greater than for small

private firms. True or False

18. Managers and owners in public companies are likely to have the same emotional attachment to their

businesses as those in private firms. True or False

19. Because of data limitations, valuation of private firms often requires more subjective adjustments than for

public firms. True or False

20. Private firms must file quarterly earnings reports with the Securities and Exchange Commission.

True or False

21. Membership or subscription businesses, such as health clubs and magazine publishers, may inflate

revenue by booking the full value of muliyear contracts in the first year of the contract. True or False

22. If the buyer believes that the seller has overstated revenue in a specific accounting period, the buyer

can reconstruct revenue by examining usage levels, in the same accounting period, of the key inputs

required to produce the product or service. True or False

23. The primary purpose of the buyer adjusting the seller earnings is to provide an accurate estimate of the

current year’s operating income or cash flow in the base year. True or False

24. In adjusting base year income, an appraiser must be aware of the implications of various accounting

methods for value. During periods of inflation, businesses frequently use the last-in, first out method to

value inventories. This approach results a reduction in the cost of sales and an increase in gross profits

and taxable income. True or False

25. Before selling a business, an owner may increase advertising expenses in order to inflate profits.

True or False

26. Intangible assets such as customer lists, intellectual property, licenses, distributorships agreements, leases,

regulatory approvals, and employment contracts may offer significant sources of value. True or False

27. Fair value is by necessity more subjective than the concept of fair market value, because it represents the

dollar value of a business based upon an appraisal of the tangible and intangible assets of the business.

True or False

8

28. Valuation of privately held businesses may involve substantial adjustment of the discount or capitalization

rate. True or False

29. The term capitalization refers to the conversion of a future income stream into a present value, and it is a

term often used by business appraisers when future income or cash flows are not expected to grow or to

grow at a constant rate. True or False

30. Restricted stock is often issued to employees of privately held firms as a significant portion of their total

compensation. Such stock is similar to other types of common stock except that its sale on the open market

is prohibited for a period of time. True or False

31. A private corporation is a firm whose securities are not registered with state or federal authorities. True or

False

32. Privately owned businesses are often referred to as “closely held” since they are usually characterized by a

small group of shareholders controlling operating and managerial policies of the firm. True or False

33. Very few closely held businesses are family owned. True or False

34. All family owned businesses are small. True or False

35. In many family owned firms, family influence is exercised by family members holding senior management

positions, seats on the board of directors, and through holding super-voting stock (i.e., stock with multiple

voting rights). True or False

36. The M&A market for employer firms tends to be concentrated among smaller firms, as firms in the United

States with 99 or fewer employees account for 98% of all firms with employees. True or False

37. Family owned businesses account for about 89% of all businesses in the U.S. True or False

38. Firms that are family owned but not managed by family members are often well managed, as family

shareholders with large equity stakes carefully monitor those charged with managing the business. True or

False

39. Succession issues tend to be easier for small family owned firms than for large publicly traded firms. True

or False

40. The market model of corporate governance is readily applicable to privately held, family owned firms.

True or False

41. In many countries, family owned firms have been successful because of their shared interests and because

investors place a higher value on short-term performance than on the long-term health of the business. True

or False

9

42. The control model of corporate governance may be more applicable where ownership tends to be highly

diverse and the right to control the business is separate from ownership. True or False

43. A family owned firm’s board faces the sometimes daunting challenge of achieving the proper balance

between monitoring and collaboration to minimize the emotionality and overlapping roles that often

characterize such firms. True or False

44. Because of the need to satisfy both the demands of stockholders and regulatory agencies, public companies

need to balance the desire to minimize taxes with the goal of achieving quarterly earnings levels consistent

with investor expectations. Failure to do so frequently results in an immediate loss in the firm’s market

value. True or False

45. Despite the lack of public exchanges for privately held firms, Wall Street analysts have ample incentive to

analyze such firms in search of emerging companies. True or False

46. Private companies are generally not subject to the same level of rigorous controls and reporting systems as

are public companies. True or False

47. Small firms may lack product, industry, and geographic diversification, which add to their specific business

risk. True or False

48. Owners of private businesses attempting to minimize taxes may overstate their contribution to the firm by

giving themselves or family members unusually low salaries, bonuses, and benefits. True or False

49. It is rare that the owner or a family member is either an investor in or an owner of a vendor supplying

products or services to the family owned firm. True or False

50. A sudden improvement in operating profits in the year in which the business is being offered for sale may

suggest that both revenue and expenses had been overstated during the historical period.

True or False

51. EBITDA has become an increasingly popular measure of value for privately held firms in recent years.

True or False

52. The fair value concept is applied when no strong market exists for a business or it is not possible to identify

the value of substantially similar firms. True or False

53. If the cash flows of the firm are not expected to grow or are expected to grow at a constant rate indefinitely,

the discount rate used by practitioners often is referred to as the capitalization rate. True or False

54. If the discount rate is assumed to be 8% and the current cash flow is $1.5 million and is expected to remain

at that level in perpetuity, the implied valuation is $18.75 million. True or False

10

55. A control premium is the additional premium a buyer is willing to pay for the right to direct the activities of

a firm. True or False

56. An investor in a small company generally has little difficulty in selling their shares because of the high

demand for small businesses. True or False

57. It is generally easier to sell a minority interest than a majority interest in a business without loss of the

value of the original investment. True or False

58. Shell corporations rarely have any value. True or False

59. Private investment in public entities (PIPES) is a commonly used method of financing reverse mergers.

True or False

60. Shell corporations may be attractive for investors interested in capitalizing on the intangible value

associated with the existing corporate shell. This could include name recognition; licenses, patents, and

other forms of intellectual properties; and underutilized assets such as warehouse space and fully

depreciated equipment with some economic life remaining. True or False

61. Studies of restricted stock sales since 1990 indicate a median liquidity discount of about 20 percent with

several showing a decline to 13 percent after 1997 following the holding period change under Rule 144

from two years to one. True or False

62. There is widespread agreement over the magnitude of the liquidity discount. True or False

63. A minority discount is the reduction in the value of a minority investor’s investment because minority

owners have little influence in how the firm is managed. True or False

64. A pure control premium is the value the acquirer believes can be created by replacing the target firm’s

incompetent management, by changing the strategic direction of the target, by gaining a foothold in a

market not currently served, or by achieving unrelated diversification. True or False

65. Studies show that control premiums vary widely across countries reflecting the efficacy of shareholder

rights laws and how well such laws are enforced in each country. True or False

66. Increasing market liquidity will reduce the value of control; an increasing value of control will reduce

market liquidity and contribute to increasing liquidity discounts. True or False

Multiple Choice Questions: Circle only one alternative.

1. Which of the following are often true about the challenges of valuing private firms?

a. There is a lack of analyses generated by sources outside of the company.

b. Financial reporting systems are often inadequate.

c. Management depth and experience is often limited.

d. Reported earnings are often understated to minimize taxes.

e. All of the above.

2. In valuing private businesses, the U.S. tax courts have historically supported the use of which valuation

method for purposes of estate valuation?

a. Discounted cash flow

b. Comparable company method

c. Tangible book value method

d. A combination of a and c

e. All of the above

3. All of the following are true of reverse mergers except for.

a. May be used to take a private firm public

b. May represent an effective alternative to an IPO

c. Commonly use private equity placements for financing

d. Requires 2 years of audited financial statements to take a private firm public

e. A and B

4. Which of the following is not true of liquidity or marketability risk or discount?

a. It is measurable.

b. It is believed to have declined in recent years

c. The magnitude of the discount or risk is inversely related to the size of the investor’s equity

ownership in the business.

d. The magnitude of the discount or risk is directly related to the size of the investor’s equity

ownership in the business.

e. It is important to adjust the discount rate for liquidity risk.

5. Corporate shells have value because they enable the buyer to

a. Avoid the cost of going public

b. Exploit intangible value such as brand name

c. A and D only

d. Provide limited liability

e. A, B, and D only

6. Leveraged employee stock ownership plans are frequently used by owners of private businesses to

a. Hide assets

b. Motivate employees

c. Sell the firm to the employees

d. B and C

e. A, B, and C

7. All of the following are often true of privately held firms except for

a. Financial data is often inaccurate and out of date

b. Internal controls are ineffective

c. Have limited access to capital markets and product distribution channels

d. Are more easily valued than public companies

e. Have limited ability to influence customers, suppliers, unions, and regulators

8. Fair market value is

a. The cash or cash equivalent value that a willing buyer would pay or seller would accept for a

business

b. The cash or cash equivalent value that a willing buyer would pay or seller would accept for a

business, assuming each had access to all necessary information

c. The cash or cash equivalent value that a willing buyer would pay or seller would accept for a

business, assuming each had access to all necessary information and that neither party is under

duress.

d. The discounted value of free cash flow to the firm

e. The discounted value of free cash flow to equity investors.

9. The discount rate may be estimated using all but the one of the following:

a. The capital asset pricing model

b. The share exchange ratio

c. The cost of capital

d. Return on total assets

e. Price-to-earnings ratio

10. All of the following represent common sources of value in appraising private or publicly owned businesses

except for

a. Intellectual property

b. Customer lists

c. Licenses

d. Contingent liabilities

e. Employment contracts

11. Revenue Ruling 59-60 describes the general factors that the IRS and tax courts consider relevant in valuing

private businesses. Of the following valuation methods, which do the IRS and tax courts view as the most

important?

a. Discounted cash flow

b. Comparable company methods

c. Tangible book value

d. Replacement cost method

e. All of the above

12. The most important element(s) in selecting a business valuation professional include which of the

following: (Select only one)

a. Overall experience

b. Demonstrated ability in the industry in which the firm to valued competes

c. Degree of specialization

d. Number of professional degrees

e. A and B only

13. A business owner may overstate revenue by

a. Failing to deduct from revenue products returned by customers

b. Billing customers for products not ordered

c. Booking the entire value of a multiyear contract in the current year

d. Counting interest income as revenue

e. All of the above

13

14. A business owner may overstate revenue and understate actual expenses when

a. The business is about to be sold

b. They are being audited by the IRS

c. They are trying to minimize tax liabilities

d. All of the above

e. None of the above

15. A corporate shell may have value because

a. It may enable the owner to avoid the costs of going public

b. The name is widely recognized

c. It could own the rights to various forms of intellectual property

d. All of the above

e. None of the above

Short Case Study Essay Questions

THE NEED FOR CAPITAL FORCES SALE

OF DEMAND ENERGY

______________________________________________________________________________

Key Points

• Insufficient capital to finance growth is a leading factor forcing the sale of privately held businesses.

• An outright sale of a startup accomplishes two goals: provides financing for growth opportunities and cash for the

founders.

• To retain the founders, the management of the startup and the acquirer must have a strong shared vision of the

future.

• Key personnel in startups acquired by large bureaucratic firms often leave due to unrealized expectations and the

resulting frustration.

____________________________________________________________________________

In the twentieth century, electrical power generation relied primarily on fossil fuels and distributing power on the

electric grid. Concerns about reliance on foreign oil, air pollution, and global warming have spawned the growth of

solar and wind power as renewable energy sources. But these power sources are not without their limitations. Wind

power may be generating electricity when no additional power is needed. Solar power generation varies with cloud

cover and at best is only available during daylight hours. However, demand tends to peak after dark. These issues

have spurred interest in developing technologies to store power generated by these renewable energy sources.

14

The Enel Group will operate Demand Energy within its renewable energy subsidiary Enel Green Power, which is

engaged in the production of electricity from renewable sources. As of 2016, the firm has 735 active power plants

with a presence on four continents (Europe, North America, South America, and Africa). In each country, its

renewable operations are managed through an operating division. Demand Energy will be operated by Enel Green

Power North America (EGPNA), which owns and operates 100 renewable facilities in 23 states and two Canadian

provinces. These facilities in North America and on other continents provide both domestic and global opportunities

to expand use of Demand Energy’s DEN.OS energy management software, which allows for the most efficient use

of storage systems in real time.

Demand Energy’s goal is to quickly obtain the resources and capabilities to grow the firm. Confronted by growth

opportunities it could not fund, the firm looked at a range of options from partnership to the outright sale of the firm.

While allowing for continued control, partnerships require consensus on strategy and prioritization of investment

opportunities. Consequently, decision making can be slow and sometimes contentious. Outright sale to the right

company seemed to be a better way to accelerate growth and for the owners to pull cash out of the startup.

While the firm had many suitors, Enel stood out because of its huge global renewables investment portfolio in

need of optimal battery storage solutions. As part of a much larger company, Demand Energy could get access to

both capital and opportunities within Enel’s expansive and geographically diverse investments in renewable

facilities. Moreover, Enel and Demand Energy shared the same belief that renewable energy represented the wave of

the future.

____________________________________________________________________________

Signal and Miragen Combine

Through a Reverse Merger

_____________________________________________________________________________________

Case Study Objectives: To illustrate

• Alternative ways to “go public,”

• The mechanics of reverse mergers,

• Risks and rewards associated with reverse mergers, and

• Why reverse mergers may be preferred to IPOs for firms wanting to “go public”

In a reverse merger, private firms become publicly traded by merging with a publicly listed shell company, with

the public company surviving.2 In a merger, it is common for the surviving firm to be viewed as the acquirer, since

its shareholders usually end up with a majority ownership stake in the merged firms; the other party to the merger is

viewed as the target firm as its former shareholders often hold only a minority interest in the combined companies.

In a reverse merger, the opposite happens. Even though the publicly traded company survives the merger with the

private firm becoming its wholly-owned subsidiary, the former shareholders of the private firm end up with a

majority ownership stake in the combined firms.

While conventional IPOs can take months to complete, reverse mergers can take only a few weeks. Moreover, as

the reverse merger is solely a mechanism to convert a private company into a public entity, the process is less

dependent on financial market conditions because the company often is not proposing to raise capital. The cost of

regulatory filings and approvals is less with reverse mergers than with IPOs. Finally, firms lacking in historical

financial statements often find the reverse merger as the only practical option.

Early in 2015, biotech firm Tobira Therapeutics went public through a reverse merger after its IPO fizzled. This

successful reverse merger seemed to pave the way for more deals such as Catalyst and Targacept in May 2015 using

a reverse merger to form Catalyst Biosciences.

Existing Miragen shareholders, as well as those in the concurrent financing (so-called PIPE investment), receive

newly issued shares of Signal common stock. Signal’s board of directors approved a 1–for-15 reverse stock split of

its common stock, which took effect immediately following the close of trading on the NASDAQ on November 4,

2016. The reverse stock split is being implemented by Signal to maintain the listing of its common stock on the

NASDAQ.3

The motivation for the merger reflected Miragen’s promising micro RNA therapeutics programs, its limited

resources to fully develop these programs, and its desire to have its shares publicly listed. In contrast, publicly

traded Signal was prepared to raise cash by selling its proprietary technology and issuing new shares through a

private placement.

2 Alternatively, the private firm may merge with an existing special-purpose acquisition company already registered

for public stock trading.

3 Signal had received a deficiency notice from NASDAQ in November 2015 as its stock was trading at about $.33

per share; the reverse split was undertaken to comply with the minimum bid requirement rule of the exchange. To be

in compliance, the closing bid price of Signal’s common stock must be at least $1.00 per share for a minimum of 10

16

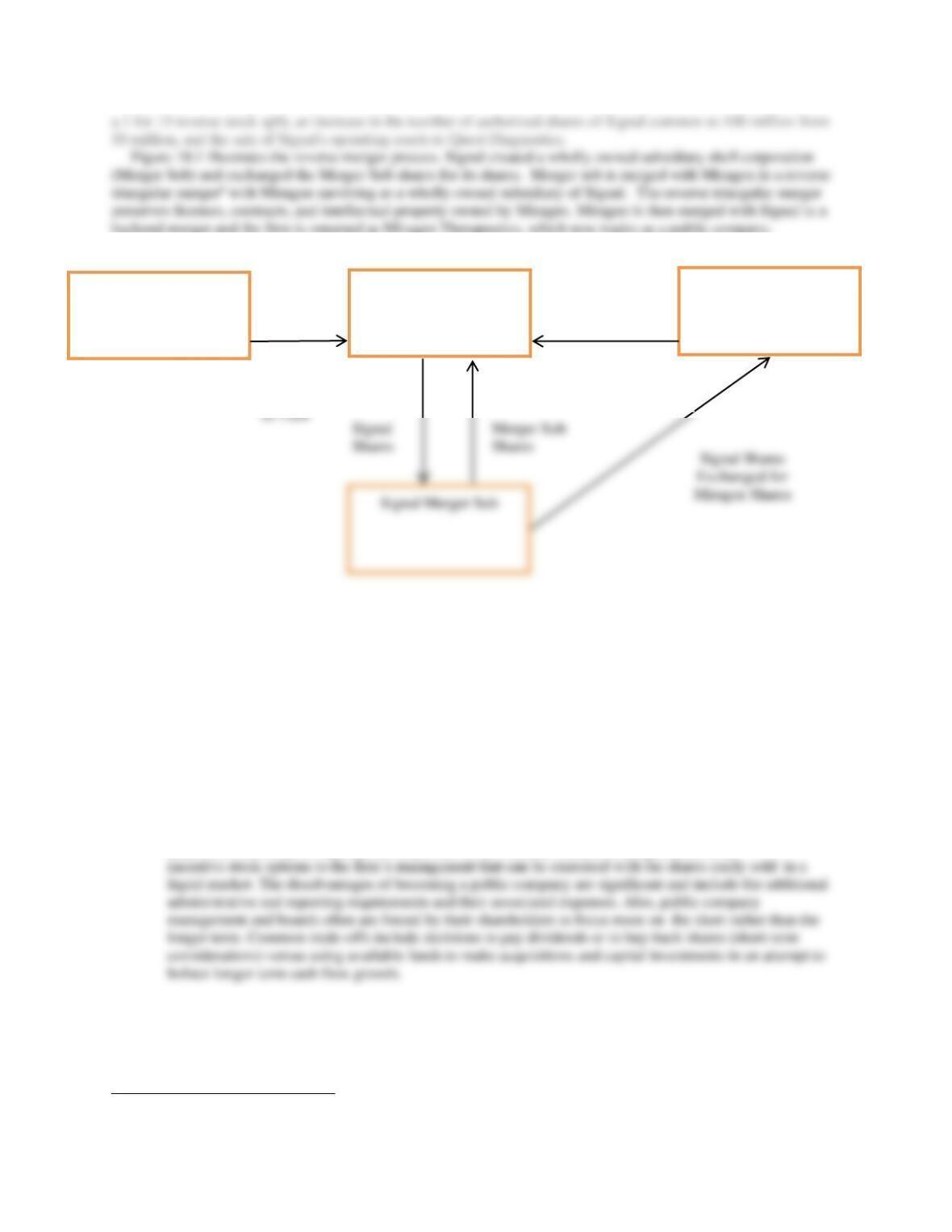

Signal Merger Sub

Figure 10.1 Reverse Merger Process

Lack of interest in biotech stocks in 2016 would have been an IPO difficult. Miragen lacked sufficient

resources to complete the needed clinical trials for its attractive drugs before they could get Food and Drug

Administration approval. In contrast, Signal had cash (or access to cash) and few attractive internal investment

opportunities. Signal was also a listed firm. These complementary needs illustrate the conditions in which reverse

mergers often take place.

Discussion Questions:

1. What are common reasons for a private firm to go public? What are the advantages and

disadvantages of doing so? Be specific.

Answer: Common reasons for a firm to go public include the ability to obtain capital, to obtain an

acquisition currency, to liquidate some portion of the founder’s share holdings, and to offer

2. Discuss the pros and cons of a reverse merger versus an IPO.

Answer: Many small businesses fail each year. In a number of cases, all that remains is a business with no

significant assets or operations. Such companies are referred to as shell corporations. Shell corporations

4 See Chapter 11 for a detailed discussion of triangular mergers.

Signal Renamed

Miragen Post Merger

Miragen

Miragen Becomes Wholly

Owned Sub of Miragen

Investor Syndicate

$40

million

17

3. Discuss why Signal and Miragen may have chosen a reverse merger over an IPO.

Answer: When firms are interested in going public, they usually want to undertake an IPO in a surging

stock market increasing the likelihood that the shares will increase in value once issued. Reverse

4. What is the purpose of private firm in wanting to be listed on a major stock exchange such as

NASDAQ?

Answer: Larger public stock exchanges offer substantially larger trading volumes than the Pink Sheets and

5. What is a shell corporation? Which firm is the shell corporation (Signal or Miragen) in the case study?

Why is it misleading to call Signal the acquirer and Miragen the target firm?

Answer: A shell corporation is a firm without significant business operations or operating assets. In

the case, Signal is the shell corporation which had agreed to sell most of its operating assets. Signal

18

6. What are the auditing challenges associated with reverse mergers? How can investors protect

themselves from the liabilities that may be contained in corporate shells?

Answer: Auditing challenges could include the following: collusion between local bank branches and

company executives in confirming the firm’s bank cash balances; collusion between vendors and customers

OWNER’S DECISION TO RETIRE

FORCES SALE OF BORTZ HEALTH CARE

_____________________________________________________________________________________

Key Points

• Succession planning and insufficient capital are leading factors forcing the sale of privately held or family

owned businesses.

• Small businesses often are unable to adapt to rapid changes in the markets in which they compete.

• For many deals to take place, sellers must feel comfortable that prospective buyers share their operating

philosophy.

____________________________________________________________________________

After being honorably discharged from the U.S. Navy in 1946, Donald Bortz, Jr. went to work for his father in the

used car business. By 1957, his father wanted a greater challenge and together they bought a nursing home in

Orchard Lake, Michigan. This would be the first of many nursing homes to be acquired by the father and son

management team. They developed a reputation of buying poorly run facilities, some in bankruptcy and some in

financial distress, and rapidly improving their operations. The growing chain of nursing facilities was named Bortz

Health Care with the slogan “We Care” a prominent part of the firm’s culture.

19

Patients are living longer and are sicker requiring more acute care. Fee for service reimbursement is ending and

other reimbursement models such as risk based managed care contracts and quality incentive withholds are being

evaluated.5 Time will tell whether these new reimbursement methods will lower patient costs while keeping the

skilled nursing facilities financially viable.

Bortz Healthcare in 2014 recorded $95 million in revenue and operated 11 nursing homes and assisted living

facilities: 10 in Michigan and one in Florida. In 2013, the firm had sold two other nursing homes located in

Michigan. The well managed operation was highly attractive to a number of larger nursing home chains hoping to

increase the scale of their operations through acquisition.

CATALYST ACQUIRES TARGACEPT IN REVERSE MERGER

____________________________________________________________________________

Case Study Objectives: To illustrate

• Motivations for “going public,”

• The mechanics of reverse mergers, and

• Why reverse mergers may be preferred to IPOs for firms wanting to “go public.”

____________________________________________________________________________

Biotech companies often partner with major pharmaceutical firms to fund the development of new drugs. Biotech

firms can attract talent and unlike big pharmaceutical firms have relatively little bureaucracy which often impedes

research and development activities at bigger firms. Without funding from the big drug companies, small biotech

firms must find alternative sources of funds often by listing on a major stock exchange. This is commonly done by

taking a private biotech company public through an initial public offering or by merging with an existing public

company through a reverse merger.

In the years following the 2008-2009 recession, biotech firms have been able to successfully go public through

IPOs due to the robust rise in stock prices and the desire for investors to achieve greater returns in the wake of

20

partnership in the ensuing years were modest. Catalyst had drugs in development (in the so-called pipeline) and

other drugs that were at various stages of clinical testing. But the firm needed money and was unable to get

financing from big pharmaceutical firms. By 2015, Catalyst went public in a reverse merger with publicly traded

Targacept, the beleaguered biotech that had suffered a number of clinical trial failures in recent years. Targacept had

little to attract investment from big drug companies and in late 2014 its partnership with AstreZeneca fell apart

diminishing its royalty revenue stream. Targacept was left to search for a new role for itself in the biotech industry.

In contrast to Targacept, Catalyst had a series of promising new drugs but was running short of cash. The long-

lead time required to bring drugs to market means that many biotech firms experience an inability to finance

aggressive R&D projects. To finance future research and development, it too had to partner with a large

pharmaceutical firm, or to go public through an IPO or a reverse merger. Cutbacks at large drug companies made

the likelihood of finding an investment partner slim and the lackluster stock market made an IPO impractical.

Therefore, the firm decided it needed to merge with a cash flush public firm which offered the opportunity to attract

new R&D talent with the offer of stock options and the ability to raise cash through future equity issues.

While conventional IPOs can take months to complete, reverse mergers can take only a few weeks. Moreover, as

the reverse merger is solely a mechanism to convert a private company into a public entity, the process is less

dependent on financial market conditions because the company often is not proposing to raise capital at the time it

goes public.

At closing, the combined firms had a pipeline of protease therapeutics, four other promising drug candidates, and

cash and cash equivalents of $40 million. Of the cash on hand, $35 million came from Targacept and the remaining

$5 million came from Catalyst, Existing Targacept shareholders received a special dividend prior to closing of about

$20 million distributed from Targacept’s cash on hand and redeemable convertible notes (convertible into Catalyst

Biosciences common shares) totally $37 million. The notes are guaranteed by the new firm Catalyst BioSciences.

The Catalyst stockholders will initially own approximately 65% of the combined company, with Targacept

shareholders owning the remainder.