CHAPTER 10

Liabilities

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

* 1. Explain how to account for

current liabilities.

1, 2, 3, 4, 5

1, 2, 3, 4, 5,

6

1a, 1b

1, 2, 3, 4, 5,

6

1A, 2A,

* 2. Describe the major

characteristics of bonds.

6, 7, 8, 9,

2

7

*6. Apply the straight-line

method of amortizing bond

discount and bond premium.

19, 20

16, 17

17, 18

6A, 7A, 8A

13, 14

11, 12

15, 16

13

4

13

5A

reported and analyzed.

17, 18

14, 15

5

14, 15, 16

1A, 2A, 3A,

4A, 5A, 6A,

7A, 10A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare current liability entries, adjusting entries, and

current liabilities section.

Moderate

30–40

4A

Prepare entries to record issuance of bonds, interest

accrual, and bond redemption.

Moderate

15–20

5A

Prepare installment payments schedule and journal

entries for a mortgage note payable.

Moderate

20–30

*6A

Prepare entries to record issuance of bonds, interest

accrual, and straight-line amortization for 2 years.

Moderate

30–40

*7A

Prepare entries to record issuance of bonds, interest,

and straight-line amortization of bond premium and

discount.

Moderate

30–40

*8A

Prepare entries to record interest payments, straight-line

premium amortization, and redemption of bonds.

Moderate

30–40

of interest, and amortization of bond premium using

effective-interest method.

Prepare entries to record issuance of bonds, payment

of interest, and amortization of discount using

effective-interest method. In addition, answer questions.

Moderate

30–40

2A

Journalize and post note transactions; show balance

sheet presentation.

Moderate

30–40

3A

Prepare entries to record issuance of bonds, interest

accrual, and bond redemption.

Moderate

20–30

WEYGANDT FINANCIAL AND MANAGERIAL ACCOUNTING 2E

CHAPTER 10

LIABILITIES

Number

LO

BT

Difficulty

Time (min.)

BE1

1

C

Simple

3–5

BE2

1

AP

Simple

2–4

BE3

1

AP

Simple

2–4

BE4

1

AP

Simple

2–4

BE11

3

AP

Simple

3–5

BE12

3

AP

Simple

6–8

BE13

4

AP

Simple

3–5

BE14

5

AP

Simple

3–5

BE15

5

AP

Simple

4–6

6

AP

Simple

4–6

*BE17

6

AP

Simple

4–6

*BE18

7

AP

Simple

DI1b

1

Simple

DI2

2

AP

Simple

5–7

DI3b

3

Simple

DI4

4

AP

Simple

4–6

DI5

5

AP

Simple

3–5

EX1

1

AN

Moderate

8–10

EX2

1

AN

Simple

6–8

EX3

1

AP

Simple

4–6

EX4

1

AN

Simple

6–8

EX5

1

AP

Simple

8–10

EX6

1

AP

Simple

3–5

EX7

2

AP

Simple

6–8

EX8

3

Simple

4–6

EX9

3

Simple

4–6

EX10

3

AP

Simple

4–6

EX11

3

AP

Simple

4–6

EX12

3

AP

Simple

6–8

Number

LO

BT

Difficulty

Time (min.)

BE5

1

AP

Simple

3–5

BE6

1

AP

Simple

3–5

BE7

3

AP

Simple

6–8

BE8

3

AP

Simple

4–6

BE9

3

AP

Simple

3–5

BE10

3

AP

Simple

4–6

EX13

4

AP

Simple

6–8

EX14

5

AP

Moderate

8–10

EX15

5

AP

Simple

6–8

EX16

5

AP

Simple

3–5

*EX17

6

AP

Simple

4–6

*EX18

6

AP

Simple

4-6

*P9A

7

AP

Moderate

30–40

*P10A

5, 7

AP

Moderate

30–40

BYP1

5

AN

Simple

5–10

BYP2

5

AP

Simple

10–15

BYP3

5

AP

Simple

10–15

BYP4

2

C

Simple

10–15

BYP5

AN

Moderate

15–20

Simple

BYP7

E

Simple

5–10

BYP8

—

AP

Moderate

15–20

BYP9

Simple

10–15

*EX19

7

AP

8–10

*EX20

7

AP

Moderate

8-10

P1A

1, 5

AN

Moderate

30–40

P2A

AN

30–40

P3A

AP

Moderate

20–30

P4A

AP

Moderate

15–20

P5A

AP

20–30

*P6A

5, 6

AP

Moderate

30–40

*P7A

5, 6

AP

Moderate

30–40

*P8A

6

AP

30–40

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Explain how to account for current

liabilities.

Q10-5

Q10-1 BE10-1

Q10-2 DI10-1

Q10-3

Q10-4

BE10-2 BE10-6 E10-5

BE10-3 DI10-1b E10-6

BE10-4 E10-3

BE10-5

E10-1 P10-1A

E10-2 P10-2A

E10-4

Q10-8

DI10-2b

4. Explain how to account for long-term

notes payable.

Q10-15

BE10-13

DI10-4

E10-13

P10-5A

5. Describe how liabilities are reported

and analyzed

Q10-16

Q10-17

Q10-18

BE10-14

BE10-15

DI10-5

E10-14

E10-15

E10-16

P10-3A

P10-4A

P10-5A

P10-6A

P10-7A

P10-1A

P10-2A

bond premium.

Q10-22

E10-19

E10-20

P10-10A

Across the

ANSWERS TO QUESTIONS

1. Lori is not correct. A current liability is a debt that a company expects to pay within one year or

the operating cycle, whichever is longer.

2. In the balance sheet, Notes Payable of $40,000 and Interest Payable of $700 ($40,000 X .07 X 3/12)

should be reported as current liabilities. In the income statement, Interest Expense of $700 should

be reported under other expenses and losses.

4. (a) The entry when the tickets are sold is:

Cash…………………………………………………………………………….. 1,200,000

Unearned Ticket Revenue ………………………………………… 1,200,000

5. Three taxes commonly withheld by employers from employees’ gross pay are: (1) federal income

taxes (2) state income taxes, and (3) social security (FICA) taxes.

Questions Chapter 10 (Continued)

7. (a) Secured bonds have specific assets of the issuer pledged as collateral. In contrast, unse-

cured bonds are issued against the general credit of the borrower. These bonds are called

8. (a) Face value is the amount of principal due at the maturity date.

(b) The contractual interest rate is the rate used to determine the amount of cash interest the borrower

9. The two major obligations incurred by a company when bonds are issued are the interest

payments due on a periodic basis and the principal which must be paid at maturity.

10. Less than. Investors are required to pay more than the face value; therefore, the market interest

rate is less than the contractual rate.

11. $56,000. $800,000 X 7% = $56, 000.

13. Debits: Bonds Payable (for the face value) and Premium on Bonds Payable (for the

unamortized balance).

Credits: Cash (for 97% of the face value) and Gain on Bond Redemption (for the difference

between the cash paid and the bonds’ carrying value).

14. A convertible bond permits bondholders to convert it into common stock at the option of the

bondholders.

(a) For bondholders, the conversion option gives an opportunity to benefit if the market price of

the common stock increases substantially.

(b) For the issuer, convertible bonds usually have a higher selling price and a lower rate of

(3) Earnings per share may be higher—although bond interest expense will reduce net income,

earnings per share on common stock will often be higher under bond financing because no

additional shares of common stock are issued.

(b) The major disadvantages in using bonds are that interest must be paid on a periodic basis

and the principal (face value) of the bonds must be paid at maturity.

18. Liquidity refers to the ability of a company to pay its maturing obligations and meet unexpected

needs for cash. Two measures of liquidity are working capital (current assets – current liabilities)

and the current ratio (current assets ÷ current liabilities).

*21. Kelli is probably indicating that since the borrower has the use of the bond proceeds over the

term of the bonds, the borrowing rate in each period should be the same. The effective-interest

method results in a varying amount of interest expense but a constant rate of interest on the

balance outstanding. Accordingly, it results in a better matching of expenses with revenues than

the straight-line method. When the difference between the straight-line method of amortization

and the effective interest method is material, GAAP requires the use of the effective interest

method.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 10-1

BRIEF EXERCISE 10-2

BRIEF EXERCISE 10-3

BRIEF EXERCISE 10-4

BRIEF EXERCISE 10-5

BRIEF EXERCISE 10-6

BRIEF EXERCISE 10-7

BRIEF EXERCISE 10-8

BRIEF EXERCISE 10-9

BRIEF EXERCISE 10-10

(a) Jan. 1 Cash ($2,000,000 X .97) ……………… 1,940,000

BRIEF EXERCISE 10-11

BRIEF EXERCISE 10-12

BRIEF EXERCISE 10-13

Annual

Interest

(A)

Cash

(B)

Interest

Expense

(C)

Reduction

of Principal

(D)

Principal

Balance

BRIEF EXERCISE 10-14

Long-term liabilities

BRIEF EXERCISE 10-15

*BRIEF EXERCISE 10-16

*BRIEF EXERCISE 10-17

*BRIEF EXERCISE 10-18

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 10-1a

DO IT! 10-1b

DO IT! 10-2

1. False. Mortgage bonds and sinking fund bonds are both examples of

DO IT! 10-3a

DO IT! 10-4

DO IT! 10-5

(a) Current ratio $11,500 ÷ $12,000 = .96:1

SOLUTIONS TO EXERCISES

EXERCISE 10-1

July 1, 2017

EXERCISE 10-2

(a) June 1 Cash …………………………………………………. 90,000

Notes Payable …………………………..… 90,000

(d) $3,600

EXERCISE 10-3

POOLE COMPANY

EXERCISE 10-4

EXERCISE 10-5

EXERCISE 10-6

EXERCISE 10-7

EXERCISE 10-8

EXERCISE 10-9

EXERCISE 10-10

(b) (1) Cash ………………………………………………………. 525,000

EXERCISE 10-11

EXERCISE 10-12

EXERCISE 10-13

2017

EXERCISE 10-14

EXERCISE 10-15

Plan One

Issue Stock

Plan Two

Issue Bonds

EXERCISE 10-16

(a) Current ratio

*EXERCISE 10-17

*EXERCISE 10-18

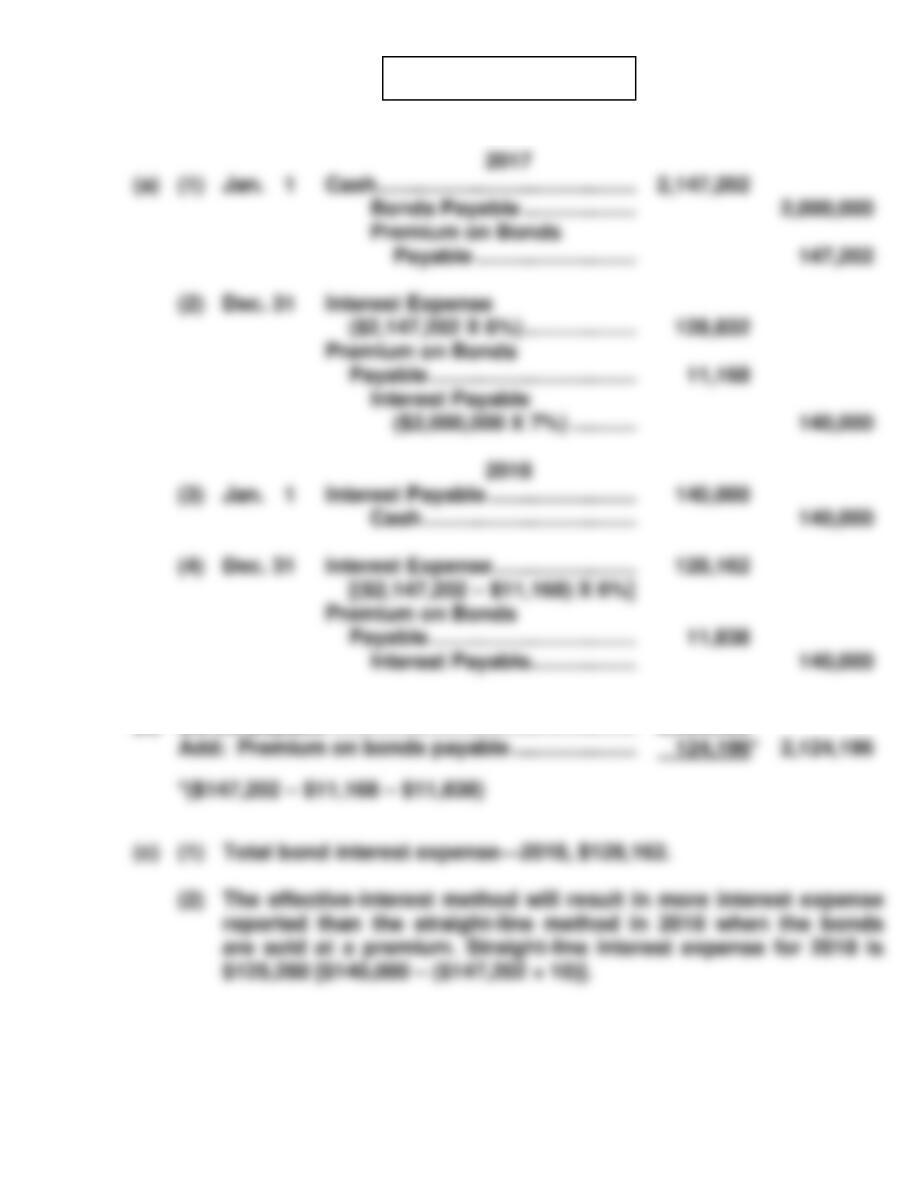

*EXERCISE 10-19 2017

*EXERCISE 10-20 2017

SOLUTIONS TO PROBLEMS

PROBLEM 10–1A

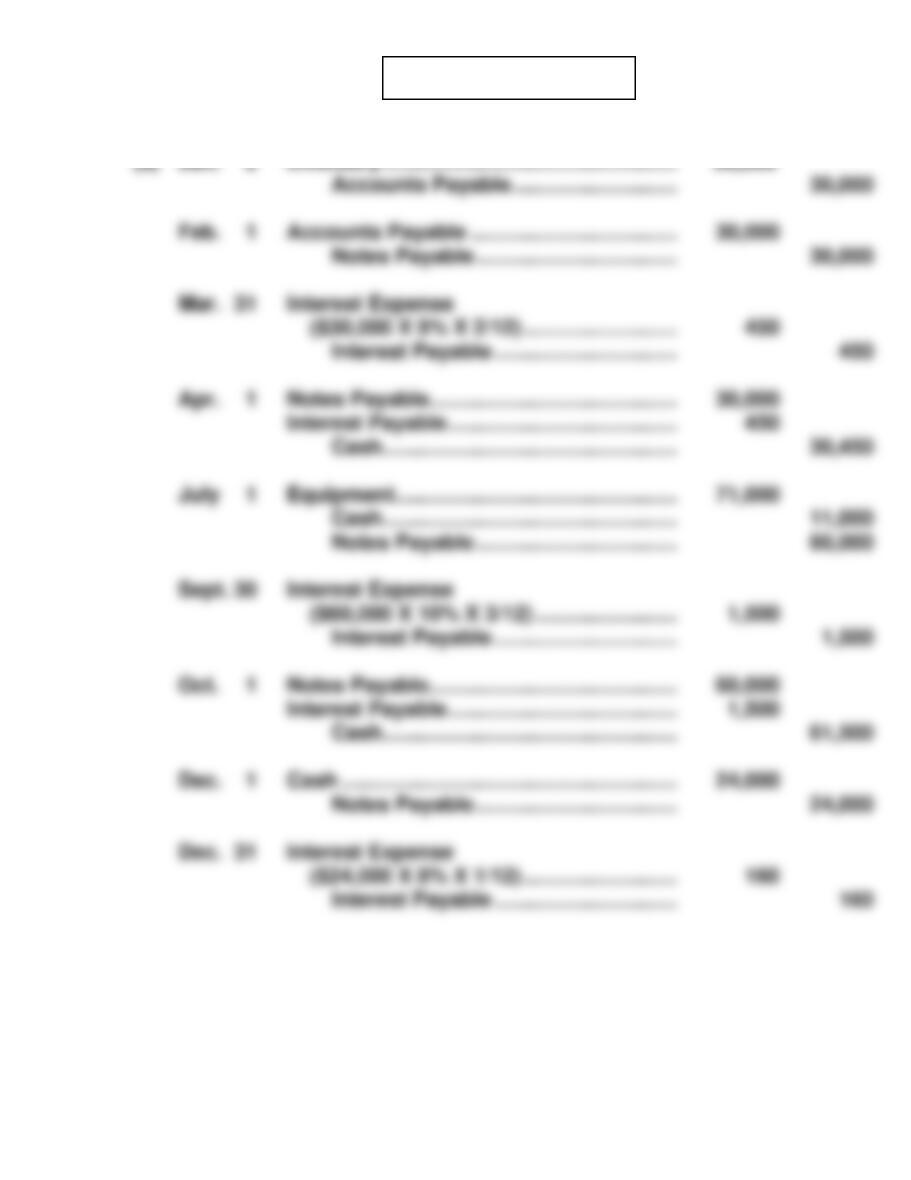

(a) Jan. 5 Cash ………………………………………………….. 20,520

PROBLEM 10-1A (Continued)

(c) Current liabilities

PROBLEM 10–2A

PROBLEM 10-2A (Continued)

(b)

PROBLEM 10-3A

(a) 2017

May 1 Cash ……………………………………………. 600,000

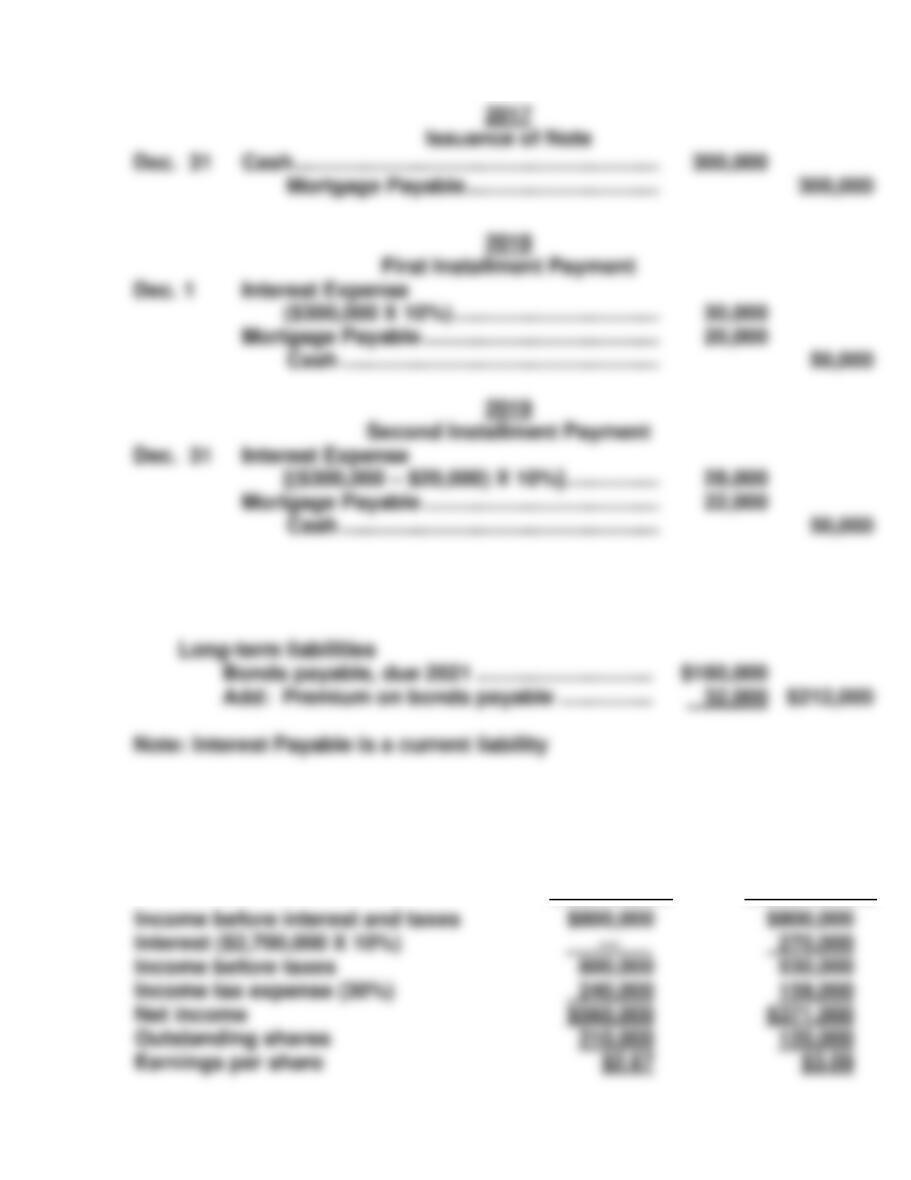

PROBLEM 10-4A

(a) 2017

Jan. 1 Cash ($6,000,000 X .98) ……………….. 5,880,000

PROBLEM 10-5A

(a)

Annual

Interest Period

Cash

Payment

Interest

Expense

Reduction of

Principal

Principal

Balance

(c) 12/31/17

Current Liabilities

*PROBLEM 10-6A

(a) 2017

(c) 2017

*PROBLEM 10-6A (Continued)

(b)

Annual

Interest

Periods

(A)

Interest to

Be Paid

(10% X

$3,000,000)

(B)

Interest Expense

to Be Recorded

(A) – (C)

(C)

Premium

Amortization

($120,000 ÷ 10)

(D)

Unamortized

Premium

(D) – (C)

(E)

Bond

Carrying Value

[$3,000,000 + (D)]

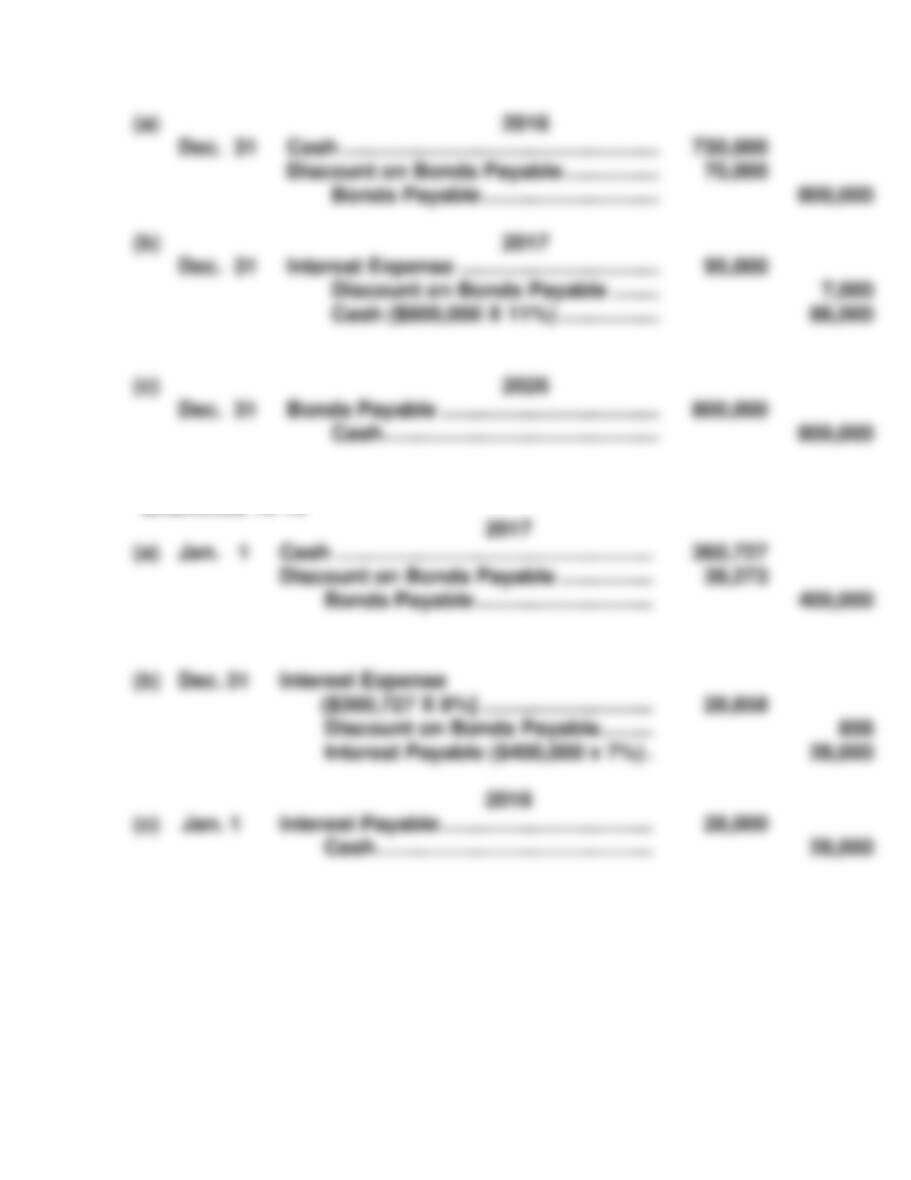

*PROBLEM 10-7A

(a) 2017

(c) Premium

Discount

*PROBLEM 10-8A

*PROBLEM 10-9A

(b) LOCK CORP.

Bond Discount Amortization

*PROBLEM 10-10A

2017

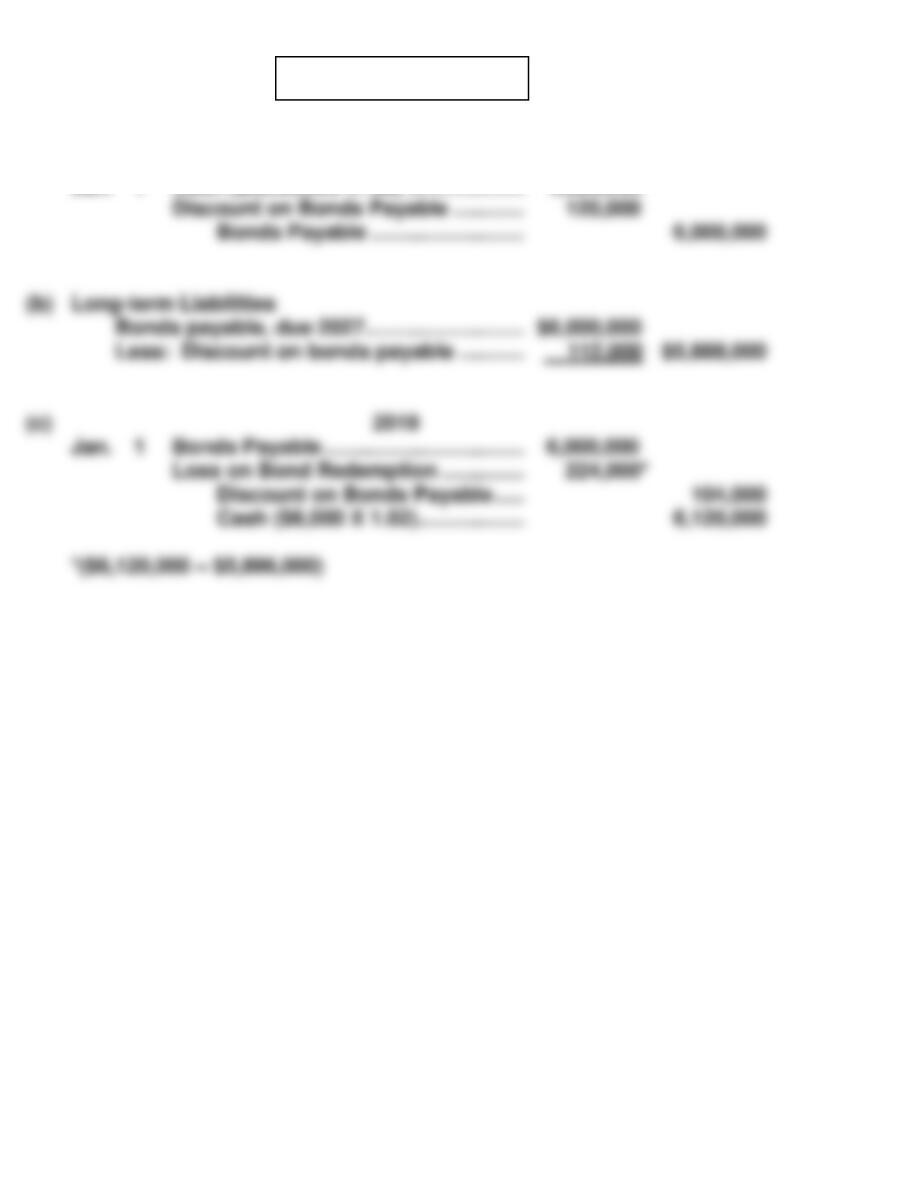

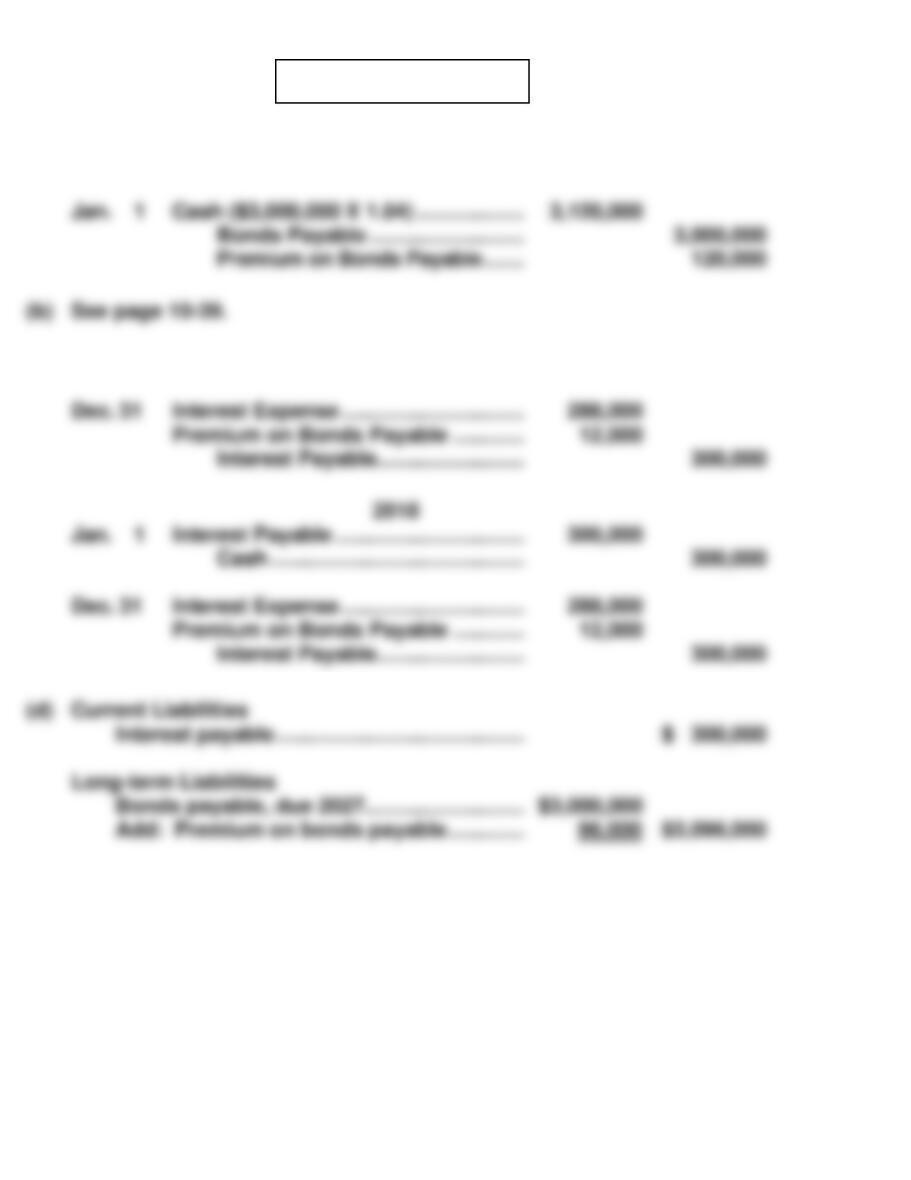

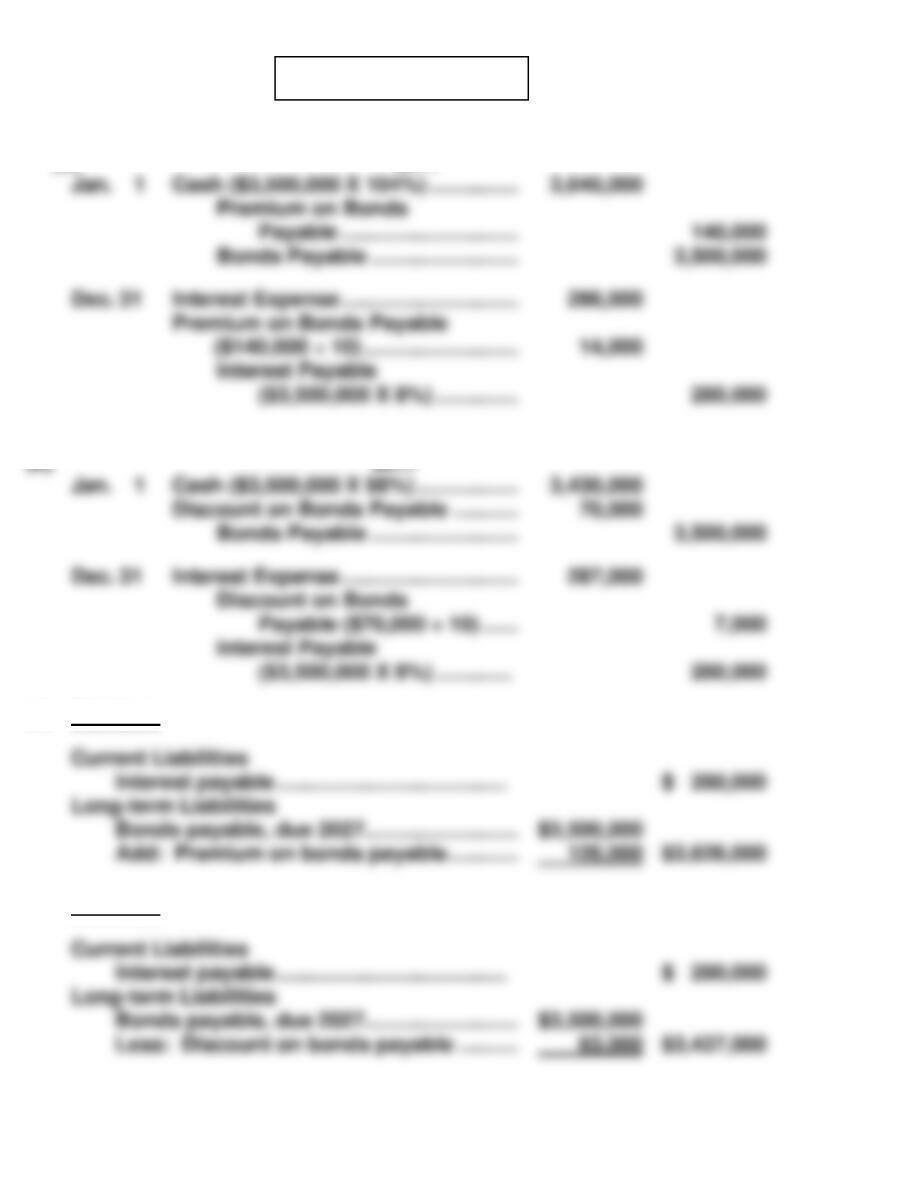

(b) Bonds payable ……………………………………………. 2,000,000

COMPREHENSIVE PROBLEM SOLUTION 10–1

(a)

1.

Interest Payable ……………………………………….

2,500

2.

Inventory …………………………………………………

COMPREHENSIVE PROBLEM SOLUTION (Continued)

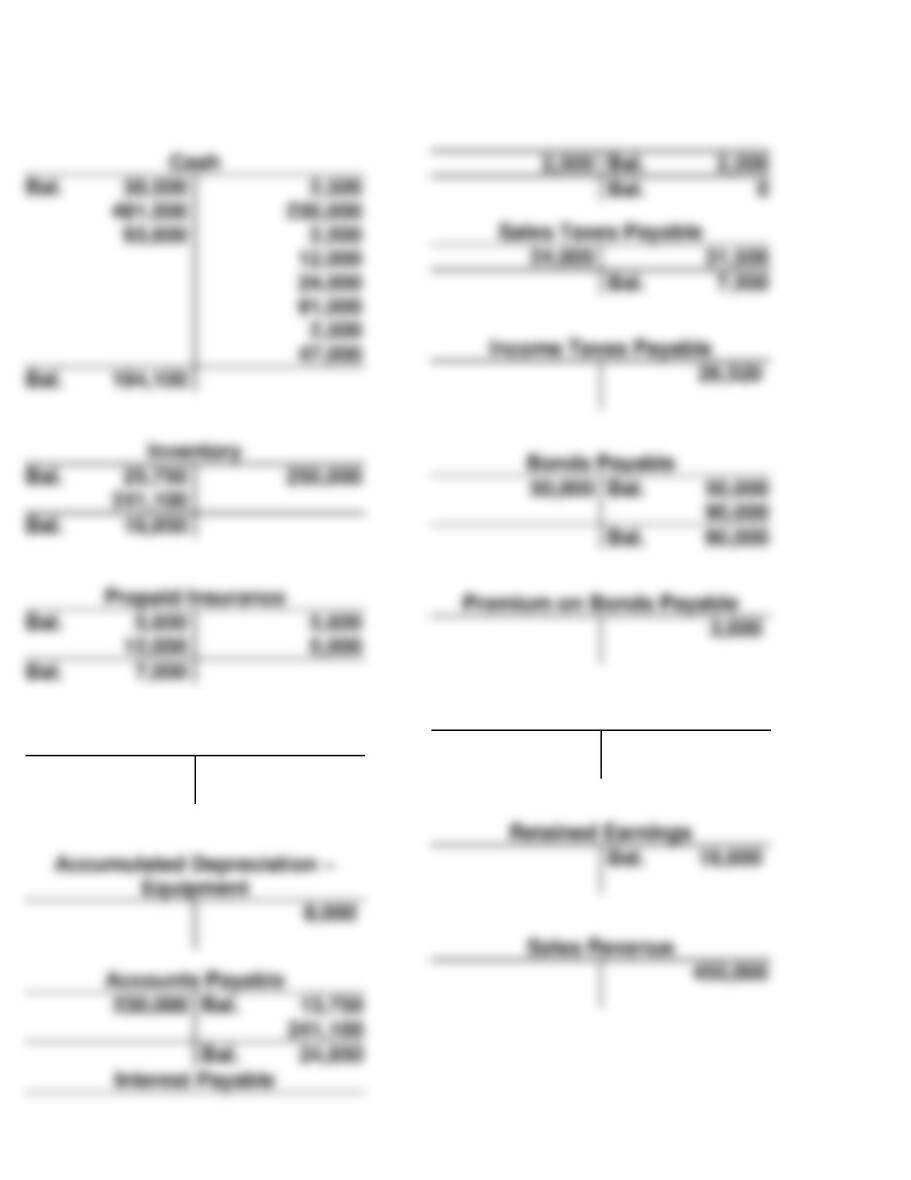

(b) JAMES CORPORATION

Trial Balance

12/31/2017

Equipment

8,000

241,100

Bal. 24,850

Bal. 18,600

450,000

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(a) and (b) Optional T accounts

Equipment

Bal. 43,000

Common Stock

Bal. 20,000

47,000

Bal. 194,100

241,100

Bal. 16,850

12,000

5,000

Bal. 7,000

2,500

Bal. 2,500

Bal. 0

24,000

31,500

Bal. 7,500

26,520

90,000

Bal. 90,000

3,600

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(a) and (b) (Continued)

250,000

8,000

Bal. 10,600

3,000

26,520

(c) JAMES CORPORATION

Income Statement

For the Year Ending 12/31/17

COMPREHENSIVE PROBLEM SOLUTION (Continued)

JAMES CORPORATION

Retained Earnings Statement

For the Year Ending 12/31/17

JAMES CORPORATION

Balance Sheet

12/31/2017

COMPREHENSIVE PROBLEM SOLUTION 10–2

(a)

Eastland

Company

Westside

Company

BYP 10-1 FINANCIAL REPORTING PROBLEM

(c) The components of current liabilities are:

BYP 10-2 COMPARATIVE ANALYSIS PROBLEM

(e) The higher the percentage of debt to assets, the greater the risk that a

BYP 10-3 COMPARATIVE ANALYSIS PROBLEM

(a) Amazon’s largest current liability was “accounts payable” at $15,133

(d)

Amazon

Wal-Mart

BYP 10-4 REAL-WORLD FOCUS

(a) An ‘A’ rating means that the company has a strong capacity to meet

BYP 10-5 DECISION MAKING ACROSS THE ORGANIZATION

(a) Face value of bonds …………………………………………………… $2,400,000

(b) 1. Bonds Payable …………………………………… 2,400,000

BYP 10-5 (Continued)

1. The cash flow of the company as it relates to bonds payable will be

adversely affected as follows:

BYP 10-6 COMMUNICATION ACTIVITY

To: Sam Masasi

From: I. M. Student

Subject: Bond Financing

(1) The advantages of bond financing over common stock financing include:

BYP 10-7 ETHICS CASE

(a) The stakeholders in the Olathe case are:

Questions:

Is what Ken wants to do legal? Is it unethical? Is Ken’s action brash

and irresponsible? Who may benefit/suffer if Ken arranges a high-risk

bond issue? Who may benefit/suffer if Barb Lowery gains control of

Olathe?

BYP 10-8 ALL ABOUT YOU

The answer to these questions depends on the state in which the student

resides. It also will be depend on the year chosen, although we expect that

the results will be much the same whether they pick any rates between

2014 and 2016. We provide a solution for this problem using the state of

Wisconsin as an example. It should be pointed out that certain taxes can

be deducted for computing federal income tax but are ignored in our

computation.

BYP 10-8 (Continued)

BYP 10-9 ALL ABOUT YOU

BYP 10-10 FASB CODIFICATION ACTIVITY

(a) Current liabilities is used principally to designate obligations whose

IFRS EXERCISES

IFRS 10-1

The similarities between GAAP and IFRS include: (1) the basic definition of

IFRS 10-2

IFRS 10-3

IFRS10-4 INTERNATIONAL FINANCIAL REPORTING PROBLEM