General Instructions

1. The following worksheet may be used to complete the exercise/problem. You may need to refer to your textbook for additional information.

P 10-2A

Required

(Round your answers to nearest whole dollar amounts)

Interest expense 18,489$

Discount amortization 5,989$

2018

Dec. 31 Interest Expense 3,691

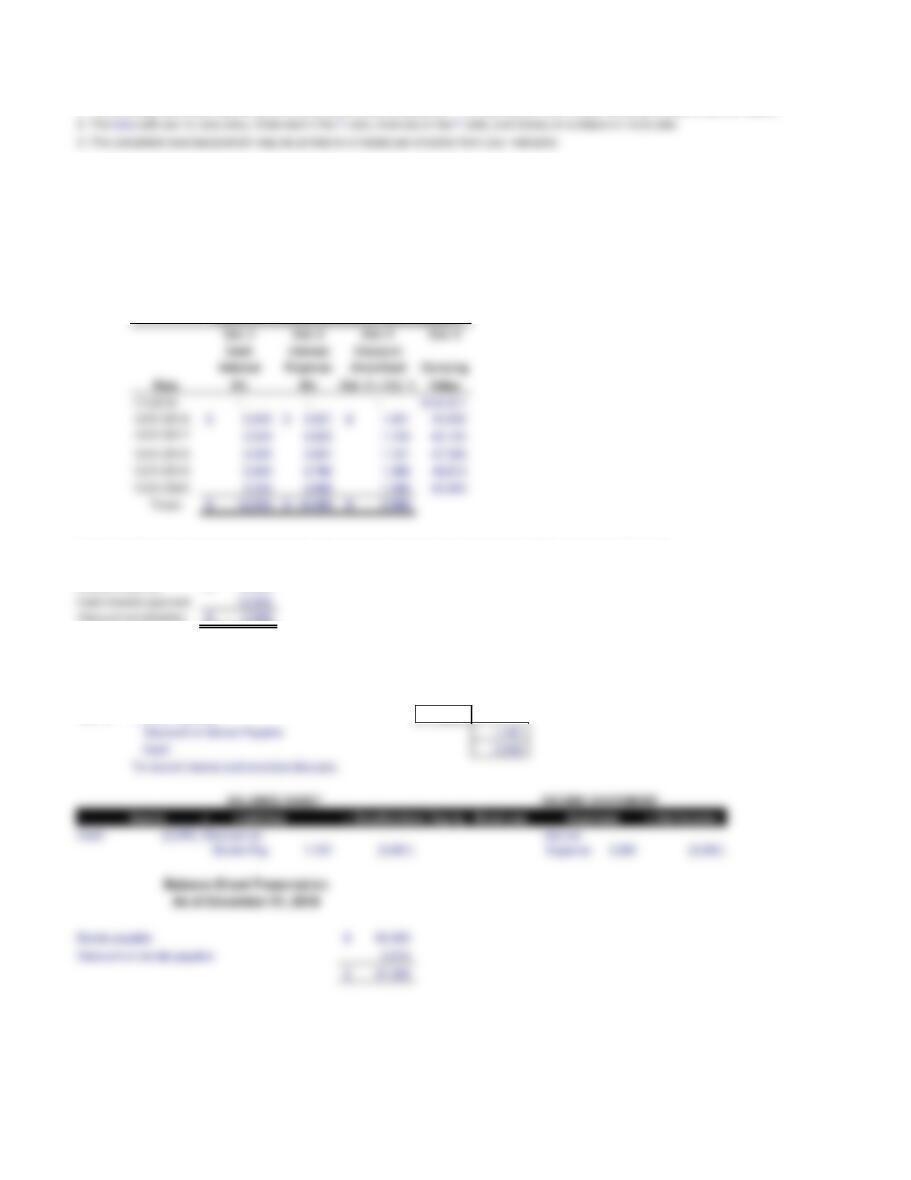

3. Prepare the journal entry for the payment of interest and the amortization of discount on December 31, 2018 (the third year), and

determine the balance sheet presentation of the bonds on that date.

Ortega Company issued five-year, 5% bonds with a face value of $50,000 on January 1, 2016. Interest is paid annually on December 31.

The market rate of interest on this date is 8%, and Ortega Company receives proceeds of $44,011 on the bond issuance.

1. Prepare a five-year table to amortize the discount using the effective interest

Discount Amortization

Effective Interest Method of Amortization

2. What is the total interest expense over the life of the bonds? cash interest payment? discount amortization?

General Instructions

2. The blue cells are for data entry. Enter text in the T cells, formulas in the F cells, and dollars or numbers in the $ cells.

P10-2

Required

(Round your answers to nearest whole dollar amounts)

Interest expense 5,721$

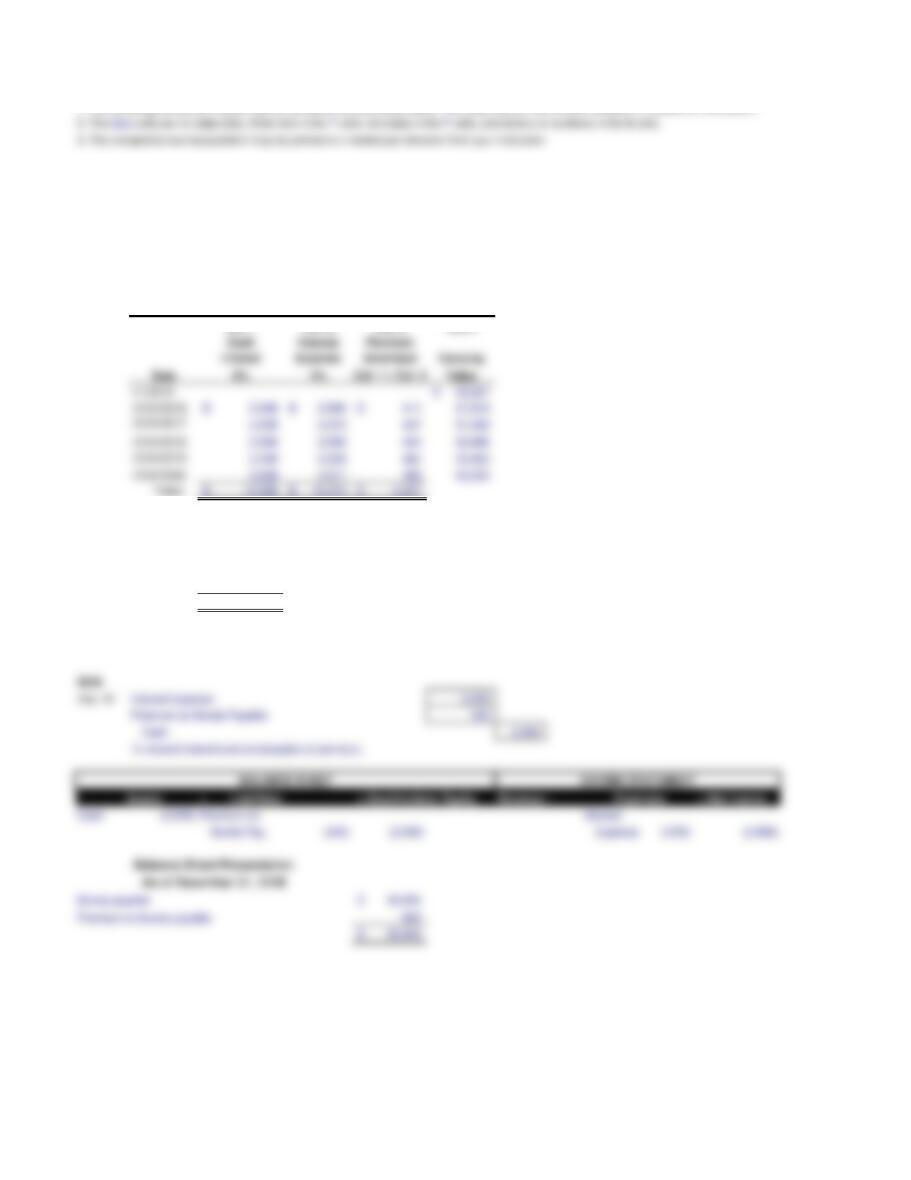

2. What is the total interest expense over the life of the bonds? cash interest payment?

discount amortization?

Stacy Company issued five-year, 10% bonds with a face value of $10,000 on January 1, 2016. Interest is paid annually on December 31. The market rate

of interest on this date is 12%, and Stacy Company receives proceeds of $9,279 on the bond issuance.

1. Prepare a five-year table to amortize the discount using the effective interest method.

Discount Amortization

Effective Interest Method of Amortization

2018

Dec. 31 Interest Expense 1,142

Discount on Bonds Payable 142

3. Prepare the journal entry for the payment of interest and the amortization of discount on

2018 (the third year), and determine the balance sheet presentation of the bonds on that date.

General Instructions

1. The following worksheet may be used to complete the exercise/problem. You may need to refer to your textbook for additional information.

P10-3A

Required

Col. 1 Col. 2 Col. 3 Col. 4

Interest expense 10,273$

Cash interest payment 12,500

Premium amortized 2,227$

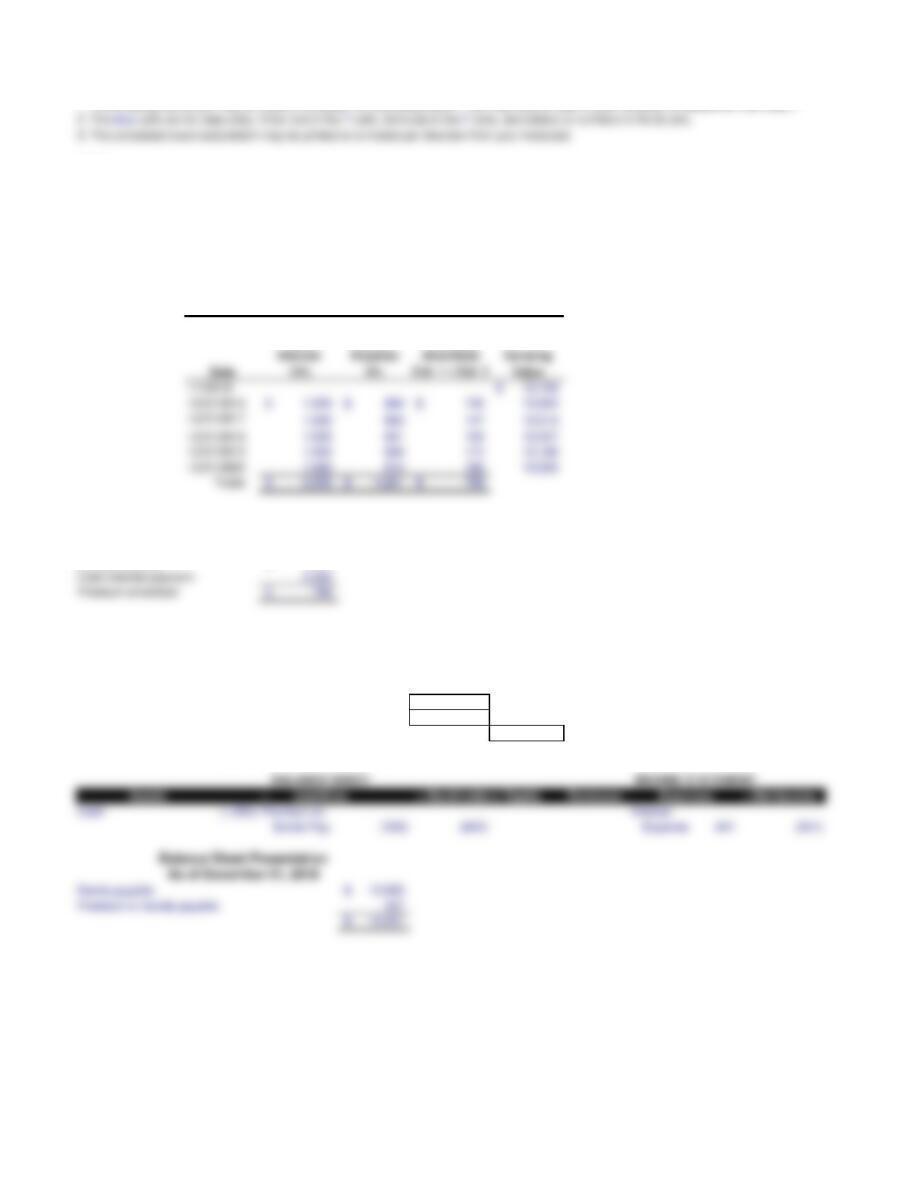

2. What is the total interest expense over the life of the bonds? cash interest payment? premium amortization?

3. Prepare the journal entry for the payment of interest and the amortization of premium on December 31,

2018 (the third year), and determine the balance sheet presentation of the bonds on that date.

Ortega Company issued five-year, 5% bonds with a face value of $50,000 on January 1, 2016. Interest is paid annually on December 31.

The market rate of interest on this date is 4%, and Ortega Company receives proceeds of $52,227 on the bond issuance.

1. Prepare a five-year table to amortize the premium using the effective interest method.

Premium Amortization

Effective Interest Method of Amortization

General Instructions

1. The following worksheet may be used to complete the exercise/problem. You may need to refer to your textbook for additional information.

P10-3

Required

1. Prepare a five-year table (similar to Exhibit 10-4) to amortize the dicount using the effective interest method.

Col. 1 Col. 2 Col. 3 Col. 4

Cash Interest Premium

Interest expense 4,201$

2018

Dec. 31 Interest Expense 841

Premium on Bonds Payable 159

Cash 1,000

To record interest and amortization of premium.

Stacy Company issued five-year, 10% bonds with a face value of $10,000 on January 1, 2016. Interest is paid annually on December 31. The

market rate of interest on January 1, 2016, is 8%, and Stacy Company receives proceeds of $10,799 on the bond issuance.

Premium Amortization

Effective Interest Method of Amortization

2. What is the total interest expense over the life of the bonds? cash interest payment? premium amortization?

3. Prepare the journal entry for the payment of interest and the amortization of premium on

2018 (the third year), and determine the balance sheet presentation of the bonds on that date.

General Instructions

1. The following worksheet may be used to complete the exercise/problem.

You may need to refer to your textbook for additional information.

P10-5

Required

Col. 1 Col. 2 Col. 3 Col. 4

2. Prepare the journal entry for the lease transaction on January 1, 2016.

2016

Jan. 1 Leased Truck 112,994

Lease Liability 112,994

To record acquisition by lease.

1. Prepare a table to show the five-year amortization of the lease obligation.

Lease Amortization: Effective Interest Method of Amortization

On January 1, 2016, Muske Trucking Company leased a semitractor and trailer for five years. Annual payments of

$28,300 are to be made every December 31 beginning December 31, 2016. Interest expense is based on a rate of 8%.

The present value of the minimum lease payments is $112,994 and has been determined to be greater than 90% of the

fair market value of the asset on January 1, 2016. Muske uses straight-line depreciation on all assets.

2. The blue cells are for data entry. Enter text in the T cells, formulas in the F cells, and

dollars or numbers in the $ cells.

2017

Dec. 31 Lease Liability 20,801

Interest Expense 7,499

Long-term assets:

Leased truck 112,994$

4. Prepare the balance sheet presentation as of December 31, 2017, for the leased asset and the lease obligation.

Balance Sheet Presentation

As of December 31, 2017

3. Prepare all necessary journal entries on December 31, 2017 (the second year of the lease).

General Instructions

2. The blue cells are for data entry. Enter text in the T cells, formulas in the F cells, and

dollars or numbers in the $ cells.

P10-7A

(In thousands) Year 1 Year 2 Year 3

Income before taxes

$120 $120 $120

Excess of book depreciation over tax depreciation

Taxable income

Taxes paid or payable (40%)

Excess of book depreciation over tax depreciation

Taxable income

Taxes paid or payable (40%)

Income before taxes

Tax-exempt income

Income before taxes

Tax-exempt income

Required

(Enter amounts in whole dollars not in thousands.)

Year 1 120,000$

(5,000)

(10,000)

105,000$

42,000$

Excess of tax depreciation over book depreciation

Taxable income

Taxes paid or payable (40%)

year for financial accounting but is depreciated for tax purposes at the rate of $30,000 in Year 1, $20,000

in Year 2, and $10,000 in Year 3.

Clemente has identified two items that are treated differently in the financial records and in the tax

The first one is interest income on municipal bonds, which is recognized on the financial reports to the

The other item, equipment, is depreciated using the straight-line method at the rate of $20,000 each

1. Determine the amount of cash that Clemente paid for income taxes each year. Assume

that a 40% tax rate applies to all three years.

Income before taxes

Tax-exempt income

Clemente Inc. has reported income for book purposes as follows for the past three years:

(Enter amounts in whole dollars not in thousands.)

The deferred tax entry for Years 1-3 would contain the following information:

2. Calculate the balance in the Deferred Tax account at the end of Years 1, 2, and 3. How does this

account appear on the balance sheet?

In the balance sheet, the account would appear as a:

In the balance sheet, the account would appear as a: