E10-12, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2017

Aug. 4

Cash

34,400(b)

Loss on Disposal

3,200(a)

Loss on disposal

=

Total cash received

=

=

(b)

Total cash received

=

Number of shares

×

=

×

=

(c)

Calculated in Requirement 1 on January 14.

Requirement 3

Strategic would report the $3,200(a) loss on disposal on its income statement for the year ended

December 31, 2017, classified as other revenues and (expenses).

(a)

Calculated in Requirement 1.

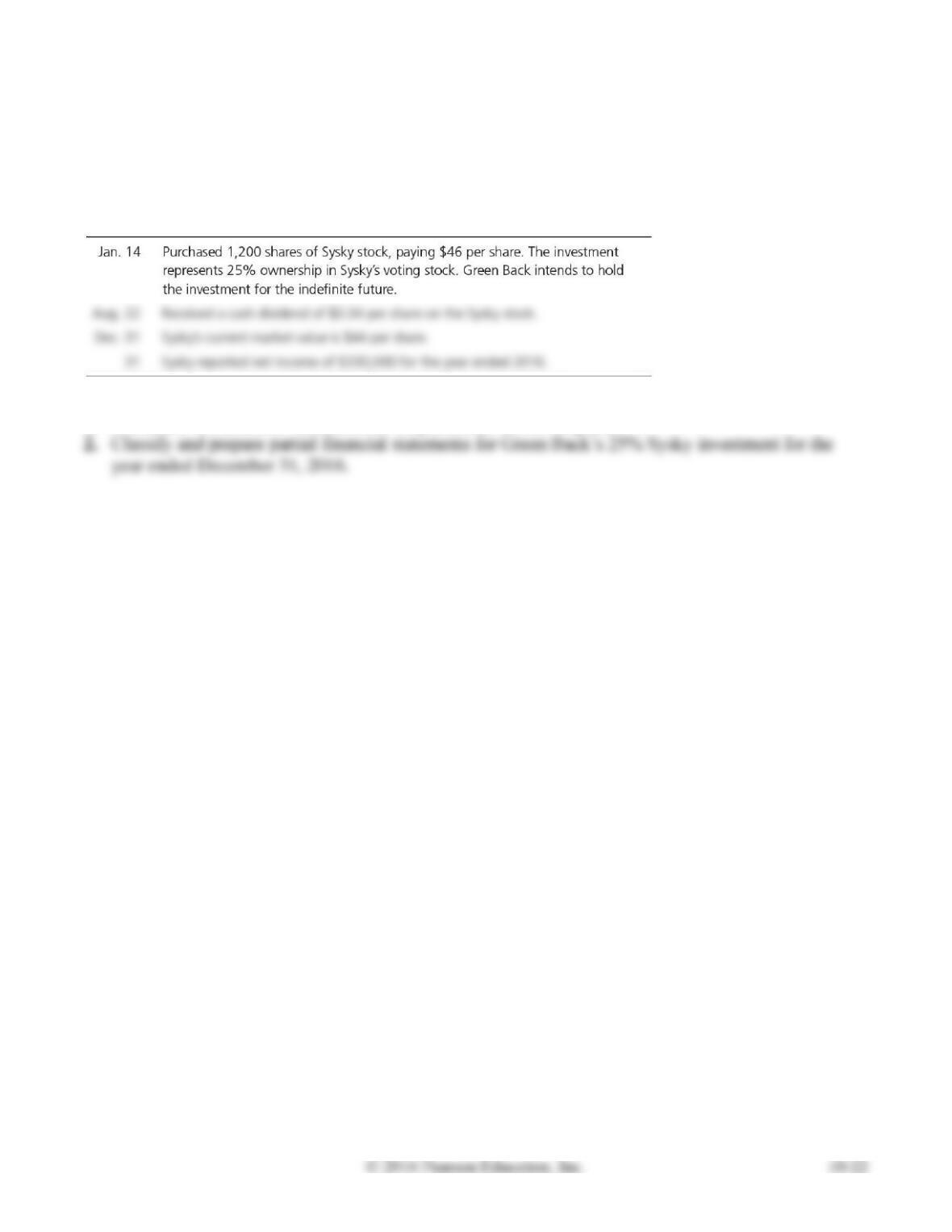

E10-13 Accounting for stock investments

Learning Objective 3

1. Revenue from Investments CR $82,500

Green Back Investments completed the following transactions during 2016:

Requirements

1. Journalize Green Back’s transactions. Explanations are not required.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 14

Long-Term Investments—Sysky

55,200(a)

Cash

55,200(a)

Aug. 22

Cash

Long-Term Investments—Sysky

Long-Term Investments—Sysky

Revenue from Investments

Calculations:

(a)

Total cost

=

Number of shares

×

Price per share

=

1,200 shares

×

$46 per share

=

$55,200

(b)

Dividend received

=

Number of shares

×

Dividend per share

=

1,200 shares

×

=

value is made.

(d)

=

×

25%

=

E10-13, cont.

Requirement 2

The investment (equity-method) is classified as a long-term asset on the balance sheet at December

31, 2016, and the revenue from investments is classified as other revenues and (expenses) on the

income statement for the year ended December 31, 2016.

GREEN BACK INVESTMENTS

Balance Sheet (Partial)

December 31, 2016

Long-term Assets:

Long-term Investments—Sysky (equity method)

Other Revenues and (Expenses):

Revenue from Investments

Calculations:

(a)

Long-Term Investments—Sysky

Jan. 14

55,200(b)

408(b)

Aug. 22

137,292

(b)

Calculated in Requirement 1.

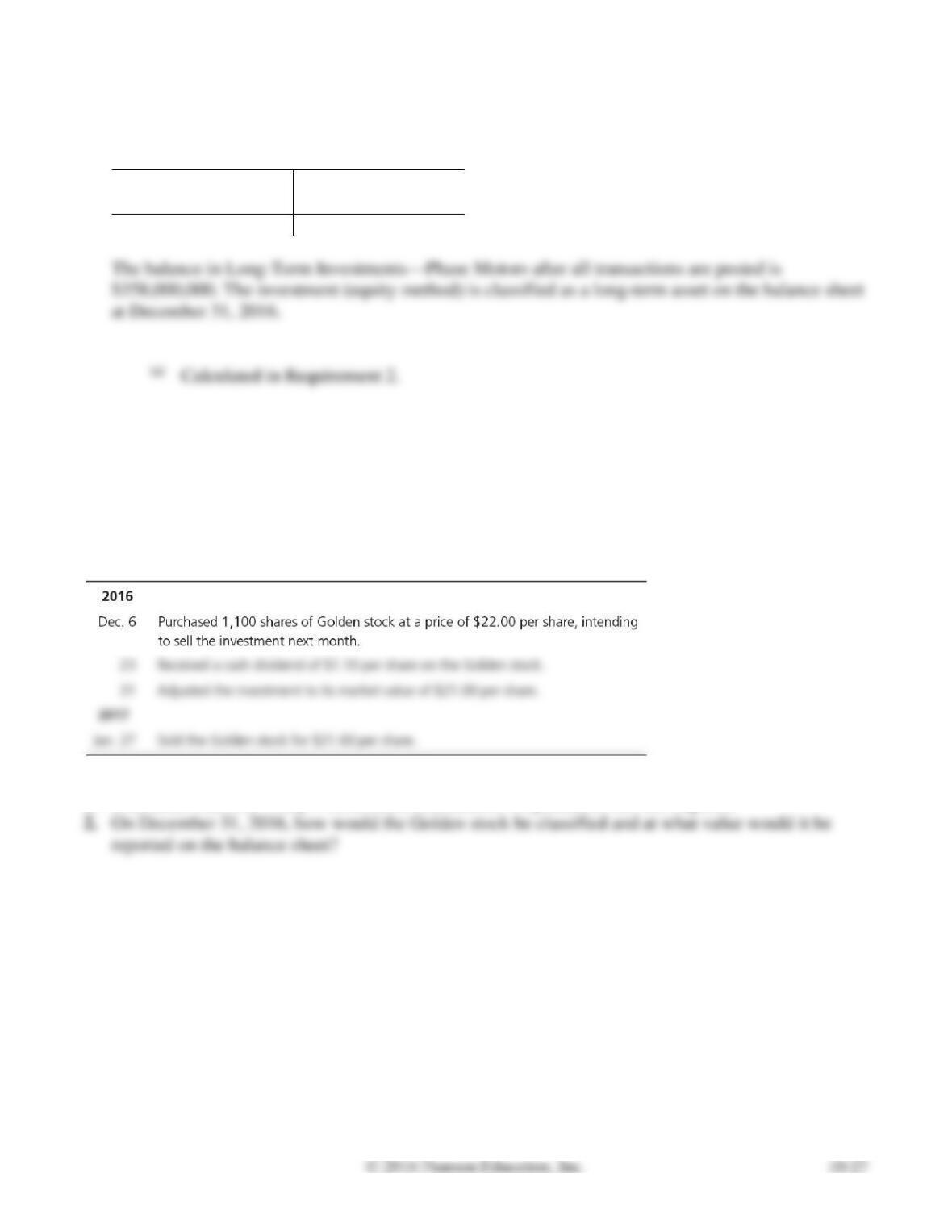

E10-14 Accounting for stock investments

Learning Objective 3

3. $358,000,000 Bal.

Suppose that on January 6, 2016, Westfall Motors paid $360,000,000 for its 40% investment in Phase

Motors. Assume Phase earned net income of $20,000,000 and paid cash dividends of $25,000,000 to all

outstanding stockholders during 2016. (Assume all outstanding stock is voting stock.)

Requirements

1. What method should Westfall Motors use to account for the investment in Phase Motors? Give your

reasoning.

SOLUTION

Requirement 1

Westfall Motors should use the equity method to account for the investment in Phase Motors

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 6

Long-Term Investments—Phase Motors

360,000,000

Cash

360,000,000

Cash

Long-Term Investments—Phase Motors

Long-Term Investments—Phase Motors

Revenue from Investments

Calculations:

(a)

Dividend received

=

Total dividend paid by investee

×

Percentage ownership

=

$25,000,000

×

40%

=

$10,000,000

(b)

=

×

40%

=

E10-14, cont.

Requirement 3

Long-Term Investments – Phase Motors

Jan. 6

360,000,000

10,000,000(a)

8,000,000(a)

Bal.

358,000,000

Calculated in Requirement 2.

E10-15 Classifying and accounting for stock investments

Learning Objectives 1, 3, 4

1. Dec. 31 Fair Value Adjustment—Trading CR $1,100

Hartford Today Publishers completed the following trading investment transactions during 2016 and

2017:

Requirements

1. Journalize Hartford Today’s investment transactions. Explanations are not required.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Dec. 6

Short-Term Investments—Trading

24,200(a)

Cash

24,200(a)

Cash

Dividend Revenue

Unrealized Holding Loss—Trading

Fair Value Adjustment—Trading

2017

Cash

23,760(d)

Loss on Disposal

440

Short-Term Investments—Trading

Calculations:

(a)

Total cost

=

Number of shares

×

Price per share

=

1,100 shares

×

$22.00 per share

=

$24,200

(b)

Total dividend received

=

Number of shares

×

Dividend per share

=

1,100 shares

×

=

(c)

Unrealized holding loss

=

Total fair value

=

=

E10-15

Requirement 1, cont.

(d)

Total cash received

=

Number of shares

×

Cash received per share

=

1,100 shares

×

$21.60 per share

=

$23,760

Loss on disposal

=

Total cash received

=

=

Requirement 2

Hartford Today would report the trading investment at its $23,100(a) fair value, classified as a current

asset on the balance sheet at December 31, 2016.

Calculated in Requirement 1.

E10-16 Computing rate of return on total assets

Learning Objective 5

Avg. total assets $315,000,000

Winter Exploration Company reported these figures for 2016 and 2015:

Compute the rate of return on total assets for 2016. (Round to two decimals.)

SOLUTION

The rate of return on total assets for 2016 is 11.81% (rounded).

Problems (Group A)

P10-17A Accounting for bond investments

Learning Objective 2

1. Dec. 31 Int. Rev. CR $15,750

Suppose Jenner and Sons purchases $700,000 of 4.5% annual bonds of McPhee Corporation at face

value on January 1, 2016. These bonds pay interest on June 30 and December 31 each year. They mature

on December 31, 2020. Jenner intends to hold the McPhee bond investment until maturity.

Requirements

1. Journalize Jenner and Sons’s transactions related to the bonds for 2016.

2. Journalize the entry required on the McPhee bonds maturity date. (Assume the last interest payment

has already been recorded.)

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 1

Long-Term Investments—Held-to-Maturity

700,000

Cash

700,000

Purchased investment in bonds.

Jun. 30

Cash

Interest Revenue

Received cash interest.

Dec. 31

Cash

Interest Revenue

Received cash interest.

P10-17A, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2020

Dec. 31

Cash

700,000

Disposed of bond at maturity.

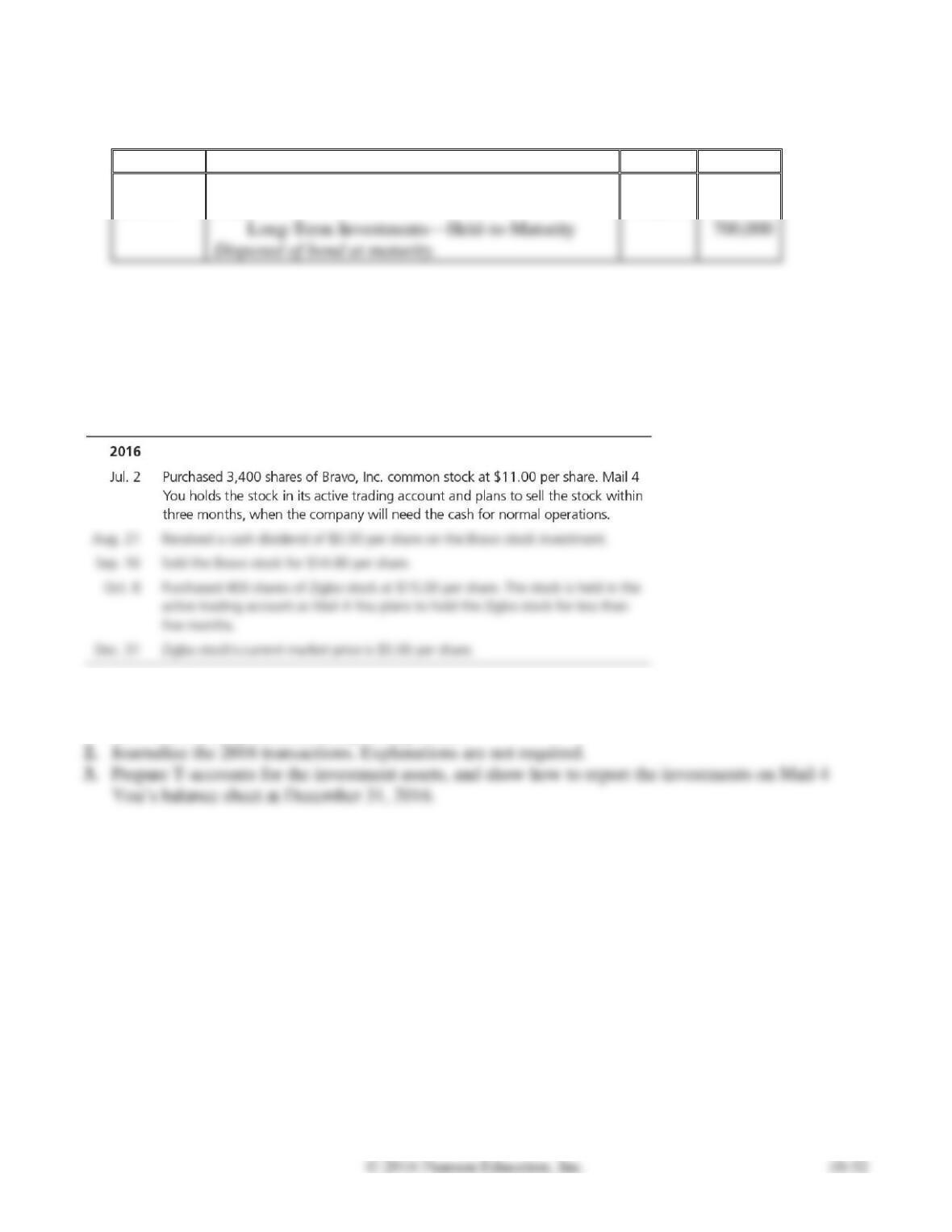

P10-18A Classifying and accounting for stock investments

Learning Objectives 1, 3, 4

2. Sep. 16 Gain on Disposal CR $12,920

Mail 4 You Corporation generated excess cash and invested in securities as follows:

Requirements

1. Classify each of the investments made during 2016. (Assume the investments represent less than

20% of ownership of outstanding voting stock.)

SOLUTION

Requirement 1

Both of the investments made during 2016 are trading investments because Mail 4 You owned less than

Requirement 2

Aug. 21

Cash

Dividend Revenue

Sep. 16

Cash

50,320(d)

Short-Term Investments—Trading

37,400(a)

Gain on Disposal

Oct. 8

Short-Term Investments—Trading

Cash

Dec. 31

Unrealized Holding Loss—Trading

Fair Value Adjustment—Trading

Date

Accounts and Explanation

Debit

Credit

2016

Jul. 2

Short-Term Investments—Trading

37,400(a)

Cash

37,400(a)

P10-18A, cont.

Requirement 2, cont.

Calculations:

(a)

Total cost

=

Number of shares

×

Price per share

=

3,400 shares

×

$11.00 per share

=

$37,400

(b)

Total dividend received

=

Number of shares

×

Dividend per share

=

3,400 shares

×

=

(c)

Gain on disposal

=

Total cash received

=

=

(d)

Total cash received

=

Number of shares

×

=

3,400 shares

×

=

$50,320

Total cost

=

Number of shares

×

Price per share

=

×

$15.00 per share

=

(f)

Unrealized holding loss

=

Total fair value

=

=

Total fair value

=

Number of shares

×

Market price (fair value) per share

=

×

=

P10-18A, cont.

Requirement 3

Short-Term Investments—Trading

Fair Value Adjustment—Trading

Jul. 2

Sep. 16

Dec. 31

Oct. 8

Bal.

MAIL 4 YOU CORPORATION

Balance Sheet (Partial)

December 31, 2016

Current Assets:

Calculated in Requirement 2.

P10-19A Accounting for stock investments

Learning Objectives 3, 4

1. Dec. 31 Fair Value Adjustment—AFS DR $36,000

The beginning balance sheet of Desk Source Co. included an $850,000 investment in Parson stock (20%

ownership). During the year, Desk Source completed the following investment transactions:

Requirements

1. Journalize the transactions for the year of Desk Source.

2. Post transactions to T-accounts to determine the December 31, 2016, balances related to the

investment and investment income accounts.

3. Prepare Desk Source’s partial balance sheet at December 31, 2016, from your answers in

Requirement 2.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Mar. 3

Long-Term Investments—Available-for-Sale

81,000(a)

Cash

81,000(a)

Purchased investment in stock.

Cash

Dividend Revenue

Received cash dividend.

Cash

Long-Term Investments—Parson

80,000

Received cash dividend (equity method).

Long-Term Investments—Parson

Revenue from Investments

60,000(c)

(equity method).

Fair Value Adjustment—Available-for-Sale

36,000(f)

Unrealized Holding Gain—Available-for-Sale

Adjusted available-for-sale investment to market value.

Calculations:

(a)

Total cost

=

Number of shares

×

Price per share

=

9,000 shares

×

$9 per share

=

$81,000

(b)

Total dividend received

=

Number of shares

×

Dividend per share

=

9,000 shares

×

$0.57 per share

=

P10-19A, cont.

Requirement 1, cont.

(c)

Revenue from

investments

=

Net income earned by investee

×

Percentage ownership

=

$300,000

×

20%

=

$60,000

recorded by the investor.

market value is made.

Unrealized holding gain

=

Total fair value

Total cost

=

=

(g)

Total fair value

=

Number of shares

×

=

×

=

Requirement 2

Long-Term Investments—AFS

Fair Value Adjustment—AFS

Mar. 3

81,000(a)

Dec. 31

36,000(a)

Bal.

81,000

Bal.

36,000

Long-Term Investments—Parson

Beg.

850,000

80,000

Dec. 15

Dec. 31

60,000(a)

Bal.

830,000

May 15

Dec. 31

5,130

Bal.

36,000

Bal.

Dec. 31

60,000

Bal.

(a)

P10-19A, cont.

Requirement 3

DESK SOURCE CO.

Balance Sheet (Partial)

December 31, 2016

Assets

Long-term Assets:

Long-term Investments—AFS (at fair value; cost $81,000(a))

$117,000(a)

Long-term Investments—Parson (equity method)

830,000(b)

Accumulated Other Comprehensive Income:

Unrealized Holding Gain—AFS

Calculated in Requirement 1.

Calculated in Requirement 2.

Problems (Group B)

P10-20B Accounting for bond investments

Learning Objective 2

1. Dec. 31 Int. Rev. CR $10,000

Suppose Ritter Brothers purchases $400,000 of 5% annual bonds of Clarkson Corporation at face value

on January 1, 2016. These bonds pay interest on June 30 and December 31 each year. They mature on

December 31, 2020. Ritter intends to hold the Clarkson bond investment until maturity.

Requirements

1. Journalize Ritter Brothers’s transactions related to the bonds for 2016.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

Jan. 1

Long-Term Investments—Held-to-Maturity

400,000

Cash

400,000

Purchased investment in bonds.

Jun. 30

Cash

Interest Revenue

Received cash interest.

Dec. 31

Cash

Interest Revenue

Received cash interest.

Calculations:

(a)

Semiannual interest

payment received

=

Face (par) value

×

Annual stated rate

×

½

=

$400,000

×

5%

×

½

=

received, because the bonds were purchased at face (par) value, rather than at

a discount or premium.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2020

Dec. 31

Cash

400,000

Long-Term Investments—Held-to-Maturity

400,000

Disposed of bond at maturity.