CHAPTER 10 • LONG-TERM LIABILITIES 10-19

LO 10 PROBLEM 10-7 DEFERRED TAX CALCULATIONS (Appendix)

1. 2014 Income before taxes ………………………………………………… $210,000

Excess of tax depreciation over

book depreciation ($50,000 – $26,667*) …………………. (23,333)

Taxable income ………………………………………………………. $186,667

2. 2014 Income before taxes ………………………………………………… $210,000

Income tax expense (35%) ……………………………………….. $ 73,500

3. Col. 1 Col. 2 Col. 3 Col. 4

Income Tax Income Tax Col. 1 – Deferred Tax

Year Expense Payable Col. 2 Account

2014 $73,500 $ 65,333 $ 8,167 $8,167 credit

10-20 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

MULTI-CONCEPT PROBLEMS

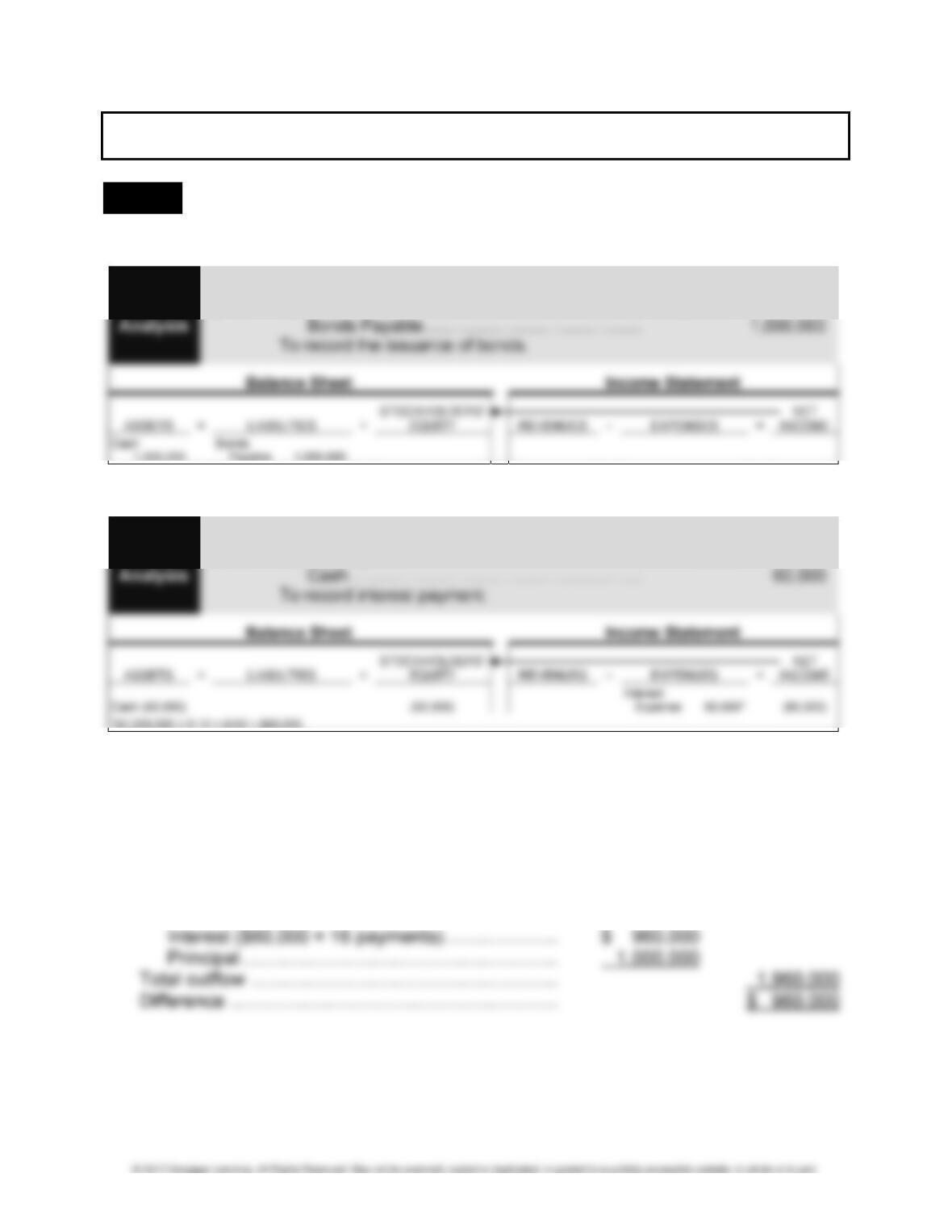

LO 4,5 PROBLEM 10-8 BOND TRANSACTIONS

1.

Journal 2016

Entry Apr. 1 Cash …………………………………………………………. 1,000,000

2.

Journal 2016

Entry Oct. 1 Interest Expense …………………………………………. 60,000

3. Additional interest must be recorded on December 31 to accrue interest for the time

period of October 1–December 31. The interest should be recorded as an expense

when it is incurred under the accrual accounting process. The accrual does not affect

the amount of interest paid on April 1, 2017. A full semiannual payment of $60,000

should occur on that date.

4. Total cash inflow to Brand ………………………………… $1,000,000

Total cash outflow:

CHAPTER 10 • LONG-TERM LIABILITIES 10-21

LO 1,8,10 PROBLEM 10-9 PARTIAL CLASSIFIED BALANCE SHEET FOR WALGREENS

1. The following is the Liabilities section of the consolidated balance sheet of

Walgreens at August 31, 2014. (All amounts are in millions.)

Current Trade accounts payable ……………………………… $4,315

2. Computation of debt-to-equity ratios:

2014: $16,621/$20,561 = 0.81

2013: $16,027/$19,454 = 0.82

3. Walgreens’ lenders want to be sure that the company can repay the principal and

pay the interest on the loan. They would be interested in Walgreens’ times interest

earned and debt service coverage ratios. Both ratios measure the degree to which a

company can make its debt payments out of current cash flows.

10-22 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

ALTERNATE PROBLEMS

LO 3 PROBLEM 10-1A FACTORS THAT AFFECT THE BOND ISSUE PRICE

1. a. The bonds would be issued at par, since the face or coupon rate is equal to the

market rate of interest.

2. a. $500,000 × 0.37689 (n = 20, i = 5%) = $188,445

$ 25,000* × 12.46221 (n = 20, i = 5%) = 311,555

Total $500,000

LO 5 PROBLEM 10-2A AMORTIZATION OF DISCOUNT

1. Discount Amortization

Effective Interest Method of Amortization

Col. 1 Col. 2 Col. 3 Col. 4

Cash Interest Discount

Interest Expense Amortized Carrying

Date 5% 8% Col. 2 – Col. 1 Value

1/01/16 $44,011

12/31/16 $ 2,500 $ 3,521** $1,021 45,032

2. Interest expense $18,489

Cash interest payments 12,500

Discount amortized $ 5,989

PROBLEM 10-2A (Concluded)

3.

Journal 2018

Entry Dec. 31 Interest Expense …………………………………………. 3,691

Analysis Discount on Bonds Payable …………………….. 1,191

Cash ……………………………………………………. 2,500

To record interest and amortization of discount.

Bonds payable ……………………………………………………………………………. $50,000

Discount on bonds payable …………………………………………………………… 2,674*

$47,326

*Total Discount – Amortization of Discount for Year 1, Year 2, and Year 3

= $5,989 – $1,021 – $1,103 – $1,191 = $2,674*

LO 5 PROBLEM 10-3A AMORTIZATION OF PREMIUM

1. Premium Amortization

Effective Interest Method of Amortization

Col. 1 Col. 2 Col. 3 Col. 4

Cash Interest Premium

Interest Expense Amortized Carrying

Date 5% 4% Col. 1 – Col. 2 Value

1/01/16 $52,227

12/31/16 $ 2,500 $ 2,089** $ 411 51,816

2. Interest expense $10,273

Cash interest payment 12,500

Premium amortized $ 2,227

10-24 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 10-3A (Concluded)

3.

Journal 2018

Entry Dec. 31 Interest Expense …………………………………………. 2,056

Analysis Premium on Bonds Payable …………………………. 444

Cash ……………………………………………………. 2,500

To record interest and amortization of premium.

*Total Premium – Amortization for Premium for Year 1, Year 2, and Year 3

= $2,227– $411 – $427 – $444 = $945

LO 6 PROBLEM 10-4A REDEMPTION OF BONDS

1. Redemption price ($100,000 × 1.01) ……………………………………. $101,000

Carrying value [$100,000 + ($5,500 – $2,000)] ………………………. 103,500

Gain on redemption …………………………………………………………… $ 2,500

2. Redemption price ($100,000 × 1.04) ……………………………………. $104,000

3. The gain or loss on bond redemption should be presented on the income statement.

4. Bonds are redeemed early only if it is advantageous to the issuing firm. However,

early redemption is usually not favorable to the investor because it usually means

CHAPTER 10 • LONG-TERM LIABILITIES 10-25

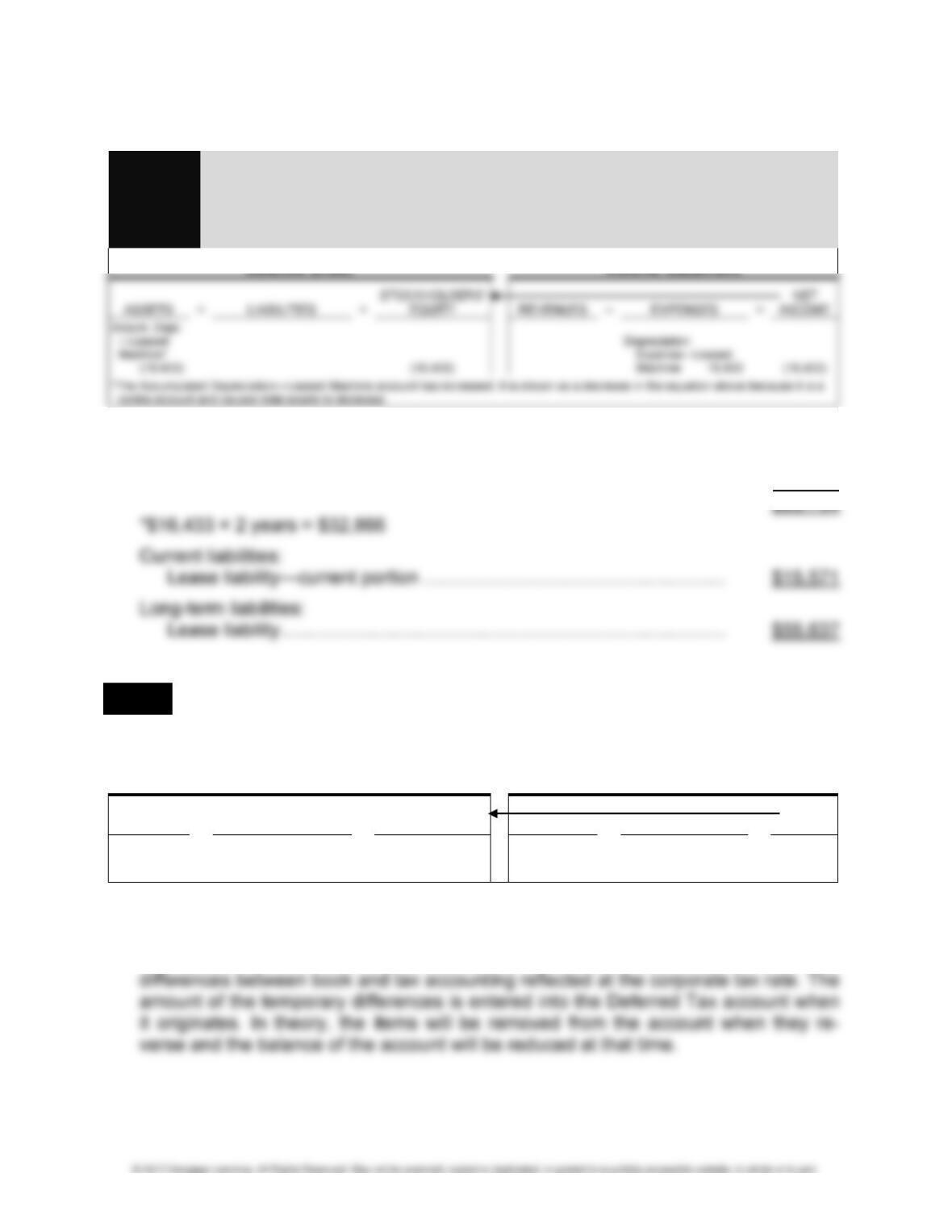

LO 7 PROBLEM 10-5A FINANCIAL STATEMENT IMPACT OF A LEASE

1. Col. 1 Col. 2 Col. 3 Col. 4

Interest Reduction of

Lease Expense Obligation Lease

Date Payment 9% Col. 1 – Col. 2 Obligation

1/01/16 $98,600

12/31/16 $21,980 $8,874** $13,106 85,494

2.

Journal 2016

Entry Jan. 1 Leased Machine …………………………………………. 98,600

Analysis Lease Liability ……………………………………….. 98,600

To record acquisition by lease.

3.

Journal 2017

Entry Dec. 31 Lease Liability …………………………………………….. 14,286

Analysis Interest Expense …………………………………………. 7,694

Cash ……………………………………………………. 21,980

To record payment of lease liability and interest.

10-26 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 10-5A (Concluded)

Journal Dec. 31 Depreciation Expense—Leased Machine ……….. 16,433

Entry Accumulated Depreciation—Leased

Analysis Machine …………………………………………….. 16,433

To record depreciation of leased asset.

Balance Sheet Income Statement

4. Long-term assets:

Leased machine …………………………………………………………………….. $98,600

Accumulated depreciation ……………………………………………………….. 32,866*

LO 10 PROBLEM 10-6A DEFERRED TAX (Appendix)

1. The effect on the accounting equation of the December 31, 2016, income tax ex-

pense, deferred tax, and income tax payable is as follows:

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Income Tax Payable 120

Deferred Tax (20)

(100)

Income Tax Expense

100

(100)

2. The Deferred Tax account exists to reconcile the difference between the accounting

done for tax purposes and that done for reporting to stockholders, also referred to as

book purposes. The balance of the Deferred Tax account represents all temporary

CHAPTER 10 • LONG-TERM LIABILITIES 10-27

LO 10 PROBLEM 10-7A DEFERRED TAX CALCULATIONS (Appendix)

1. Year 1 Income before taxes ……………………………………………. $120,000

Tax-exempt income …………………………………………….. (5,000)

Excess of tax depreciation over book

depreciation ($30,000 – $20,000) ……………………… (10,000)

2. The Deferred Tax account for Years 1–3 would contain the following information:

Year 1 entry: Tax expense greater than

tax payable ($10,000 × 40%) = $4,000 credit

10-28 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

ALTERNATE MULTI-CONCEPT PROBLEMS

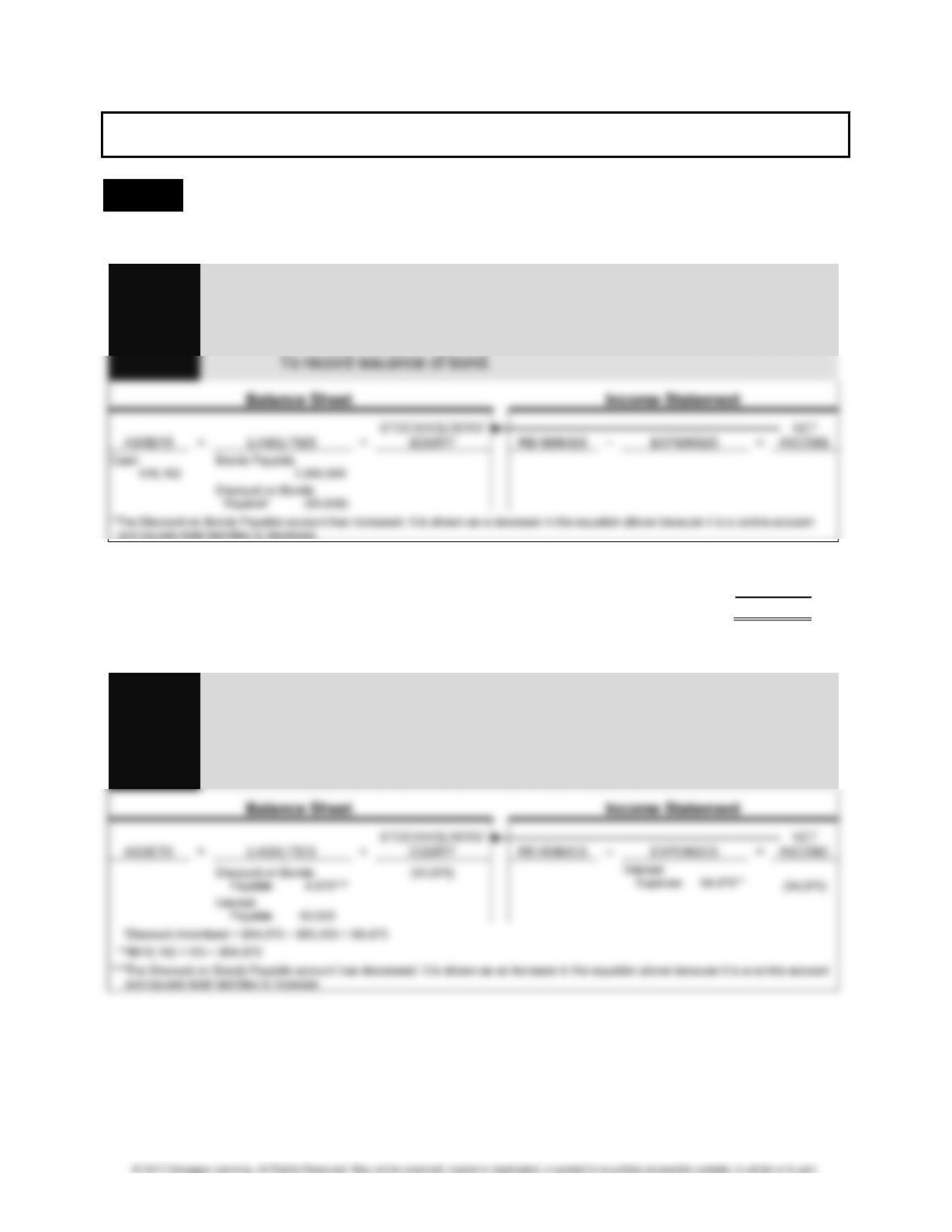

LO 4,6 PROBLEM 10-8A FINANCIAL STATEMENT IMPACT OF A BOND

1.

Journal 2016

Entry July 1 Cash …………………………………………………………. 916,162

Analysis Discount on Bonds Payable………………………….. 83,838

Bonds Payable ………………………………………. 1,000,000

$ 50,000* × 8.38384 (Table 9-4, n = 12, i = 6%) = $419,192

$1,000,000 × 0.49697 (Table 9-2, n = 12, i = 6%) = 496,970

$916,162

*$1,000,000 × 10% × 6/12 = $50,000

Journal 2016

Entry Dec. 31 Interest Expense ($916,162 × 6%) ………………… 54,970

Analysis Discount on Bonds Payable …………………….. 4,970*

Interest Payable …………………………………….. 50,000

To record interest and amortization of discount.

CHAPTER 10 • LONG-TERM LIABILITIES 10-29

PROBLEM 10-8A (Concluded)

3.

Journal 2017

Entry Jan. 1 Interest Payable ………………………………………….. 50,000

4. On the maturity date, July 1, 2022, the balance in Discount on Bonds Payable will

have been reduced to $0. The only remaining amount to be paid is the principal on

the bond as shown in the Bonds Payable account, $1,000,000.

LO 1,8,10 PROBLEM 10-9A PARTIAL CLASSIFIED BALANCE SHEET FOR BOEING

1. The following is the Liabilities section of the consolidated balance sheet of Boeing,

Inc., at December 31, 2013. (All amounts are in millions.)

Liabilities

Current liabilities:

10-30 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

2. Computation of debt-to-equity ratios:

2013

$77,666/$14,997= 5.18

2012

3. Boeing’s lenders want to be sure that the company can repay the principal and pay

the interest on the loan. They would be interested in Boeing’s times interest earned

and debt service coverage ratios. Both ratios measure the degree to which a com-

pany can make its debt payments out of current cash flows.

DECISION CASES

READING AND INTERPRETING FINANCIAL STATEMENTS

LO 1,8 DECISION CASE 10-1 EVALUATING THE LIABILITIES OF PANERA BREAD CO.

1. Panera Bread has the following long-term liabilities:

Long-term debt increased from 2013 to 2014.

2. Debt-to-equity ratio for 2014: $654,718/$736,184 = 0.89

Debt-to-equity ratio for 2013: $480,970/$699,892 = 0.69

Times interest earned for 2014: $279,118/$1,824 = 153.03

CHAPTER 10 • LONG-TERM LIABILITIES 10-31

LO 9,10 DECISION CASE 10-2 MAKING BUSINESS DECISIONS: COMPARING TWO

COMPANIES IN THE SAME INDUSTRY: PANERA BREAD AND CHIPOTLE

Part A. The Ratio Analysis Model

1. Formulate the Question:

The use of debt is a good management strategy, but sometimes a company may

have too much debt. The important questions to ask are:

What is the amount of debt in relation to the total equity of the company?

Will the company be able to meet its obligations related to the debt? That is, when

2. Gather the Information from the Financial Statements:

For those questions to be addressed, information from the balance sheet and the in-

3. Calculate the Ratio:

Debt-to-equity ratio for Panera Bread:

4. Compare the Ratio with Other Ratios:

The debt-to-equity ratio for the two companies is quite different. Chipotle carries a very

10-32 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

DECISION CASE 10-2 (Concluded)

Part B. The Business Decision Model

1. Formulate the Question:

If you were a lender, would you be willing to lend money to either or both companies

based on their use of debt?

2. Gather Information from the Financial Statements and Other Sources:

This information will come from a variety of sources, not limited to but including:

● The balance sheet provides information about the amount of debt and equity.

The income statement and statement of cash flows provide information about

3. Analyze the Information Gathered:

Whether a company is using leverage effectively is always a matter of judgment. For

4. Make the Decision:

Taking into account all of the various sources of information, decide either to

● Lend money to either company or

● Find an alternative use for the money

5. Monitor Your Decision:

If you decide to lend money, you will need to monitor your investment periodically.

CHAPTER 10 • LONG-TERM LIABILITIES 10-33

LO 9,10 DECISION CASE 10-3 READING PEPSICO’S STATEMENT OF CASH FLOWS

1. Proceeds from debt is a positive amount on the cash flows statement because it in-

2. When interest rates are at low levels, companies often pay off loans that carry inter-

3. A company may repurchase stock for several reasons. The company may want to

eliminate a certain class of stock or reduce the need to pay dividends. The company

may also want to have more control of its stock by having the stock in the hands of

fewer stockholders. Finally, when a company repurchases stock, this does have a

positive impact on its earnings per share.

MAKING FINANCIAL DECISIONS

LO 1,7 DECISION CASE 10-4 MAKING A LOAN DECISION

1. The bank’s policy is that a 2-to-1 ratio of assets to debt must be maintained. The

note in Molitor’s annual report indicates that generally accepted accounting princi-

2. The bank should adopt a more flexible policy to consider those financing techniques

that are off-balance-sheet. However, it is very difficult to develop a policy that ac-

10-34 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 6 DECISION CASE 10-5 BOND REDEMPTION DECISION

DATE:

TO: Controller

FROM: Student Name

RE: Retirement of Outstanding Bonds

The outstanding bonds require the company to continue to pay 10% in a market that

requires only a 4% return. If the company issues new bonds at 4%, the new issuance

will yield the company $100,000 and the interest cash payment will be much lower at

ETHICAL DECISION MAKING

LO 7 DECISION CASE 10-6 DETERMINATION OF ASSET LIFE

1. Recognize an ethical dilemma:

2. Analyze the key elements in the situation:

Even though criteria exist that govern lease accounting, significant judgment is

3. List alternatives and evaluate the impact of each on those affected:

Whether to record an asset as an operating lease or capital lease can have a potential

CHAPTER 10 • LONG-TERM LIABILITIES 10-35

DECISION CASE 10-6 (Concluded)

4. Select the best alternative:

If Jen believes that the first source of information is valid, she should record the

lease as a capital lease. If the trade publication is more valid, she should record the

lease as an operating lease. Jen should gather additional information and consult