21

following closing. Targacept shareholders ownership would increase to 49% from 35% at closing if the notes are

fully converted.

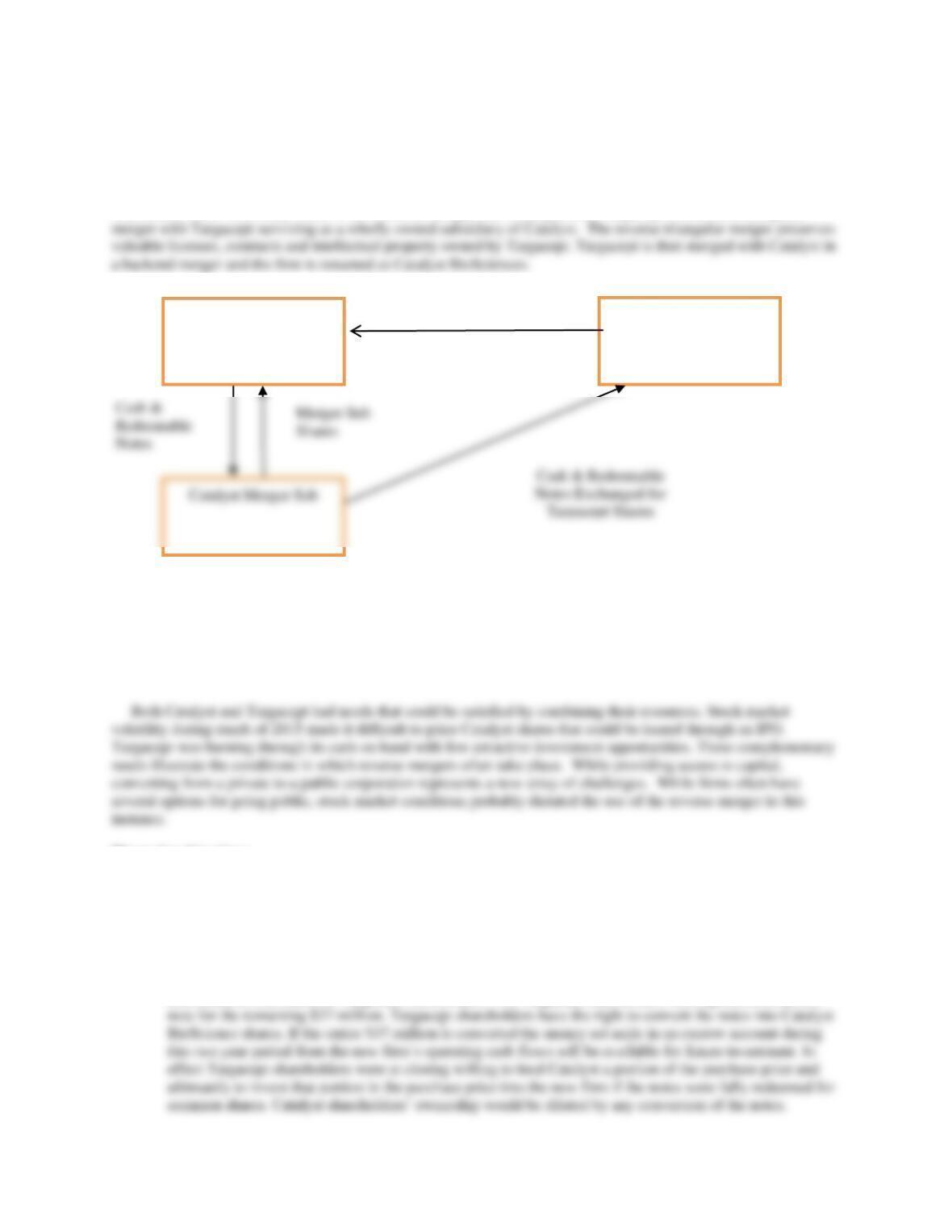

Figure 10.1 illustrates how ownership is transferred in a typical reverse merger. Catalyst creates a wholly owned

subsidiary shell corporation (Merger Sub) and exchanges the shares of the Merger Sub for $20 million in cash and

redeemable notes with a face value of $37 million. Merger sub is merged with Targacept in a reverse triangular

Figure 10.1 Reverse Merger Process

Shares of Targacept common stock were listed on the NASDAQ Global Select Market under the symbol

“TRGT.” Prior to completion of the merger, Targacept filed an initial listing application with the NASDAQ Global

Select Market relating on behalf of the combined company, subject to NASDAQ “reverse merger” rules. After

completion of the merger, Targacept was renamed “Catalyst Biosciences, Inc.” and trades on the NASDAQ Global

Select Market under the symbol “CBIO.”

Discussion Questions

1. What is the purchase price of Targacept and how is it financed? How does this financing structure

potentially help the combined firm Catalyst BioSciences fund future spending? How would Catalyst’s

original shareholders be impacted by a conversion of the notes?

Answer: The purchase price paid to Targacept shareholders is $57 million consisting of $20 million in cash

and redeemable notes of $37 million. The cash is distributed from Targacept’s cash on hand and is

distributed as a dividend to Targacept shareholders. The Targacept shareholders have agreed to assume a

Catalyst

Targacept

Targacept Becomes Wholly

Owned Sub of Catalyst

22

2. What are common reasons for a private firm to go public? What are the advantages and disadvantages or

doing so? Be specific.

Answer: Common reasons for a firm to go public include the ability to obtain capital, to obtain an

acquisition currency, to liquidate some portion of the founder’s share holdings, and to offer incentive stock

3. What are corporate shells, and how can they create value? Be specific.

Answer: A corporate shell is a corporation usually without any significant operating assets and liabilities.

4. Discuss the pros and cons of a reverse merger versus an IPO.

Answer: Many small businesses fail each year. In a number of cases, all that remains is a business with no

significant assets or operations. Such companies are referred to as shell corporations. Shell corporations

can be used as part of a deliberate business strategy in which a corporate legal structure is formed in

5. What is the purpose of private firm in listing of a major stock exchange such as NASDAQ?

Answer: Larger public stock exchanges offer substantially larger trading volumes than the Pink Sheets and

OTC Bulletin Board. Therefore, they are likely to provide greater liquidity for Catalyst’s shares offering

Privately Owned La Boulange Café & Bakery Goes Nationwide

23

_____________________________________________________________________________________

Key Points

• Financing growth represents a common challenge for most small businesses.

• Selling a portion of a business either to other investors, in a public offering, or to a strategic buyer

represents common ways for small businesses to finance major expansion plans.

____________________________________________________________________________

Founded in 1999 as La Boulangerie, the business started as a store front with an oven in the back room. The

founder, Pascal Rigo who started baking in France at age seven, lived above that store for nine years. The first store

became a prototype for what was to become La Boulange Café & Bakery with nineteen sites across the San

Francisco bay area, with the business eventually sold to Starbucks in 2013.

In 2005, Rigo was able to expand the number of locations by partnering with Next World Group, a privately

held investment firm that provided much needed financing. The business was managed as a subsidiary of Bay

Bread Group, a holding company, which also operated the Bay Bread Company. The long-term business objective

was to take the La Boulange Café & Bakery nationwide. However, limited resources meant that the roll out would

take a long time.

With food current accounting for about 20 percent or $1.5 billion of the firm’s total annual revenue, Starbucks

looked at the acquisition as an opportunity to bring high-quality pastries and bread into its locations nationwide.

The acquisition provides an entrée into the casual restaurant industry, putting the firm potentially in direct

competition with the likes of Panera Bread Co. and its 1500 locations across the country. Starbuck’s believes that

the inclusion of La Boulange-branded French pastries, croissants, breads, and muffins will drive traffic and cause

Shell Game: STK Steakhouse Chain Goes Public

Through a Reverse Merger

_____________________________________________________________________________________

Case Study Objectives: To illustrate

• Some of the motivations for “going public,”

• The mechanics of reverse mergers, and

• Risks and rewards associated with reverse mergers.

Introduction

With growth slowed by limited resources, a robust stock market, and intensifying investor interest in high-end

restaurant dinning chains, One Group LLC, the owner of steakhouse chain STK faced a critical decision. Should

The Decision

The timing appeared to be right. The broad stock market indices were up by almost 30% during the first nine

months of 2013 over the same period the prior year. Niche high-end restaurant chains appeared to be in vogue. In

mid-2013, Del Frisco’s Restaurant Group undertook an IPO at $13 per share. Since then its shares have risen by

40%. In early October 2013, hedge fund Barrington Capital took a 2.8% stake in Darden Restaurants Inc. urging

the dining conglomerate to separate its faster growing Capital Grille and Eddie V’s from its larger restaurant chains

through spin-offs or divestitures.

Committed Capital Acquisition Group (CCAC), a special purpose acquisition company (SPAC), seemed to offer

an immediate vehicle for entering the public stock market. SPACs are shell or so-called blank-check companies

that have no operations but which raise funds through an initial public offering with the intention of merging with

The Process

The combination of One Group and CCAC involved a process called a reverse merger. To undertake a reverse

merger, a firm finds a shell corporation with relatively few shareholders who are interested in selling their stock.

The shell corporation’s shareholders often are interested in either selling their shares for cash, owning even a

relatively small portion of a financially viable company to recover their initial investments, or in transferring the

25

In a merger, it is common for the surviving firm to be viewed as the acquirer, since its shareholders usually end

up with a majority ownership stake in the merged firms; the other party to the merger is viewed as the target firm as

its former shareholders often hold only a minority interest in the combined companies. In a reverse merger, the

In recent years, private equity investors have found the comparative ease of the reverse merger process

convenient, because it has enabled them to take public their investments in both domestic and foreign firms. The

story of the rapid growth of Chinese firms has held considerable allure for investors prompting a flurry of reverse

mergers involving Chinese-based firms. With speed comes additional risk. Shell company shareholders may

simply be looking for investors to take over their liabilities such as pending litigation, safety hazards,

The Deal

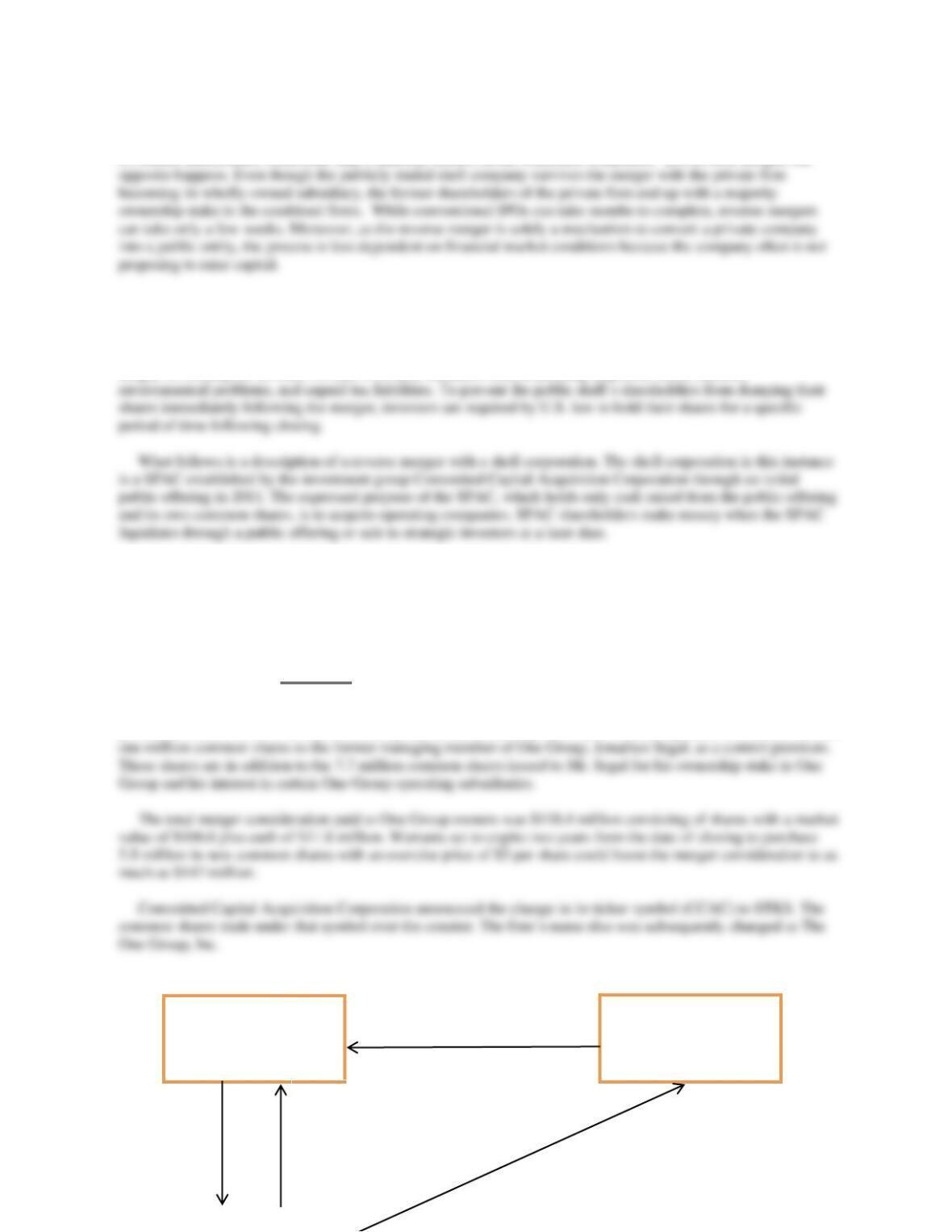

On October 16, 2013, Committed Capital Acquisition Corporation (CCAC), a publicly traded Delaware

Corporation, agreed to merge its wholly-owned CCAC Acquisition Sub (Merger Sub) into One Group LLC.

CCAC had created Merger Sub transferring cash and its common shares in exchange for all of Merger Sub’s

shares. One Group was the surviving legal entity of the merger. As such One Group became a wholly-owned

subsidiary of CCAC. See Figure 10.1.

Simultaneously, CCAC issued 12.6 million shares of its common shares having a par value of $.0001 per share

plus $11.8 million in cash for their ownership interest (membership interest) in One Group LLC. CCAC also issued

Committed Capital

Acquisition Corporation

(The Company)

One Group LLC

Cash &

CCAC

Common

Shares

Merger Sub

Shares

One Group Becomes

Wholly-Owned CCAC Sub

Membership Interests

26

Coinciding with the closing date, CCAC completed a private placement of 3.1 million common shares at a

purchase price of $5 to investors consisting of some CCAC’s existing shareholders realizing proceeds of $15.5

million. In connection with the private placement, CCAC agreed to register the shares with the Securities and

Exchange Commission within 120 days of closing. This activity is sometimes called private investment in public

equity or PIPE financing.

Concluding Comments

One Group had the choice of remaining private or taking STK public. Each ownership structure has its pros and

cons. For example, after twenty years as a publicly traded company, Dell Inc. converted from to a private

Discussion Questions

1. What are common reasons for a private firm to go public? What are the advantages and disadvantages or

doing so? Be specific.

Answer: Common reasons for a firm to go public include the ability to obtain capital, to obtain an

acquisition currency, to liquidate some portion of the founder’s share holdings, and to offer incentive stock options

to the firm’s management that can be exercised with the shares easily sold in a liquid market. The disadvantages of

2. What are corporate shells, and how can they create value? Be specific.

Answer: A corporate shell is a corporation usually without any significant operating assets and liabilities. Such

3. What were the options available to One Group LLC to raise capital to finance their expansion plans? Discuss

the pros and cons of each. Be specific.

27

Answer: Options available to One Group included borrowing from banks or hedge funds, entering into a private

equity placement with a hedge fund or private equity investor group, undertaking an initial public offering, and

going public through a reverse merger. (Since One Group is a limited liability company, a private placement would

involve the sale of units rather than shares unless it converted to a C corporation before the sale.)

4. Discuss the pros and cons of a reverse merger versus an IPO.

Answer: Many small businesses fail each year. In a number of cases, all that remains is a business with no

significant assets or operations. Such companies are referred to as shell corporations. Shell corporations can be

used as part of a deliberate business strategy in which a corporate legal structure is formed in anticipation of future

financing, a merger, joint venture, spin-off, or some other infusion of operating assets. This may be accomplished

5. Why is it likely that shares trade at a discount from their value when issued if investors attempted to sell

such shares within one year following closing of the reverse merger?

Answer: Following a reverse merger, the operating company is technically public in that its shares once

registered with the SEC are traded on the Pink Sheets or OTC Bulletin Board. Such shares under current U.S.

28

6. What is the purpose of ultimately listing of a major stock exchange such as NASDAQ?

Answer: Larger public stock exchanges offer substantially larger trading volumes than the Pink Sheets and

OTC Bulletin Board. Therefore, they are likely to offer greater liquidity for One Group’s shares offering greater

Shell Game: Going Public through Reverse Mergers

___________________________________________________________________________________________

Key Points

Reverse mergers represent an alternative to an initial public offering (IPO) for a private company wanting to “go

public.”

The challenge with reverse mergers often is gaining access to accurate financial statements and quantifying current

or potential liabilities.

Performing adequate due diligence may be difficult, but it is the key to reducing risk.

______________________________________________________________________________

The highly liquid U.S. equity markets have proven to be an attractive way of gaining access to capital for both

privately owned domestic and foreign firms. Common ways of doing so have involved IPOs and reverse mergers.

While both methods allow the private firm’s shares to be publicly traded, only the IPO necessarily results in raising

capital, which affects the length of time and complexity of the process of “going–public.”

To undertake a reverse merger, a firm finds a shell corporation with relatively few shareholders who are

interested in selling their stock. The shell corporation’s shareholders often are interested in either selling their shares

for cash, owning even a relatively small portion of a financially viable company to recover their initial investments,

In a merger, it is common for the surviving firm to be viewed as the acquirer, since its shareholders usually end

up with a majority ownership stake in the merged firms; the other party to the merger is viewed as the target firm

because its former shareholders often hold only a minority interest in the combined companies. In a reverse merger,

the opposite happens. Even though the publicly traded shell company survives the merger, with the private firm

becoming its wholly owned subsidiary, the former shareholders of the private firm end up with a majority ownership

stake in the combined firms. While conventional IPOs can take months to complete, reverse mergers can take only a

few weeks. Moreover, as the reverse merger is solely a mechanism to convert a private company into a public entity,

the process is less dependent on financial market conditions because the company often is not proposing to raise

capital.

29

The reverse merger process employed by Allied, the privately owned operating company and owner of Huiheng,

to merge with Mill, the public shell corporation, early in 2008 to become a publicly listed firm is described in the

following steps. Allied is the target firm, and Mill is the acquiring firm.

Step 1. Negotiate terms and conditions: Premerger, Mill and Allied had 10,150,000 and 13,000,000 common

shares outstanding, respectively. Mill also had 266,666 preferred shares outstanding. Mill and Allied agreed to a

Step 2. Recapitalize the acquiring firm: Prior to the share exchange, shareholders in Mill, the shell corporation,

recapitalized the firm by contributing 9,700,000 of the shares they owned prior to the merger to Treasury stock,

Step 3. Close the deal: The terms of the merger called for Mill (the acquirer) to purchase 100% of the outstanding

Allied (the target) common and preferred shares, which required Mill to issue 13,000,000 new common shares and

266,666 new preferred shares. All premerger Allied shares were cancelled. Mill Basin Technologies was renamed

30

Exhibit 10.4 Mill Basin Technologies (Mill)

Pre-Merger Equity Structure:

Common 10,150,000

Series A Preferred 266,666

Recapitalized Equity Structure

Common 450,000a

Series A Preferred 266,666

New Mill Shares Issued to Acquire 100% of Allied shares

aMill shareholders contributed 9,700,000 shares of their pre-merger holdings to treasury stock cutting the

number of Mill shares outstanding to 450,000 in order to reduce the total number of shares outstanding

postmerger, which would equal Mill’s premerger shares outstanding plus the newly issued shares. This also

could have been achieved by the Mill shareholders agreeing to a reverse stock split. The 10,150,000 pre-

merger Mill shares outstanding could be reduced to 450,000 through a reverse split in which Mill

shareholders receive 1 new Mill share for each 22.555 outstanding prior to the merger.

bPost-Merger Mill Basin Technologies’ capital structure equals the 450,000 premerger Mill common shares

resulting from the recapitalization plus the 13,000,000 newly issued common shares plus 266,666 Series A

preferred shares.

c(13,000,000/13,450,000)

Huiheng ran into legal problems soon after its reverse merger. Harborview Master Fund, Diverse Trading Ltd.,

and Monarch Capital Fund, institutional investors having a controlling interest in Huiheng, approved the reverse

Discussion Questions

1. What are common reasons for a private firm to go public?

Answer: Common reasons for a firm to go public include the ability to obtain capital, to obtain an

31

2. What is a corporate shell and how can they create value?

Answer: A corporate shell is a firm usually without any significant operating assets and liabilities. Such

3. Who are the key participants in the case study and what are their roles in the reverse merger?

Answer: Mill Basin Technologies and Allied Moral Holdings are the publicly listed shell corporation and

4. Discuss the pros and cons of a reverse merger versus an initial public offering for taking a company public.

Answer: Many small businesses fail each year. In a number of cases, all that remains is a business with no

significant assets or operations. Such companies are referred to as shell corporations. Shell corporations

can be used as part of a deliberate business strategy in which a corporate legal structure is formed in

5. What are the auditing challenges associated with reverse mergers? How can investors protect themselves

from the liabilities that may be contained in corporate shells?

Answer: Auditing challenges could include the following: collusion between local bank branches and

company executives in confirming the firm’s bank cash balances; collusion between vendors and customers

32

6. Mill was recapitalized just prior to completing its merger with Allied. What was the purpose of the

recapitalization? Did it affect the ability of the combined firm’s to generate future earnings? Explain your

answers.

Answer: The recapitalization of Mill was intended to reduce the number of Mill common shares that Allied

would have to acquire in the share for share exchange. In doing so, the total number of shares outstanding

Determining Liquidity Discounts: The Taylor Devices and Tayco Development Merger

____________________________________________________________________________________________

Key Points

Privately held shares or shares for which there is not a readily available resale market often can only be sold at a

discount from what is believed to be their intrinsic value.

However, estimating the magnitude of the discount often is highly problematic.

____________________________________________________________________________________________

This discussion10 is a highly summarized version of how a business valuation firm evaluated the liquidity risk

associated with Taylor Devices’ unregistered common stock, registered common shares, and a minority investment

in a business that it was planning to sell following its merger with Tayco Development. The estimated liquidity

discounts were used in a joint proxy statement submitted to the SEC by the two firms to justify the value of the offer

the boards of Taylor Devices and Tayco Development had negotiated.