CHAPTER 10

Long-Term Liabilities

OVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated

Time in

Learning Objectives Exercises Minutes Level

Module 1

1. Identify the components of the Long-Term Liability

category of the balance sheet.

2. Define the important characteristics of bonds payable. 1 10 Easy

Module 2

5. Find the amortization of premium or discount 15* 15 Mod

using the effective interest method. 16* 15 Mod

17* 20 Mod

6 10 Mod

Module 3

7. Determine whether a lease agreement must be 7 10 Mod

reported as a liability on the balance sheet. 8 10 Mod

9 20 Mod

Module 4

8. Explain how inventors use ratios to evaluate long-term

liabilities.

12 10 Mod

Module 5

10. Explain deferred taxes and calculate the deferred tax liability 13 5 Easy

(Appendix). 14 10 Easy

*Exercise, problem, or case covers two or more learning objectives

Level = Difficulty levels: Easy; Moderate (Mod); Difficult (Diff)

10-2 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Problems Estimated

and Time in

Learning Objectives Alternates Minutes Level

Module 1

1. Identify the components of the Long-Term Liability 9 20 Mod

category of the balance sheet.

Module 2

5. Find the amortization of premium or discount 2 25 Mod

using the effective interest method. 3 25 Mod

8# 20 Mod

8** 20 Mod

Module 3

7. Determine whether a lease agreement must be 5 35 Diff

reported as a liability on the balance sheet.

Module 4

8. Explain how investors use ratios to evaluate long-term 9* 20 Mod

liabilities.

Module5

10. Explain deferred taxes and calculate the deferred tax liability 6 15 Mod

(Appendix). 7 30 Diff

9* 20 Mod

CHAPTER 10 • LONG-TERM LIABILITIES 10-3

Estimated

Time in

Learning Objectives Cases Minutes Level

Module 1

1. Identify the components of the Long-Term Liability 1* 40 Mod

category of the balance sheet. 4* 25 Mod

2. Define the important characteristics of bonds payable.

Module 2

5. Find the amortization of premium or discount

using the effective interest method.

Module 3

7. Determine whether a lease agreement must be 4* 25 Mod

reported as a liability on the balance sheet. 6 30 Mod

Module 4

8. Explain how investors use ratios to evaluate long-term 1* 25 Mod

liabilities.

Module 5

10. Explain deferred taxes and calculate the deferred tax liability 2* 40 Mod

(Appendix). 3* 25 Mod

10-4 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISES

LO 2 EXERCISE 10-1 RELATIONSHIPS

Cash Interest Amort. Carrying

Interest Expense Disc./Prem. Value

LO 3 EXERCISE 10-2 ISSUE PRICE

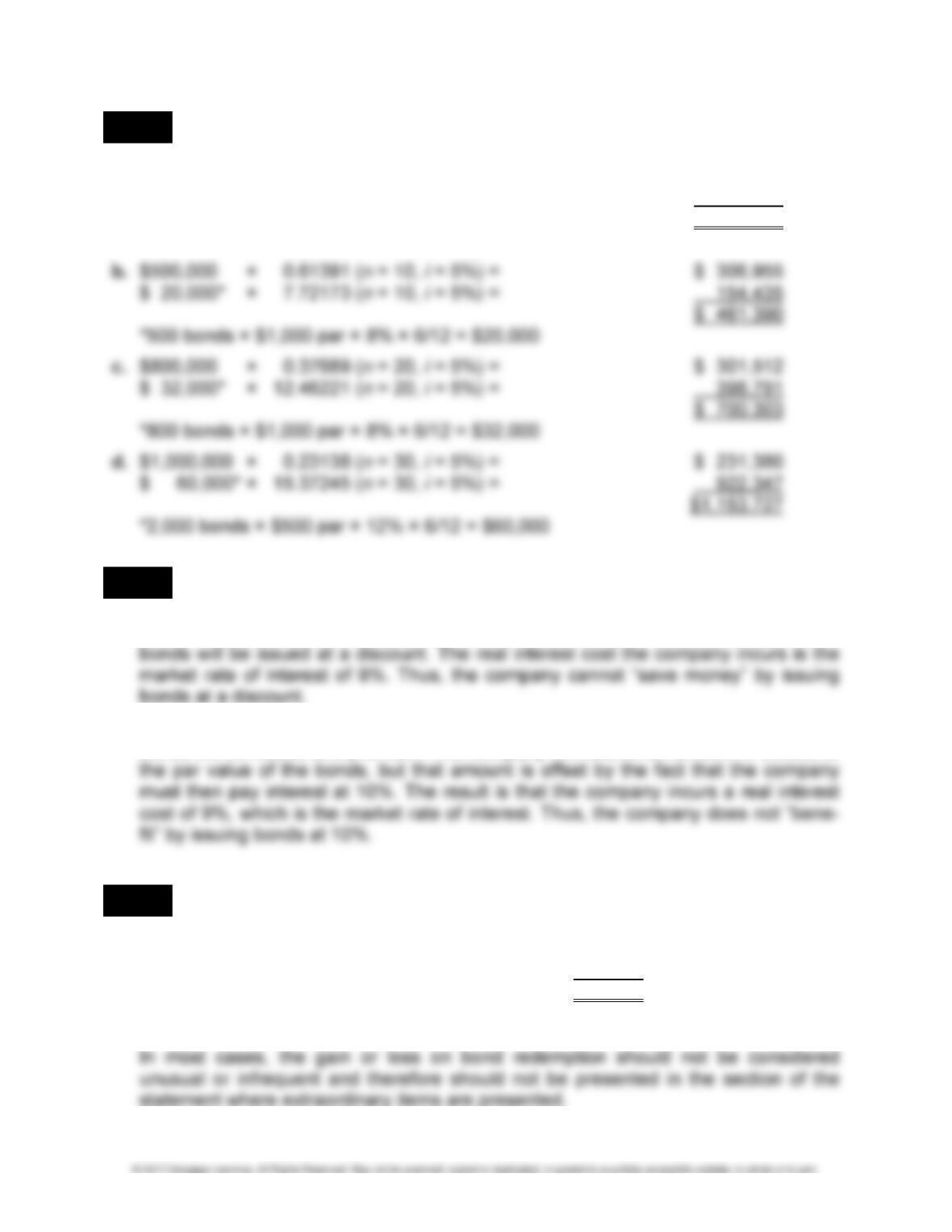

1. a. $500,000

2. a. $500,000 × 8% × 1/2 year = $20,000

3. a. $ 20,000 × 13.59033 (Table 9-4, n = 20, i = 4%) = $271,807

$500,000 × 0.45639 (Table 9-2, n = 20, i = 4%) = 228,195

Issue price $500,002*

*Should equal $500,000; the difference is due to rounding in present value

factors.

CHAPTER 10 • LONG-TERM LIABILITIES 10-5

LO 3 EXERCISE 10-3 ISSUE PRICE

a. $500,000 × 0.62092 (n = 5, i = 10%) = $ 310,460

$ 40,000* × 3.79076 (n = 5, i = 10%) = 151,630

$ 462,090

*500 bonds × $1,000 par × 8% = $40,000

LO 4 EXERCISE 10-4 IMPACT OF TWO BOND ALTERNATIVES

1. If the company issues bonds with a face rate of 8% when the market rate is 9%, the

2. If the company issues bonds with a face rate of 10% when the market rate is 9%, the

bonds will be issued at a premium. The company will receive an amount in excess of

LO 6 EXERCISE 10-5 REDEMPTION OF BONDS

1. Redemption price: $75,000 × 1.03 = $ 77,250

Carrying value: $75,000 – $1,750 = 73,250

$ (4,000) loss

2. The gain or loss on bond redemption should be presented on the income statement.

10-6 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 6 EXERCISE 10-6 REDEMPTION OF A BOND AT MATURITY

Since the bonds are fully matured, the carrying value equals the face value and there

will be no gain or loss on the redemption of the bonds.

The effect on the accounting equation of the redemption of the bonds is as follows:

LO 7 EXERCISE 10-7 LEASED ASSET

1. Payment × Table Factor Ord. Annuity = PV Min. Lease Payments

LO 7 EXERCISE 10-8 FINANCIAL STATEMENT IMPACT OF A LEASE

1. Payment × Table Factor Ord. Annuity = PV Min. Lease Payment

2. $9,508.65

Lease Interest Reduction of Lease

Date Payment Expense Obligation Obligation

CHAPTER 10 • LONG-TERM LIABILITIES 10-7

LO 7 EXERCISE 10-9 LEASED ASSETS

1. a. The value of the forklift will not appear on the balance sheet.

b. The lease payments will appear on the income statement as lease expense.

2. a.

b.

Journal Dec. 31 Lease Liability ……………………………………….. 1,110

Entry Interest Expense ……………………………………. 400*

Analysis Cash ………………………………………………. 1,510

To record lease payment.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash (1,510) Lease Liability (1,110) (400) Interest Expense 400* (400)

*$5,001 × 8% = $400

10-8 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 9 EXERCISE 10-10 IMPACT OF TRANSACTIONS INVOLVING BONDS ON

STATEMENT OF CASH FLOWS

F—Proceeds from issuance of bonds payable

LO 9 EXERCISE 10-11 IMPACT OF TRANSACTIONS INVOLVING CAPITAL LEASES ON

STATEMENT OF CASH FLOWS

1. Garnett obtained the equipment by signing a lease; no cash changed hands. As a

2. F—Reduction of lease obligation (principal portion of lease payment)

O—Interest expense

O—Depreciation expense—leased assets

LO 9 EXERCISE 10-12 IMPACT OF TRANSACTIONS INVOLVING TAX LIABILITIES ON

STATEMENT OF CASH FLOWS

LO 10 EXERCISE 10-13 TEMPORARY AND PERMANENT DIFFERENCES (Appendix)

1. Permanent 4. Temporary

CHAPTER 10 • LONG-TERM LIABILITIES 10-9

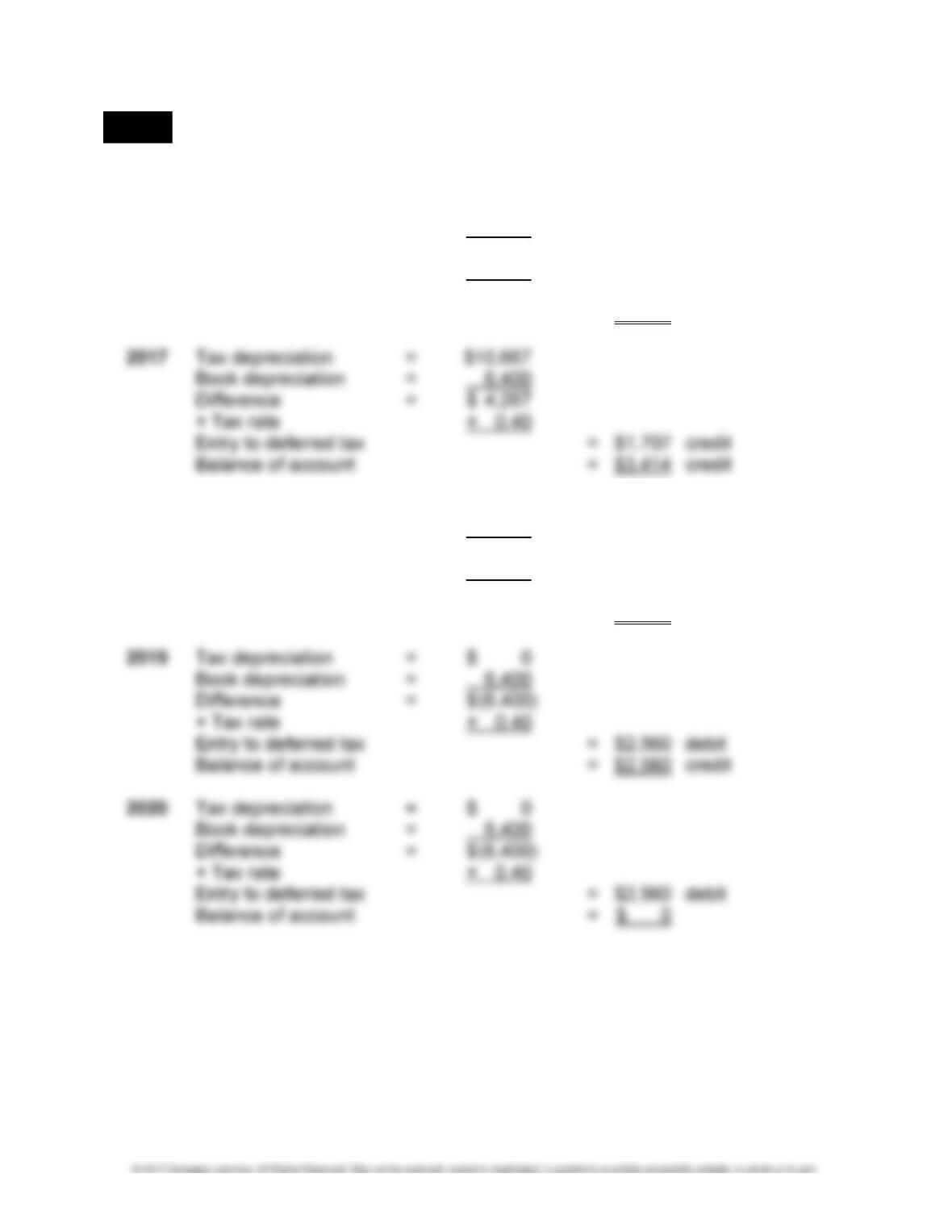

LO 10 EXERCISE 10-14 DEFERRED TAX (Appendix)

Balance of deferred tax account:

2016 Tax depreciation = $10,667

Book depreciation = 6,400

Difference = $ 4,267

× Tax rate × 0.40

Entry to deferred tax = $1,707 credit

Balance of account = $1,707 credit

2018 Tax depreciation = $10,666

Book depreciation = 6,400

Difference = $ 4,266

× Tax rate × 0.40

Entry to deferred tax = $1,706 credit

Balance of account = $5,120 credit

10-10 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

MULTI-CONCEPT EXERCISES

LO 4,5 EXERCISE 10-15 ISSUANCE OF A BOND AT FACE VALUE

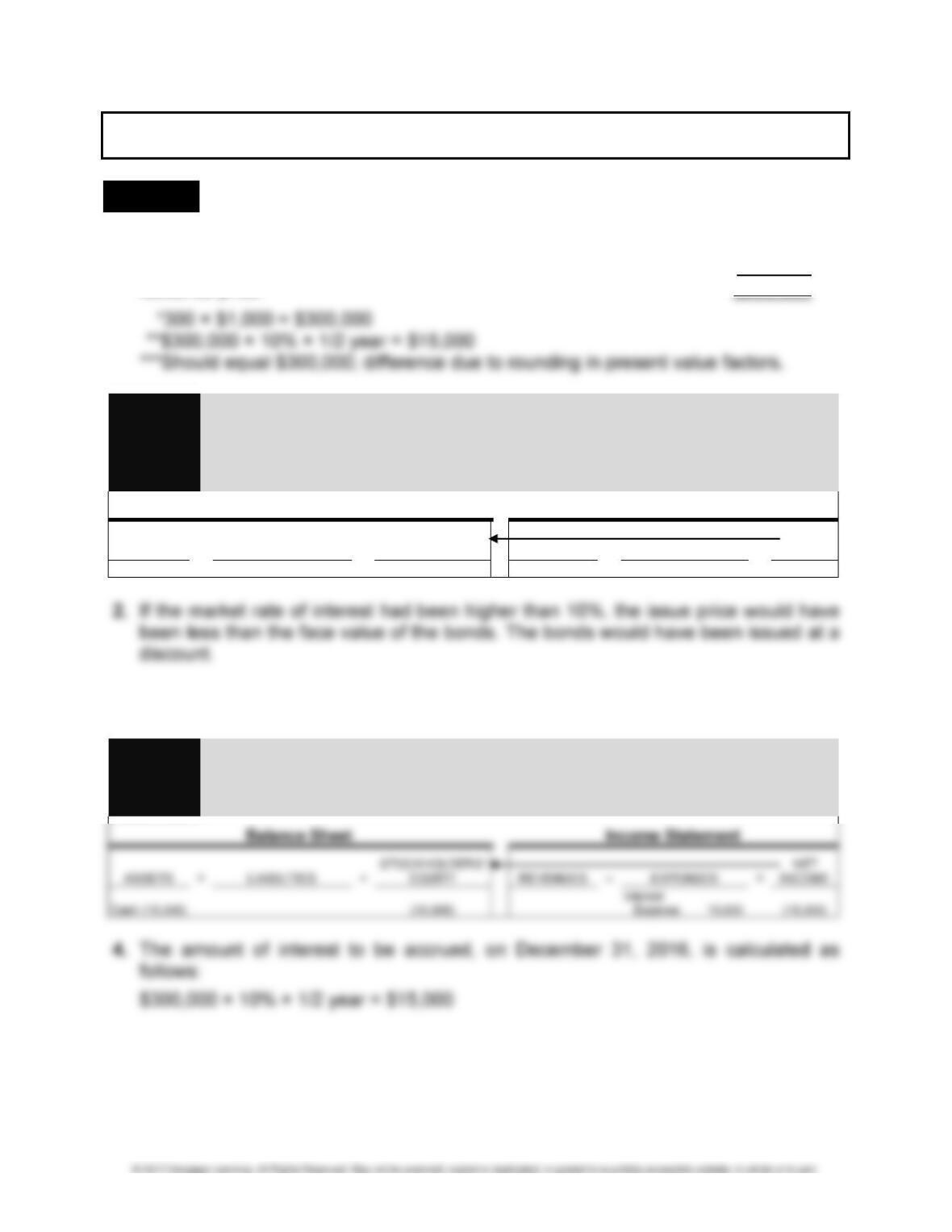

1. $300,000* × 0.61391 (Table 9-2, n = 10, i = 5%) = $184,173

$ 15,000** × 7.72173 (Table 9-4, n = 10, i = 5%) = 115,826

Issuance price $299,999***

Journal 2016

Entry Jan. 1 Cash …………………………………………………………. 300,000

Analysis Bonds Payable ………………………………………. 300,000

To record issuance of bond.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 300,000 Bonds Payable 300,000

3. The effect on the accounting equation of the payment of interest, on July 1, 2016, is

as follows:

Journal July 1 Interest Expense …………………………………………. 15,000

Entry Cash ……………………………………………………. 15,000

Analysis To record payment of interest.

CHAPTER 10 • LONG-TERM LIABILITIES 10-11

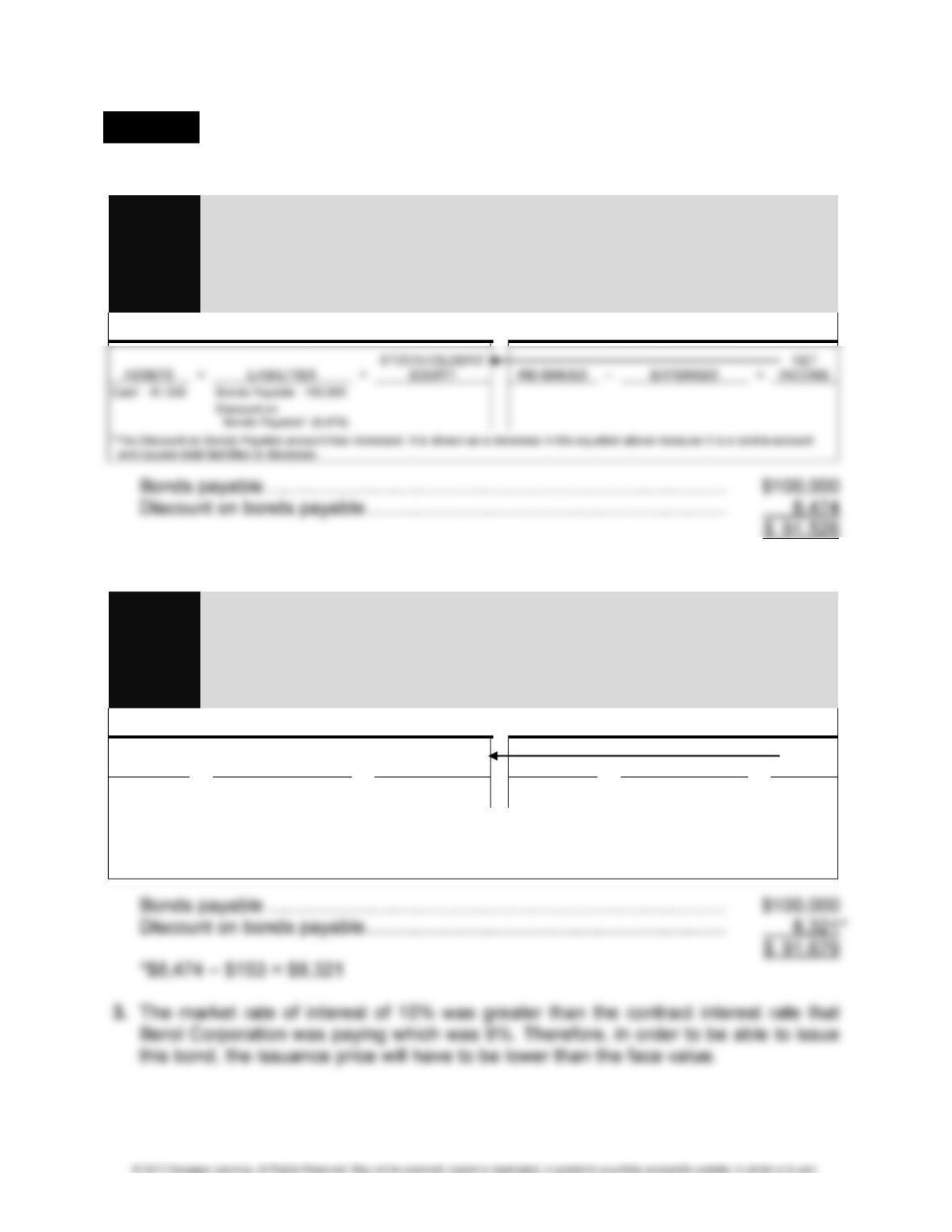

LO 4,5 EXERCISE 10-16 IMPACT OF A DISCOUNT

1.

Journal 2016

Entry Jan. 1 Cash …………………………………………………………. 91,526

Analysis Discount on Bonds Payable………………………….. 8,474

Bonds Payable ………………………………………. 100,000

To record issuance of bond.

Balance Sheet Income Statement

2.

Journal 2016

Entry Dec. 31 Interest Expense …………………………………………. 9,153

Analysis Cash ($100,000 × 9%) ……………………………. 9,000

Discount on Bonds Payable …………………….. 153

To record payment of interest and amortization of discount.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash* (9,000)

Discount on

Bonds Payable*** 153

(9,153)

Interest

Expense** 9,153

(9,153)

*$100,000 × 9% × 1 year = $9,000

**$91,526 × 10% × 1 year = $9,153

***TheDiscountonBondsPayableaccounthasdecreased.Itisshownasanincreaseintheequationabovebecauseitisacontraaccountand

causestotalliabilitiestoincrease.

10-12 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

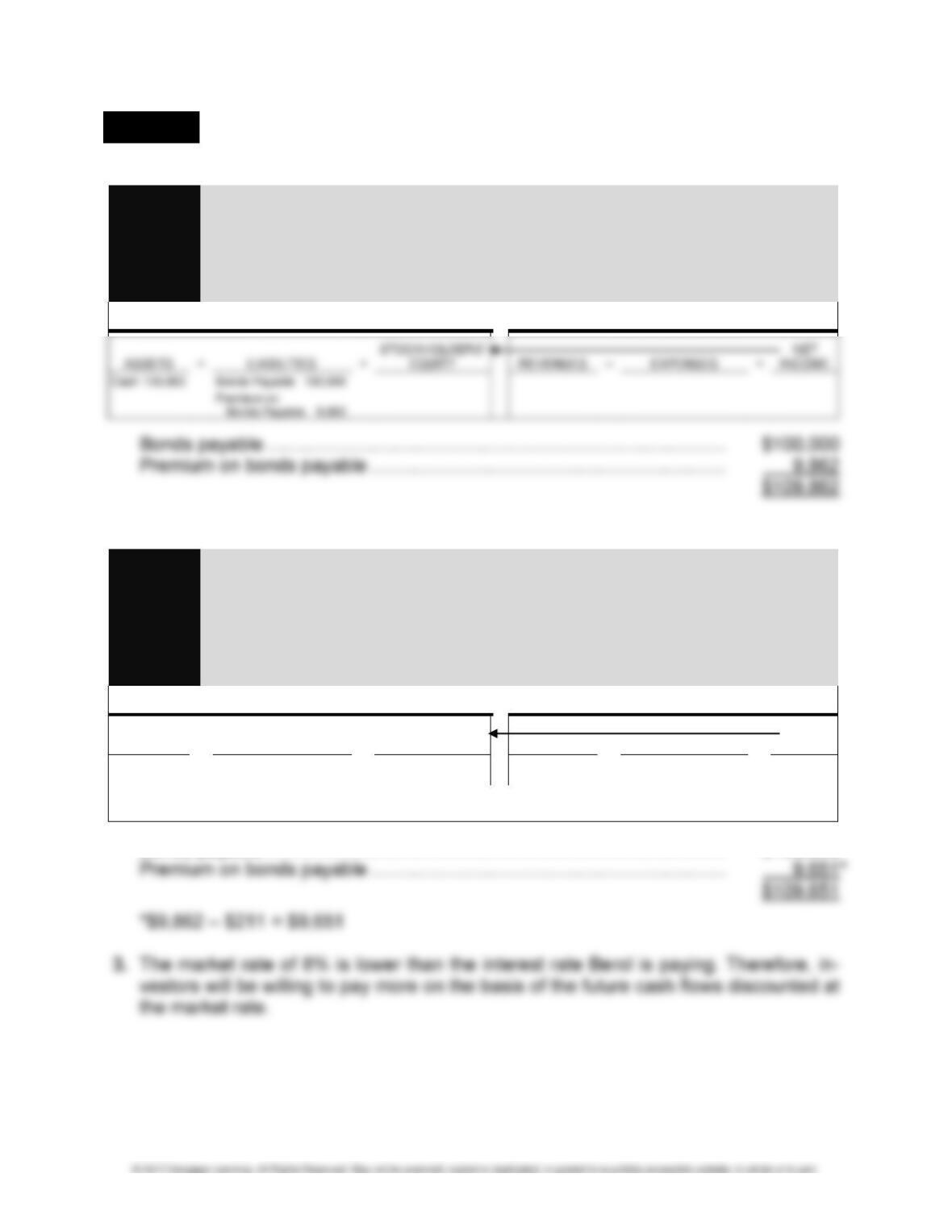

LO 4,5 EXERCISE 10-17 IMPACT OF A PREMIUM

1.

Journal 2016

Entry Jan. 1 Cash …………………………………………………………. 109,862

Analysis Premium on Bonds Payable ……………………. 9,862

Bonds Payable ………………………………………. 100,000

To record the issuance of bonds.

Balance Sheet Income Statement

2.

Journal 2016

Entry Dec. 31 Interest Expense …………………………………………. 8,789

Analysis Premium on Bonds Payable …………………………. 211

Cash ($100,000 × 9%) ……………………………. 9,000

To record interest and amortize premium

on bond.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash (9,000)*

Premium on

Bonds Payable (211) (8,789)

Interest

Expense 8,789** (8,789)

*$100,000 × 9% × 1 year = $9,000

**$109,862 × 8% × 1 year = $8,789

Bonds payable ……………………………………………………………………………. $100,000

CHAPTER 10 • LONG-TERM LIABILITIES 10-13

PROBLEMS

LO 3 PROBLEM 10-1 FACTORS THAT AFFECT THE BOND ISSUE PRICE

1. a. The bonds would be issued at par, since the face or coupon rate is equal to the

market rate of interest.

2. a. $100,000 × 0.55368 (Table 9-2, n = 20, i = 3%) = $ 55,368

$ 3,000* × 14.87747 (Table 9-4, n = 20, i = 3%) = 44,632

Total present value = $100,000

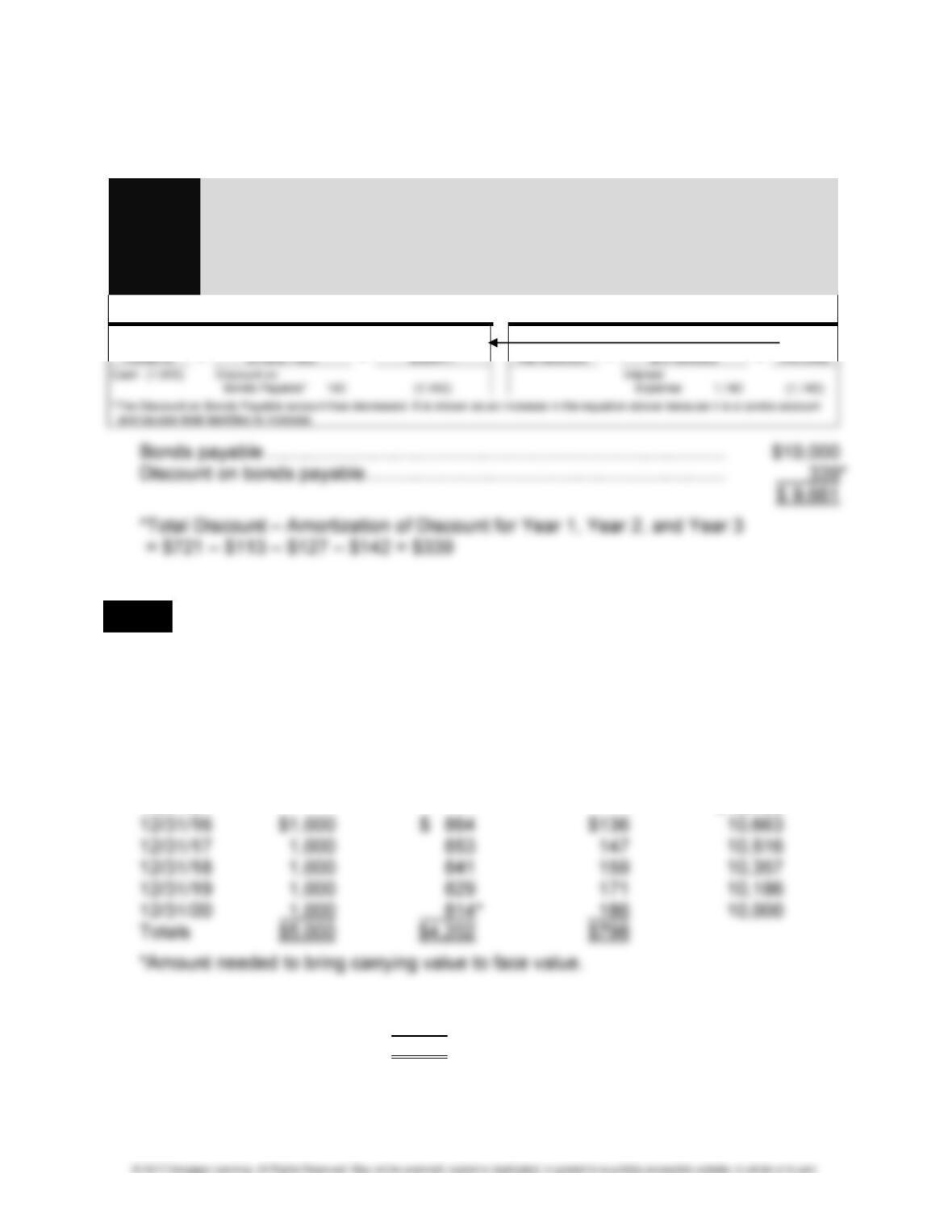

LO 5 PROBLEM 10-2 AMORTIZATION OF DISCOUNT

1. Discount Amortization

Effective Interest Method of Amortization

Col. 1 Col. 2 Col. 3 Col. 4

Cash Interest Discount

Interest Expense Amortized Carrying

Date 10% 12% Col. 2 – Col. 1 Value

1/01/16 $ 9,279

2. Interest expense $5,721

Cash interest payment 5,000

Discount amortized $ 721

10-14 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 10-2 (Concluded)

3.

Journal 2018

Entry Dec. 31 Interest Expense …………………………………………. 1,142

Analysis Discount on Bonds Payable …………………….. 142

Cash ……………………………………………………. 1,000

To record interest and amortize discount.

Balance Sheet Income Statement

STOCKHOLDERS’

NET

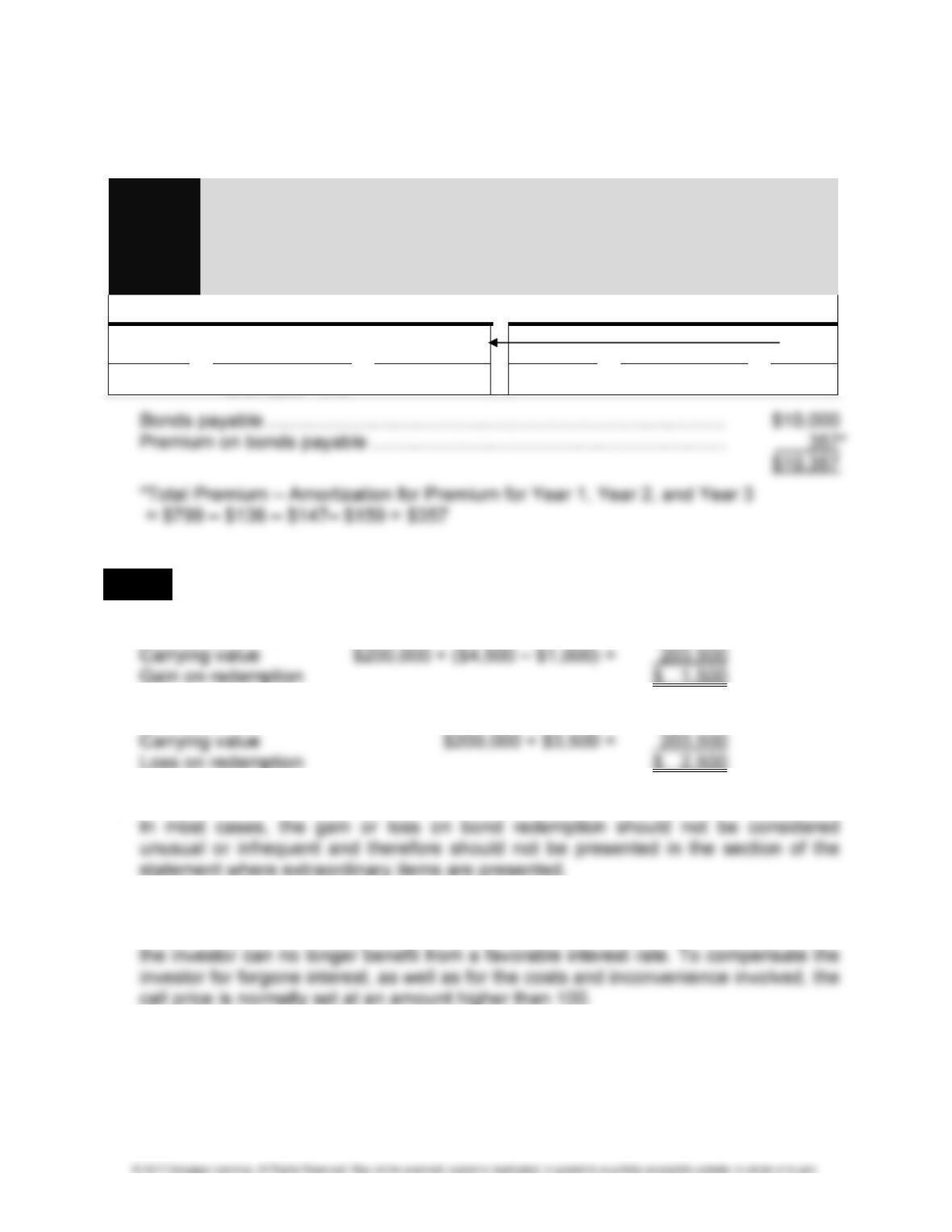

LO 5 PROBLEM 10-3 AMORTIZATION OF PREMIUM

1. Premium Amortization

Effective Interest Method of Amortization

Col. 1 Col. 2 Col. 3 Col. 4

Cash Interest Premium

Interest Expense Amortized Carrying

Date 10% 8% Col. 2 – Col. 1 Value

1/01/16 $10,799

2. Interest expense $4,202

Cash interest payment 5,000

Premium amortized $ 798 (rounded to $798 in amortization table)

CHAPTER 10 • LONG-TERM LIABILITIES 10-15

PROBLEM 10-3 (Concluded)

3.

Journal 2018

Entry Dec. 31 Interest Expense …………………………………………. 841

Analysis Premium on Bonds Payable …………………………. 159

Cash ……………………………………………………. 1,000

To record interest and amortize premium.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash (1,000)

Premium on

Bonds Payable (159)

(841)

Interest Expense 841

(841)

LO 6 PROBLEM 10-4 REDEMPTION OF BONDS

1. Redemption price $200,000 × 1.01 = $202,000

2. Redemption price $200,000 × 1.03 = $206,000

3. The gain or loss on bond redemption should be presented on the income statement.

4. Bonds are redeemed early only if it is advantageous to the issuing firm. However,

early redemption is usually not favorable to the investor because it usually means

10-16 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 7 PROBLEM 10-5 FINANCIAL STATEMENT IMPACT OF A LEASE

1. Col. 1 Col. 2 Col. 3 Col. 4

Interest Reduction of

Lease Expense Obligation Lease

Date Payment 8% Col. 1 – Col. 2 Obligation

1/01/16 $112,994

12/31/16 $28,300 $9,040 $19,260 93,734

2.

Journal 2016

Entry Jan. 1 Leased Truck ……………………………………………… 112,994

3.

Journal 2017

Entry Dec. 31 Lease Liability …………………………………………….. 20,801

Analysis Interest Expense …………………………………………. 7,499

Cash ……………………………………………………. 28,300

To record payment of lease liability

and interest.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash (28,300) Lease Liability (20,801) (7,499) Interest Expense 7,499 (7,499)

CHAPTER 10 • LONG-TERM LIABILITIES 10-17

PROBLEM 10-5 (Concluded)

Journal Dec. 31 Depreciation Expense—Leased Truck …………… 22,599

Entry Accumulated Depreciation—

Analysis Leased Truck ……………………………………… 22,599

4. Long-term assets:

Leased truck ………………………………………………………………………….. $113,000

Accumulated depreciation ……………………………………………………….. 45,198*

$ 67,802

*$22,599 × 2 years = $45,198

Current liabilities:

Lease liability …………………………………………………………………………. $ 22,465

Long-term liabilities:

Lease liability …………………………………………………………………………. $ 50,473

10-18 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 10 PROBLEM 10-6 DEFERRED TAX (Appendix)

1.

Journal 2016

Entry Dec. 31 Income Tax Expense …………………………………… 200

2. The Deferred Tax account exists to reconcile the difference between the accounting

done for tax purposes and that done for reporting to stockholders, also referred to as

book purposes. The balance of the Deferred Tax account represents all temporary

differences between book and tax accounting reflected at the corporate tax rate. The