CHAPTER 1

ENVIRONMENT AND THEORETICAL STRUCTURE OF FINANCIAL ACCOUNTING

Overview

The primary function of financial accounting is to provide useful financial information to users

external to the business enterprise. The focus of financial accounting is on the information needs of

investors and creditors. These users make critical resource allocation decisions that affect the

Learning Objectives

LO1–1 Describe the function and primary focus of financial accounting.

LO1–2 Explain the difference between cash and accrual accounting.

LO1–3 Define generally accepted accounting principles (GAAP) and discuss the historical

development of accounting standards, including convergence between U.S. and international

standards.

Lecture Outline

Part A: Financial Accounting Environment

I. The Function and Primary Purpose of Financial Accounting

A. There are a number of financial information supplier groups as well as several external

user groups. (T1-1)

1-2 Intermediate Accounting, 8/e

2. Income statement or statement of operations

3. Statement of cash flows

II. The Economic Environment and Financial Reporting

A. The capital markets provide a mechanism to help our economy allocate resources

efficiently.

B. Corporations, the dominant form of business organization in the United States in terms of

the ownership of productive resources, acquire capital from investors in exchange for

ownership interest and by borrowing from creditors.

C. The investment-credit decision—A cash flow perspective

1. A company will be able to provide a return to investors and creditors only if it can

III. The Development of Financial Accounting and Reporting Standards

A. Historical perspective and U.S. standards (T1-4)

1. Generally accepted accounting principles (GAAP) are a set of guidelines companies

follow in measuring and reporting financial information.

2. The Securities and Exchange Commission (SEC) has the authority to set accounting

(T1-5)

B. International standard setting

1. The International Accounting Standards Committee (IASC) was formed in 1973 to

develop global accounting standards. The IASC reorganized itself and created a new

C. Convergence between FASB and IASB standards

1. In 2002 the FASB and IASB signed the Norwalk Agreement, pledging to remove

existing differences between standards. Since then, both boards have been working

towards convergence.

2. In November 2008, the SEC proposed a Roadmap for the potential use of financial

3. In July 2012, the SEC staff issues its Final Staff Report in which it concludes that it is

not feasible for the U.S. to simply adopt IFRS, given (1) a need for the U.S. to have

strong influence on the standard-setting process and ensure that standards meet U.S.

4. As of the date this text was written, the SEC still had not made an announcement about

whether it would adopt or incorporate IFRS into U.S. GAAP.

D. The establishment of accounting standards—A political process

1. A standard setter must consider potential economic consequences of accounting

standards.

IV. Encouraging high-quality financial reporting

A. Auditors offer credibility to financial statements by verifying that they are presented fairly

in conformity with GAAP.

1-4 Intermediate Accounting, 8/e

B. The Public Company Accounting Reform and Investor Protection Act of 2002, commonly

referred to as the Sarbanes-Oxley Act, provides for the regulation of auditors and the types

of services they furnish to clients, increases accountability if corporate executives,

IV. Ethics in Accounting

A. Recent accounting scandals have rekindled the debate over principles-based, or more

recently termed, objectives-oriented, versus rules-based accounting standards. A

principles-based approach to standard setting stresses professional judgment, as opposed to

Part B: The Conceptual Framework

I. Purpose of the Conceptual Framework

A. The conceptual framework does not prescribe GAAP.

B. It provides an underlying foundation for accounting standards.

II. Objective of Financial Reporting (T1-10)

A. To provide financial information that is useful to capital providers.

III. Fundamental Qualitative Characteristics of Accounting Information (T1-11)

A. Overriding objective is decision usefulness.

B. Primary qualities of useful information are relevance and faithful representation.

C. Components of relevance are:

IV. Elements of Financial Statements (T1-12)

A. Balance sheet elements:

1. Assets

5. Distributions to owners

B. Income statement elements:

1. Revenues

V. Underlying Assumptions (T1-13)

A. Economic entity assumption

VI. Recognition, Measurement and Disclosure Concepts

A. Recognition

1. An item should be recognized in the basic financial statements when it meets certain

criteria. (T1-14)

2. Revenue recognition recently changed due to issuance of ASU 2014-09. It requires

that revenue be recognized when the seller transfers goods and services to customers,

3. Expense recognition typically occurs in the period in which expenses are incurred to

produce revenue.

B. Measurement (T1-15)

1. GAAP uses a “mixed attribute” model, in which different attributes are used to

measure different financial statement elements.

2. The five measurement attributes commonly employed in GAAP are:

a. Historical cost

1-6 Intermediate Accounting, 8/e

C. Disclosure (T1-17)

1. Financial reports should include any information that could affect users’ decisions.

2. Techniques for providing full disclosure include parenthetical comments, disclosure

notes and supplemental schedules and tables.

VII. Evolution of Accounting Principles

A. Two competing approaches for the recognition of revenues and expense are (1) the

revenue/expense approach and (2) the asset/liability approach.

PowerPoint Slides

A PowerPoint presentation of the chapter is available in the Connect library.

Teaching Transparency Masters

The following can be reproduced on transparency film as they appear here, or

FINANCIAL INFORMATION SUPPLIER GROUPS AND EXTERNAL USER GROUPS

PROVIDERS OF

FINANCIAL

EXTERNAL USER

INFORMATION

GROUPS

Profit-oriented

Investors

companies

Creditors

(banks, bondholders, other

lenders)

Employees

Customers

Illustration 1-1

T1-1

1-8 Intermediate Accounting, 8/e

FINANCIAL STATEMENTS

➢ The primary means of conveying financial information to

➢ The financial statements most frequently provided are:

1. The balance sheet or statement of financial position

5. Either

a) a statement of other comprehensive income

immediately following the income statement, or

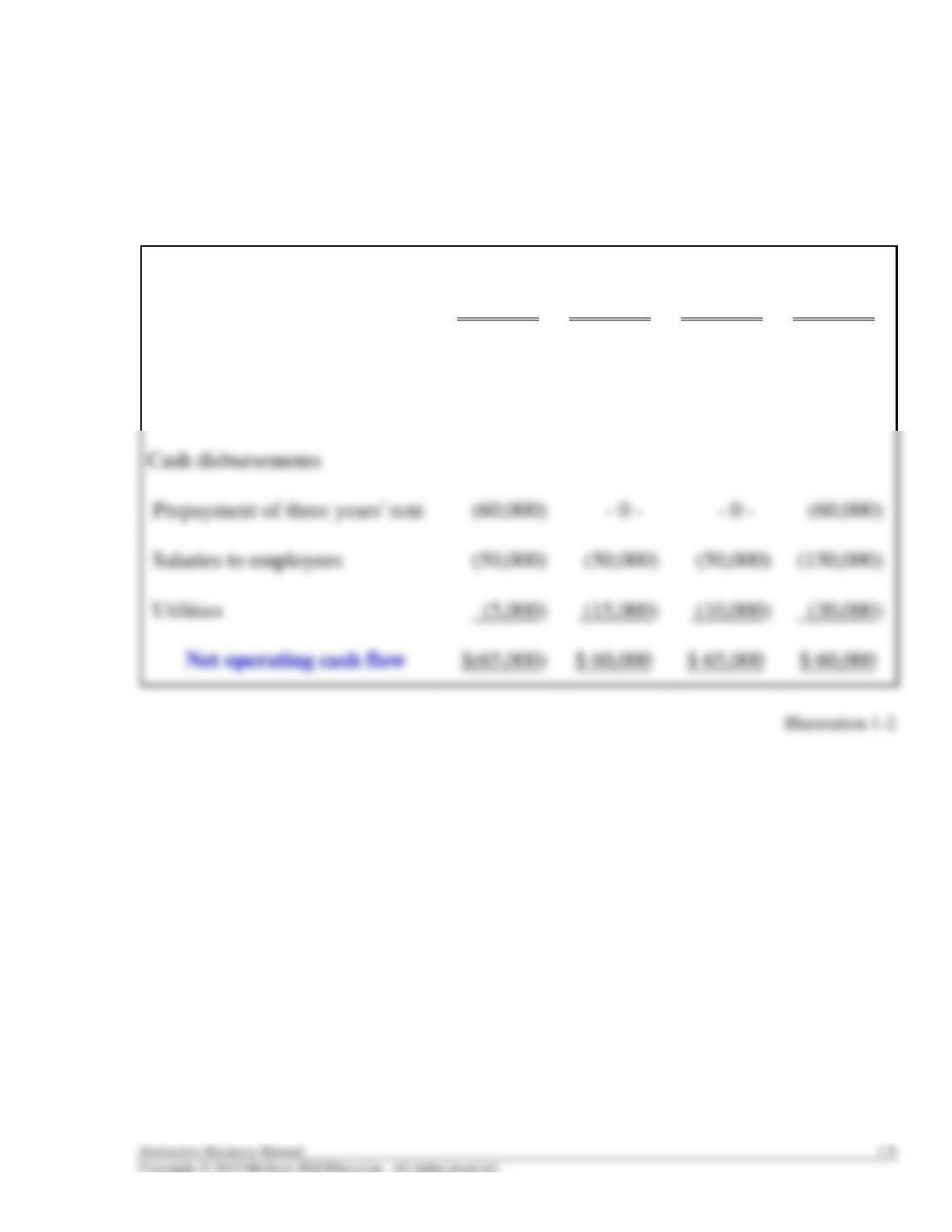

CASH VERSUS ACCRUAL ACCOUNTING

Carter Company — 3 Years of Operating Transactions

Year 1

Year 2

Year 3

Total

Sales (on credit)

$100,000

$100,000

$100,000

$300,000

Net Operating Cash Flows:

Cash receipts from customers

$ 50,000

$125,000

$125,000

$300,000

Cash disbursements

Prepayment of three years’ rent

Salaries to employees

Utilities

$ 60,000

$ 65,000

$ 60,000

T1-3

1-10 Intermediate Accounting, 8/e

➢ Measuring the same activities by the accrual accounting

model provides a more accurate prediction of future operating

cash flows.

Carter Company — Income Statements

Year 1

Year 2

Year 3

Total

Revenues

$100,000

$100,000

$100,000

$300,000

Expenses:

Rent

Salaries

Utilities

10,000

Net Income

$ 20,000

$ 20,000

$ 20,000

$ 60,000

Illustration 1-3

T1-3 (Continued)

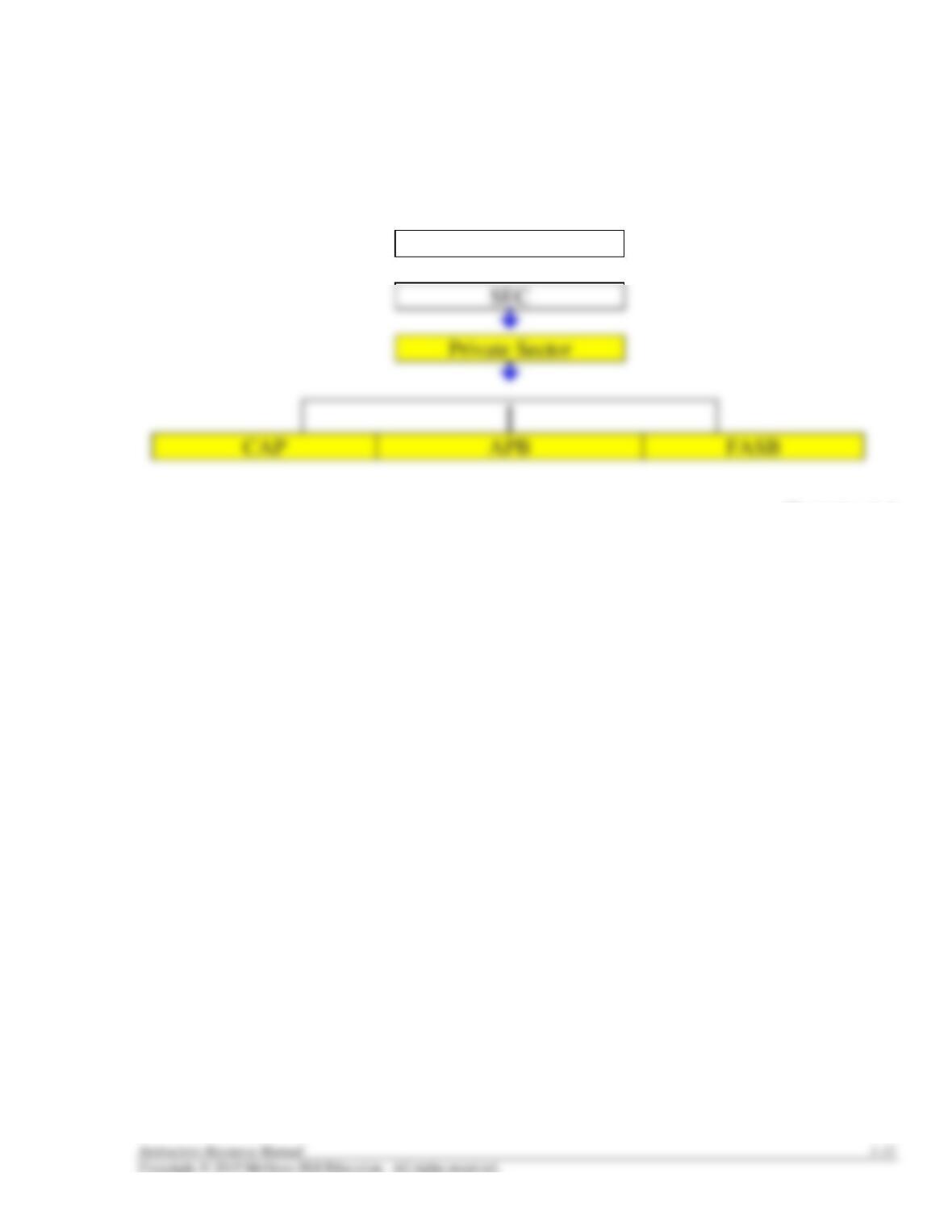

ACCOUNTING STANDARD SETTING

HIERARCHY OF STANDARD-SETTING AUTHORITY

Congress

Illustration 1-4

T1-4

1-12 Intermediate Accounting, 8/e

FASB Accounting Standards Codification Topics

Topic

Numbered

General Principles

100-199

Presentation

200-299

Assets

300-399

Liabilities

400-499

Revenues

600-699

Expenses

700-799

800-899

Illustration 1-5

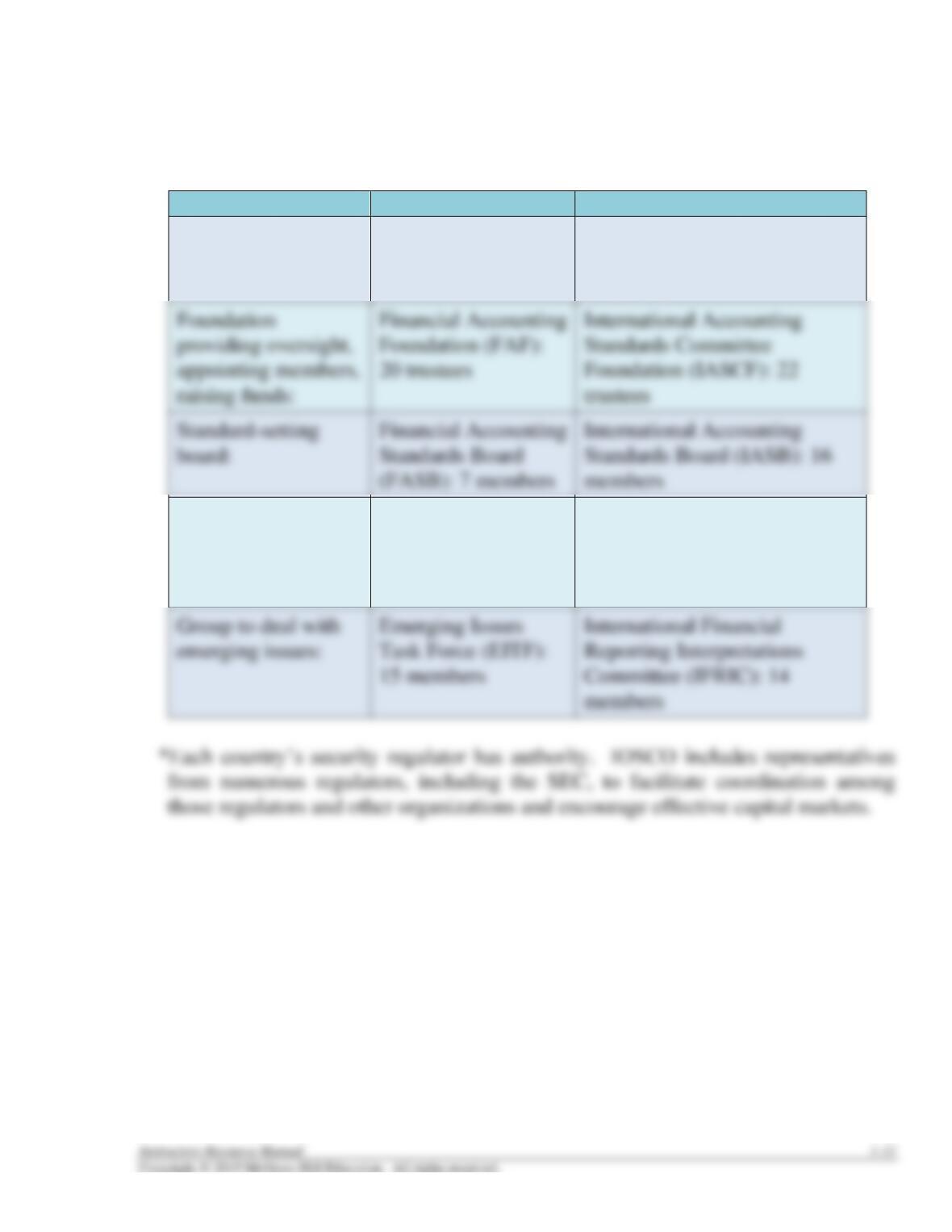

THE FASB’s STANDARD-SETTING PROCESS

U.S. GAAP

IFRS

Regulatory oversight

provided by:

Securities Exchange

Commission (SEC)

International Organization of

Securities Commissions

(IOSCO)*

Standard-setting

Financial Accounting

Standards Board

International Accounting

Standards Board (IASB): 16

Advisory council

providing input on

agenda and projects:

Financial Accounting

Standards Advisory

Council (FASAC):

30-40 members

Standards Advisory Council

(SAC): 30-40 members

emerging issues:

Task Force (EITF):

15 members

Reporting Interpretations

Committee (IFRIC): 14

members

Illustration 1-6

T1-6

1-14 Intermediate Accounting, 8/e

THE FASB’s STANDARD-SETTING PROCESS

STEP

EXPLANATION

1.

The Board deliberates at one or more public meetings the various

The Board identifies financial reporting issues based on

requests/recommendations from stakeholders or through other

means.

4.

The Board issues an Exposure Draft. (In some projects, a

Discussion Paper may be issued to obtain input at an early stage

that is used to develop an Exposure Draft.)

5.

The Board holds a public roundtable meeting on the Exposure

Draft, if necessary.

Illustration 1-7

THE SARBANES-OXLEY ACT

Key Provisions of the Act:

• Oversight board. The five-member (two accountants) Public Company Accounting Oversight

Board has the authority to establish standards dealing with auditing, quality control, ethics,

• Non-audit services. The law makes it unlawful for the auditors of public companies to perform

a variety of non-audit services for audit clients. Prohibited services include bookkeeping,

internal audit outsourcing, appraisal or valuation services, and various other consulting services.

Other non-audit services, including tax services, require pre-approval by the audit committee of

the company being audited.

preceding year.

• Hiring of auditor. Audit firms are hired by the audit committee of the board of directors of the

company, not by company management.

• Internal Control. Section 404 of the Act requires that company management document and

Illustration 1-5

T1-8

1-16 Intermediate Accounting, 8/e

ANALYTICAL MODEL FOR ETHICAL DECISIONS

Step 1. Determine the facts of the situation. This involves

determining the who, what, where, when, and how.

Step 4. Specify the alternative courses of action.

Step 5. Evaluate the courses of action specified in step 4 in terms

of their consistency with the values identified in step 3.

This step may or may not lead to a suggested course of

action.

T1-9

THE CONCEPTUAL FRAMEWORK

Objective

To provide financial information that is useful to capital

providers.

Phase A

Qualitative

Characteristics

Recognition and

Measurement Concepts

(including consistency)

Primary

Relevance

Predictive value

Faithful Representation

Completeness

Enhancing

Comparability

Elements

Equity

Investments by owners

Distributions to owners

Losses

Comprehensive income

Assumptions

Periodicity

Monetary unit

Mixed attribute

measurement

Financial Statements

Constraint

• Balance sheet

• Income statement

Illustration 1-9