1-1

CHAPTER 1

Accounting as a Form

of Communication

OVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated

Time in

Learning Outcomes Exercises Minutes Level

Module 1

1. Explain what business is about.

Module 2

4. Define accounting and identify the primary users of accounting 2 5 Easy

information and their needs. 15* 10 Mod

Module 3

6. Identify and explain the primary assumptions made in 12 10 Mod

preparing financial statements. 16* 10 Mod

7. Identify the various groups involved in setting accounting standards 13 10 Mod

and the role of auditors in determining whether the standards are

followed.

1-2 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Problems Estimated

and Time in

Learning Outcomes Alternates Minutes Level

Module 1

1. Explain what business is about.

Module 2

4. Define accounting and identify the primary users of accounting 1 30 Mod

information and their needs. 2 20 Mod

9 20 Mod

Module 3

6. Identify and explain the primary assumptions made in 10* 45 Diff

preparing financial statements.

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-3

Estimated

Time in

Learning Outcomes Cases Minutes Level

Module 1

1. Explain what business is about.

Module 2

4. Define accounting and identify the primary users of accounting 1* 25 Mod

information and their needs. 4 30 Mod

6* 75 Diff

Module 3

6. Identify and explain the primary assumptions made in

preparing financial statements.

1-4 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISES

LO 3 EXERCISE 1-1 TYPES OF BUSINESS ACTIVITIES

F 1. Issued shares of stock to each of the four owners.

I 2. Purchased two limousines.

LO 4 EXERCISE 1-2 USERS OF ACCOUNTING INFORMATION AND THEIR NEEDS

1. Company management

2. Stockholder

3. Labor union

LO 5 EXERCISE 1-3 THE ACCOUNTING EQUATION

A = L + SE

Case 1: $125,000 = $75,000 + SE

SE = $50,000

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-5

LO 5 EXERCISE 1-4 THE ACCOUNTING EQUATION

1. A = L + SE

$500,000 = $250,000 + SE

SE = $250,000

2. A = L + SE

($500,000 + $100,000) = ($250,000 + $77,000) + SE

SE = $273,000*

*SE = ($500,000 + $100,000) – ($250,000 + $77,000) = $273,000

LO 5 EXERCISE 1-5 THE ACCOUNTING EQUATION

1. A = L + SE

Beginning of year $100,000 = $80,000 + $20,000

Net income + 25,000

Dividends – 0

Stockholders’ equity at end of year $45,000

1-6 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 EXERCISE 1-6 CHANGES IN OWNERS’ EQUITY

1. First, compute the amount of stockholders’ equity at the end of each year. Then,

compute the change.

A = L + SE

2014: $25,000 = $12,000 + SE

SE = $13,000

2. 2015:

($1,000) = Income – $0 in dividends

Net loss = ($1,000)

3. 2016:

$35,000 = Income – $10,000 in dividends

Net income = $45,000*

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-7

LO 5 EXERCISE 1-7 THE ACCOUNTING EQUATION

(In thousands of dollars)

A = L + CS + (Beg. RE + Income – Div.)

Case 1:

40 = L + 10 + (15 + 8 – 2)

Liabilities = 9

Case 2:

A = 15 + 5 + (8 + 7 – 1)

Assets = 34

LO 5 EXERCISE 1-8 CLASSIFICATION OF FINANCIAL STATEMENT ITEMS

Appears on the Classified as

1. IS E

2. BS A

3. BS L

1-8 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 EXERCISE 1-9 CLASSIFICATION OF FINANCIAL STATEMENT ITEMS

Item Appears on the Classified as

1. Trade and other receivables, net BS A

2. Class A common stock BS SE

3. Inventories BS L

LO 5 EXERCISE 1-10 NET INCOME (OR LOSS) AND RETAINED EARNINGS

1. Revenue – Expenses = Net Income

$25,000 – ($6,500 + $12,000) = $6,500

4. Total Liabilities:

Accounts payable …………….. $5,000

5. Stockholders’ Equity:

Capital Stock + Retained Earnings = Stockholders’ Equity

$8,000 + $12,000 = $20,000

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-9

LO 5 EXERCISE 1-11 STATEMENT OF RETAINED EARNINGS

ACE CORPORATION

STATEMENT OF RETAINED EARNINGS

FOR THE MONTH ENDED FEBRUARY 29, 2016

Retained earnings, beginning of month ……………………………………… $229,800*

Net income ……………………………………………………………………………. 14,000**

LO 6 EXERCISE 1-12 ACCOUNTING PRINCIPLES AND ASSUMPTIONS

1. Going concern (also economic entity)

2. Cost principle

LO 7 EXERCISE 1-13 ORGANIZATIONS AND ACCOUNTING

1. Securities and Exchange Commission

2. Financial Accounting Standards Board

1-10 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 EXERCISE 1-14 CLASSIFICATION OF ITEMS ON THE STATEMENT OF CASH FLOWS

Item Section

1. Cash paid for land I

2. Cash received from issuance of note F

MULTI-CONCEPT EXERCISES

LO 4,5 EXERCISE 1-15 USERS OF ACCOUNTING INFORMATION AND THE FINANCIAL

STATEMENTS

USER FINANCIAL STATEMENT

Stockholder IS

Banker BS

Supplier BS

LO 5,6 EXERCISE 1-16 CHIPOTLE’S LAND

Land would be included in “Leasehold improvements, property and equipment, net” on

Chipotle’s balance sheet. The amount represents how much the company paid for the

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-11

PROBLEMS

LO 4 PROBLEM 1-1 YOU WON THE LOTTERY

Obviously, there is no single, correct answer to this problem. Students should start by

considering their personal circumstances and preference for risk. They should also con-

sider their liquidity requirements. From this point, it is appropriate to consider sources of

information.

Following are guidelines to be used:

Options

Issues Stock Bonds Bank deposit

Risk High Medium Low

Information Market price Market price Interest rate

needed Dividends Interest rate

Maturity date

This problem provides the instructor with an opportunity to introduce the concept of the

time value of money. Certainly, it would be preferable to receive $1 million today, rather

than $200,000 over each of the next five years. If a lump sum is received immediately, it

could be put into one of the investments chosen, as opposed to spreading the invest-

ment over a five-year period.

1-12 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 4 PROBLEM 1-2 USERS OF ACCOUNTING INFORMATION AND THEIR NEEDS

Information Management Stockholders Banker

1. a. b. a.

2. a. c. a.

LO 5 PROBLEM 1-3 BALANCE SHEET

FREESCIA CORPORATION

BALANCE SHEET

END OF THE YEAR

Assets Liabilities and Stockholders’ Equity

Cash ……………………………… $ 4,220 Accounts payable ………………… $ 12,550

Accounts receivable ………… 23,920 Notes payable ……………………… 50,000

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-13

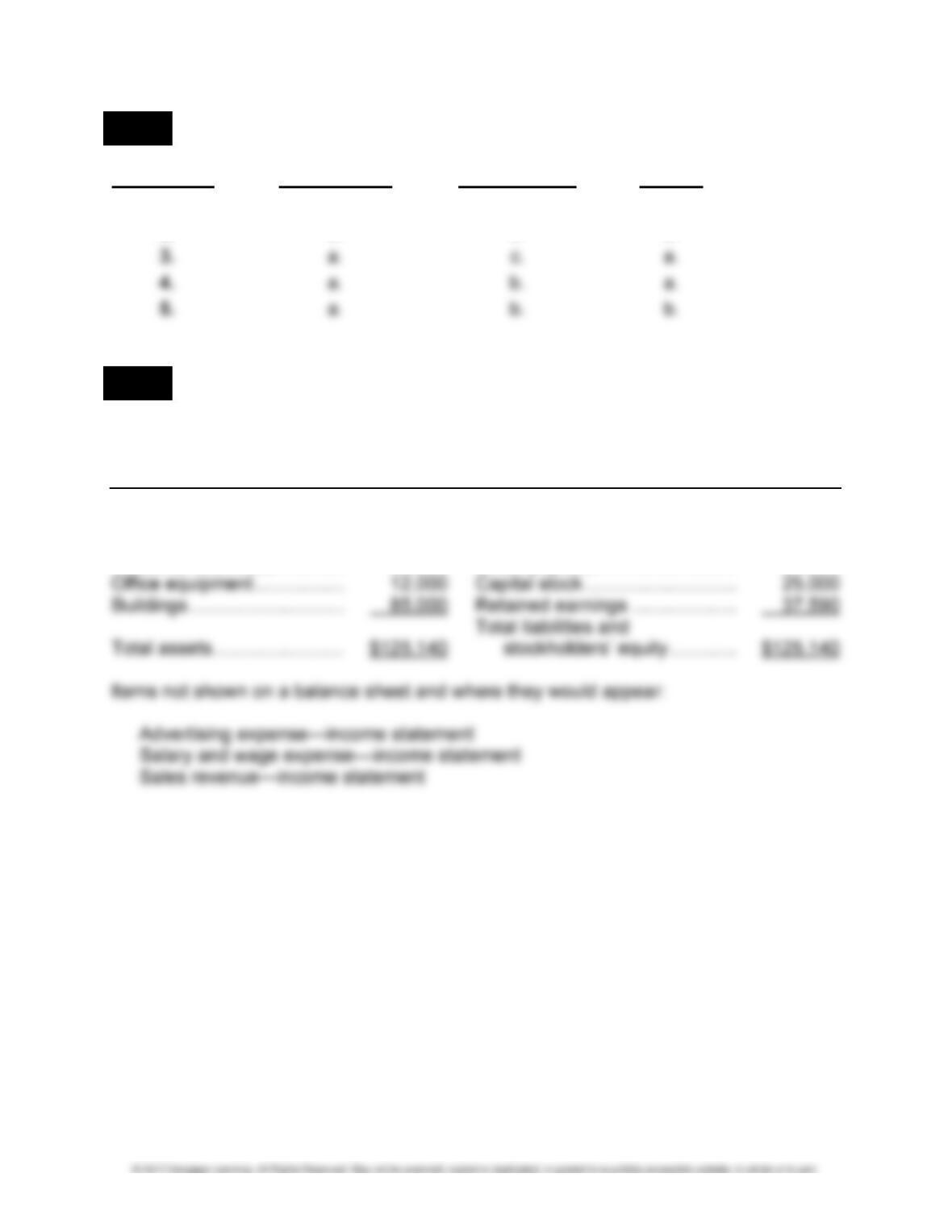

LO 5 PROBLEM 1-4 CORRECTED BALANCE SHEET

1. AVON CONSULTING INC.

BALANCE SHEET

END OF THE YEAR

Assets Liabilities and Stockholders’ Equity

Cash ………………………… $21,000 Accounts payable ………………… $13,000

Accounts receivable ……. 16,000 Capital stock ……………………….. 20,000

2. Memorandum to the company president:

TO: Company president

FROM: Student’s name

lows:

1. The balance sheet is always as of a certain date, in this case, the end of the cur-

rent year, rather than a period of time, such as a year.

2. Accounts payable should be classified as a liability.

3. Cash dividends do not belong on the balance sheet; this amount should appear

instead on the statement of retained earnings for the year.

4. Accounts receivable should be classified as an asset.

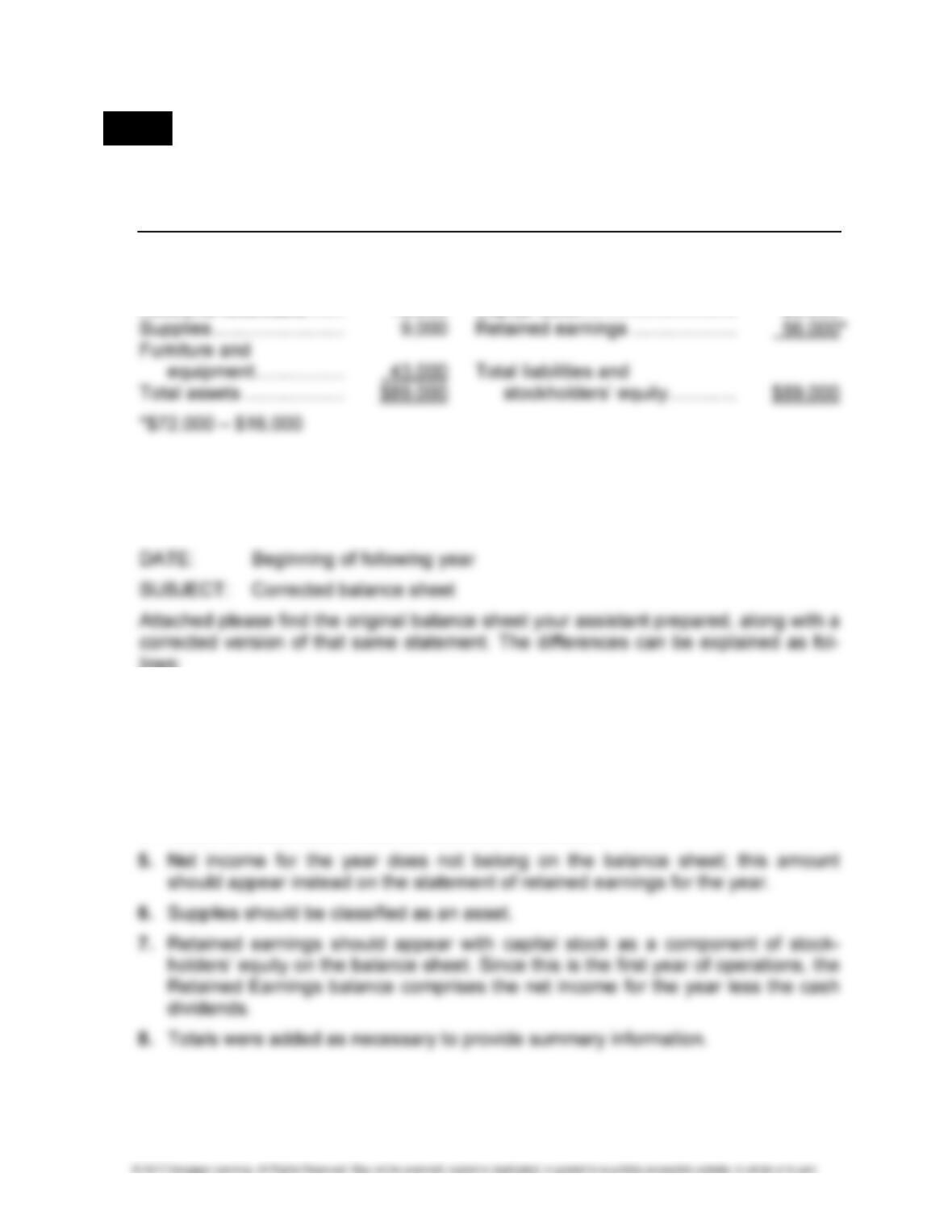

1-14 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

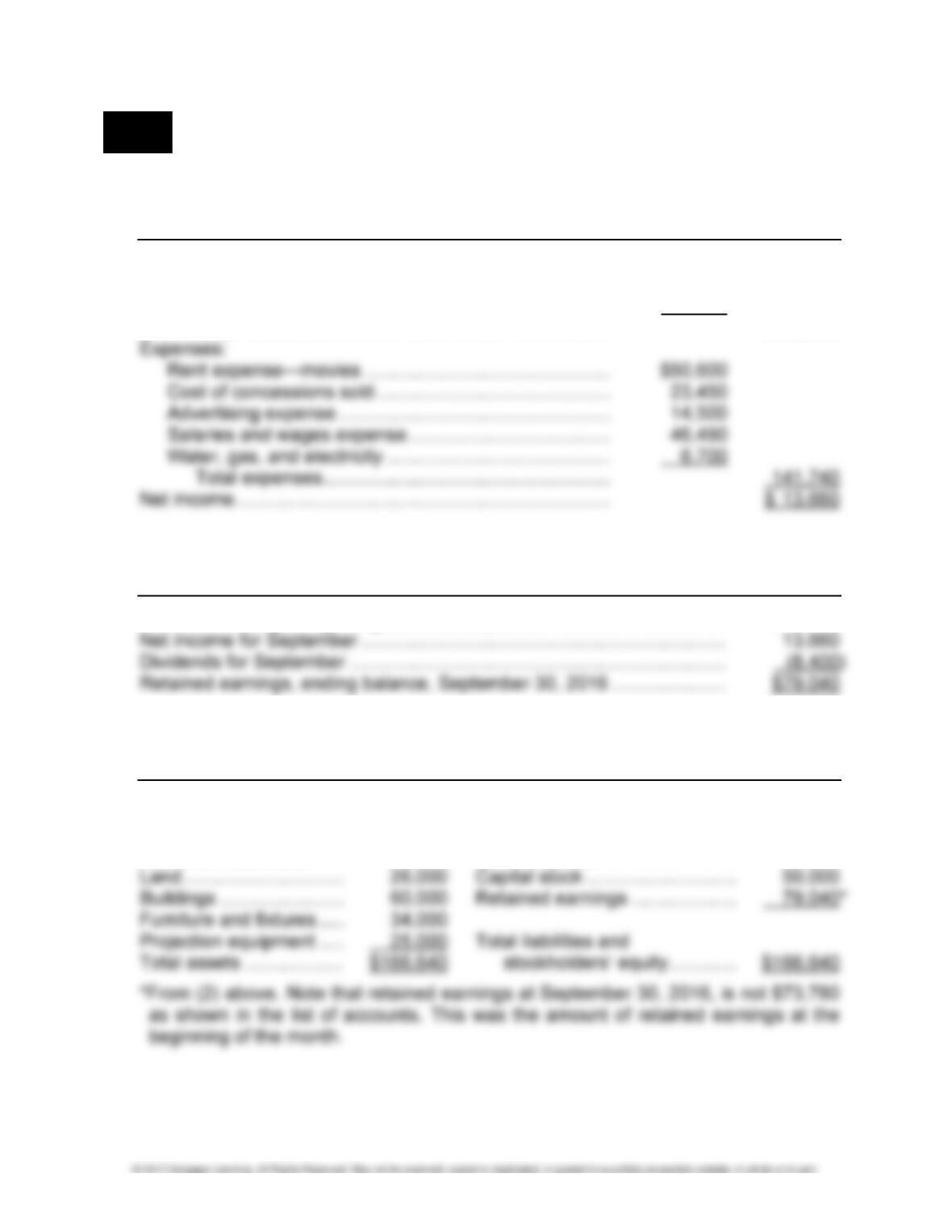

LO 5 PROBLEM 1-5 INCOME STATEMENT, STATEMENT OF RETAINED EARNINGS,

AND BALANCE SHEET

1. MAPLE PARK THEATRES CORP.

INCOME STATEMENT

FOR THE MONTH ENDED SEPTEMBER 30, 2016

Revenues:

Ticket sales………………………………………………………… $95,100

Concessions revenue ………………………………………….. 60,300

Total revenues ………………………………………………. $155,400

2. MAPLE PARK THEATRES CORP.

STATEMENT OF RETAINED EARNINGS

FOR THE MONTH ENDED SEPTEMBER 30, 2016

Retained earnings, beginning balance, September 1, 2016 ………………. $73,780

3. MAPLE PARK THEATRES CORP.

BALANCE SHEET

SEPTEMBER 30, 2016

Assets Liabilities and Stockholders’ Equity

Cash ………………………… $ 15,230 Accounts payable ………………… $ 17,600

Accounts receivable ……. 6,410 Notes payable ……………………… 20,000

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-15

PROBLEM 1-5 (Concluded)

4. On the basis of these statements alone, Maple Park would appear to be a good

candidate for an investment. It is operating at a profit and is paying dividends. Before

one makes an investment in Maple Park stock, it would be useful to see the state-

LO 5 PROBLEM 1-6 INCOME STATEMENT AND BALANCE SHEET

1. GREEN BAY CORPORATION

INCOME STATEMENT

FOR THE MONTH ENDED JULY 31, 2016

Revenues:

Fishing revenue ………………………………………………….. $21,300

Passenger service revenue ………………………………….. 12,560

2. GREEN BAY CORPORATION

BALANCE SHEET

JULY 31, 2016

Assets Liabilities and Stockholders’ Equity

Cash ………………………… $ 7,730 Notes payable ……………………… $ 60,000

3. To fully assess Green Bay’s long-term viability, you would need the following infor-

mation about the $60,000 note payable:

• When is it due?

• What is the interest rate?

1-16 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

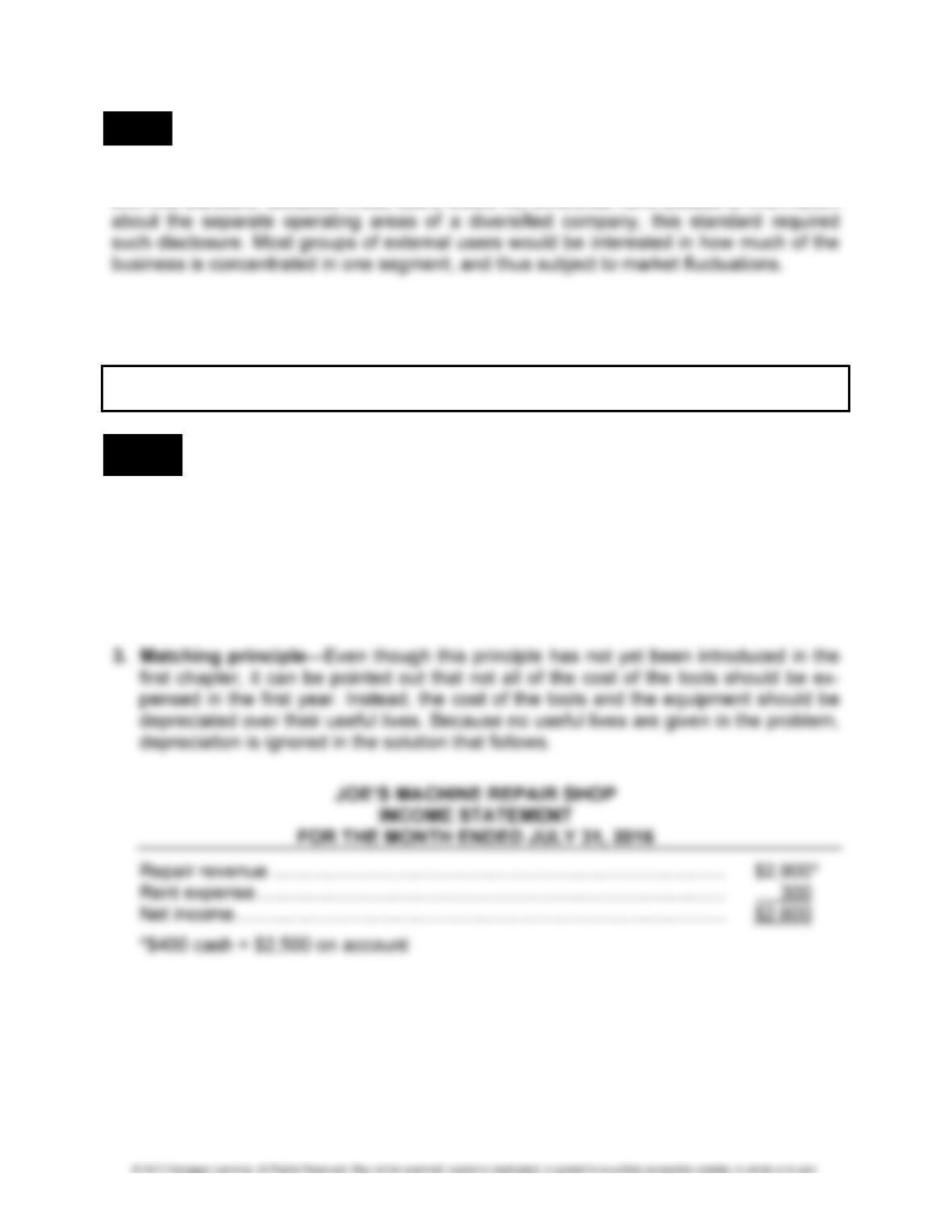

LO 5 PROBLEM 1-7 CORRECTED FINANCIAL STATEMENTS

1. HOMETOWN CLEANERS INC.

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2016

Revenues:

Cleaning revenue—credit sales …………………………….. $26,200

Cleaning revenue—cash sales ……………………………… 32,500

2. HOMETOWN CLEANERS INC.

STATEMENT OF RETAINED EARNINGS

FOR THE YEAR ENDED DECEMBER 31, 2016

Retained earnings, beginning of year …………………………………………….. $42,700*

3. HOMETOWN CLEANERS INC.

BALANCE SHEET

DECEMBER 31, 2016

Assets Liabilities and Stockholders’ Equity

Cash ………………………… $ 7,400 Accounts payable ………………… $ 4,500

Accounts receivable ……. 15,200 Notes payable ……………………… 50,000

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-17

PROBLEM 1-7 (Concluded)

4. Memorandum to the company president:

TO: Company president

FROM: Student’s name

DATE: January 1, 2017

SUBJECT: Corrected income statement

Attached please find the original income statement you prepared, along with a cor-

rected version of that same statement. Fortunately, your disappointment with the

2016 net income is not warranted, as you will see from my revised statement. The

LO 5 PROBLEM 1-8 STATEMENT OF RETAINED EARNINGS FOR THE COCA-COLA

COMPANY

1. THE COCA-COLA COMPANY

STATEMENT OF RETAINED EARNINGS

FOR THE YEAR ENDED DECEMBER 31, 2013

(amounts in millions)

Retained earnings, beginning of year …………………………………………….. $58,045

Net income attributable to shareowners of the

1-18 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 4 PROBLEM 1-9 INFORMATION NEEDS AND SETTING ACCOUNTING STANDARDS

The Financial Accounting Standards Board would have been targeting external users

with this standard. Because these users would not otherwise have access to information

MULTI-CONCEPT PROBLEM

LO 5,6 PROBLEM 1-10 PRIMARY ASSUMPTIONS MADE IN PREPARING FINANCIAL

STATEMENTS

Assumptions violated:

1. Economic entity—Should have separated his personal affairs from those of the

business.

2. Cost principle—Should have recorded the new equipment at the amount paid to

acquire it, not its list price.