CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-19

PROBLEM 1-10 (Concluded)

JOE’S MACHINE REPAIR SHOP

BALANCE SHEET

JULY 31, 2016

Assets Liabilities and Owner’s Equity

Cash ………………………… $ 400

Rent deposit ………………. 1,000

Accounts receivable ……. 2,500

1-20 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

ALTERNATE PROBLEMS

LO 4 PROBLEM 1-1A WHAT TO DO WITH A MILLION DOLLARS?

Obviously, there is no single, correct answer to this problem. Students should start by

considering their personal circumstances and preference for risk. They should also con-

sider their liquidity requirements. From this point, it is appropriate to consider sources of

Following are guidelines to be used:

Options

Issues Stock Bonds Bank deposit

Risk High Medium Low

Information Market price Market price Interest rate

needed Dividends Interest rate

Maturity date

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-21

LO 4 PROBLEM 1-2A USERS OF ACCOUNTING INFORMATION AND THEIR NEEDS

Information Manager Stockholders Franchisor

1. a. b. a.

2. a. b. a.

LO 5 PROBLEM 1-3A BALANCE SHEET

VICTOR CORPORATION

BALANCE SHEET

END OF THE YEAR

Assets Liabilities and Stockholders’ Equity

Cash ……………………………… $ 21,800 Accounts payable ………………… $ 16,900

Accounts receivable ………… 5,700 Notes payable ……………………… 50,000

Butter and cheese Capital stock ……………………….. 25,000

inventory …………………… 12,100 Retained earnings ……………….. 26,300

Computerized mixers ………. 25,800

Office equipment …………….. 12,000

1-22 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 PROBLEM 1-4A CORRECTED BALANCE SHEET

1. ISLAND ENTERPRISES

BALANCE SHEET

END OF THE YEAR

Assets Liabilities and Stockholders’ Equity

Cash ………………………… $ 14,750 Accounts payable ………………… $ 29,600

Accounts receivable ……. 23,200 Capital stock ……………………….. 100,000

2. Memorandum to the company president:

TO: Company president

FROM: Student’s name

DATE: Beginning of following year

SUBJECT: Corrected balance sheet

Attached please find the original balance sheet your assistant prepared, along with a

corrected version of that same statement. The differences can be explained as

follows:

4. Accounts receivable should be classified as an asset.

5. Net income for the year does not belong on the balance sheet; this amount

should appear instead on the statement of retained earnings for the year.

6. Supplies should be classified as an asset.

7. Retained earnings should appear with capital stock as a component of stock-

holders’ equity on the balance sheet. Since this is the first year of operations, the

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-23

LO 5 PROBLEM 1-5A INCOME STATEMENT, STATEMENT OF RETAINED EARNINGS,

AND BALANCE SHEET

1. STERNS AUDIO BOOK RENTAL CORP.

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2016

Rental revenue ……………………………………………………….. $125,900

Expenses:

2. STERNS AUDIO BOOK RENTAL CORP.

STATEMENT OF RETAINED EARNINGS

FOR THE YEAR ENDED DECEMBER 31, 2016

Retained earnings, beginning of year …………………………. ………………… $ 35,390

3. STERNS AUDIO BOOK RENTAL CORP.

BALANCE SHEET

DECEMBER 31, 2016

Assets Liabilities and Stockholders’ Equity

Cash ………………………… $ 2,490 Accounts payable ………………… $ 4,500

Accounts receivable ……. 300 Notes payable ……………………… 10,000

1-24 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 1-5A (Concluded)

4. On the basis of these statements alone, Sterns would appear to be a good candi-

date for an investment. It is operating at a profit and is paying dividends. It is control-

ling its costs and has a profit margin (net income divided by rental revenue) of nearly

LO 5 PROBLEM 1-6A INCOME STATEMENT AND BALANCE SHEET

1. FORT WORTH CORPORATION

INCOME STATEMENT

FOR THE MONTH ENDED JANUARY 31, 2016

Cleaning revenue …………………………………………………….. $45,900

Expenses:

2. FORT WORTH CORPORATION

BALANCE SHEET

JANUARY 31, 2016

Assets Liabilities and Stockholders’ Equity

Cash ………………………… $ 51,650 Notes payable ……………………… $ 30,000

Accounts receivable ……. 24,750 Capital stock ……………………….. 80,000

3. To fully assess Fort Worth’s long-term viability, you would need the following infor-

mation about the $30,000 note payable:

• When is it due?

• What is the interest rate?

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-25

LO 5 PROBLEM 1-7A CORRECTED FINANCIAL STATEMENTS

1. HEIDI’S BAKERY INC.

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2016

Revenues:

Pastry cash sales ……………………………………………….. $23,700

2. HEIDI’S BAKERY INC.

STATEMENT OF RETAINED EARNINGS

FOR THE YEAR ENDED DECEMBER 31, 2016

Retained earnings, beginning of year …………………………………………….. $39,900

3. HEIDI’S BAKERY INC.

BALANCE SHEET

DECEMBER 31, 2016

Assets Liabilities and Stockholders’ Equity

Cash ………………………… $ 3,700 Accounts payable ………………… $ 6,800

Accounts receivable ……. 15,500 Notes payable ……………………… 40,000

1-26 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 1-7A (Concluded)

4. Memorandum to the company president:

TO: Company president

FROM: Student’s name

1. Accounts receivable of $15,500 does not belong on the income statement; in-

stead, services provided on account of $22,100 should be shown on the income

statement; the difference is $6,600.

2. Dividends are not an expense and thus they do not belong on the income state-

ment: $5,600.

LO 5 PROBLEM 1-8A STATEMENT OF RETAINED EARNINGS FOR BRUNSWICK

CORPORATION

1. BRUNSWICK CORPORATION

STATEMENT OF RETAINED EARNINGS

FOR THE YEAR ENDED DECEMBER 31, 2013

(amounts in millions)

Retained earnings, beginning of year …………………………………… $ 503.2

Net income for the year ………………………………………………………. 769.2

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-27

LO 4 PROBLEM 1-9A INFORMATION NEEDS AND SETTING ACCOUNTING STANDARDS

The Financial Accounting Standards Board would have been targeting external users

with this standard. Because these users would not otherwise have access to information

ALTERNATE MULTI-CONCEPT PROBLEM

LO 5,6 PROBLEM 1-10A PRIMARY ASSUMPTIONS MADE IN PREPARING FINANCIAL

STATEMENTS

Assumptions violated:

1. Economic entity—Should have separated her personal affairs from those of the

business.

3. Matching principle—Even though this principle has not yet been introduced in the

first chapter, it can be pointed out that a portion of the cost of the long-term assets

1-28 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 1-10A (Concluded)

MILLIE’S CERAMIC STUDIO

INCOME STATEMENT

FOR THE MONTH ENDED JULY 31, 2016

Revenues:

Classes ……………………………………………………………… $ 700

Greenware sales ………………………………………………… 3,000

Total revenues ………………………………………………. $3,700

Expenses:

*Assumes the owner brought $600 of supplies from home and used all of them

during the month of July.

MILLIE’S CERAMIC STUDIO

BALANCE SHEET

JULY 31, 2016

Assets Liabilities and Owner’s Equity

Cash ………………………… $ 4,400 Unearned revenue ……………….. $ 700

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-29

DECISION CASES

READING AND INTERPRETING FINANCIAL STATEMENTS

LO 4,5 DECISION CASE 1-1 AN ANNUAL REPORT AS READY REFERENCE

1. Earnings per share is reported at the bottom of the consolidated statement of

income and comprehensive income. Information about any dividends paid to stock-

3. Information about the company’s current liquid assets, such as cash and accounts

receivable, can be found on the consolidated balance sheet. The balance sheet will

also provide bankers and other creditors with information about existing debts of the

company. The statement of cash flows is also useful in learning about a company’s

operating, financing, and investing activities over the past year.

LO 5 DECISION CASE 1-2 READING AND INTERPRETING CHIPOTLE’S

FINANCIAL STATEMENTS

1. 2014 Net income: $445,374,000

2. Assets = Liabilities + Stockholders’ Equity

$2,546,285,000 = $533,916,000 + $2,012,369,000

1-30 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 DECISION CASE 1-3 COMPARING TWO COMPANIES IN THE SAME INDUSTRY:

CHIPOTLE AND PANERA BREAD

1. Chipotle reported total revenues for 2014 of $4,108,269,000. This amount

represented an increase of 27.8% from the prior year. Panera Bread reported total

revenues for 2014 of $2,529,195,000, which represented an increase of 6.0% from

the prior year.

2. Chipotle reported net income for 2014 of $445,374,000, an increase of 36.0% from

the prior year. Panera Bread reported net income for 2014 of $179,293,000, which

was a decrease of 8.6% from the prior year’s amount.

MAKING FINANCIAL DECISIONS

LO 4 DECISION CASE 1-4 AN INVESTMENT OPPORTUNITY

All investments require a trade-off between risk and return. A college education may

have intrinsic value, but it is risky in that it does not assure anyone of a job upon

graduation. However, the return may be worth the risk involved in committing one’s life

savings to a college education if the degree allows one the opportunity to make a start

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-31

LO 5 DECISION CASE 1-5 PREPARATION OF PROJECTED STATEMENTS FOR A NEW

BUSINESS

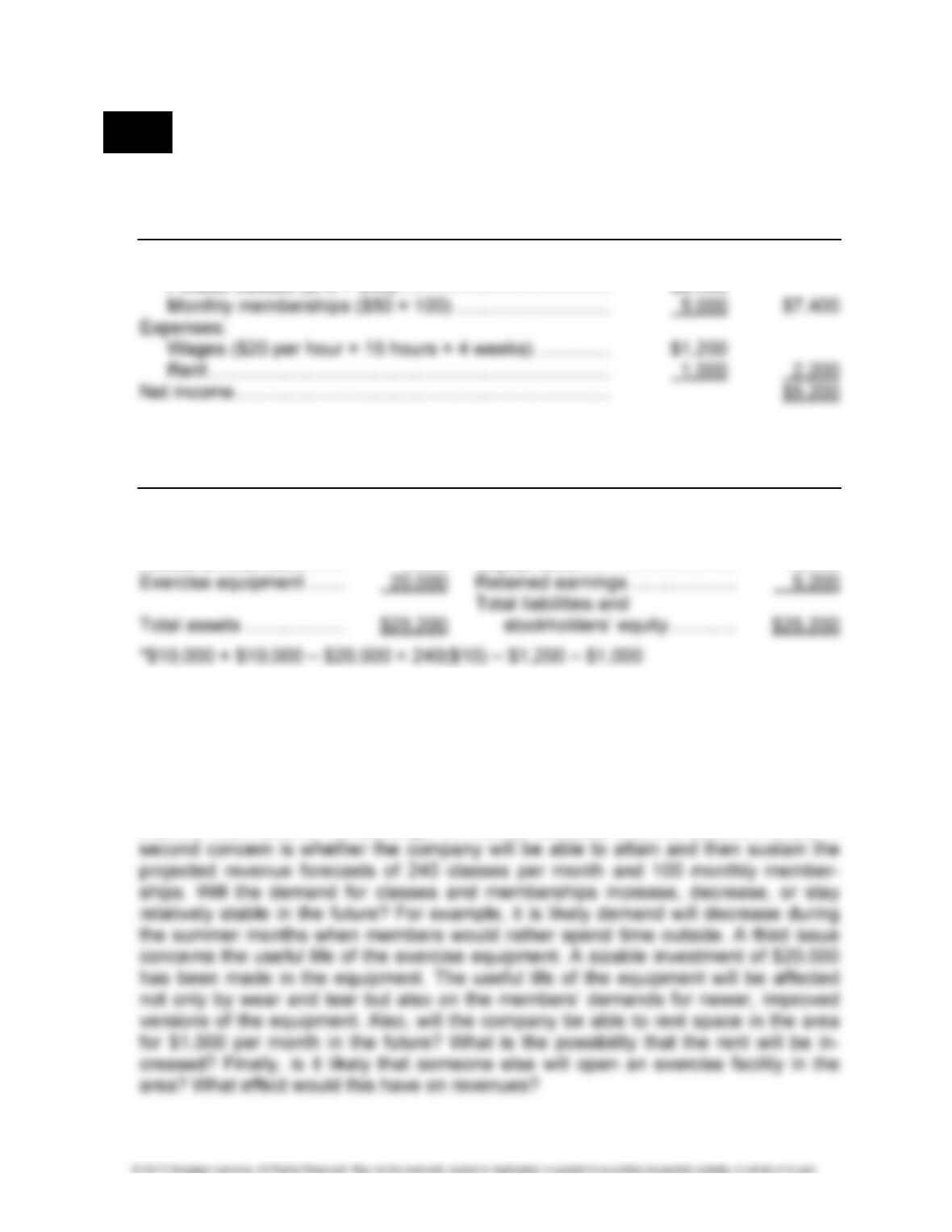

1. REMOTE FITNESS WORLD INC.

PROJECTED INCOME STATEMENT

FOR THE FIRST MONTH

Revenues:

2. REMOTE FITNESS WORLD INC.

PROJECTED BALANCE SHEET

END OF FIRST MONTH

Assets Liabilities and Stockholders’ Equity

Cash ………………………… $ 200* Notes payable ……………………… $10,000

Accounts receivable ……. 5,000 Capital stock ……………………….. 10,000

3. On the surface, the decision to invest in the business appears to be an easy one.

With net income of $5,200 per month, it seems as if the $10,000 loan from the bank

could be repaid in two months (of course, interest would have to be paid also). How-

ever, net income is not always the same as cash flow from operations. In this case,

the ability to generate $5,200 in cash flow each month depends on whether the

$5,000 in monthly memberships can be collected each month (the assumption is

that the first month’s memberships will not be collected until the second month). A

1-32 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

ETHICAL DECISION MAKING

LO 4,5,8 DECISION CASE 1-6 IDENTIFICATION OF ERRORS IN FINANCIAL STATE-

MENTS AND PREPARATION OF REVISED STATEMENTS

1. Recognize an ethical dilemma:

Errors made in preparing the financial statements:

a. The recognition of the 2017 season ticket sales as revenue in 2016. Because

Lakeside has not provided these fans with any service yet (the games), the sale

of the 2017 season tickets does not result in revenue in 2016.

personal residence is not an asset of the business.

Revised financial statements:

LAKESIDE SLAMMERS INC.

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2016

Revenues:

Single-game ticket revenue ………………………………….. $420,000

Concessions revenue ………………………………………….. 280,000

Total revenues ………………………………………………. $ 700,000

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-33

DECISION CASE 1-6 (Continued)

LAKESIDE SLAMMERS INC.

STATEMENT OF RETAINED EARNINGS

FOR THE YEAR ENDED DECEMBER 31, 2016

Retained earnings, beginning of year …………………………………………….. $ 0

LAKESIDE SLAMMERS INC.

BALANCE SHEET

DECEMBER 31, 2016

Assets Liabilities and Stockholders’ Equity

Cash ………………………… $ 5,000 Notes payable ……………………… $ 50,000

Equipment …………………. 50,000 Due to parent club ……………….. 125,000

Capital stock ……………………….. 40,000

2. Analyze the key elements in the situation:

a. The owners of the company may benefit in the short term, because the bank may

be more likely to give them a loan based on the original financial statements. All

outsiders are harmed, because the financial information they receive does not

represent the economic activity of the firm.

1-34 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

DECISION CASE 1-6 (Concluded)

c. The company may lack the resources to pay the claims of the creditors (the

notes payable and the liability to the parent club). The dividend payment probably

violated the corporate charter for the company (most companies would not be

permitted to pay dividends without positive stockholders’ equity).

3. List alternatives and evaluate the impact of each on those affected:

As one of the investors, your options are to either ignore the errors made in prepar-

ing the financial statements or call them to the attention of your fellow owners.

The information in the original set of financial statements is not relevant: the

revenue numbers are not useful for predicting future revenue numbers, since they

include both earned and unearned revenue. The information regarding season ticket

revenue does not provide reliable information to the outsider. Reliable information

represents what it claims to represent. The $140,000 recognized by the initial

4. Select the best alternative:

Because you are aware of these errors, it is your responsibility to share the revisions

with the other owners as well as the bank. It appears that a deliberate attempt has

been made to overstate the assets and income of the business for the express pur-

CHAPTER 1 • ACCOUNTING AS A FORM OF COMMUNICATION 1-35

LO 8 DECISION CASE 1-7 RESPONSIBILITY FOR FINANCIAL STATEMENTS AND THE

ROLE OF THE AUDITOR

1. Preparation of the financial statements in a company’s annual report is the responsi-

bility of that company.

3. Independence is critical to the integrity of the audit of a company’s financial state-

ments. A company’s financial statements are relied on by stockholders, bankers,