264

C A S E T E A C H I N G N O T E S

Ryanair: the low-fares airline future directions?

Eleanor OHiggins

1. Introduction

Ryanair was the first budget airline in Europe, modelled after the successful US carrier,

Southwest Airlines. It had enjoyed remarkable growth and financial success, as one of the most

profitable airlines in the world. Despite these apparent achievements, the case offers students

the opportunity to analyse and try to resolve various strategic issues faced by Ryanair. The most

pressing, shared by all airlines, was an industry that continued to be structurally sick and in

intensive carei, with plunging demand in the global economic recession and skyrocketing oil

Business students at all levels enjoy this case and relate to it, since air travel is an activity

virtually everyone has experienced and we all have stories to tell about the various airlines

which we have experienced. Nowadays, the additional charges levied by airlines are a talking

point. The colourful personality of Ryanair CEO, Michael OLeary is a further interest in the

case.

The case consists of:

an overview of Ryanair, with its history, philosophy and review of its financial results in

2012;

2. Position of the case

The case is a comprehensive one and would be well placed toward the end of a course on

strategic management. At this stage, students will have learned something of the economic,

organisational and human context of strategy. The case concentrates on how to analyse industry

environments (Chapter 2), and internal resources/capabilities of companies and their connection

Those participants with work experience can engage well with the internal management aspects

of the case, e.g. leadership, culture and human resources issues. Suggestions are also given in

this teaching note for using more advanced analytical techniques, such as scenario analysis

(Chapter 2).

3. Learning objectives

The overarching learning objective is a comprehensive strategic analysis and evaluation of a

business enterprise with the challenge of finding viable solutions to issues facing the company.

This includes:

An understanding of how a companys business strategy leads to success or failure, based

Understanding developmental directions and a change in the process; how the process of

sustaining competitive advantage is a dynamic one, requiring constant adjustment,

alongside external and internal monitoring (Chapters 7 and 11). In Ryanairs case the

constant search for ways to cut costs alongside finding ways to add charges and ancillary

4. Teaching scheme

The case breaks down into two inter-related parts that can be organised into two sessions of 1.5

to 2 hours each. The first session could cover an analysis of Ryanairs current position,

including a SWOT or situational analysis, assessing how robust the companys strategy is

5. Questions for discussion

First class session

1. Why has Ryanair been successful so far?

2. Is Ryanairs strategy sustainable?

267

Second class session

3. Would you recommend any changes to Ryanairs approach in changing environmental

circumstances? Does the proposal to introduce long-haul flights make strategic sense?

6. Case analysis

Tutors are referred to the Ryanair Supplement which follows this teaching note this gives

further details about Ryanair and its competitors

1. Why has Ryanair been successful so far?

Students can refer to Chapter 6 to answer this question. There is no doubt that Ryanair has been

successful in terms of market share and of profitability, notwithstanding the Aer Lingus issue.

Ryanairs operating profit margin compares very well to that of all comparators case Table 1a,

Supplement Exhibit S4. (Further, results published in March 2013 for fiscal 2013 showed a 13

per cent increase in revenues, a 14 per cent increase in pre-tax profits, and 13 per cent in post-

Ryanair could operate successfully in the No frills category because it charged the lowest fares

and it was the cost leader. Calculating Ryanairs operating profit margin from Case Table 1a,

compared to comparators and competitors in Supplement Exhibit S4, shows how well Ryanair

controls its operating costs. Its cost base is so low that its break-even load factor is the lowest in

the industry. It created a virtuous cycle, because low-cost allows for low fares, which attracts

customers. Ryanair would appear to have managed to integrate cost saving into all aspects of its

operations, perhaps something its competitors have not mastered as well.

268

We do not have any externally verified evidence about proportion of cancelled flights,

especially relative to competitors, so Ryanairs claims of superiority on these factors cannot be

confirmed. Some observers claim that encouraging carry-on luggage rather than checked-in

bags results in excessive delays in aircraft being loaded and unloaded as passengers consume

valuable time bringing carry-on bags onto the main deck, placing them in the overhead bins and

then taking their seats.

Ryanairs strategy can also be seen in terms of the frameworks that explain the achievement of

competitive advantage in Chapter 6 Hypercompetition and Game Theory.

Its aggressive approach to growth and opening new destinations and routes gives it first mover

advantage. Thus, it may inaugurate flights to a given airport, gaining an advantageous deal

The fact that Ryanair has such an extensive route system, compared to its competitors also gives

it an advantage, as rivals who wish to grow must bear in mind whether Ryanair is already in situ

where they are considering new destinations. This automatically curtails their options. Thus, if

they do decide to enter a route where Ryanair already exists, they will have to find a source of

2. Is Ryanairs strategy sustainable?

This question is best answered by first conducting a SWOT analysis to identify the issues facing

Ryanair, and to evaluate its present situation. (Note that while the Aer Lingus takeover issue is

germane to this question, it is dealt with separately in Question 4, below.)

269

2.1 We start with an environmental analysis, and an emphasis on the budget sector (Chapter 2).

The best way to approach this analysis is to go from the broadest unit of analysis to the

narrowest: (a) analysis of the whole European airline industry, through to the budget sector, (b)

(i) Competitive rivalry

General:

Economic recession has adversely affected traditional carriers.

Rivalry, along with non-viable cost structures, has ruined some national carriers, e.g.

Consolidation and rationalisation

Airlines try to counter increasing rivalry by forming strategic alliances, e.g. British

Airways with American Airlines

Budget:

Increasing number of rivals entering the sector, attracted by the idea that in a recession,

passengers will trade down. This refers to business as well as leisure passengers. In June

2013, Ryanair declared its ambitions for further growth in Germany, Scandinavia and

Central Europe to increase its market share of 15 per cent on European short-haul routes to

20 per cent by 201819.

Potential trend among some competitors to attempt to differentiate by adding some frills

and flexibility, especially to attract business travellers, e.g. EasyJet adds flexibility and uses

mainstream airports; Air Berlin offers on-board frills and frequent flyer benefits.

Some differentiation based on main airport locations, but adds costs for carriers.

Capacity utilisation (load factor) especially critical in low margin industry increased

rivalry.

Several budget airlines have gone bankrupt or been taken over:

Bmibaby, owned by BMI, bought out by British Airways in 2012

MyAir.com Italian airline which offered domestic Italian discount flights as well as

flights to other southern European countries, went out of service in the summer of 2009

Sterling Airlines an Icelandic based low cost airline offering flights between the

Scandinavian countries, UK and southern Europe, went out of service in autumn 2008

Volareweb.com Italian airline primarily offering flights within Italy; stopped flights in

early 2009.

Newly founded airlines or established airlines on new routes might have to be prepared to

lose money for a period of time to gain customers, especially if there is already an

established incumbent with deep pockets requires strong financial backing for entry.

Scarcity of landing slots, and reserved slots for national carriers serves as a barrier to entry

at certain airports, e.g. British Airways slots at Heathrow, Air France at De Gaulle.

Budget:

Perceived customer demand attracting new entrants to budget sector, although very few

financially as strong as established incumbents, Ryanair and EasyJet; budget airline

Ryanairs perspective low-moderate threat from new entrants

(iii) Power of suppliers

General:

Aircraft suppliers oversupply of aircraft and fierce rivalry between Airbus and Boeing. In

the past, stronger airlines, larger orders get better deals. Boeing, experiencing difficulties

Budget:

Aircraft suppliers hegemony of Boeing in budget sector broken by Airbus giving Boeing

less power. Nonetheless, Airbus not interested in bidding for Ryanair business, and their

Airports smaller secondary airports want business from budget airlines, offering good

deals:

Airport deals subject to EU constraints;

(iv) Power of buyers

General:

Passengers have more choice and access to information via the internet. Although this can

be confusing regarding special deals hedged with conditions and limited seat availability.

Budget:

Copious choice for passengers from budget airlines with different features and fare

structures, from mainstream airlines offering cheap fares, and from charter airlines moving

273

Distribution direct internet booking is very convenient for simple point-to-point travel

Blogs enable passengers to share complaints about customer service of various carriers

not favourable to Ryanair.

Ryanairs perspective strong power of buyers

(v) Threat of substitutes

General:

Fast rail and cross water tunnels and bridges enable faster and more convenient land travel.

Price of rail substitute is important; in many cases more expensive than budget and even

Budget:

Rail and road more likely to be viable substitutes for the shorter journeys typical of budget

airlines.

(b) Competitive groupings within the budget sector

Having identified the challenges facing the budget sector of the European airline industry, it

would be helpful to examine whether the sector can be broken down into subgroups with similar

competitive postures. This exercise could help to identify those rivals who are most threatening

In addition to information contained in the website supplement on Competitors and

Comparators, the most up-to-date information on competitors can be obtained by students as

part of the exercise of constructing the group maps, by visiting the websites of the various

competitors. The most relevant rivals of interest are easyJet, Air Berlin, Norwegian Airlines,

Wizz Air and Aer Lingus.

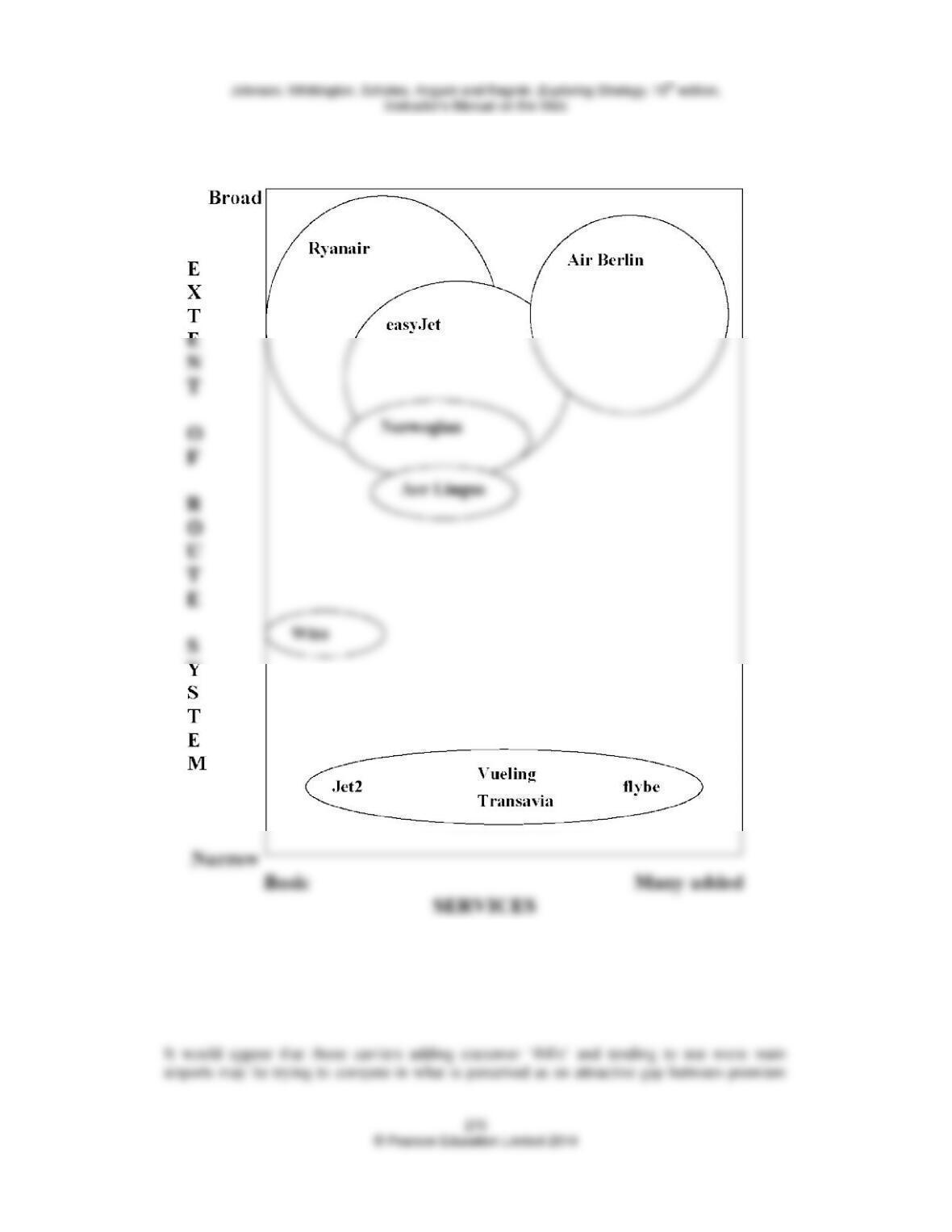

An example of a strategic map is given in Figure 1 of this teaching note. The dimensions used

are (i) extent of route system from number and locations of destinations and bases and

(ii) customer service. The information for both dimensions is contained in the text of the case,

and Skytrax ratingsiv, in Table 1c of the case study and Exhibits S2 and S5 of the website

Figure 1 Strategic group map of european airline industry, budget sector

There appears to be a rather crowded space of medium service airlines using main airports

(although not exclusively). easyJet is the leader within this space of airlines of varying size and

stage of development. Thus, this space may be becoming increasingly competitive in its own

right. Another question from the Ryanair perspective is whether these airlines are going to

encroach on its territory.

priced business class services and the most basic budget airlines, appealing to the price

conscious business traveller. The issue for these airlines is their ability to organise the provision

of added services and convenient airports without compromising the quintessential combination

of cost effective operations typical of Ryanair. However, instead of capturing a lucrative

strategic space, they could find that they are losing out to the mainstream carriers offering

bargains at the top end and the lowest cost/price budget carriers like Ryanair at the lower end. If

The lower part of the map shows a sample of small carriers that fall along a continuum of added

frills. The question is whether these small carriers can ever get to the critical mass to compete

with Ryanair and beat Ryanair at its own game, if they encounter Ryanair head-to-head on the

same routes. How can they outlast Ryanair in a price war, especially those who are competing

with a very basic product?

Air Berlin is certainly very pricey, and can be even more expensive than mainstream carrier

Lufthansa (Exhibit S1 website supplement). Financially, it is still fragile. It really does not

operate in the same space as Ryanair at all. However, it does appear to have captured significant

(c) Evaluating selected individual competitors

The next stage in industry analysis is the evaluation of rivals that compete in the same arena as

Ryanair. This evaluation helps to predict the actions of individual competitors and the impact of

those actions on Ryanair. In addition to the information provided in the case, the websites of the

individual competitors detailed above can be sourced.

easyJet

Air Berlin

Fast growing, by alliance (Niki, TUIfly) and many acquisitions (e.g. dba formerly Deutsch

BA); may be difficult to integrate all the acquisitions, alliances efficiently and effectively.

Definitely more upmarket than Ryanair, in effect has become a mainstream rather than a

budget airline; high cost base, due to free onboard services, offering connections rather than

point-to-point only, mixed fleet, main airports.

Norwegian

Another fast growing carrier, third largest budget carrier by market share in Europe in 2010.

Also upgrading and increasing its fleet.

278

Wizz Air

An example of an aggressive new competitor from Eastern Europe; very growth oriented,

but predominately in Eastern Europe. So far, very limited direct competition with Ryanair

or EasyJet.

Aer Lingus

The target of Ryanairs bid, the first one was a week after Aer Lingus partially floated in

2006.

Traditionally high cost, almost completely unionised, but reinvigorated after near

bankruptcy in 2001/02 recovery, thanks to cutting more than one-third of staff and severe

cost-cutting plan.

2.2 The next step in the SWOT is to evaluate Ryanairs strengths and weaknesses. This

analysis is based primarily on Chapter 3.

(a) Strengths: This question can be approached by listing Ryanairs strengths in relation to

competitors, and evaluating whether any of the strengths are sources of sustainable

competitive advantage. To fulfil this criterion, they should (1) offer superior customer

value, (2) be unique, (3) not be easily imitable by competitors and non-substitutable.

Given its passenger growth, load factors and market share, customers appear to be happy

enough with value for money proposition of Ryanair reputation as the aggressive low fares

champion.

Pursuing clear strategy, efficient and effective low cost operator (Case Tables 1a to 1c);

activities fit together to create low cost difficult to undercut Ryanair on cost, and

therefore on price (but see weaknesses for some possible cost and price vulnerabilities).

Low break even load factor, easily cleared, reduces financial risk. Fuel price is not under

control of the carrier, but this is no worse than competitors face continuous good

(b) Weaknesses: In an inverse way to the analysis of its strengths, Ryanairs weaknesses can be

listed and assessed to see whether any of them create critical vulnerabilities that impair

Ryanairs positioning and viability.

Any threats to low cost model are especially serious to Ryanair, since it is less able to pass

on cost increases on to passengers, due to dependency on low fares as its key selling point.

280

Overly cost conscious? Could be irritating to passengers; note that customers are not very

satisfied with Ryanair, other than value for money. This suggests that low fares are the only

factor that attracts customers to Ryanair.

Reputation Ryanair has antagonised many constituencies (EU commissioners and

officials, trade unions, competitors, various airport authorities, some politicians, and

journalists) whose support might have been useful in certain situations, e.g. the EU decision

about Charleroi, the court decision on wheelchairs, the decision by Channel 4 to highlight

alleged safety problems in Ryanair, and the authorities decision about the proposed

Is continuing stream of legal actions an unnecessary distraction and depletion of resources?

Or, again, is it a sign that Ryanair will lead the fight for low fares on behalf of the people?

Increase in security delays, and latterly, uncertainly due to volcanic ash clouds, etc. may

drive some passengers to use substitutes, like rail or car, but low prices of Ryanair mitigate

this threat somewhat.

2.3 Having completed the SWOT, we are now in a position to answer the question as to whether

Ryanairs strategy is sustainable.

On the strategy clock (Chapter 6), Ryanair is firmly in the Low Price, No Frills zone, highly

dependent on charging low prices. The question is whether Ryanairs formula enables the airline

to continue in its leadership position of the budget sector of the European airline industry. It can

be addressed by evaluating:

Figure 2a is a diagrammatic representation of how perceived customer value interacts with

efficiency to produce sustainability.

Figure 2a Strategic sustainability

Perceived

High

4 1

Quadrant 1 most sustainable

Quadrants 2 and 4 sustainable

Quadrant 3 unsustainable

(a) Customer viewpoint:

Ryanair has succeeded in penetrating Irish, UK and mainland Europe markets, including

Eastern Europe. Surveys suggest low customer expectations of service, whilst the fact that

Ryanair gets them to their destinations at a perceived rock-bottom price appeals to

customers.

(b) Producer/Efficiency viewpoint:

Ryanair has put all the pieces within its control in place to run a budget airline, as

demonstrated by its low break-even load factor.

However, certain cost advantages which Ryanair now enjoys could disappear:

favourable treatment by airports and service suppliers due to EU moves against anti-

competitiveness, Ryanair may no longer be able to benefit from discounts, grants, etc.

relative to competitors. As airports like Stansted, one of Ryanairs mainstays, became

(c) Sustainability:

Ryanair is probably in Quadrant 2 of teaching note Figure 2a in terms of sustainability. While it

gets a high vote on value for money, doubts over customer satisfaction as compared to other

airlines suggest that it could not be placed in the high category on perceived customer value

delivery. Although customers rate the components of the Ryanair experience poorly, the carrier

comes out quite well in the proportion of passengers who vote with their feet and continue to

patronise the airline.

Also, as predicted by Michael OLeary himself, Ryanair will find itself in vicious price wars on

a number of fronts, even if no one airline has the wherewithal to defeat Ryanair on its own.

These price wars, while not a threat to Ryanairs survival, could adversely affect profits. This

could undermine Ryanairs erstwhile robustness and have a further negative effect on its share

price.

Ryanairs past free or next-to-nothing seat giveaways in special period sales are interesting

from a game theory perspective (see game theory section in Chapter 6). While they do fill

empty seats, it is questionable as to whether they create long-term loyal customers, if the

experience itself isnt so great. However, free seats are a way of diverting passengers away from

Thus, Ryanair fulfils all the methods recommended in Chapter 6 to sustain its price-based

strategy: accept reduced margin; win a price war; reduce costs; focus on specific segments.

Another concurrent alternative for Ryanair is to attempt a move into the highest sustainable

category (Figure 2b). It could shy away from competing so exclusively on price and try to add

some more value to its customer offerings. However, it is constrained on the cost and logistics

side from augmenting perks and services to customers. Ryanair would need to be careful that

Figure 2b Ryanairs positioning and potential improvement

Perceived

customer

High