Chapter 17

ANSWERS TO QUESTIONS

1. What are the benefits of using a nominal anchor for the conduct of monetary policy?

A nominal anchor helps promote price stability by tying inflation expectations to low levels

2. What incentives arise for a central bank to fall into the time-inconsistency trap of pursuing

overly expansionary monetary policy?

Central bankers might think they can boost output or lower unemployment by pursuing

3. Why would it be problematic for a central bank to have a primary goal of maximizing

economic growth?

This could pose a problem for a couple reasons. First of all, monetary policy has limited

4. “Since financial crises can impart severe damage to the economy, a central bank’s primary

goal should be to ensure stability in financial markets.” Is this statement true, false, or

uncertain? Explain.

Uncertain. Most economists probably would not dispute that trying to maintain stability in

financial markets is important to the economy. However, having a constant and prioritized

5. “A central bank with a dual mandate will achieve lower unemployment in the long run than a

central bank with a hierarchical mandate in which price stability takes precedence.” Is this

statement true, false, or uncertain? Explain.

False. There is no long-run trade-off between inflation and unemployment, so in the long run

a central bank with a dual mandate that attempts to promote maximum employment by

6. Why is a public announcement of numerical inflation rate objectives important to the success

of an inflation-targeting central bank?

The success of inflation targeting relies on its ability to credibly anchor inflation expectations

at a low, desirable level. Without formal public announcements and reminders about the

7. How does inflation targeting help reduce the time-inconsistency problem of discretionary

policy?

Inflation targeting increases the accountability of monetary policymakers, and is a

8. What methods have inflation-targeting central banks used to increase communication with

the public and to increase the transparency of monetary policymaking?

Inflation-targeting central banks engage in extensive public information campaigns that

9. Why might inflation targeting increase support for the independence of the central bank in

conducting monetary policy?

Sustained success in the conduct of monetary policy as measured against a pre-announced

10. “Because inflation targeting focuses on achieving the inflation target, it will lead to

excessive output fluctuations.” Is this statement true, false, or uncertain? Explain.

False. Inflation targeting does not imply a sole focus on inflation. In practice, inflation

targeters do worry about output fluctuations, and inflation targeting may even be able to reduce

11. What are the key advantages and disadvantages of the monetary strategy used by the Federal

Reserve under Alan Greenspan and Ben Bernanke, in which the nominal anchor was implicit

rather than explicit?

This strategy has the following advantages: (a) it enables monetary policy to focus on

domestic considerations; (b) underscoring the importance of price stability has helped it to

mitigate the time-inconsistency problem, and (c) it has had a demonstrated success,

12. “The zero lower bound on short-term interest rates is not a problem, since the central bank

can just use quantitative easing to lower intermediate and longer-term interest rates

instead.” Is this statement true, false, or uncertain? Explain.

False. Although it is true that quantitative easing and other types of nonconventional policy

can be used once the zero lower bound is reached on short-term interest rates, it is not a

13. If higher inflation is bad, then why might it be advantageous to have a higher inflation target

rather than a lower target that is closer to zero?

The zero lower bound on nominal interest rates makes it harder to implement expansionary

policy as actual inflation (and hence short-term interest rates) fall closer to zero. As a

14. Why might macroprudential regulation be more effective in managing asset price bubbles

than monetary policy?

There are several reasons why monetary policy may not be effective in eliminating asset

price bubbles. The main reason is that asset price bubbles are extremely difficult to identify

15. Why might it be better to lean against credit-driven bubbles rather than just clean up after

other types of asset bubbles burst?

In general, the question of appropriate policy response is one of minimizing loss. Credit-

driven bubbles (such as the housing bubble experience that resulted in the global financial

crisis) can be far more devastating to the economy if a crash occurs than if policymakers acted

16. According to the Greenspan doctrine, under what conditions might a central bank respond to

a perceived stock market bubble?

Because a stock market bubble may be hard to identify (at least through consensus) and

policy could cause more damage than necessary, in general Greenspan would advocate not

acting directly on the stock market bubble. However, insofar as the stock market bubble raised

17. Classify each of the following as either a policy instrument or an intermediary target. Explain

your answer.

a. Long-term interest rates

Long-term interest rates are an intermediary target because they stand between short-term

interest rates and stabilized long-term interest rates.

18. “If the demand for reserves did not fluctuate, the Fed could pursue both a reserves target

and an interest-rate target at the same time.” Is this statement true, false, or uncertain?

Explain.

19. What procedures can the Fed use to control the federal funds rate? Why does control of this

interest rate imply that the Fed will lose control of nonborrowed reserves?

The Fed can control the federal funds rate by buying and selling bonds in the open market.

When the fed funds rate rises above the target level, the Fed would buy bonds, which would

20. What are the main criteria for choosing a policy instrument? Why? Explain.

The main criteria for choosing a policy instrument are observability and measurability, as

21. “Interest rates can be measured more accurately and quickly than reserve aggregates; hence

an interest rate is preferred to the reserve aggregates as a policy instrument.” Do you agree or

disagree? Explain your answer.

Disagree. Although nominal interest rates are measured more accurately and more quickly than

reserve aggregates, the interest-rate variable that is of more concern to policymakers is the

22. How can forward guidance as a tool of the central bank impact the policy instrument,

intermediate targets, and goals?

There are two main channels by which forward guidance can ultimately impact goal

variables. First off, the central bank can communicate information about the expected path of

23. What does the Taylor rule imply that policymakers should do to the fed funds rate under the

following scenarios?

a. Unemployment rises due to a recession.

If unemployment rises, this would lower the output gap, and trigger a lower fed funds rate

according to the Taylor rule.

d. Potential output declines while actual output remains unchanged.

If potential output declines, this is the opposite of (c) above, so the fed funds rate would

rise according to the Taylor rule.

ANSWERS TO APPLIED PROBLEMS

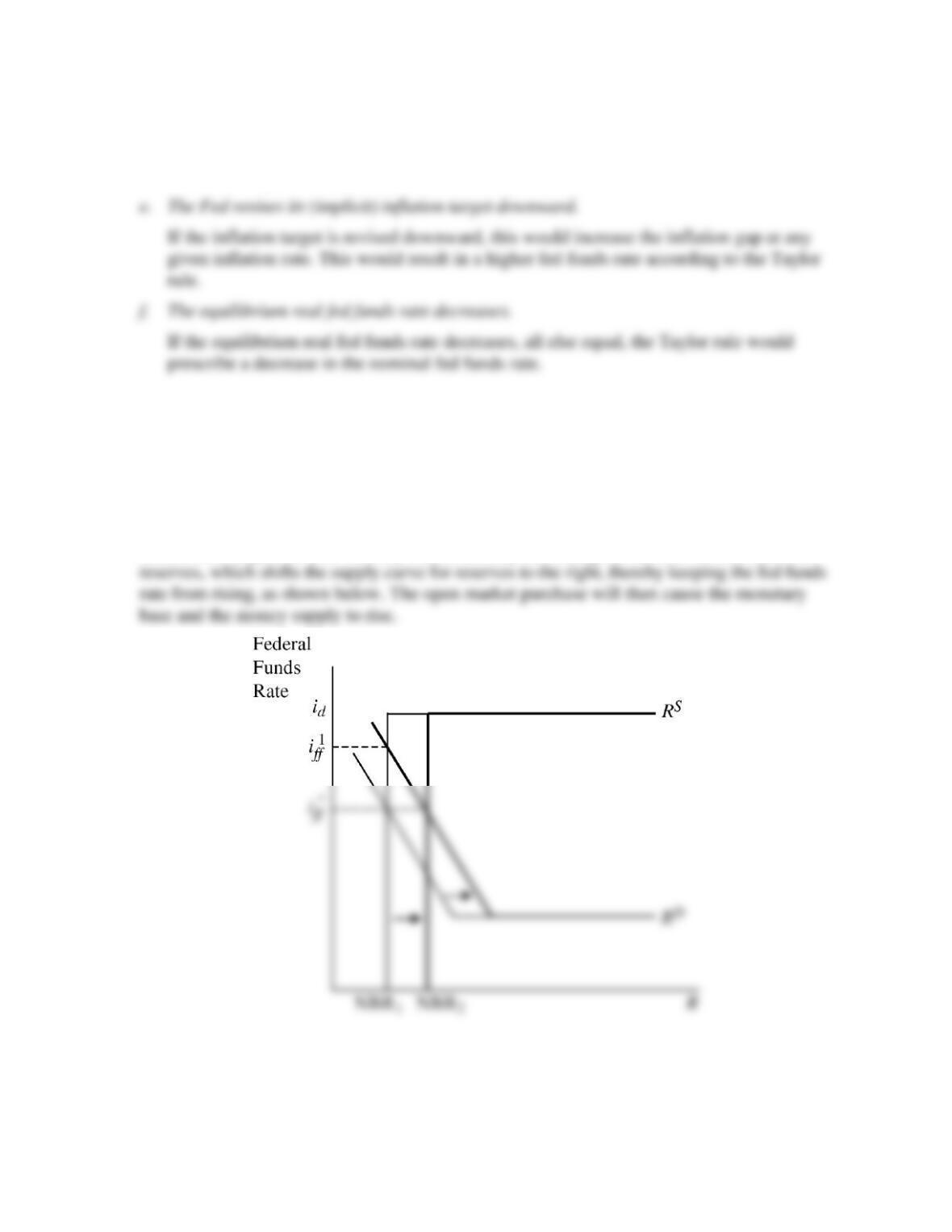

24. If the Fed has an interest-rate target, why will an increase in the demand for reserves lead to a

rise in the money supply? Use a graph of the market for reserves to explain.

An increase in the demand for reserves will raise the federal funds rate. In order to maintain the

interest rate target, the Fed will buy bonds, thereby increasing the amount of nonborrowed

25. Since monetary policy changes made through the fed funds rate occur with a lag,

policymakers are usually more concerned with adjusting policy according to changes in the

forecasted or expected inflation rate, rather than the current inflation rate. In light of this,

suppose that monetary policymakers employ the Taylor rule to set the fed funds rate, where

the inflation gap is defined as the difference between expected inflation and the target

inflation rate. Assume that the weights on both the inflation and output gaps are ½, the

equilibrium real fed funds rate is 4%, the inflation rate target is 3%, and the output gap is

2%.

a. If the expected inflation rate is 7%, then at what target should the fed funds rate be set

according to the Taylor rule?

Assuming the output gap and all other parameters remain constant, the Taylor rule is ffr =

πe + 2 + 0.5(πe – 2) + 0.5(1), where πe is expected inflation. Thus, if πe = 7%, then the fed

funds rate should be set to 7 + 2 + 0.5(5) + 0.5 = 12%.

c. Now suppose half of Fed economists forecast inflation to be 0%, and half forecast

inflation to be 14%. If the Fed uses the average of these two forecasts as its measure of

expected inflation, then at what target should the fed funds rate be set according to the

Taylor rule?

ANSWERS TO DATA ANALYSIS PROBLEMS

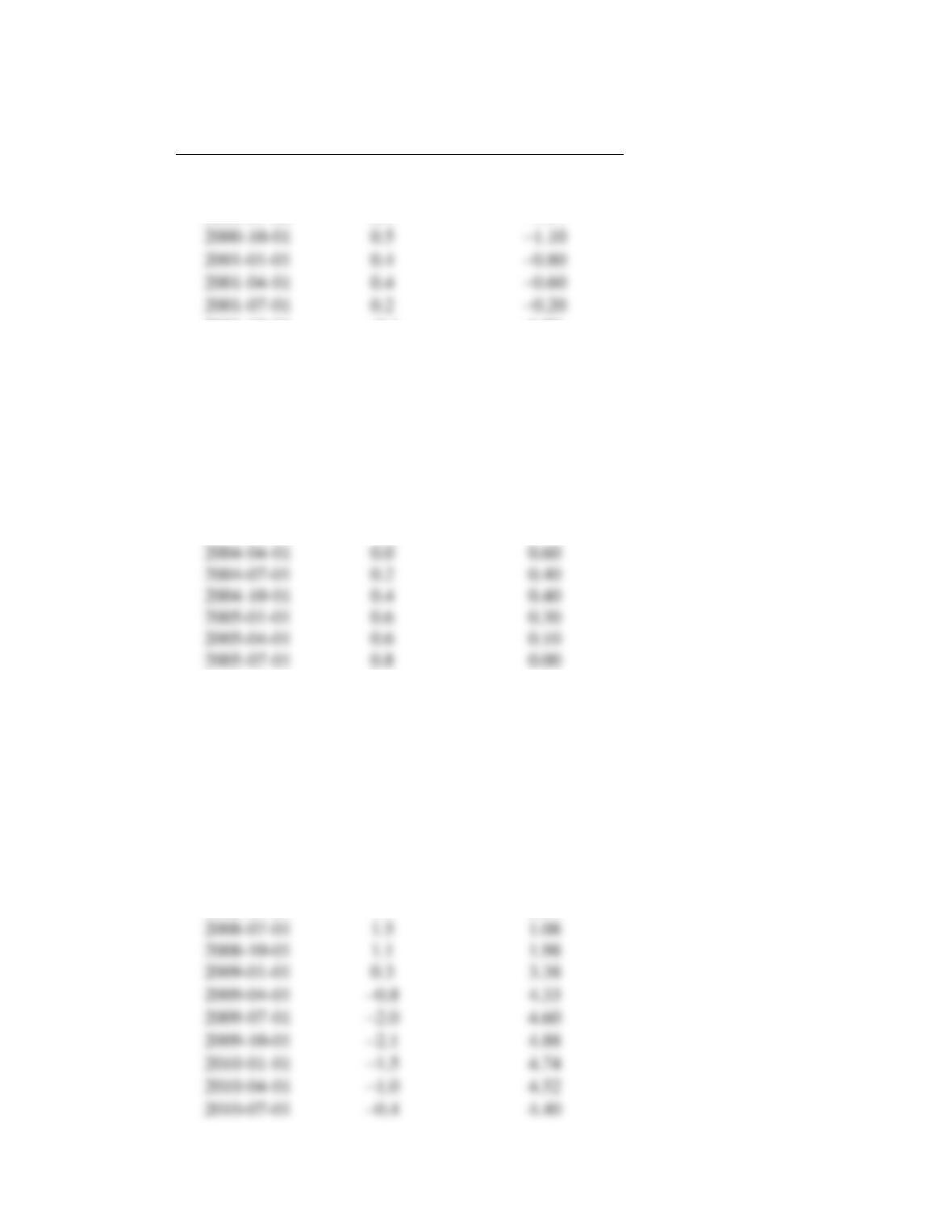

1. The Fed’s maximum employment mandate is generally interpreted as an attempt to achieve

an unemployment rate that is as close as possible to the natural rate and inflation that is

close to its 2% goal for personal consumption expenditure price inflation. Go to the St. Louis

Federal Reserve FRED database and find data on the personal consumption expenditure

price index (PCECTPI), the unemployment rate (UNRATE), and a measure of the natural

rate of unemployment (NROU). For the price index, adjust the units setting to “Percent

Change From Year Ago” to convert the data to the inflation rate; for the unemployment rate,

change the frequency setting to “Quarterly.” Download the data into a spreadsheet.

Calculate the unemployment gap and inflation gap for each quarter. Then, using the inflation

gap, create an average inflation gap measure by taking the average of the current inflation

gap and the gaps for the previous three quarters. Now apply the following (admittedly

arbitrary and ad hoc) test to the data from 2000:Q1 through the most recent data available:

If the unemployment gap is larger than 1.0 for two or more consecutive quarters, and/ or the

average inflation gap is larger in absolute value than 0.5 for two or more consecutive

quarters, consider the mandate “violated.”

a. Based on this ad hoc test, in which quarters has the Fed “violated” the price stability

portion of its mandate? In which quarters has the Fed “violated” the maximum

employment mandate?

See table below. As of 2017:Q1, the Fed violated the price stability mandate according

b. Is the Fed currently “in violation” of its mandate?

Yes, according to this test, the Fed currently is violating the price stability part of its

c. Interpret your results. What do your response to part (a) and the data imply about the

challenge that monetary policymakers face in achieving the Fed’s mandate perfectly at

all times?

It is clearly very difficult to meet the objectives set forth in the Fed’s mandate, even

under ideal conditions. The Fed “failed” the price stability test 40 out of 69 quarters over

4 Qtr. Average

Inflation Gap

Unemployment

Gap

2000-01-01

−0.2

−1.01

2000-04-01

0.1

−1.11

2000-07-01

0.4

−1.01

2000-10-01

0.5

−1.10

2001-01-01

0.4

−0.80

2001-04-01

0.4

−0.60

2001-07-01

0.2

−0.20

2001-10-01

−0.1

0.50

2002-01-01

−0.4

0.70

2002-04-01

−0.8

0.80

2002-07-01

−0.8

0.70

2002-10-01

−0.7

0.90

2003-01-01

−0.2

0.90

2003-04-01

−0.1

1.10

2003-07-01

0.0

1.10

2003-10-01

0.0

0.80

2004-01-01

−0.2

0.70

2004-04-01

0.0

0.60

2004-07-01

0.2

0.40

2004-10-01

0.4

0.40

2005-01-01

0.6

0.30

2005-04-01

0.6

0.10

2005-07-01

0.8

0.00

2005-10-01

0.8

0.02

2006-01-01

1.0

−0.27

2006-04-01

1.1

−0.37

2006-07-01

1.0

−0.36

2006-10-01

0.7

−0.55

2007-01-01

0.5

−0.45

2007-04-01

0.3

−0.44

2007-07-01

0.1

−0.24

2007-10-01

0.5

−0.13

2008-01-01

0.8

0.07

2008-04-01

1.1

0.37

2008-07-01

1.5

1.08

2008-10-01

1.1

1.98

2009-01-01

0.3

3.38

2009-04-01

−0.8

4.33

2009-07-01

−2.0

4.60

2009-10-01

−2.1

4.88

2010-04-01

−1.0

4.52

2010-07-01

−0.4

4.40

2010-10-01

−0.3

4.39

2011-01-01

−0.4

3.87

2011-04-01

−0.2

3.96

2011-07-01

0.1

3.85

2011-10-01

0.5

3.45

2012-01-01

0.7

3.17

2012-04-01

0.4

3.08

2012-07-01

0.1

2.90

2012-10-01

−0.1

2.73

2013-01-01

−0.3

2.65

2013-04-01

−0.5

2.47

2013-07-01

−0.5

2.30

2013-10-01

−0.7

1.92

2014-01-01

−0.7

1.75

2014-04-01

−0.6

1.27

2014-07-01

−0.5

1.18

2014-10-01

−0.5

0.82

2015-01-01

−0.7

0.67

2015-04-01

−1.1

0.61

2015-07-01

−1.4

0.33

2015-10-01

−1.7

0.24

2016-01-01

−1.5

0.15

2016-04-01

−1.3

0.15

2016-07-01

−1.2

0.16

2016-10-01

−0.9

−0.04

2017-01-01

−0.7

−0.04

2. Go to the St. Louis Federal Reserve FRED database and find data on the personal

consumption expenditure price index (PCECTPI), real GDP (GDPC1), an estimate of

potential GDP (GDPPOT), and the federal funds rate (DFF). For the price index, adjust the

units setting to “Percent Change From Year Ago” to convert the data to the inflation rate;

for the federal funds rate, change the frequency setting to “Quarterly.” Download the data

into a spreadsheet. Assuming the inflation target is 2% and the equilibrium real fed funds

rate is 2%, calculate the inflation gap and the output gap for each quarter, from 2000 until

the most recent quarter of data available. Calculate the output gap as the percentage

deviation of output from the potential level of output.

a. Use the output and inflation gaps to calculate, for each quarter, the fed funds rate

predicted by the Taylor rule. Assume that the weights on inflation stabilization and output

stabilization are both ½ (see the formula in the chapter). Compare the current (quarterly

average) federal funds rate to the federal funds rate prescribed by the Taylor rule. Does

the Taylor rule accurately predict the current rate? Briefly comment.

For the most recent period in 2017:Q1, the federal funds rate is 0.70%, while the Taylor

b. Create a graph that compares the predicted Taylor rule values with the actual quarterly

federal funds rate averages. How well, in general, does the Taylor rule prediction fit the

average federal funds rate? Briefly explain.

See graph below. The Taylor rule since 2000 has periods in which they are fairly closely

correlated, particularly from 2000 to 2002. However, there are significant gaps in other

times, or periods in which they do not seem to move together, such as the period from

c. Based on the results from the 2008–2009 period, explain the limitations of the Taylor

rule as a formal policy tool. How do these limitations help explain the use of

nonconventional monetary policy during this period?

Since the Federal funds rate was at the zero lower bound during that time, conventional

d. Suppose Congress changes the Fed’s mandate to a hierarchical one in which inflation

stabilization takes priority over output stabilization. In this context, recalculate the

predicted Taylor rule value for each quarter since 2000, assuming that the weight on

inflation stabilization is ¾ and the weight on output stabilization is ¼. Create a graph

showing the Taylor rule prediction calculated in part (a), the prediction using new

“hierarchical” Taylor rule, and the fed funds rate. How, if at all, does changing the

mandate change the predicted policy paths? How would the fed funds rate be affected

by a hierarchical mandate? Briefly explain.

See graph below. For the most part, the baseline Taylor rule and the hierarchical Taylor

rule predict nearly the same federal funds paths. The only significant deviations are from

e. Assume again equal weights of ½ on inflation and output stabilization, and suppose

instead that beginning after the end of 2008, the equilibrium real fed funds rate declines

by 0.05 each quarter (i.e. 2009:Q1 is 1.95, then 1.90, etc.), and once it reaches zero, it

remains at zero thereafter. How does it affect the prescribed fed funds rate? Why might

this be important for policymakers to take into consideration?

A decline in the equilibrium real fed funds rate has the effect of reducing the implied

Taylor rule fed funds rate lower. In fact, under this policy rule, it would have implied the

fed funds rate to be negative during 2015, which also coincided with a period of low