Chapter 16

ANSWERS TO QUESTIONS

1. If the manager of the open market desk hears that a snowstorm is about to strike New York

City, making it difficult to present checks for payment there and so raising the float, what

defensive open market operations will the manager undertake?

The snowstorm would cause float to increase, which would increase the monetary base. To

2. During the holiday season, when the public’s holdings of currency increase, what defensive

open market operations typically occur? Why?

3. If the Treasury pays a large bill to defense contractors and as a result its deposits with the

Fed fall, what defensive open market operations will the manager of the open market desk

undertake?

4. If float decreases to below its normal level, why might the manager of domestic operations

consider it more desirable to use repurchase agreements to affect the monetary base, rather

than an outright purchase of bonds?

Because the decrease in float is only temporary, the monetary base is expected to decline

only temporarily. A repurchase agreement only temporarily injects reserves into the banking

5. “The only way that the Fed can affect the level of borrowed reserves is by adjusting the

discount rate.” Is this statement true, false, or uncertain? Explain your answer.

False. The Fed also can affect the level of borrowed reserves by directly limiting the amount

6. “The federal funds rate can never be above the discount rate.” Is this statement true, false,

or uncertain? Explain your answer.

Uncertain. In theory, the market for reserves model indicates that once the fed funds rate

reaches the discount rate, it would never surpass the discount rate since banks would then

borrow directly from the Fed, and not in the fed funds market, which would prevent the fed

funds rate from ever rising above the discount rate. However, in practice, the fed funds rate

7. “The federal funds rate can never be below the interest rate paid on excess reserves.” Is this

statement true, false, or uncertain? Explain your answer.

Uncertain. In theory, the market for reserves model indicates that once the fed funds rate

reaches the interest rate on excess reserves, it would never go below this rate since banks

could then earn a risk-free interest rate paid directly from the Fed, rather than loaning excess

reserves in the more risky fed funds market at an equivalent or lower rate; this should prevent

8. Why is paying interest on excess reserves an important tool for the Federal Reserve in

managing crises?

During crises, the Fed may need to provide a large amount of liquidity to the banking and

financial system, which would reduce the fed funds rate. If the Fed needs to sterilize these

9. Why are repurchase agreements used to conduct most short-term monetary policy

operations, rather than the simple, outright purchase and sale of securities?

Repurchase agreements are used because they are temporary, and allow the Fed to adjust

10. Open market operations are typically repurchase agreements. What does this tell you about

the likely volume of defensive open market operations relative to the volume of dynamic open

market operations?

It suggests that defensive open market operations are far more common than dynamic

11. Following the global financial crisis in 2008, assets on the Federal Reserve’s balance sheet

increased dramatically, from approximately $800 billion at the end of 2007 to $3 trillion by

2011. Many of the assets held are longer-term securities acquired through various loan

programs instituted as a result of the crisis. In this situation, how could reverse repos

(matched sale–purchase transactions) help the Fed reduce its assets held in an orderly

fashion, while reducing potential inflationary problems in the future?

Because of the large amount of liquidity in banks and the financial system, this could

eventually lead to substantial inflation problems as liquidity in the form of excess reserves

12. “Discount loans are no longer needed because the presence of the FDIC eliminates the

possibility of bank panics.” Is this statement true, false, or uncertain?

This statement is false. The FDIC alone would likely be ineffective in eliminating bank panics

13. What are the disadvantages of using loans to financial institutions to prevent bank panics?

Providing loans to financial institutions creates a moral hazard problem. If firms know that

they will have access to Fed loans, they are more likely to take on risk, knowing that the Fed

14. Suppose your country is concerned about inflation and has set a target rate for the year. The

government believes that targeting inflation is the most important role of monetary politics.

The central bank is responsible for targeting inflation. What is the main tool that central

banks can use for inflation targeting? Will this tool be enough?

Some emerging countries do believe that targeted inflation is an important aspect of

monetary policy. In situations where the government has set a target inflation rate, central

15. Compare the methods of controlling the money supply—open market operations, loans to

financial institutions, and changes in reserve requirements—on the basis of the following

criteria: flexibility, reversibility, effectiveness, and speed of implementation.

Open market operations are more flexible, reversible, and faster to implement than the other

16. What are the advantages and disadvantages of quantitative easing as an alternative to

conventional monetary policy when short-term interest rates are at the zero lower bound?

Since short-term interest rates cannot be lowered below the zero bound in this environment,

conventional monetary policy would be ineffective. Thus, the main advantage of quantitative

17. Why is the composition of the Fed’s balance sheet a potentially important aspect of monetary

policy during an economic crisis?

By purchasing particular types of securities, the Fed can impact interest rates and liquidity in

particular sectors of credit and financial markets, thereby providing a more surgical provision

18. What is the main advantage and the main disadvantage of an unconditional policy

commitment?

19. In which economic conditions would a central bank want to use a “forward-guidance”

strategy? Based on your previous answer, can we easily measure the effects of such a

strategy?

In general a central bank would use a strategy of “forward guidance” when other types of

conventional tools of monetary policy cannot affect the economy in the desired way. In

practice, this strategy was followed by the Fed during the aftermath of the Great Recession

20. How do the monetary policy tools of the European System of Central Banks compare to the

monetary policy tools of the Fed? Does the ECB have a discount lending facility? Does the

ECB pay banks an interest rate on their deposits?

In general the set of monetary policy tools available to the ECB is quite similar to the one at

the Fed’s disposal. The ECB has a discount lending facility, called the marginal lending

21. What is the main rationale behind paying negative interest rates to banks for keeping their

deposits at central banks in Sweden, Switzerland, and Japan? What could happen to these

economies if banks decide to loan their excess reserves, but no good investment

opportunities exist?

22. In early 2016 as the Bank of Japan began to push policy interest rates negative, there was a

sharp increase in sales for home in Japan. Why might this be, and what does it mean for the

effectiveness of negative interest rate policy?

Negative policy interest rates have the effect of making deposit rates at banks negative. Thus,

people can avoid negative returns on holding cash by simply pulling their money out of

deposit accounts and keeping the cash in safes (with a zero return). This has two main

ANSWERS TO APPLIED PROBLEMS

23. If a switch occurs from deposits into currency, what happens to the federal funds rate? Use

the supply and demand analysis of the market for reserves to explain your answer.

The switch from deposits into currency lowers the amount of reserves as was shown in the

T-accounts of Chapter 15, and this lowers the supply of reserves at any given interest rate,

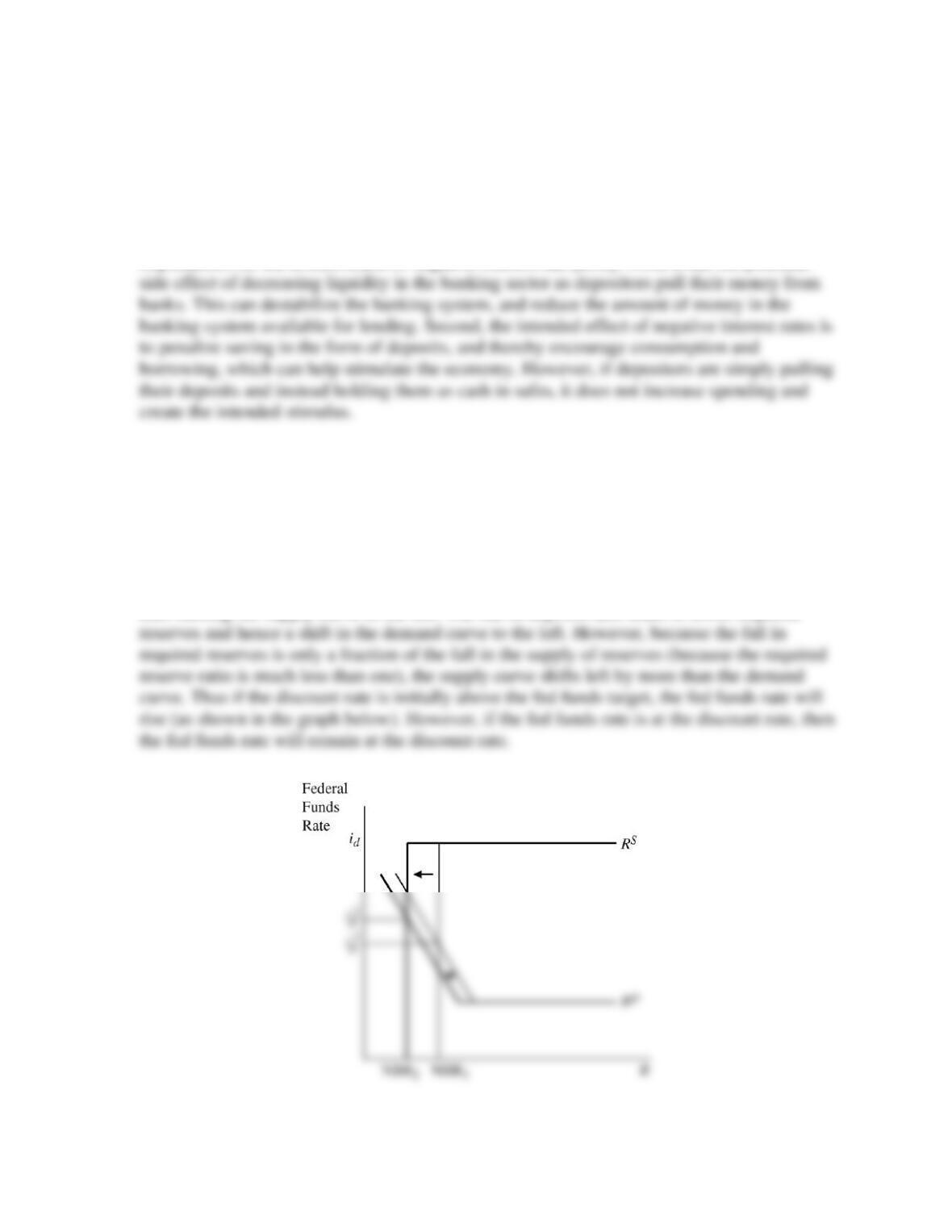

24. Why is it that a decrease in the discount rate does not normally lead to an increase in

borrowed reserves? Use the supply and demand analysis of the market for reserves to explain.

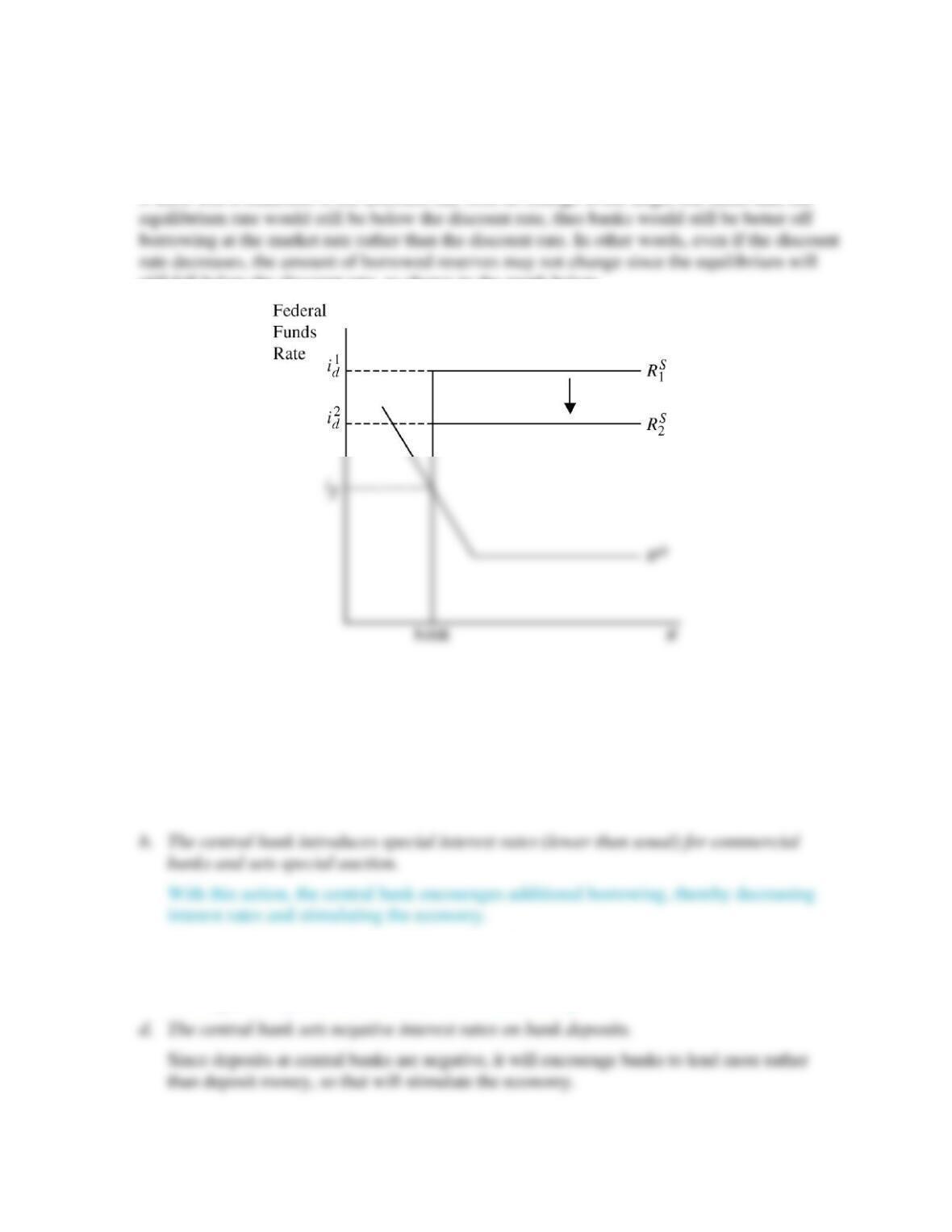

In most cases, the discount rate is set far enough above the fed funds target rate such that, even

still fall below the discount rate, as shown in the graph below.

25. Using the supply and demand analysis of the market for reserves, indicate how the following

situations would affect central bank interest rates and economies in general.

a. The central bank eliminates interest paid on excess reserve.

Usually central bank interest rates will decline, which may cause a decline in interest

rates in general and stimulate the economies.

c. The central bank conducts an open market sale of certain securities.

This action will increase the supply of securities and may increase interest rates leading

to a negative impact on the stimulation of the economy.

e. The central bank increases reserve requirements.

In such cases, money supply decreases making borrowing costlier, and has a negative

impact on economic stimulation.

ANSWERS TO DATA ANALYSIS PROBLEMS

1. Go to the St. Louis Federal Reserve FRED database, and find data on nonborrowed reserves

(NONBORRES) and the federal funds rate (FEDFUNDS).

a. Calculate the percent change in nonborrowed reserves and the percentage point change

in the federal funds rate for the most recent month of data available and for the same

month a year earlier.

b. Is your answer to part (a) consistent with what you expect from the market for reserves?

Why or why not?

Nonborrowed reserves decreased modestly over the one year period, while the federal

funds rate increased. This is generally consistent with what you would expect in the

2. In December 2008, the Fed switched from a point federal funds target to a range target

(and it’s possible that it will switch back to a point target in the future). Go to the St. Louis

Federal Reserve FRED database, and find data on the federal funds targets/ ranges

(DFEDTAR, DFEDTARU, DFEDTARL) and the effective federal funds rate (DFF).

Download into a spreadsheet the data from the beginning of 2006 through the most current

data available.

a. What is the current federal funds target/range, and how does it compare to the effective

federal funds rate?

b. When was the last time the Fed missed its target or was outside the target range? By how

much did it miss?

The last time the Fed missed its target was when it switched from a target of between

c. For each daily observation, calculate the “miss” by taking the absolute value of the

difference between the effective federal funds rate and the target (use the abs(.) function).

For the periods in which the rate was a range, calculate the absolute value of the “miss”

as the amount by which the effective federal funds rate was above or below the range.

What was the average daily miss between the beginning of 2006 and the end of 2007?

What was the average daily miss between the beginning of 2008 and December 15,

2008? What is the average daily miss for the period from December 16, 2008, to the most

current date available? Since 2006, what was the largest single daily miss? Comment on

the Fed’s ability to control the federal funds rate during these three periods.

From the beginning of 2006 to the end of 2007, the average daily miss was 0.05, or 5

basis points. From the beginning of 2008 to December 15, 2008, the average daily miss

and the most recent period, the Fed has demonstrated relatively good precision in

maintaining the federal funds rate close to target, but for somewhat different reasons. In

the 2006-2007 period, reserve demand was relatively stable, so it was relatively easier to

conduct defensive open market operations to keep the effective federal funds rate close to

target. In the most recent period, because a range is specified, it is somewhat easier to

keep the federal funds rate within target range. In addition, given the large size of the