Chapter 10

ANSWERS TO QUESTIONS

1. Why are deposit insurance and other types of government safety nets important to the health

of the economy?

A government safety net can short-circuit runs on banks and bank panics, and overcome

reluctance by depositors to put funds in the banking system. This helps to eliminate a

2. Why can government safety nets create both an adverse selection problem and a moral

hazard problem?

An adverse selection problem occurs when risk-taking individuals view the banking system

as an opportunity to use other people’s funds knowing that those funds are protected. A

3. In some countries, governments and bank authorities adopt policies that impose restrictions

on asset holdings. Why do they do this?

Banks and financial institutions tend to acquire risky assets because such assets generate

higher income. At the same time, governments need to make sure that depositors and

4. How could higher deposit insurance premiums for banks with riskier assets benefit the

economy?

The economy would benefit from reduced moral hazard; that is, banks would not want to

5. What are the costs and benefits of a too-big-to-fail policy?

The benefits of a too-big-to-fail policy are that it makes bank panics less likely. The costs are

that it increases the incentives for moral hazard by big banks that know that depositors do not

6. Suppose that you have $300,000 in deposits at a bank. After careful consideration, the FDIC

decides that this bank is now insolvent. Which method would you like to see the FDIC apply?

What if your deposit were $200,000?

If you have deposited $300,000 at the failed bank, it would be better for you if the FDIC uses

the purchase and assumption method. This way, the bank never closes, and you do not lose a

7. Would you recommend the adoption of a system of deposit insurance, like the FDIC in the

United States, in a country with weak institutions, prevalent corruption, and ineffective

regulation of the financial sector?

You probably would not recommend the adoption of a system of deposit insurance in a

country with weak institutions, prevalent corruption and ineffective regulation of the

8. Banking crises have occurred throughout the world, like the Finnish banking crisis of 1990s,

the 2002 Uruguay banking crisis, and the 2003 Myanmar banking crisis. In this context,

what similarity do we find when we look at various different countries?

One similarity seen across countries is that financial deregulation, with inadequate

supervision, can lead to increased moral hazard when banks take on additional risks.

9. What special problem do off-balance-sheet activities present to bank regulators, and what

have they done about it?

Because off-balance-sheet activities do not appear on bank balance sheets, they cannot be

dealt with by simple bank capital requirements, which are based on bank assets, such as a

10. What are some of the limitations to the Basel and Basel 2 Accords? How does the Basel 3

Accord attempt to address these limitations?

The original Basel Accord takes into account the riskiness of capital, but in practice, the risk

weights can differ substantially from the actual risk the bank faces. The Basel 2 Accords

were created to address this limitation; however, addressing these shortfalls greatly increased

the complexity of the accord, and there was substantial delay with countries adopting and

implementing the regulations. More specifically, Basel 2 did not require banks to hold adequate

11. How does bank chartering reduce adverse selection problems? Does it always work?

Chartering banks helps reduce the adverse selection problem because it attempts to screen

12. Why has the trend in bank supervision moved away from a focus on capital requirements to a

focus on risk management?

With the advent of new financial instruments, a bank that is quite healthy at a particular point

in time can be driven into insolvency extremely rapidly from risky trading in these

13. Suppose that after a few mergers and acquisitions, only one bank holds 70% of all deposits

in the United States. Would you say that this bank would be considered too big to fail? What

does this tell you about the ongoing process of financial consolidation and the government

safety net?

If only one bank holds 70% of all deposits in the United States, it would be a financial

catastrophe if this institution fails. We can expect that the FDIC and any other competent

office to do everything to prevent this institution to go bankrupt. However, as banks keep

14. Suppose Universal Bank holds $100 million in assets, which are composed of the following:

Required reserves: $10 million

Excess

reserves: $ 5 million

Mortgage

loans: $20 million

Corporate bonds: $15 million

Stocks: $25 million

Commodities: $25 million

a. Do you think it is a good idea for Universal Bank to hold stocks, corporate bonds, and

commodities as assets? Why or why not?

Probably not. Since these assets are relatively high risk, the bank is subject to fluctuations

b. If the housing market suddenly crashed, would Universal Bank be better off using a

mark-to-market accounting system or the historical-cost system?

If the housing market crashed, it is likely that many of the mortgage loans would default,

and the value of collateral on those loans (the market price of the house) would decline

c. If the price of commodities suddenly increased sharply, would Universal Bank be better

off using a mark-to-market accounting system or the historical-cost system?

If the price of commodities spiked, this would lead to a significant increase in the value

d. What do your answers to parts (b) and (c) tell you about the tradeoffs between the two

accounting systems?

Although mark–to–market rules can be more efficient in that they generally provide a more

accurate picture of a bank’s capital position, in severe downturns such as the one

15. Why might more competition in financial markets be a bad idea? Would restrictions on

competition be a better idea? Why or why not?

With more competition in financial markets, there are more firms making less profits. Thus,

16. In what way might consumer protection regulations negatively affect a financial

intermediary’s profits? Can you think of a positive effect of such regulations on profits?

Consumer protection regulations in general make sure that all relevant information is

disclosed to potential borrowers (including costs and conditions of loans) and forbid

discrimination against lenders. Complying with these regulations can be costly for financial

ANSWERS TO APPLIED PROBLEMS

17. Consider a failing bank. How much is a deposit of $290,000 worth to the depositor if the

FDIC uses the payoff method? The purchase-and-assumption method? Which method is

more costly to taxpayers?

Under the payoff method, the depositor only gets around $0.90/dollar on the amount of the

deposit above $250,000. Hence, the $290,000 is worth only $286,000 ($250,000 + $40,000 ×

0.90). Under the purchase and assumption policy, the bank is completely absorbed, and all

18. Consider a bank with the following balance sheet:

Assets

Liabilities

Required reserves

$ 9 million

Checkable deposits

$ 90 million

Excess reserves

$ 2 million

Bank capital

$ 6 million

T-bills

$ 46 million

Commercial loans

$ 39 million

The bank makes a loan commitment for $15 million to a commercial customer. Calculate the

bank’s capital ratio before and after the agreement. Calculate the bank’s risk-weighted

assets before and after the agreement.

Before the commitment, the capital ratio = 6/96 = 6.25%. Since the loan commitment is not

an accounting transaction yet, the capital ratio is the same after.

Before, the loan commitment, for risk-weighted assets:

Reserves and T-bills have a zero weight. So, $57 million has zero weight.

After the loan commitment, risk-weighted assets:

Reserves and T-bills have a zero weight. So $57 million has zero weight.

Commercial loans carry a 100% weight. RW Assets = $39 million.

19. Oldhat Financial starts its first day of operations with $11 million in capital. A total of $120

million in checkable deposits are received. The bank makes a $30 million commercial loan

and another $40 million in mortgages with the following terms: 200 standard, 30-year, fixed-

rate mortgages with a nominal annual rate of 5.25%, each for $200,000. Assume that

required reserves are 8%.

a. What does the bank balance sheet look like?

b. How well capitalized is the bank?

20. Early the next day, the bank invests $35 million of its excess reserves in commercial loans.

Later that day, terrible news hits the mortgage markets, and mortgage rates jump to 13%,

implying a present value of Oldhat’s current mortgage holdings of $99,838 per mortgage.

Bank regulators force Oldhat to sell its mortgages to recognize the fair market value. What

does Oldhat’s balance sheet look like? How do these events affect its capital position?

Debit

Credit

Cash

$ 99,838

Mortgages

$200,000

After the fact, the actual balance sheet is:

Assets

Liabilities

Required Reserves

$9.6 million

Checkable Deposits

$120 million

As the true state of the bank’s position is realized, it is revealed that bank capital is negative,

so the bank is in a dire capital position.

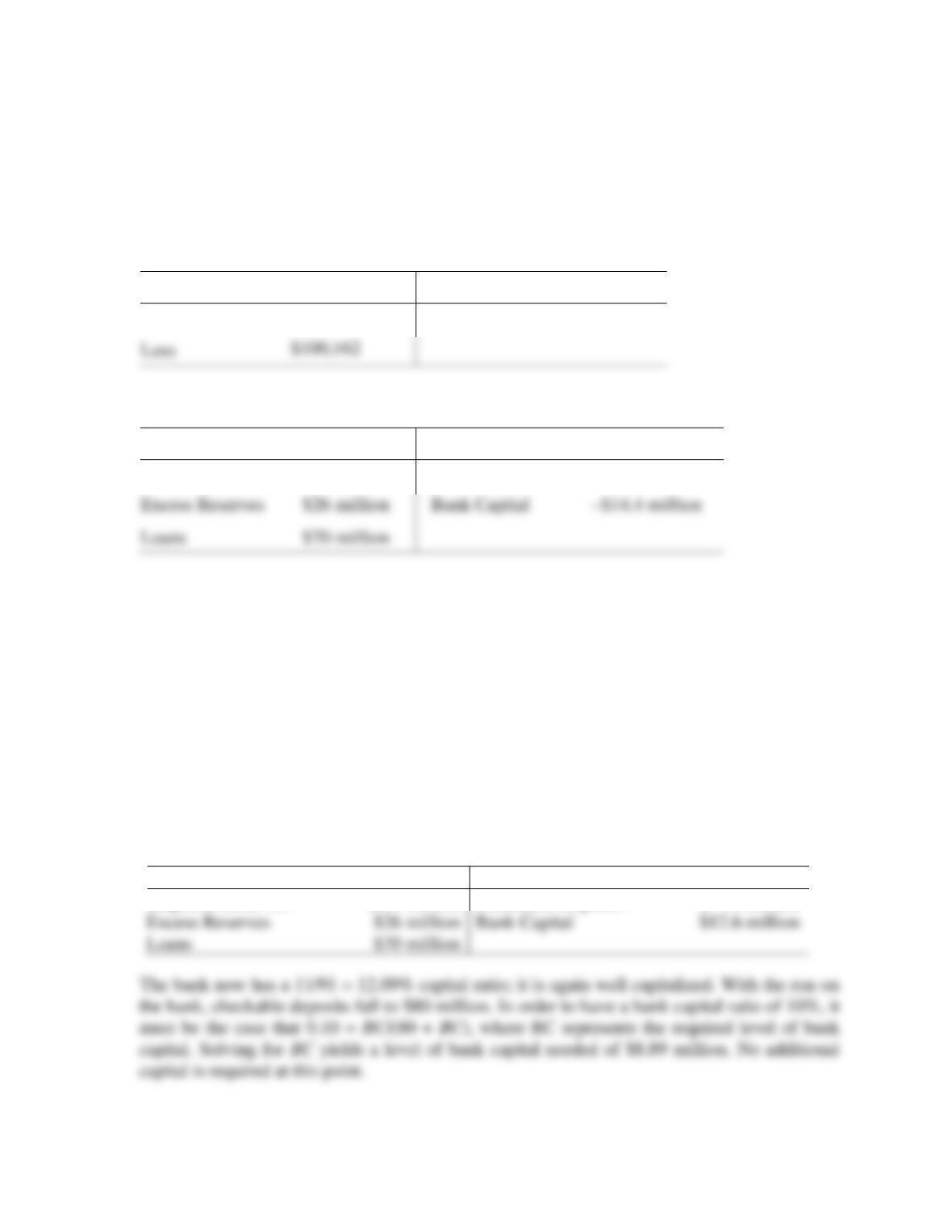

21. To avoid insolvency, regulators decide to provide the bank with $27 million in bank capital.

Assume that bad news about mortgages is featured in the local newspaper, causing a bank

run. As a result, $40 million in deposits is withdrawn. Show the effects of the capital injection

and the bank run on the balance sheet. Was the capital injection enough to stabilize the

bank? If the bank regulators decide that the bank needs a capital ratio of 10% to prevent

further runs on the bank, how much of an additional capital injection is required to reach a

10% capital ratio?

The effect of the capital injection and bank run are shown in the balance sheet below:

Assets

Liabilities

Required Reserves

$6.4 million

Checkable Deposits

$ 80 million

Excess Reserves

Bank Capital

$12.6 million

Loans

ANSWERS TO DATA ANALYSIS PROBLEMS

1. Go to the St. Louis Federal Reserve FRED database and find data on the number of

commercial banks in the United States in each of the following categories: average assets

less than $100 million (US100NUM), average assets between $100 million and $300 million

(US13NUM), average assets between $300 million and $1 billion (US31NUM), average

assets between $1 billion and $15 billion (US115NUM), and average assets greater than $15

billion (USG15NUM). Download the data into a spreadsheet. Calculate the percentage of

banks in the smallest (less than $100 million) and largest (greater than $15 billion)

categories, as a percentage of the total number of banks, for the most recent quarter of data

available and for 1990:Q1. What has happened to the proportion of very large banks? What

has happened to the proportion of very small banks? What does this say about the “too-big-

to-fail” problem and moral hazard?

In 1990:Q1, there were 25 ‘very large’ banks, and 9,529 ‘very small’ banks, representing

0.2% and 76.5% of total commercial banks in the United States, respectively. For the most

recent quarter of 2017:Q1, there were 77 ‘very large’ banks, and 1,324 ‘very small’ banks,

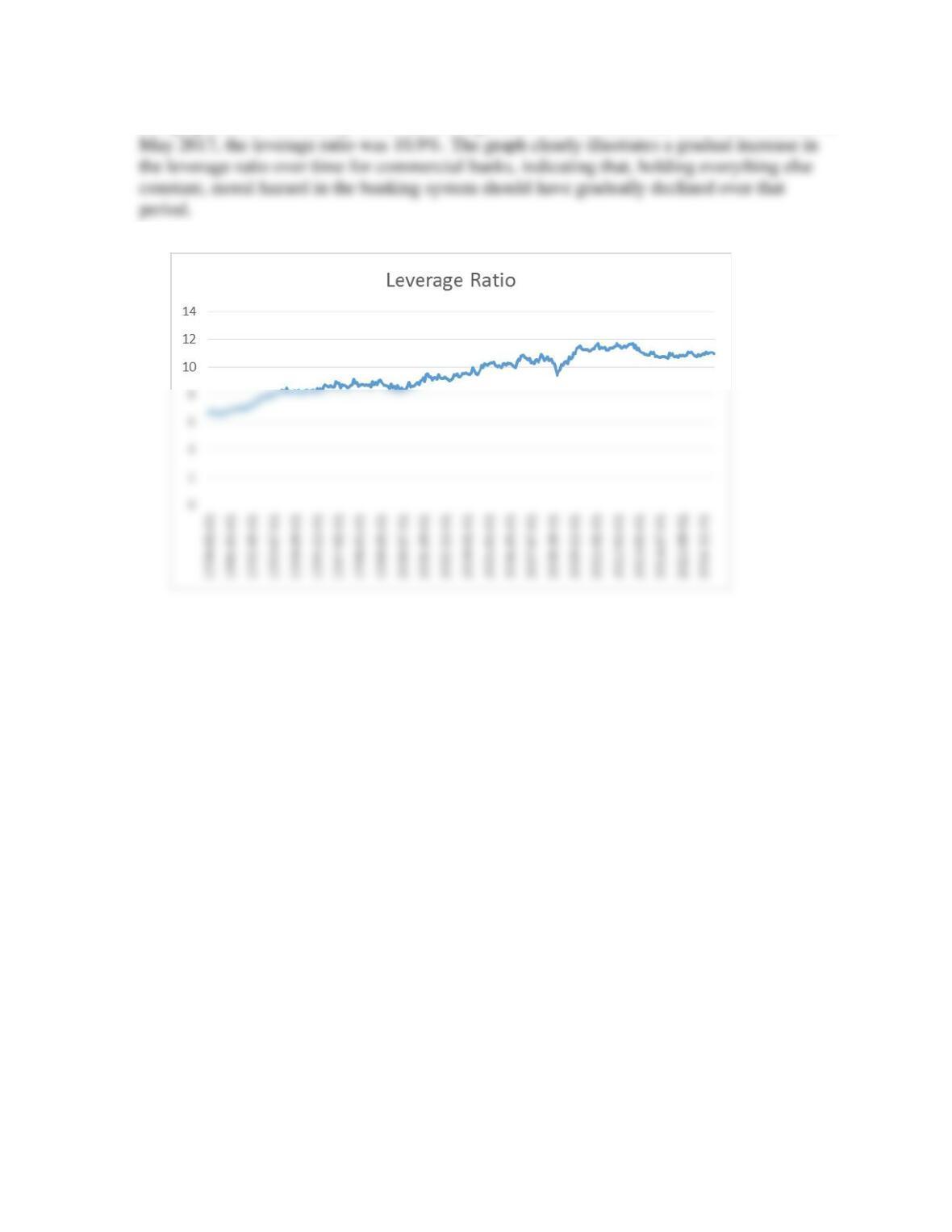

2. Go to the St. Louis Federal Reserve FRED database and find data on the residual of assets

less liabilities, or bank capital (RALACBM027SBOG), and total assets of commercial banks

(TLAACBM027SBOG). Download the data from January 1990 through the most recent

month available into a spreadsheet. For each monthly observation, calculate the bank

leverage ratio as the ratio of bank capital to total assets. Create a line graph of the leverage

ratio over time. All else being equal, what can you conclude about leverage and moral

hazard in commercial banks over time?

See graph below. In January 1990, the leverage ratio was 6.6%, and the most recent month of