APPENDIX J

Other Significant Liabilities

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Exercises

A

Problems

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

ANSWERS TO QUESTIONS

1. A contingent liability is a potential liability that may become an actual liability in the future.

5. In a capital lease agreement the lessee records the present value of the lease payments as an

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE J-1

BRIEF EXERCISE J-2

BRIEF EXERCISE J-3

SOLUTIONS TO EXERCISES

EXERCISE J-1

(a)

Estimated warranties outstanding:

Month

Estimate

Units Defective

Outstanding

November

December

Total

(b)

Warranty Expense (1,800 X $15) …………………………..

Warranty Liability ……………………………………….

Warranty Liability ………………………………………………..

Repair Parts ……………………………………………….

(c)

Warranty Liability (500 X $15) ………………………………

7,500

Repair Parts ……………………………………………….

EXERCISE J-2

(a) HARVEY ONLINE COMPANY

Partial Balance Sheet

Long-term debt due within one year ………………………..

Sales taxes payable ……………………………………………….

EXERCISE J-2 (Continued)

EXERCISE J-3

EXERCISE J-4

SOLUTIONS TO PROBLEMS

PROBLEM J-1A

(a)

Jan. 1

Cash …………………………………………………..

15,000

Notes Payable ……………………………..

15,000

(b)

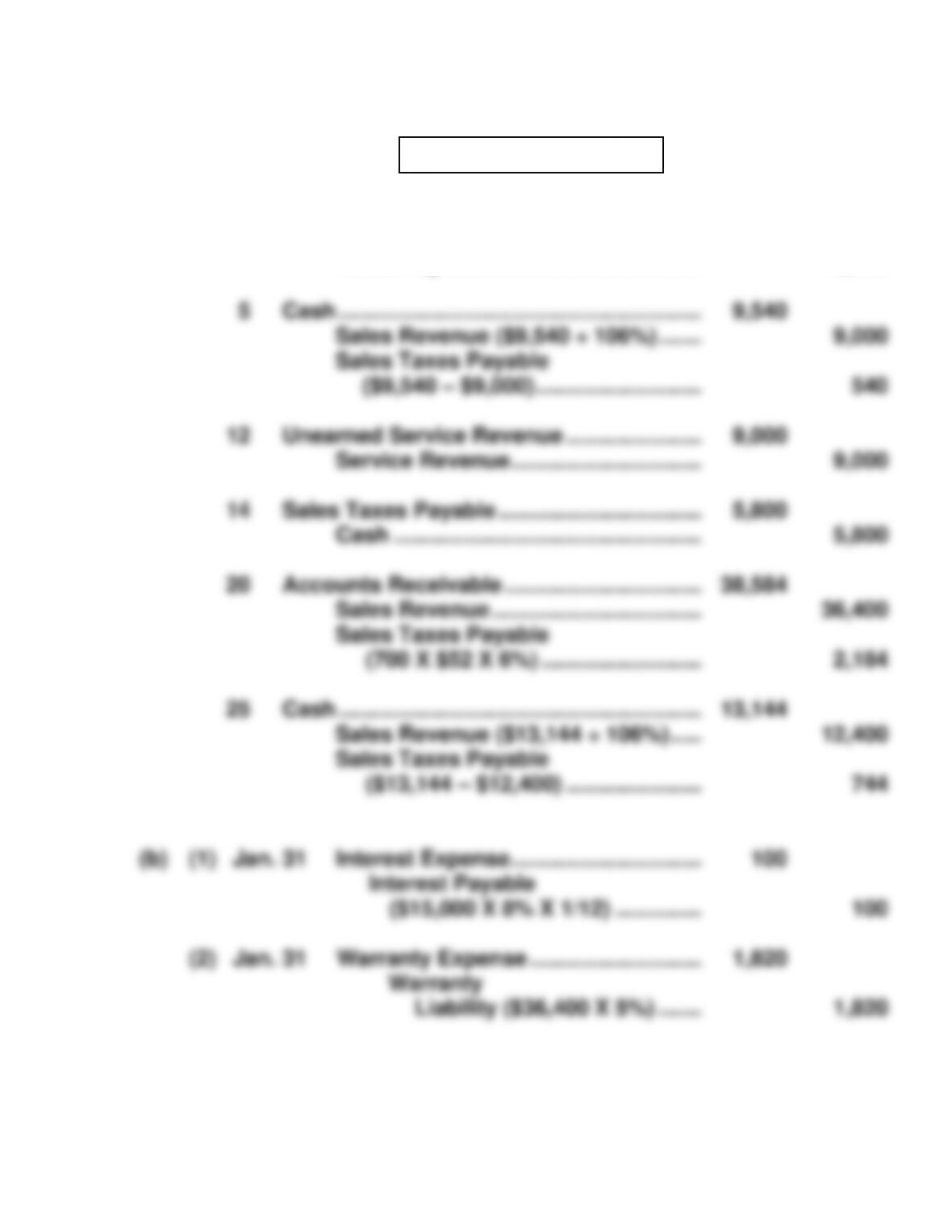

(1) Jan. 31

Interest Expense ………………………………..

Interest Payable

($15,000 X 8% X 1/12) ………………

(2) Jan. 31

Warranty Expense ……………………………..

Warranty

Liability ($36,400 X 5%) …….

Cash …………………………………………………..

Sales Revenue ($9,540 ÷ 106%) …….

Sales Taxes Payable

Unearned Service Revenue ………………….

Service Revenue ………………………….

Sales Taxes Payable …………………………...

Cash …………………………………………..

Accounts Receivable …………………………..

Sales Revenue …………………………….

Sales Taxes Payable

(700 X $52 X 6%) ……………………..

Cash …………………………………………………..

Sales Revenue ($13,144 ÷ 106%) …..

Sales Taxes Payable

PROBLEM J-1A (Continued)

(c)

Current liabilities

Accounts payable …………………………………………………….

Unearned service revenue ($15,000 – $9,000) …………….

Warranty liability ………………………………………………………

Interest payable ……………………………………………………….

PROBLEM J-2A

(a) Carson Enterprises should record the Logan Co. lease as a capital

Cash ……………………………………………….. 4,800

BYP J-1 FINANCIAL REPORTING PROBLEM

BYP J-2 FINANCIAL REPORTING PROBLEM

BYP J-3 GROUP DECISION CASE

(a) The bank probably did not loan money to Stephens, Inc. because it

(b) This lease should be reported as an operating lease. To be reported as

a capital lease, it must meet one of four criteria:

(c) Alexis Long means that many companies use leasing as a means of