APPENDIX I

Subsidiary Ledgers and Special Journals

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Describe the nature and

purpose of a subsidiary

ledger.

1, 2, 5, 7,12

1, 2

1

1, 2, 3, 4, 5, 6,

7, 9, 11, 12

1A, 2A, 3A,

4A, 5A, 6A

2. Explain how companies

3, 4, 6, 7, 8, 9,

10, 13

3, 4, 5, 6

2

6, 7, 8, 10, 12

1A, 2A, 3A,

4A, 5A, 6A

3. Indicate how companies

journal.

8, 11

7

1, 3, 9, 11, 13,

1A, 2A, 3A,

4A, 5A, 6A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Journalize transactions in cash receipts journal;

post to control account and subsidiary ledger.

Simple

30–40

2A

Journalize transactions in cash payments journal;

post to control account and subsidiary ledgers.

Simple

30–40

3A

Journalize transactions in multi-column purchases

journal; post to the general and subsidiary ledgers.

40–50

Journalize transactions in special journals.

prepare adjusting entries; prepare an adjusted

trial balance.

6A

Journalize in special journals; post; prepare

a trial balance.

60–70

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Describe the nature and purpose

of a subsidiary ledger.

QI-1

QI-2

QI-5

QI–12

BEI-1

BEI-2

EI-2

EI–11

DII-1

EI-1

EI-3

EI-4

EI-5

EI-6

EI-7

EI-9

EI–11

EI–12

PI-1A

PI–2A

PI–3A

PI–4A

PI–5A

PI–6A

QI-7

EI–12

PI–1A

PI–2A

PI–3A

QI-8

QI–11

BEI-7

EI-1

EI-3

EI-9

EI–13

EI–14

PI–1A

PI–2A

PI–3A

PI–5A

PI–6A

(Mini Practice Set)

ANSWERS TO QUESTIONS

1. A subsidiary ledger is a group of accounts with a common characteristic. The accounts are assembled

2. (a) (1) Transactions to individual accounts are generally posted daily to the subsidiary ledger.

3. Sales journal. Records entries for all sales of merchandise on account.

In general, special journals: (1) allow greater division of labor because various individuals can

record entries in different journals at the same time; and (2) reduce posting time of journals.

4. The entry for the sales return should be recorded in the general journal. Since Burguet Company

Questions Appendix I (Continued)

5. At the end of the month, after all postings to both the general ledger and the subsidiary accounts

6. The purpose of special journals is to facilitate the recording process of the business entity. Therefore,

8. The special journal is the sales journal. The other account is Sales Revenue. (The cash receipts

11. Typically included would be credit purchases of equipment, office supplies, and store supplies.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE I-1

Accounts Receivable Subsidiary Ledger

General Ledger

Adcock Co.

Accounts Receivable

BRIEF EXERCISE I-2

BRIEF EXERCISE I-3

BRIEF EXERCISE I-4

Debit

9,000

BRIEF EXERCISE I-5

(a). General Journal (if a one-column Purchases Journal)

BRIEF EXERCISE I-6

(a). Cash Receipts Journal

BRIEF EXERCISE I-7

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! I-1

Subsidiary balances:

DO IT! I-2

SOLUTIONS TO EXERCISES

EXERCISE I-1

(a) $344,400. Beginning balance of $314,000 plus $161,400 debit from sales

journal less $131,000 credit from cash receipts journal.

EXERCISE I-2

To: Erica Grier, Chief Financial Officer

From: Student

Subject: Martha Nott account

The explanation of the three entries in the subsidiary ledger for the Martha

Nott account is as follows:

EXERCISE I-3

(a) & (b) General Ledger

Accounts Receivable

Date

Explanation

Ref.

Debit

Credit

Balance

Dey

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Debit

Credit

Balance

Date

Explanation

Debit

Credit

Balance

EXERCISE I-3 (Continued)

Zeyen

Date

Explanation

Ref.

Debit

Credit

Balance

(c) STARK COMPANY

Schedule of Customers

As of September 30, 2017

EXERCISE I-4

(a) $3,700 [$10,200 – ($4,000 + $2,500)].

EXERCISE I-5

(a) $3,375 [$8,250 – ($3,000 + $1,875)].

EXERCISE I-6

(a) & (b) NORREN COMPANY

Sales Journal S1

Date

Account

Debited

Invoice

No.

Ref.

Accounts Receivable Dr.

Sales Revenue Cr.

Cost of Goods Sold Dr.

Inventory Cr.

EXERCISE I-7

(a) & (b) MILNER CO.

Cash Receipts Journal CR1

Date

Account

Credited

Ref.

Cash

Dr.

Sales

Discounts

Dr.

Accounts

Receivable

Cr.

Sales

Revenue

Cr.

Other

Accounts

Cr.

Cost of Goods Sold

Dr.

Inventory

Cr.

2

Common Stock

9,000

9,000

EXERCISE I-7 (Continued)

MILNER CO.

Cash Payments Journal CP1

Date

Ck.

No.

Account Debited

Ref.

Other

Accounts

Dr.

Accounts

Payable

Dr.

Cash

Cr.

EXERCISE I-8

(a) Journal

(b) Columns in the journal

Cash Payments

Cash Receipts

Sold (Dr.), and Inventory (Cr.).

1.

2.

Cash Payments

Cash Receipts

Cash (Cr.), Other Accounts (Dr.).

Cash (Dr.), Sales Discounts (Dr.), and

May 3

Inventory

Salaries and Wages Expense

700

EXERCISE I-9

(a) Mar. 2 Equipment …………………………………………….. 9,400

Accounts Payable—Brantly

Company ……………………………………. 9,400

(b) To: President Nolasco

From: Chief Accountant

Subject: Posting of Control and Subsidiary Accounts

The posting of these accounts varies with the journals used in recording

the transactions.

EXERCISE I-10

1. Cash Payments Journal 8. Cash Receipts Journal

EXERCISE I-11

(a) The debit posting reference on February 28 should be from the cash

EXERCISE I-12

(a)

Purchases Journal P1

Date

Account Credited

Ref.

Inventory Dr.

Accounts Payable Cr.

EXERCISE I-12 (Continued)

(b)

General Journal

Date

Accounts and Explanations

Ref.

Debit

Credit

EXERCISE I-13

EXERCISE I-14

SOLUTIONS TO PROBLEMS

PROBLEM I-1A

(a)

Cash Receipts Journal CR1

Account

Cash

Sales

Discounts

Accounts

Receivable

Sales

Revenue

Cr.

Other

Accounts

Cost of Goods Sold

Dr.

Inventory

(b) General Ledger

Accounts Receivable No. 112

Date

Explanation

Ref.

Debit

Credit

Balance

Accounts Receivable Subsidiary Ledger

Park

Date

Explanation

Ref.

Debit

Credit

Balance

Hurt Co.

Kolten

1,500

PROBLEM I-1A (Continued)

Kolten

Date

Explanation

Ref.

Debit

Credit

Balance

Hurt Co.

Date

Explanation

Ref.

Debit

Credit

Balance

Afzal

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM I-2A

(a)

Cash Payments Journal CP1

Date

Ck.

No.

Account Debited

Ref.

Other

Accounts

Dr.

Accounts

Payable

Dr.

Inventory

Cr.

Cash

Cr.

(b) General Ledger

Accounts Payable No. 201

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM I-2A (Continued)

Trent Company

PROBLEM I-3A

(a)

Purchases Journal P1

Accounts

Payable

Inventory

Other

Accounts

Sales Journal S1

Date

Account Debited

Ref.

Accounts Receivable Dr.

Sales Revenue Cr.

Cost of Goods Sold Dr.

Inventory Cr.

PROBLEM I-3A (Continued)

General Journal G1

Date

Accounts and Explanations

Ref.

Debit

Credit

(b) General Ledger

Accounts Receivable No. 112

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM I-3A (Continued)

Equipment No. 157

Date

Explanation

Ref.

Debit

Credit

Balance

Cost of Goods Sold No. 505

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM I-3A (Continued)

Accounts Receivable Subsidiary Ledger

Orsen Bros.

Date

Explanation

Ref.

Debit

Credit

Balance

Gentry Company

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Credit

Balance

Date

Explanation

Ref.

Credit

Balance

Date

Explanation

Ref.

Credit

Balance

PROBLEM I-3A (Continued)

Rensing Shipping

Date

Explanation

Ref.

Debit

Credit

Balance

Langer Company

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

Explanation

Ref.

Debit

Credit

PROBLEM I-3A (Continued)

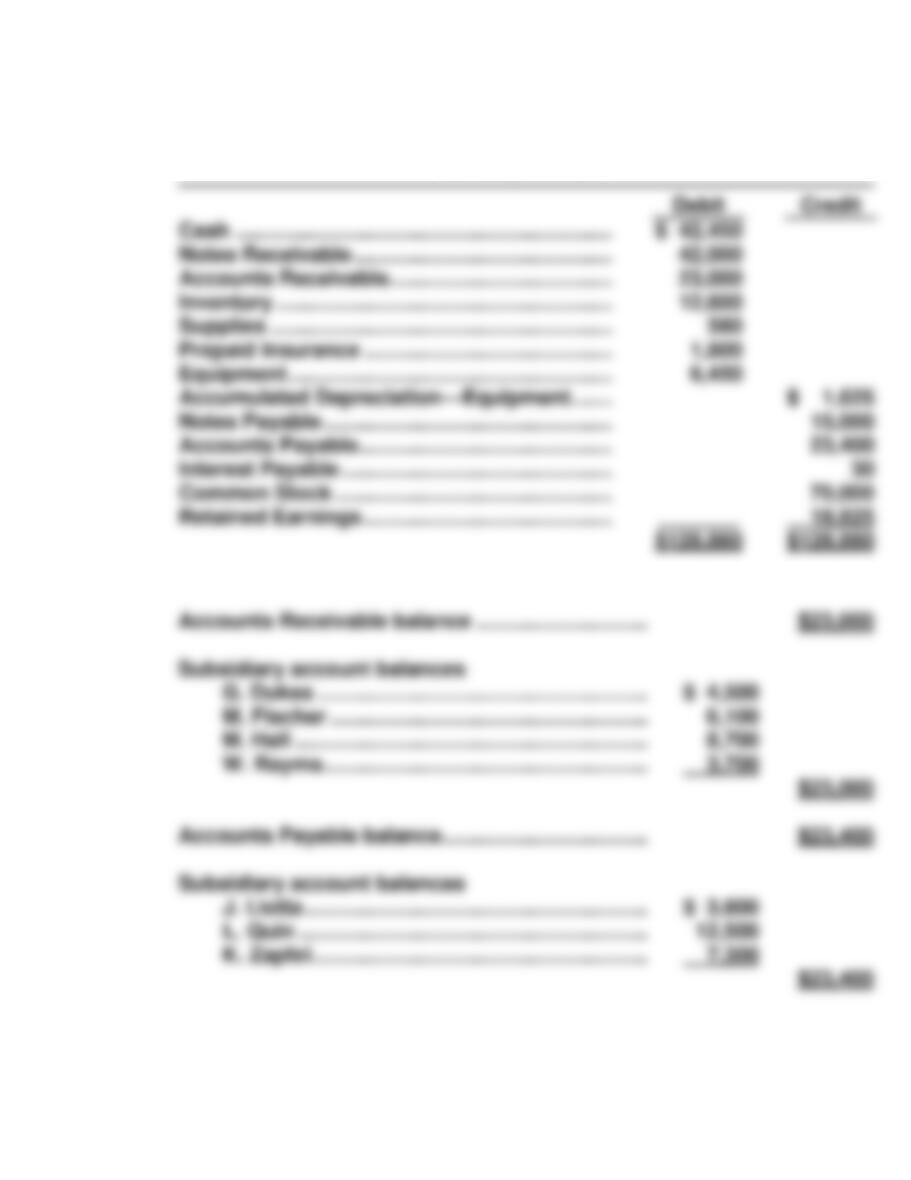

(c) Accounts receivable balance …………………………... $16,965

PROBLEM I-4A

(a), (b) & (c)

Sales Journal S1

Date

Account

Debited

Invoice

No.

Ref.

Accounts Receivable Dr.

Sales Revenue Cr.

Cost of Goods Sold Dr.

Inventory Cr.

Purchases Journal P1

Date

Account Credited

Ref.

Inventory Dr.

Accounts Payable Cr.

PROBLEM I-4A (Continued)

Cash Receipts Journal CR1

Date

Account

Credited

Ref.

Cash

Dr.

Sales

Discounts

Dr.

Accounts

Receivable

Cr.

Sales

Revenue

Cr.

Other

Accounts

Cr.

Cost of Goods Sold

Dr.

Inventory

Cr.

30,576

1,200

13,200

(X)

PROBLEM I-5A

(a), (d) & (g) General Ledger

Cash No. 101

Date

Explanation

Ref.

Debit

Credit

Balance

Inventory No. 120

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM I-5A (Continued)

Accounts Payable No. 201

Date

Explanation

Ref.

Debit

Credit

Balance

Sales Revenue No. 401

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Ref.

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM I-5A (Continued)

Supplies Expense No. 631

Date

Explanation

Ref.

Debit

Credit

Balance

(b)

Sales Journal S1

Date

Account Debited

Ref.

Accounts Receivable Dr.

Sales Revenue Cr.

Cost of Goods Sold Dr.

Inventory Cr.

Cash Receipts Journal CR1

Date

Account

Credited

Ref.

Cash

Dr.

Sales

Discounts

Dr.

Accounts

Receivable

Cr.

Sales

Revenue

Cr.

Other

Accounts

Cr.

Cost of Goods Sold

Dr.

Inventory

Cr.

(414)

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM I-5A (Continued)

(c) Accounts Receivable Subsidiary Ledger

Edwards Co.

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Date

Explanation

Ref.

Debit

Credit

Balance

Carmoni

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM I-5A (Continued)

G. Young

Date

Explanation

Ref.

Debit

Credit

Balance

(e) RAMIREZ CO.

Trial Balance

July 31, 2017

Date

Explanation

Ref.

Credit

Balance

Explanation

Ref.

Debit

Credit

PROBLEM I-5A (Continued)

PROBLEM I-5A (Continued)

(h) RAMIREZ CO.

Adjusted Trial Balance

July 31, 2017

PROBLEM I-6A

(b) & (c)

Cash Receipts Journal CR1

Date

Account Credited

Ref.

Cash

Dr.

Sales

Discounts

Dr.

Accounts

Receivable

Cr.

Sales

Revenue

Cr.

Other

Accounts

Cr.

Cost of Goods Sold

Dr.

Inventory

Cr.

Sales Journal S1

Date

Account

Debited

Ref.

Accounts Receivable Dr.

Sales Revenue Cr.

Cost of Goods Sold Dr.

Inventory Cr.

(X)

PROBLEM I-6A (Continued)

Purchases Journal P1

Date

Account Credited

Ref.

Inventory Dr.

Accounts Payable Cr.

General Journal G1

Date

Accounts and Explanations

Ref.

Debit

Credit

(a) & (c)

General Ledger

Cash No. 101

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM I-6A (Continued)

Accounts Receivable No. 112

Date

Explanation

Ref.

Debit

Credit

Balance

Inventory No. 120

Date

Explanation

Ref.

Debit

Credit

Balance

Equipment No. 157

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM I-6A (Continued)

Notes Payable No. 200

Common Stock No. 311

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Credit

Balance

Date

Explanation

Ref.

Credit

Balance

Explanation

Ref.

Debit

Credit

Balance

PROBLEM I-6A (Continued)

Cost of Goods Sold No. 505

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Accounts Receivable Subsidiary Ledger

Explanation

Ref.

Credit

Balance

PROBLEM I-6A (Continued)

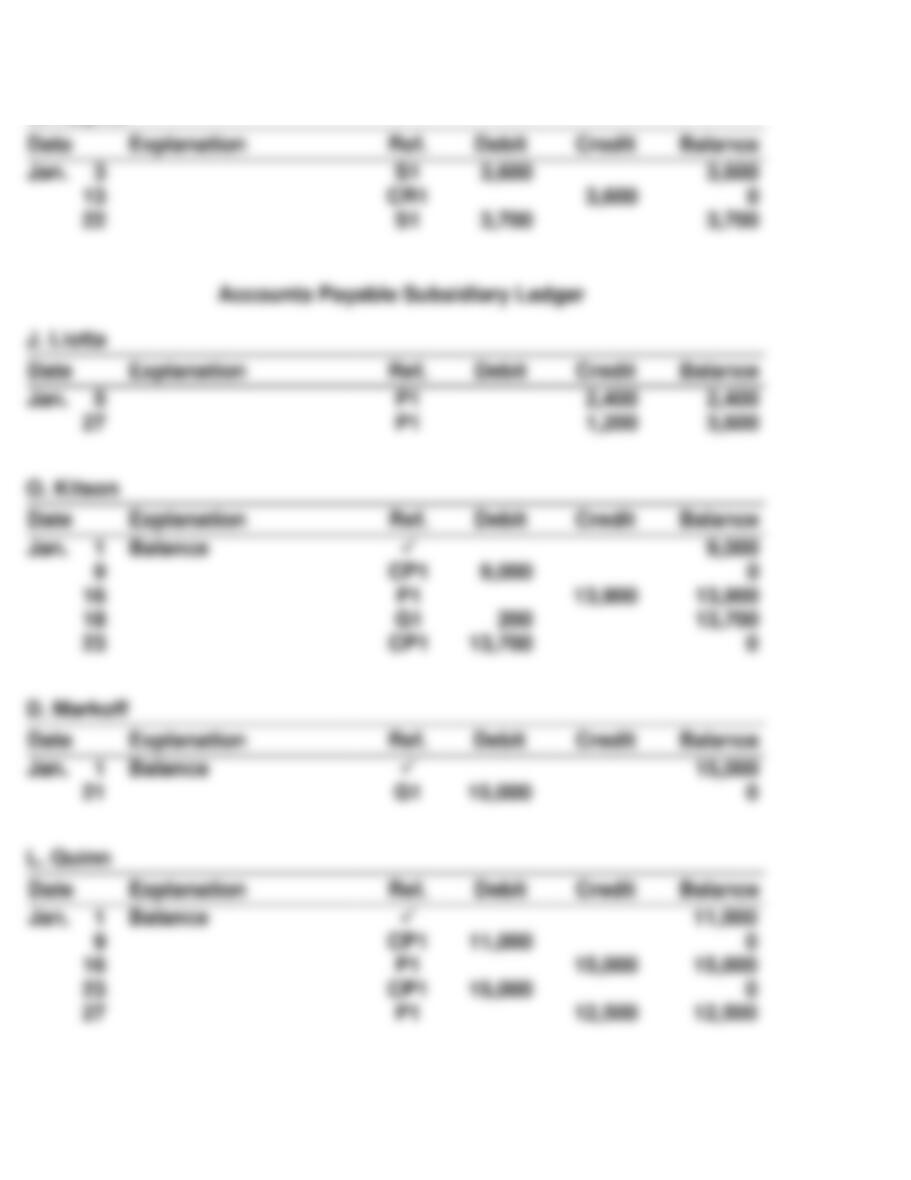

Accounts Payable Subsidiary Ledger

PROBLEM I-6A (Continued)

(d) BENSEN CO.

Trial Balance

January 31, 2017

PROBLEM I-6A (Continued)

COMPREHENSIVE PROBLEM: CHAPTERS 3 TO 6 AND APPENDIX I

Note: If the working papers that accompany this text are not used in

solving this problem, account numbers may differ from those presented in

this solution.

(a)

Sales Journal S1

Date

Account Debited

Invoice No.

Ref.

Accounts Receivable Dr.

Sales Cr.

Purchases Journal P1

Purchases Dr.

COMPREHENSIVE PROBLEM (Continued)

Cash Receipts Journal CR1

Date

Account

Credited

Ref.

Cash

Dr.

Accounts

Receivable

Cr.

Sales

Cr.

Other

Accounts

Cr.

Cash Payments Journal CP1

Date

Account Debited

Ref.

Other

Accounts

Dr.

Accounts

Payable

Dr.

Supplies

Dr.

Cash

Cr.

9,230

(X)

7,400

COMPREHENSIVE PROBLEM (Continued)

(a) & (e)

General Journal G1

Date

Account Titles and Explanations

Ref.

Debit

Credit

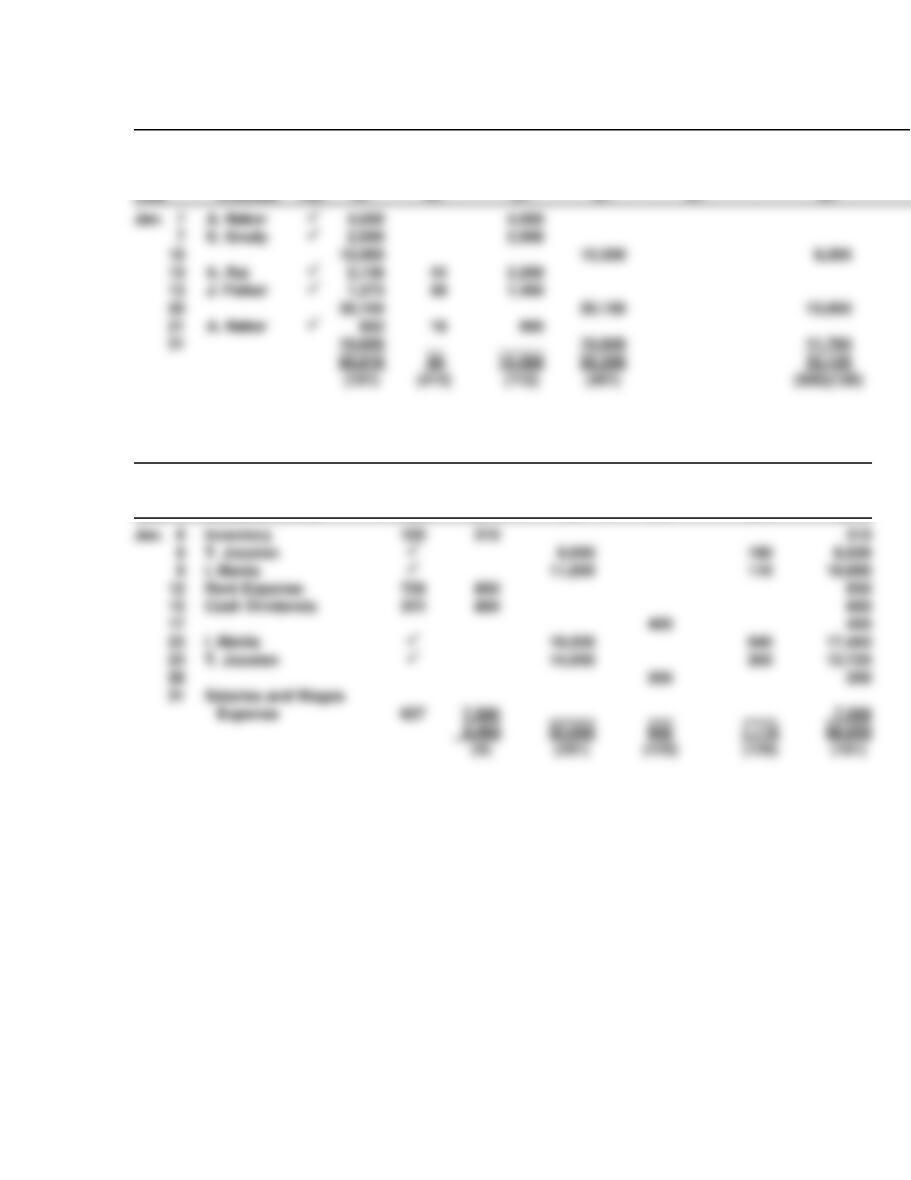

M. Fischer ……………………….

112/

Allowances ……………………..

512

Notes Payable …………………….

200

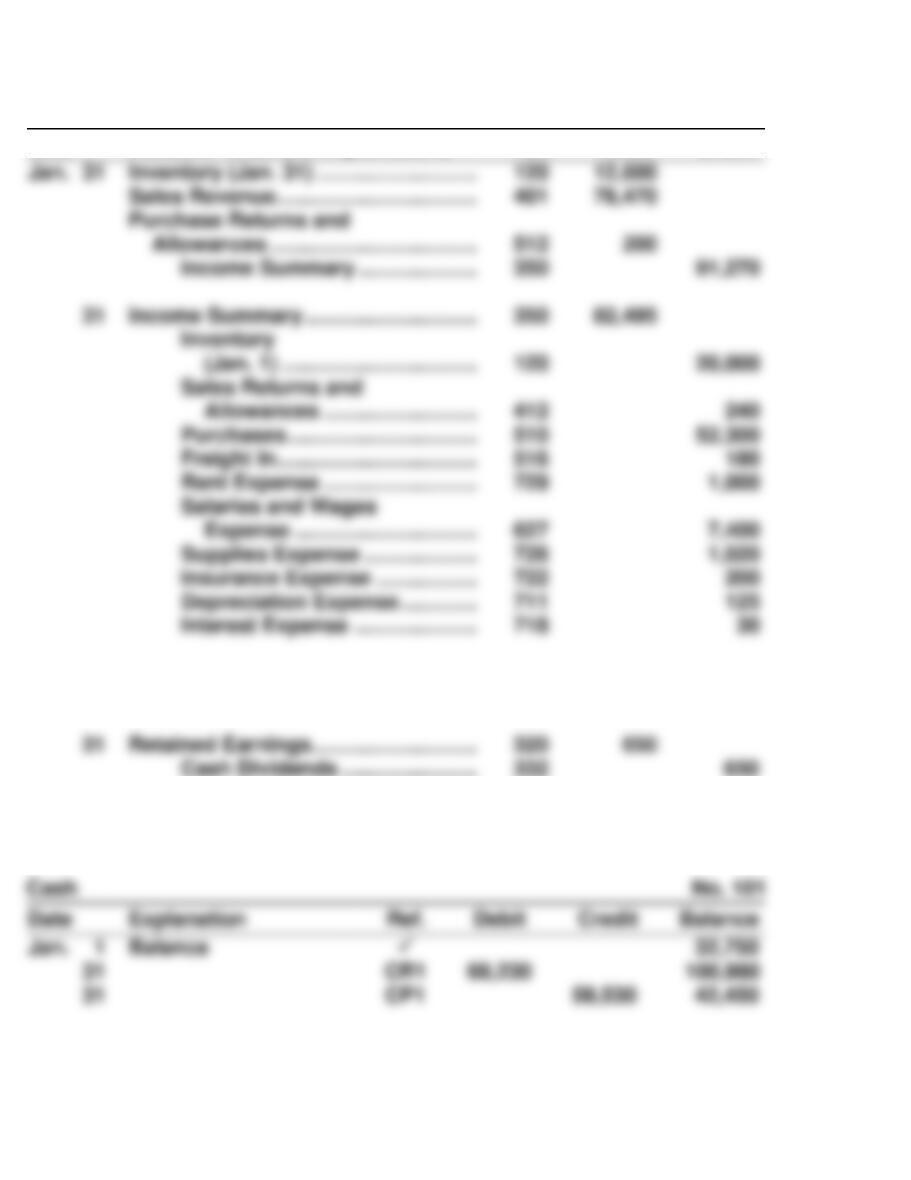

Adjusting Entries

31

Supplies Expense ……………………….

Supplies ……………………………..

728

125

1,020

1,020

31

Insurance Expense

(1/12 X $1,500) …………………………

Accumulated Depreciation—

Equipment ………………………

711

Interest Expense …………………………

Interest Payable ………………….

718

COMPREHENSIVE PROBLEM (Continued)

General Journal G1

Date

Account Titles and Explanations

Ref.

Debit

Credit

31

Income Summary ………………………..

Retained Earnings ……………….

350

320

8,775

8,775

31

Retained Earnings ……………………….

Cash Dividends …………………..

320

332

Date

Explanation

Ref.

(b) & (e) General Ledger

Allowances ……………………………..

Income Summary ………………..

512

350

91,270

Interest Expense …………………

718

COMPREHENSIVE PROBLEM (Continued)

Accounts Receivable No. 112

COMPREHENSIVE PROBLEM (Continued)

Accumulated Depreciation—Equipment No. 158

Interest Payable No. 230

COMPREHENSIVE PROBLEM (Continued)

Income Summary No. 350

Sales Returns and Allowances No. 412

Date

Explanation

Credit

Balance

Purchase Returns and Allowances No. 512

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Debit

Credit

Date

Explanation

Debit

Credit

COMPREHENSIVE PROBLEM (Continued)

COMPREHENSIVE PROBLEM (Continued)

Rent Expense No. 729

COMPREHENSIVE PROBLEM (Continued)

W. Rayms

COMPREHENSIVE PROBLEM (Continued)

COMPREHENSIVE PROBLEM (Continued)

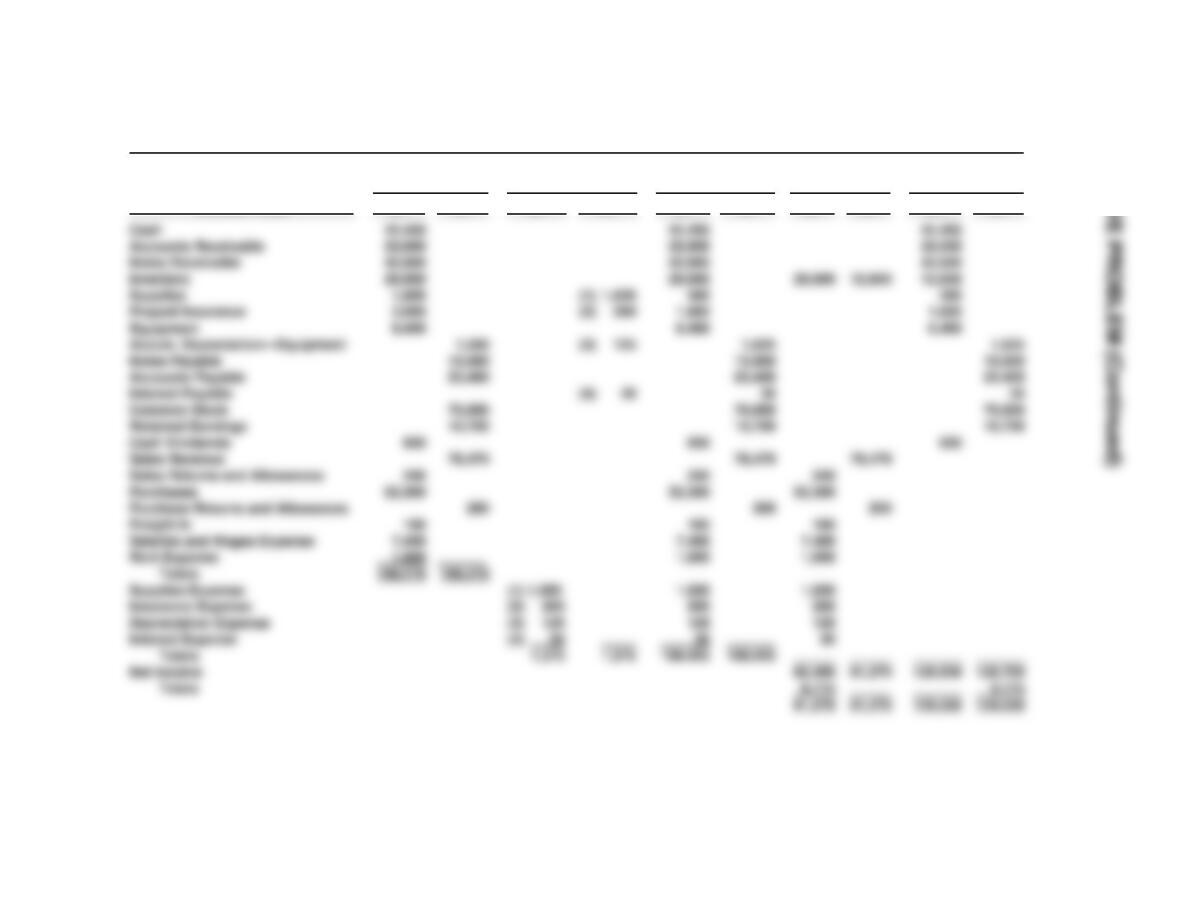

(c) ZWEIFEL COMPANY

Worksheet

For the Month Ended January 31, 2017

Trial Balance

Adjustments

Adjusted

Trial Balance

Income

Statement

Balance Sheet

Account Titles

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

COMPREHENSIVE PROBLEM (Continued)

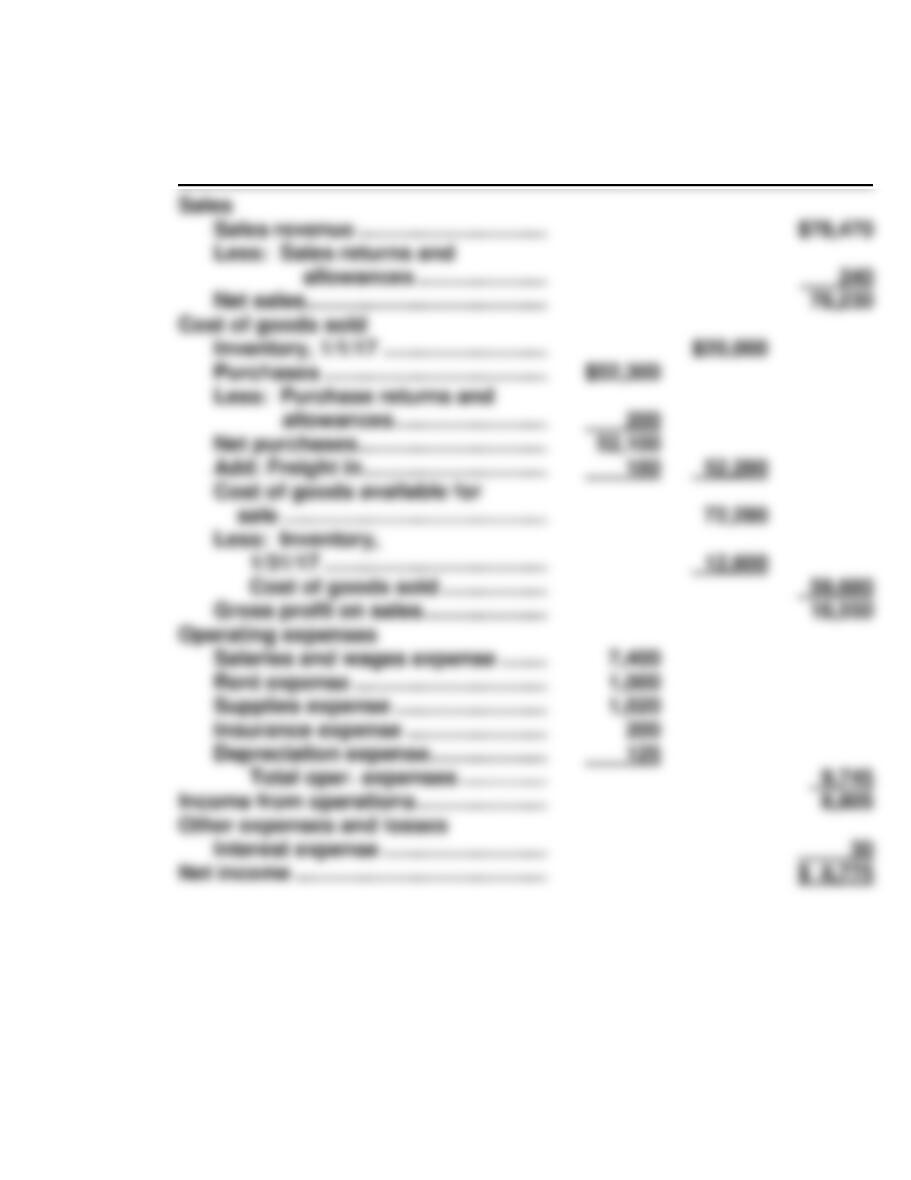

(d) ZWEIFEL CO.

Income Statement

For the Month Ended January 31, 2017

COMPREHENSIVE PROBLEM (Continued)

ZWEIFEL CO.

Statement Retained Earnings

For the Month Ended January 31, 2017

ZWEIFEL CO.

Balance Sheet

January 31, 2017

COMPREHENSIVE PROBLEM (Continued)

(f) ZWEIFEL CO.

Post-Closing Trial Balance

January 31, 2017

BYP I-1 FINANCIAL REPORTING PROBLEM—A MINI PRACTICE SET

(a)

Sales Journal S1

Date

Account

Debited

Invoice

No.

Ref.

Accounts Receivable Dr.

Sales Revenue Cr.

Cost of Goods Sold Dr.

Inventory Cr.

Purchases Journal P1

Date

Account Credited

Terms

Ref.

Inventory Dr.

Accounts Payable Cr.

BYP I-1 (Continued)

Cash Receipts Journal CR1

Date

Account

Credited

Ref.

Cash

Dr.

Sales

Discounts

Dr.

Accounts

Receivable

Cr.

Sales

Revenue

Cr.

Other

Accounts

Cr.

Cost of Goods Sold

Dr.

Inventory

Cr.

Cash Payments Journal CP1

Date

Account Debited

Ref.

Other

Accounts

Dr.

Accounts

Payable

Dr.

Supplies

Dr.

Inventory

Cr.

Cash

Cr.

Expense

(X)

52,000

(112)

BYP I-1 (Continued)

(a) & (e)

General Journal G1

Date

Account Titles and Explanations

Ref.

Debit

Credit

BYP I-1 (Continued)

General Journal G1

Date

Account Titles and Explanations

Ref.

Debit

Credit

Date

Credit

Date

Explanation

Credit

BYP I-1 (Continued)

Notes Receivable No. 115

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Credit

Explanation

Debit

Credit

Explanation

Debit

Credit

BYP I-1 (Continued)

Accumulated Depreciation—Equipment No. 158

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

BYP I-1 (Continued)

Income Summary No. 350

Sales Discounts No. 414

BYP I-1 (Continued)

Salaries and Wages Expense No. 627

Interest Expense No. 718

BYP I-1 (Continued)

Rent Expense No. 729

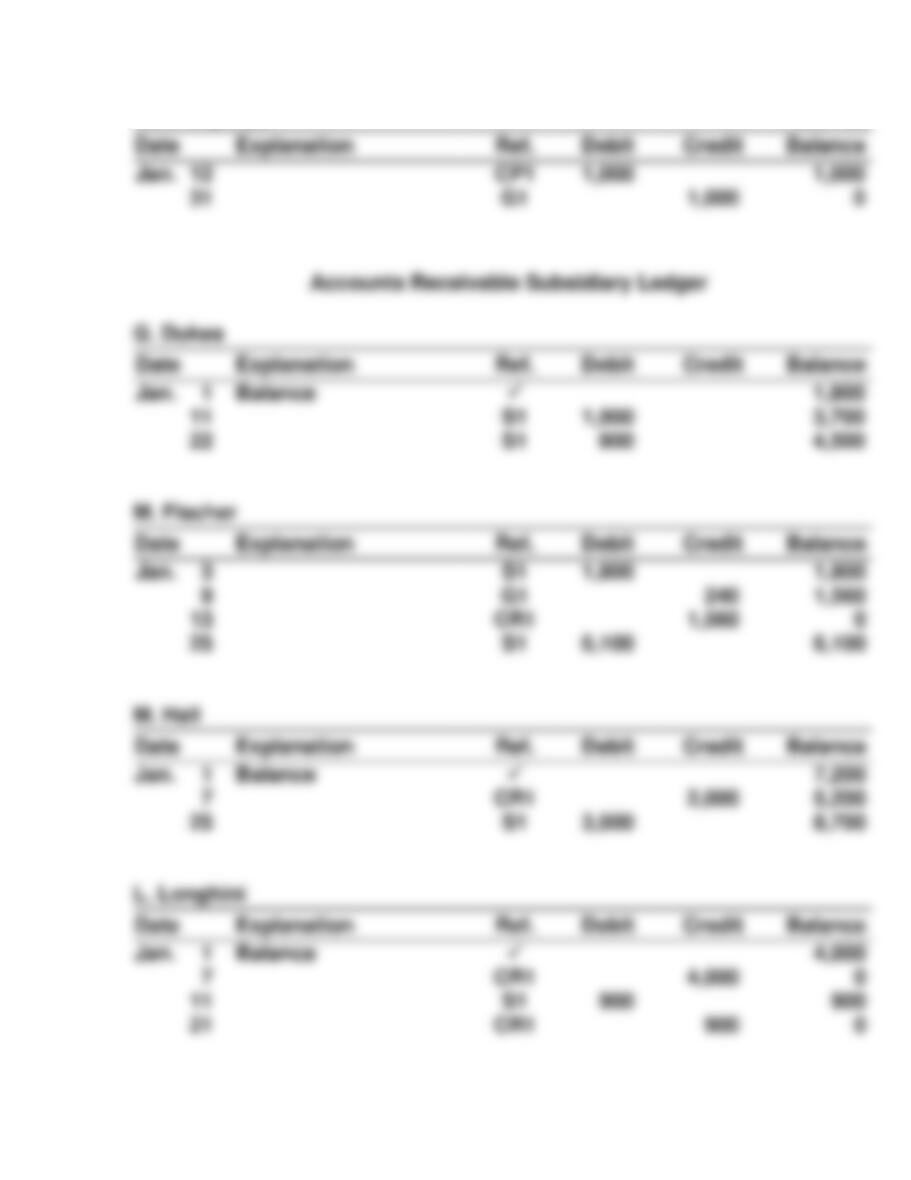

Accounts Receivable Subsidiary Ledger

C. Dunlap

BYP I-1 (Continued)

A. Mangrich

BYP I-1 (Continued)

D. Vang

BYP I-1 (Continued)

(c) BRYANT COMPANY

Worksheet

For the Month Ended January 31, 2017

Trial Balance

Adjustments

Adjusted

Trial Balance

Income

Statement

Balance Sheet

Account Titles

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Net Income

Totals

BYP I-1 (Continued)

(d) BRYANT CO.

Income Statement

For the Month Ended January 31, 2017

BYP I-1 (Continued)

BRYANT CO.

Retained Earnings Statement

For the Month Ended January 31, 2017

BRYANT CO.

Balance Sheet

January 31, 2017

BYP I-1 (Continued)

(f) BRYANT CO.

Post-Closing Trial Balance

January 31, 2017

BYP I-2 REAL-WORLD FOCUS

Some of the key features of the general ledger module highlighted by

the company are:

Some of the key features of the payables management module highlighted

by the company are:

BYP I-3 DECISION–MAKING ACROSS THE ORGANIZATION

(a) The special journals for Garin & Clark should be: (1) sales journal, (2)

purchases journal, (3) cash receipts journal, and (4) cash payments

journal.

3. Cash Receipts Journal columns:

BYP I-3 (Continued)

4. Cash Payments Journal columns:

(b) Garin & Clark should have:

1. An accounts receivable control account with individual customers’

accounts in a customers’ subsidiary ledger.

BYP I-4 COMMUNICATION ACTIVITY

Mr. Peter Gogan

2 Main Street

Central City, Michigan 48172

Dear Mr. Gogan:

Thank you for hiring two additional bookkeepers a month ago to help me with

BYP I-5 ETHICS CASE

(a) The stakeholders in this case are:

(b) Orlando instructions to assign the Bayport code to all uncoded and