SOLUTION

Requirements 1, 2 and 3

Sales Journal

Page 1

Date

Invoice

No.

Customer

Account Debited

Post.

Ref.

Accounts Receivable

DR

Cost of Goods Sold

DR

Sales Revenue

CR

Merchandise Inventory

CR

PC–27B, cont.

Requirements 1, 2 and 3, cont.

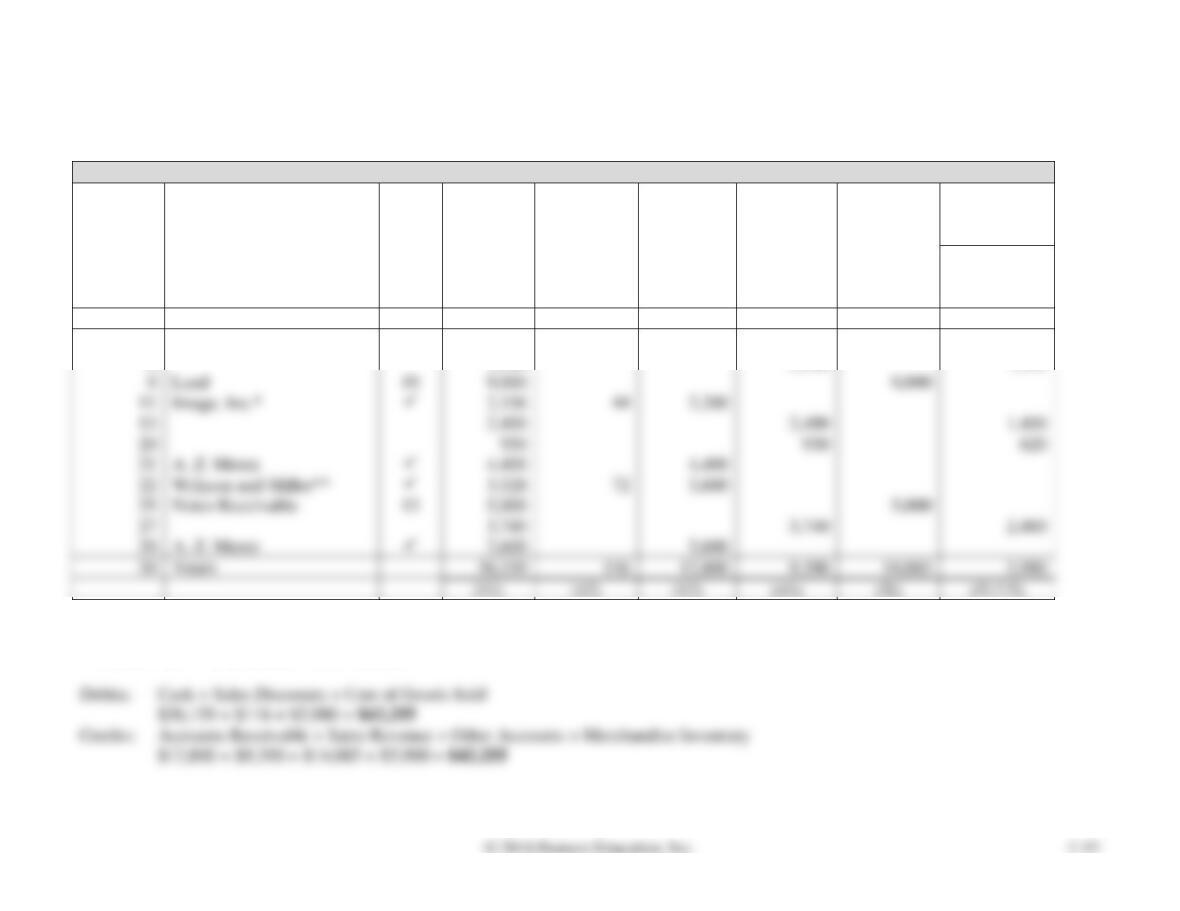

Cash Receipts Journal

Page 1

Date

Account Credited

Post.

Ref.

Cash

DR

Sales

Discounts

DR

Accounts

Receivable

CR

Sales

Revenue

CR

Other

Accounts

CR

Cost of

Goods Sold

DR

Merchandise

Inventory

CR

2016

Nov. 6

Equipment

18

85

85

6

2,300

2,300

1,500

9

Land

19

9,000

11

Image, Inc.*

2,156

13

2,400

2,400

1,400

20

4,400

Wilkson and Miller**

3,528

Notes Receivable

13

5,000

3,740

3,740

2,460

2,600

Totals

36,159

9,390

14,085

5,980

(11)

(41)

(51/15)

*$2,200 × 2% = $44; $2,200 – $44 = $2,156

**$3,600 × 2% = $72; $3,600 – $72 = $3,528

Debits:

Cash + Sales Discounts + Cost of Goods Sold

Credits:

Accounts Receivable + Sales Revenue + Other Accounts + Merchandise Inventory

PC–27B, cont.

Requirements 1, 2 and 3, cont.

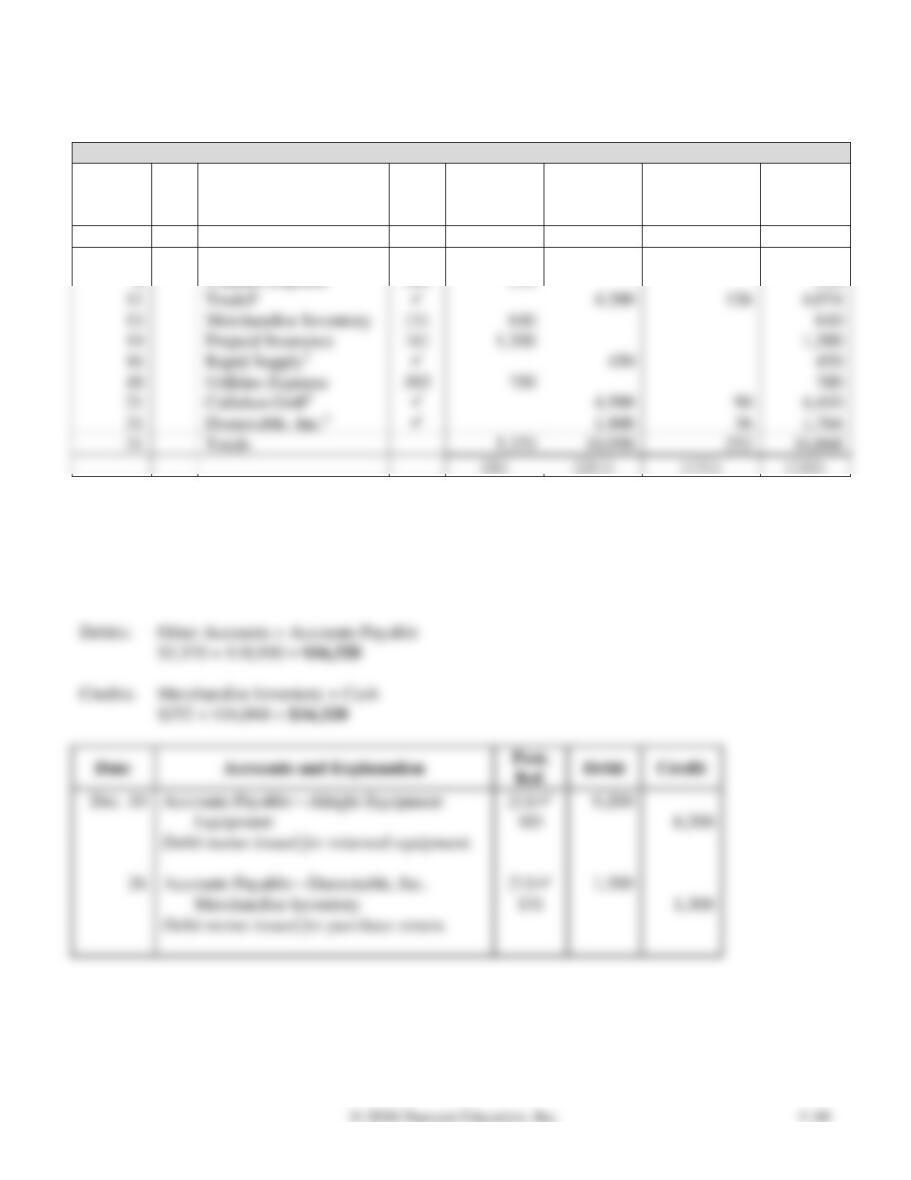

Date

Accounts and Explanation

Post.

Ref.

Debit

Credit

Jul. 18

Sales Returns and Allowances

43

500

Accounts Receivable—A. Z. Metz

12/✓

500

Merchandise Inventory

15

100

Cost of Goods Sold

51

100

Sales Returns and Allowances

43

Accounts Receivable—Oliver Co.

12/✓

Merchandise Inventory

15

Cost of Goods Sold

51

PC-28B Using the purchases, cash payments, and general journals

Learning Objectives 3, 4

Purchases Journal, Accounts Payable CR column total $18,750

The general ledger of Circus Lake Golf Shop includes the following selected accounts, along with their

account numbers:

Transactions in December that affected purchases and cash payments were as follows:

Requirements

1. Use the appropriate journal to record the preceding transactions in a purchases journal, a cash

payments journal (omit the Check No. column), and a general journal. Circus Lake Golf Shop

records purchase returns in the general journal. The company uses the perpetual inventory system.

2. Total each column of the special journals. Show that total debits equal total credits in each special

journal.

3. Show how postings would be made from the journals by writing the account numbers and check

marks in the appropriate places in the journals.

SOLUTION

Requirements 1, 2 and 3

Purchases Journal

Page 1

Date

Vendor

Account Credited

Terms

Post.

Ref.

Accounts

Payable

CR

Merchandise

Inventory

DR

Office

Supplies

DR

Other Accounts DR

Account

Title

Post.

Ref.

Amount

2016

Dec. 2

Trudel

3/10, n/30

✓

4,200

4,200

Rapid Supply

3/10, n/30

Alright Equipment

n/30

Equipment

Callahan Gold

2/10, n/30

Dunnstable, Inc.

2/10, n/45

Office Space, Inc.

n/30

Totals

Debits:

Merchandise Inventory + Office Supplies + Other Accounts

Credits:

Accounts Payable

PC–28B, cont.

Requirements 1, 2 and 3, cont.

Cash Payments Journal

Page 1

Date

Ck.

No.

Account Debited

Post.

Ref.

Other

Accounts

DR

Accounts

Payable

DR

Merchandise

Inventory

CR

Cash

CR

2016

Dec. 3

Rent Expense

564

2,200

2,200

8

Utilities Expense

583

530

530

4,200

4,074

Merchandise Inventory

131

640

640

Prepaid Insurance

161

1,300

1,300

450

450

583

700

700

4,500

4,410

1,800

1,764

Totals

5,370

10,950

1$4,200 × 3% = $126; $4,200 – $126 = $4,074

2Did not make payment within the discount period

3$4,500 × 2% = $90; $4,500 – $90 = $4,410

4$3,100 – $1,300 = $1,800; $1,800 × 2% = $36; $1,800 – $36 = $1,764

Debits:

Other Accounts + Accounts Payable

Credits:

Merchandise Inventory + Cash

Accounts Payable—Alright Equipment

6,200

26

Accounts Payable—Dunnstable, Inc.

1,300

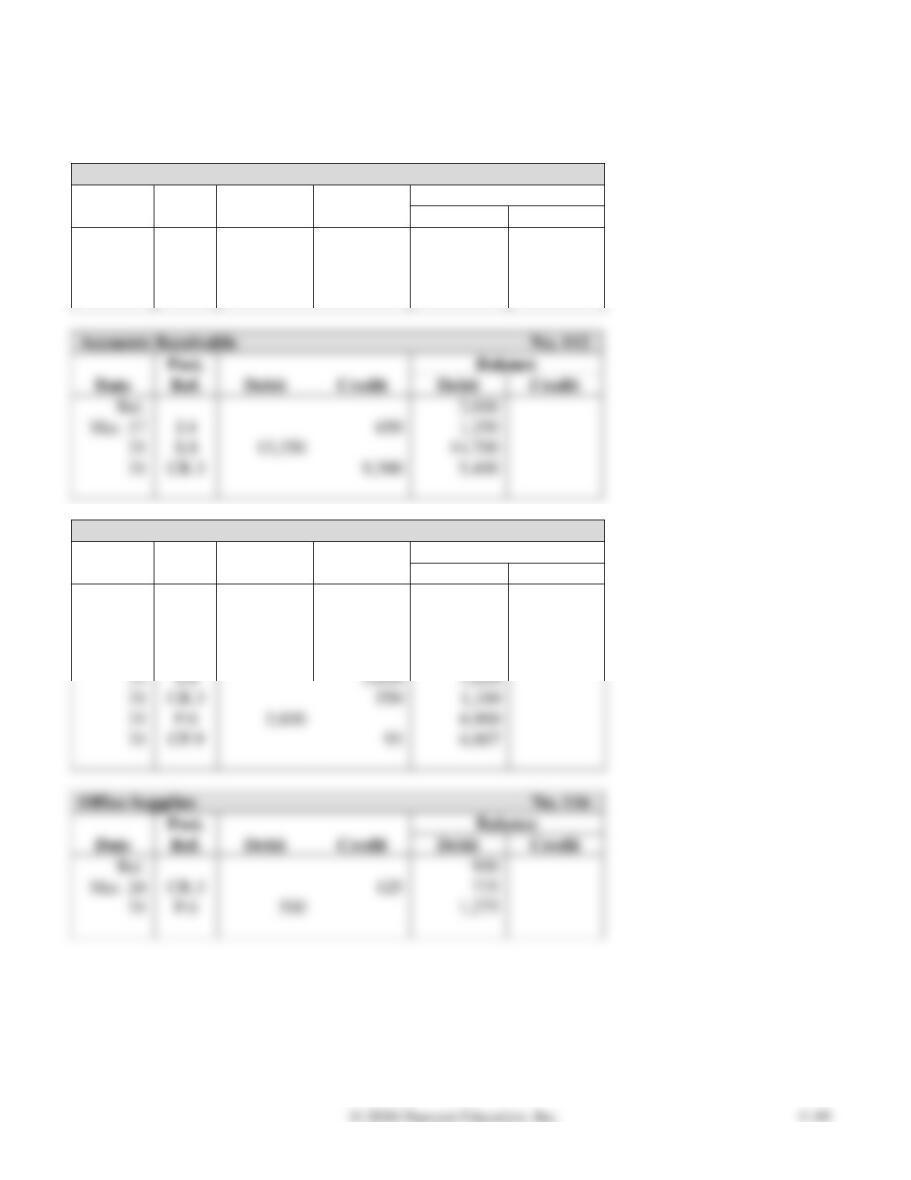

PC-29B Using all journals, posting, and balancing the ledgers

Learning Objectives 2, 3, 4

Trial balance, total debits $49,400

Kingston Computer Security uses the perpetual inventory system and makes all credit

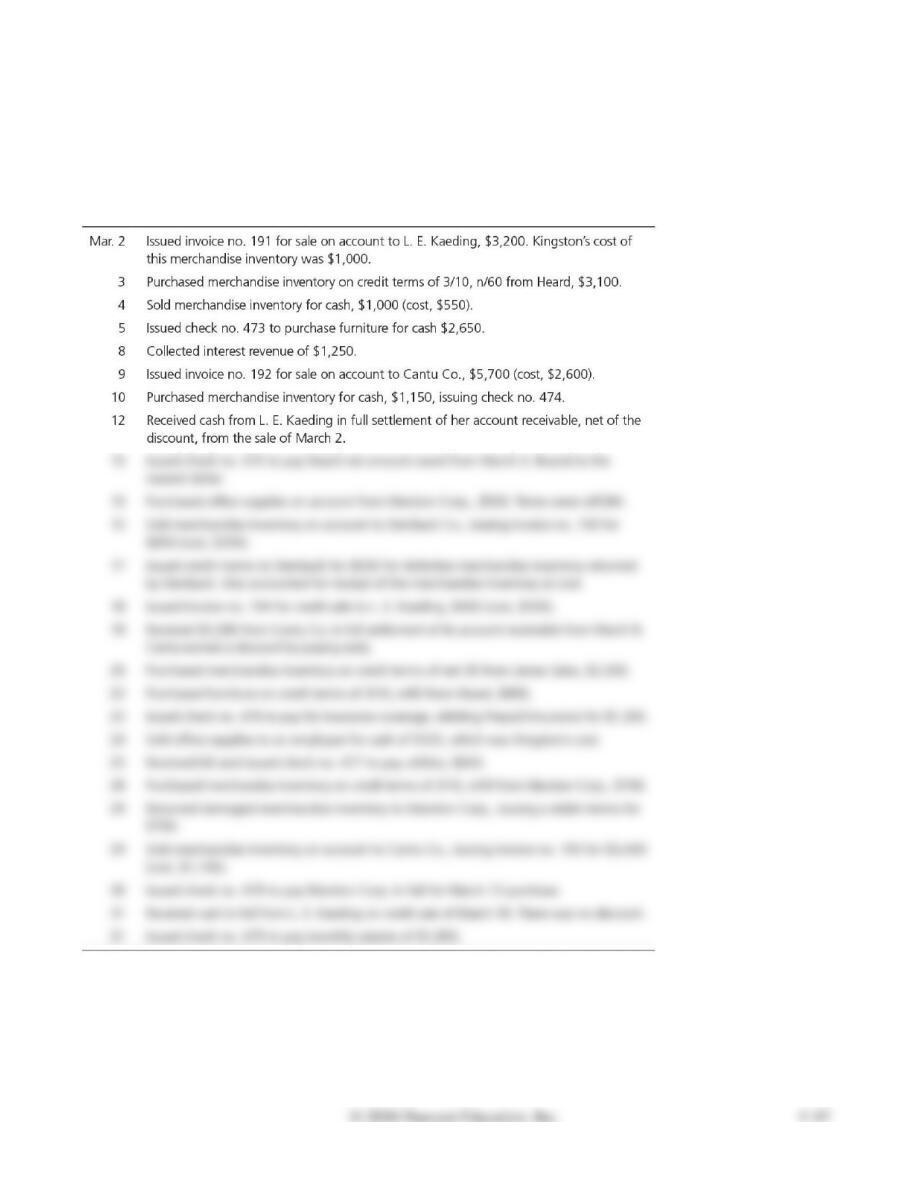

sales on terms of 2/10, n/30. During March, Kingston completed these transactions:

Requirements

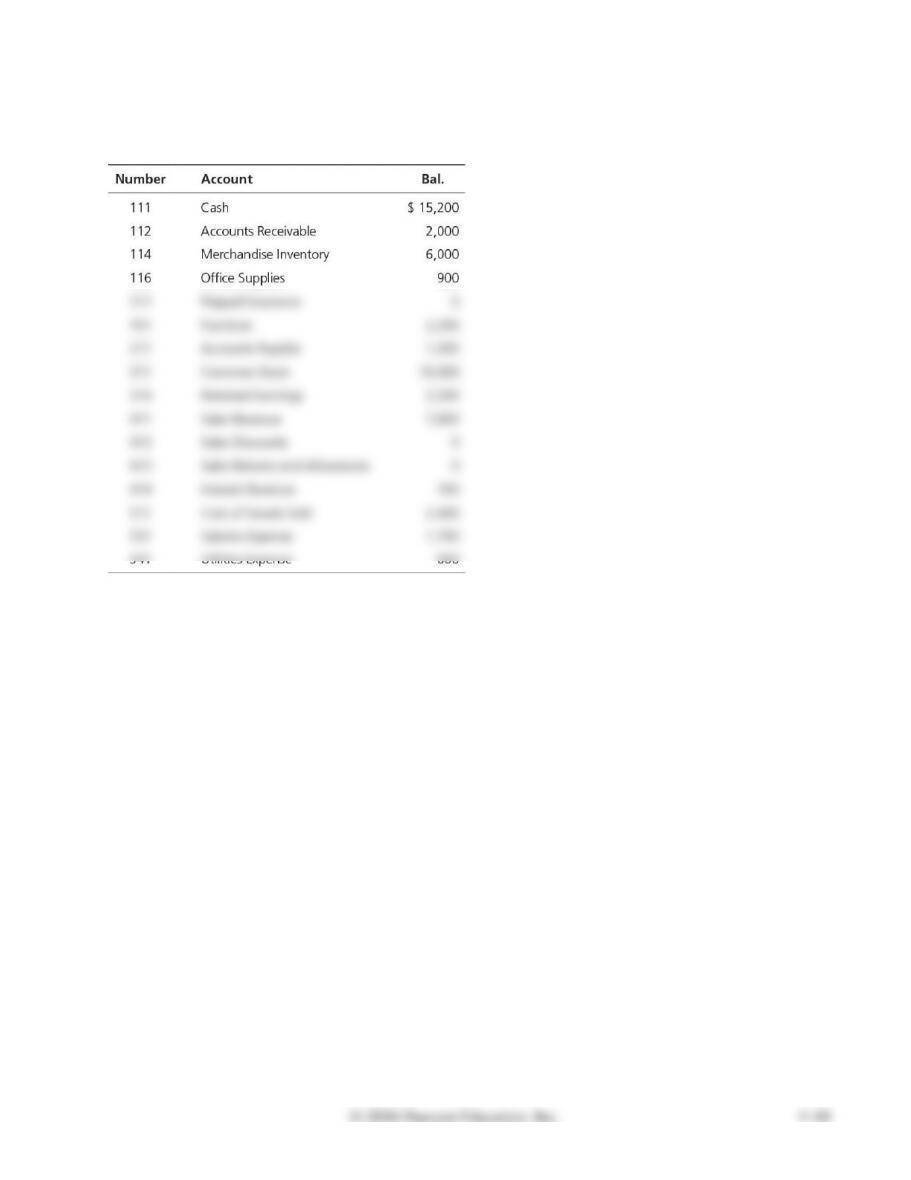

1. Open four-column general ledger accounts using Kingston Computer Security’s account numbers

and balances as of March 1, 2016, that follow. All accounts have normal balances.

2. Open four-column accounts in the subsidiary ledgers with beginning balances as of March 1, if any.

Accounts receivable subsidiary ledger: Abney Co., $2,000; Cantu Co., $0; J. R. Kaeding, $0; and

Stenback, $0. Accounts payable subsidiary ledger: Heard, $0; Marston Corp, $0; James Sales, $0;

and Yount Co., $1,000.

3. Enter the transactions in a sales journal (page 8), a cash receipts journal (page 3), a purchases journal

(page 6), a cash payments journal (page 9), and a general journal (page 4), as appropriate.

4. Post daily to the accounts receivable subsidiary ledger and to the accounts payable subsidiary ledger.

5. Total each column of the special journals. Show that total debits equal total credits in each special

journal. On March 31, post to the general ledger.

6. Prepare a trial balance as of March 31, 2016, to verify the equality of the general ledger. Balance the

total of the customer account balances in the accounts receivable subsidiary ledger against Accounts

Receivable in the general ledger. Do the same for the accounts payable subsidiary ledger and

Accounts Payable in the general ledger.

SOLUTION

Requirements 1 and 5

Cash

No. 111

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

15,200

Mar. 31

CR.3

11,497

26,697

31

CP.9

11,107

15,590

Accounts Receivable

No. 112

Date

Debit

Credit

Debit

Credit

Bal.

Mar. 17

J.4

650

31

13,350

14,700

31

CR.3

Merchandise Inventory

No. 114

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

6,000

Mar. 10

CP.9

1,150

7,150

17

J.4

250

7,400

29

J.4

700

6,700

31

1,650

31

CR.3

550

1,100

31

6,900

31

CP.9

6,807

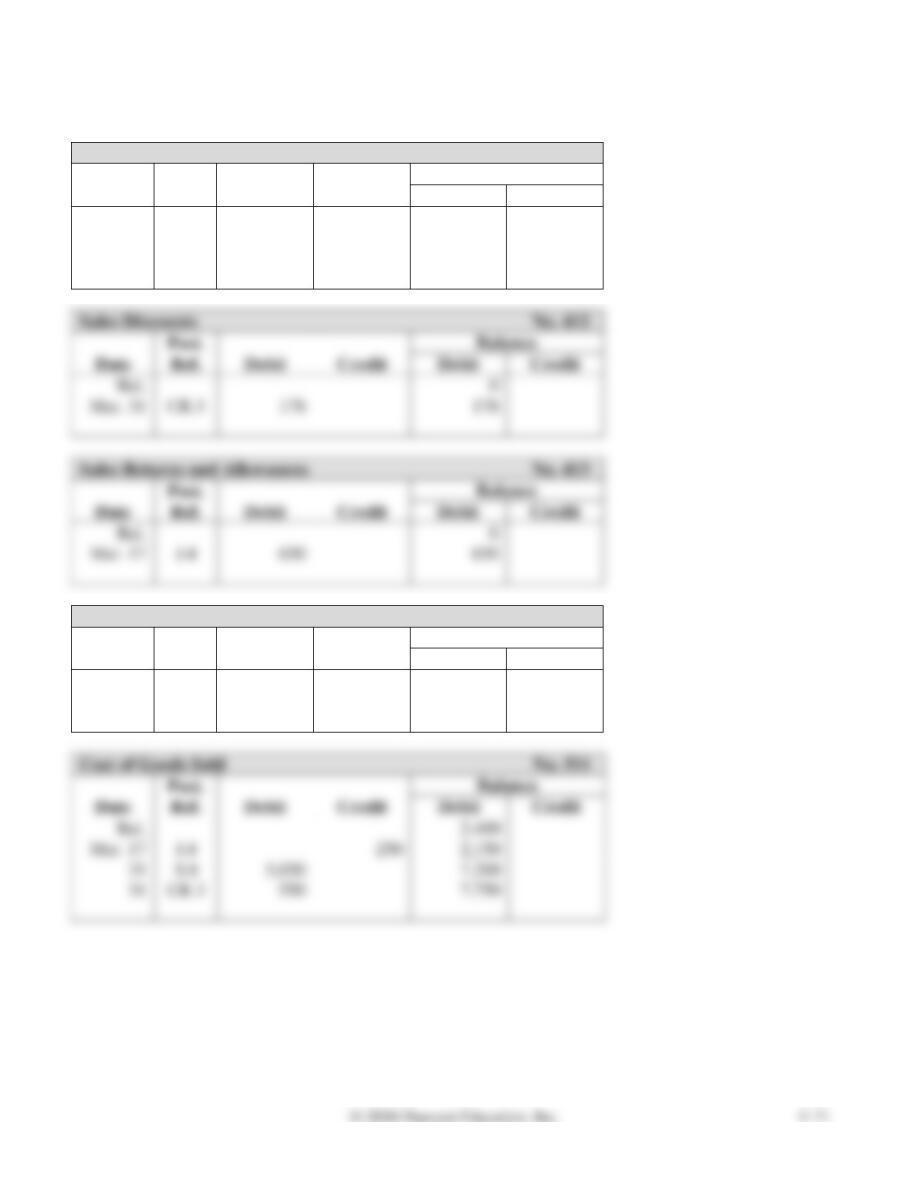

Office Supplies

No. 116

Date

Post.

Ref.

Debit

Credit

Debit

Credit

Mar. 24

CR.3

125

775

31

500

PC–29B, cont.

Requirements 1 and 5, cont.

Prepaid Insurance

No. 117

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

0

Mar. 22

CP.9

1,300

1,300

Furniture

No. 151

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

CP.9

2,650

4,850

5,650

Accounts Payable

No. 211

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

Mar. 29

7,100

CP.9

3,600

Common Stock

No. 311

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

Retained Earnings

No. 314

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

2,500

PC–29B, cont.

Requirements 1 and 5, cont.

Sales Revenue

No. 411

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

7,800

Mar. 31

S.8

13,350

21,150

31

CR.3

1,000

22,150

Sales Discounts

No. 412

Balance

Bal.

Mar. 31

CR.3

178

178

Sales Returns and Allowances

No. 413

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

Mar. 17

650

650

Interest Revenue

No. 419

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

700

Mar. 8

CR.3

1,250

1,950

Cost of Goods Sold

No. 511

Date

Debit

Credit

Credit

Bal.

Mar. 17

250

31

S.8

5,050

31

CR.3

550

PC–29B, cont.

Requirements 1 and 5, cont.

Salaries Expense

No. 531

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Utilities Expense

No. 541

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

PC-29B, cont.

Requirements 2 and 4

Accounts Receivable—Abney Co.

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Accounts Receivable—Cantu Co.

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Accounts Receivable—Stenback Co.

Date

Debit

Credit

Balance

Debit

Credit

PC-29B, cont.

Requirements 2 and 4

Accounts Receivable—L. E. Kaeding

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

0

Mar. 2

S.8

3,200

3,200

12

CR.3

3,200

0

18

S.8

400

400

31

CR.3

400

0

Accounts Payable—Heard

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

0

P.6

3,100

3,100

13

3,100

0

22

P.6

800

800

Accounts Payable—Marston Corp.

Balance

Bal.

0

P.6

500

500

28

P.6

700

1,200

29

700

500

30

500

0

Accounts Payable—James Sales

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

0

Mar. 20

P.6

2,000

2,000

Accounts Payable—Yount Co.

Date

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

Bal.

1,000

PC–29B, cont.

Requirements 3, 4, 5 and 6

Sales Journal

Page 8

Date

Invoice

No.

Customer

Account Debited

Post.

Ref.

Accounts Receivable

DR

Cost of Goods Sold

DR

Sales Revenue

CR

Merchandise Inventory

CR

2016

L. E. Kaeding

Cantu Co.

Stenback Co.

L. E. Kaeding

Cantu Co.

Totals

Debits:

Accounts Receivable + Cost of Goods Sold

Credits:

Sales Revenue + Merchandise Inventory

PC–29B, cont.

Requirements 3, 4, 5 and 6, cont.

Cash Receipts Journal

Page 3

Date

Account Credited

Post.

Ref.

Cash

DR

Sales

Discounts

DR

Accounts

Receivable

CR

Sales

Revenue

CR

Other

Accounts

CR

Cost of

Goods Sold

DR

Merchandise

Inventory

CR

2016

Mar. 4

1,000

1,000

550

Interest Revenue

1,250

3,136

5,586

Office Supplies

L. E. Kaeding

Totals

1,000

550

(411)

Debits:

Cash + Sales Discounts + Cost of Goods Sold

Credits:

Accounts Receivable + Sales Revenue + Other Accounts + Merchandise Inventory

PC–29B, cont.

Requirements 3, 4, 5 and 6, cont.

Purchases Journal

Page 6

Date

Vendor

Account Credited

Terms

Post.

Ref.

Accounts

Payable

CR

Merchandise

Inventory

DR

Office

Supplies

DR

Other Accounts DR

Account

Title

Post.

Ref.

Amount

2016

Mar. 3

Heard

3/10, n/60

✓

3,100

3,100

James Sales

n/30

✓

2,000

2,000

Heard

3/10, n/60

✓

Furniture

Marston Corp.

2/10, n/30

✓

Totals

7,100

5,800

Debits:

Merchandise Inventory + Office Supplies + Other Accounts

Credits:

Accounts Payable

PC–29B, cont.

Requirements 3, 4, 5 and 6, cont.

Cash Payments Journal

Page 9

Date

Ck.

No.

Account Debited

Post.

Ref.

Other

Accounts

DR

Accounts

Payable

DR

Merchandise

Inventory

CR

Cash

CR

2016

Mar. 5

473

Furniture

151

2,650

2,650

10

474

Merchandise Inventory

114

1,150

1,150

13

475

3,100

3,007

22

476

Prepaid Insurance

117

1,300

1,300

25

477

Utilities Expense

541

30

478

Marston Corp.

31

479

Salaries Expense

531

1,850

1,850

31

Totals

7,600

3,600

Debits:

Other Accounts + Accounts Payable

Credits:

Merchandise Inventory + Cash

PC–29B, cont.

Requirements 3, 4, 5 and 6, cont.

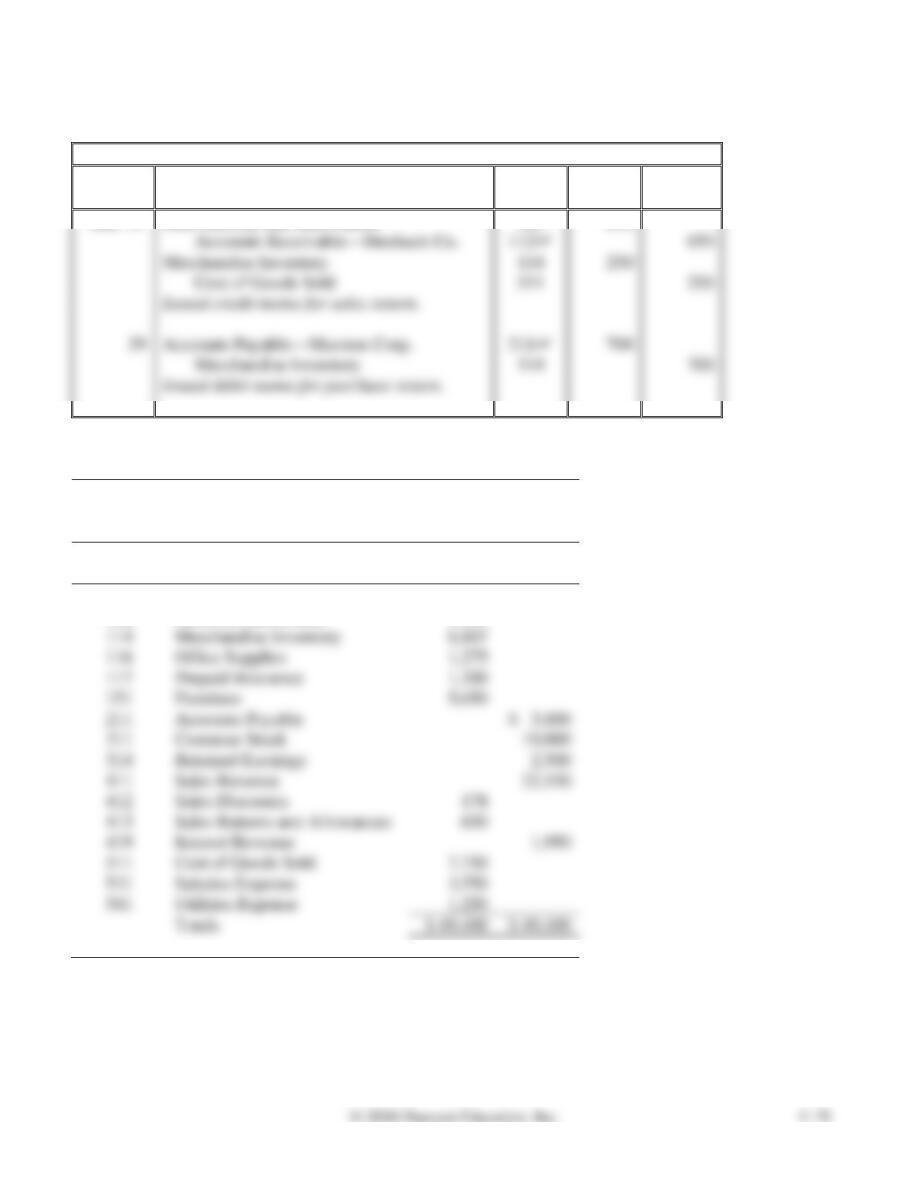

General Journal Page 4

Date

Accounts and Explanation

Post.

Ref.

Debit

Credit

Mar. 17

Sales Returns and Allowances

413

650

Merchandise Inventory

114

250

511

Issued credit memo for sales return.

Accounts Payable—Marston Corp.

700

Issued debit memo for purchase return.

Requirement 6

KINGSTON COMPUTER SECURITY

Trial Balance

March 31, 2016

Acct. No.

Account Name

Debit

Credit

111

Cash

$ 15,590

112

Accounts Receivable

5,400

114

Merchandise Inventory

116

Office Supplies

117

Prepaid Insurance

151

Furniture

211

Accounts Payable

311

Common Stock

314

Retained Earnings

411

Sales Revenue

412

Sales Discounts

413

Sales Returns and Allowances

419

Interest Revenue

511

Cost of Goods Sold

531

Salaries Expense

541

Utilities Expense

Totals

$ 49,400

PC–29B, cont.

Requirement 6, cont.

Accounts Receivable Subsidiary Ledger

Customer

Balance

Abney Co.

$ 2,000

Cantu Co.

3,400

Stenback Co.

0

L. E. Kaeding

0

Total

$ 5,400

Balance

Heard

Marston Corp.

0

James Sales

2,000

Yount Co.

1,000

Total

$ 3,800

Continuing Problem

PC-30 Using all journals

This problem continues the Daniels Consulting situation. Daniels Consulting per- forms systems

consulting. Daniels has also begun selling accounting software and uses the perpetual inventory system

to account for software inventory. During January 2017, Daniels completed the following transactions:

Daniels Consulting had the following selected accounts with account numbers and normal balances: