Process Costing in Sequential Production Departments: Weighted-Average Method

Solutions Manual

to accompany

Process Costing in Sequential

Production Departments:

Weighted-Average Method

to accompany

MANAGERIAL

ACCOUNTING

Tenth Edition

Process Costing in Sequential Production Departments: Weighted-Average Method

Preface

The best way for most students to learn managerial accounting is to read the text and then

solve a representative sample of the review questions, exercises, problems and cases. The

topic of each exercise, problem, and case is indicated in the text. The estimated amount of

Process Costing in Sequential Production Departments: Weighted-Average Method

Supp 4-1

ANSWERS TO REVIEW QUESTIONS

Process Costing in Sequential Production Departments: Weighted-Average Method

Supp 4-2

SOLUTIONS TO EXERCISES

EXERCISE 3 (10 MINUTES)

1.

Work-in-Process Inventory: Pouring Department ……………

1,090,000

Raw-Material Inventory ………………………………………….

Wages Payable ……………………………………………………..

340,000

Manufacturing Overhead ……………………………………….

680,000

2.

Work-in-Process Inventory: Finishing Department ………….

900,000

Work-in-Process Inventory: Pouring Department ……

3.

Work-in-Process Inventory: Finishing Department ………….

725,000

Raw-Material Inventory ………………………………………..

Wages Payable …………………………………………………….

280,000

Manufacturing Overhead ………………………………………

420,000

4.

Finished-Goods Inventory ……………………………………………..

400,000

Work-in-Process Inventory: Finishing Department …

400,000

EXERCISE 4 (10 MINUTES)

1.

Work-in-Process Inventory: Preparation Department ………

1,635,000

Raw-Material Inventory ………………………………………….

105,000

Wages Payable ……………………………………………………..

510,000

Manufacturing Overhead ……………………………………….

1,020,000

2.

Work-in-Process Inventory: Finishing Department ………….

1,350,000

Work-in-Process Inventory: Preparation Department

1,350,000

3.

Work-in-Process Inventory: Finishing Department ………….

1,087,500

Raw-Material Inventory ………………………………………..

Wages Payable …………………………………………………….

420,000

Manufacturing Overhead ………………………………………

630,000

4.

Finished-Goods Inventory ……………………………………………..

600,000

Work-in-Process Inventory: Finishing Department …

600,000

Process Costing in Sequential Production Departments: Weighted-Average Method

Supp 4-3

SOLUTIONS TO PROBLEMS

PROBLEM 5 (30 MINUTES)

1.

a.

Cost of units completed and transferred to finished-goods inventory during

February:

Units completed and transferred out……………………………………….

5,950

Cost of units completed and transferred out …………………………...

b.

To compute the cost of the Finishing Department’s work-in–process inventory

on February 28, first determine the number of units in ending work-in–

process inventory, as follows:

Add: Units transferred in ………………………………………………………..

7,000

Units to account for ……………………………………………………………….

7,700

Less: Units transferred to finished goods ……………………………….

5,950

1,750

Then compute the transferred-in, direct-material, and conversion costs in the

February 28 work-in-process inventory:

Input

Equivalent

Units

Cost per

Equivalent

Unit

Cost

2.

Equivalent units of transferred-in costs ……………………………………………

7,700

Total transferred-in cost ………………………………………………………………….

Deduct: Transferred-in cost in February 1 work-in-process inventory .

Total cost transferred in from the Assembly Department ………………….

Journal entry to record transfer:

Work-in-Process Inventory: Assembly Department ……………

Supp 4-4

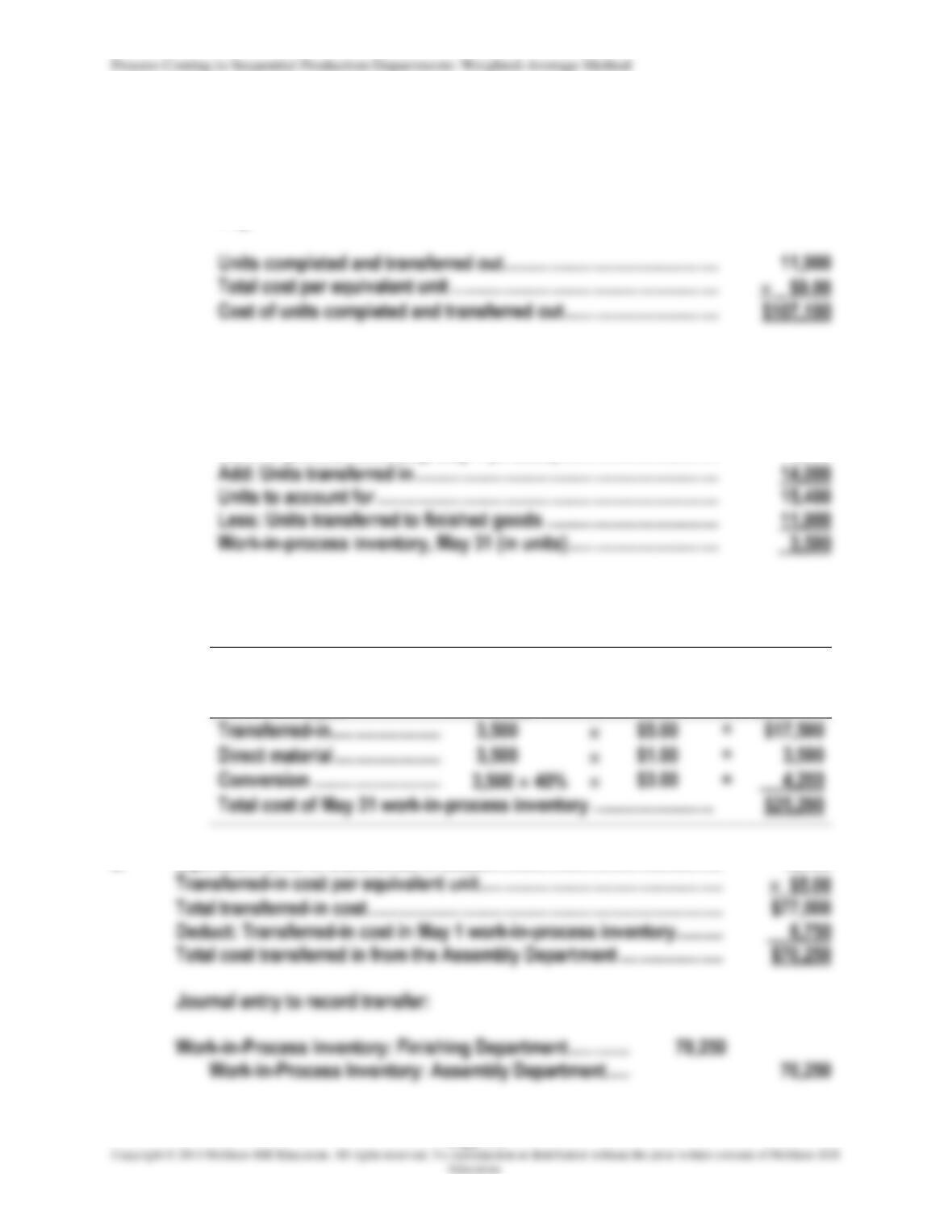

PROBLEM 6 (30 MINUTES)

1.

a.

Cost of units completed and transferred to finished-goods inventory during

May:

Units completed and transferred out……………………………………….

11,900

Cost of units completed and transferred out …………………………...

b.

To compute the cost of the Finishing Department’s work-in–process inventory

on May 31, first determine the number of units in ending work-in-process

inventory, as follows:

Work-in-process inventory, May 1 (in units) …………………………….

1,400

Add: Units transferred in ………………………………………………………..

14,000

Units to account for ……………………………………………………………….

15,400

Less: Units transferred to finished goods ……………………………….

11,900

Work-in-process inventory, May 31 (in units) …………………………..

Then compute the transferred-in, direct-material, and conversion costs in the

May 31 work-in-process inventory:

Input

Equivalent

Units

Cost per

Equivalent

Unit

Cost

2.

Equivalent units of transferred-in costs ……………………………………………

15,400

Total transferred-in cost ………………………………………………………………….

Deduct: Transferred-in cost in May 1 work-in-process inventory ……….

Total cost transferred in from the Assembly Department ………………….

Journal entry to record transfer:

Work-in-Process Inventory: Finishing Department …………………..

70,250

Work-in-Process Inventory: Assembly Department ……………

70,250

Process Costing in Sequential Production Departments: Weighted-Average Method

Supp 4-5

SOLUTIONS TO CASES

CASE 7 (60 MINUTES)

PRODUCTION REPORT: HOME GARDEN COMPANY – GRADING DEPARTMENT

Weighted-Average Method

Physical

Units

(pounds)

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

Work in process, November 1 ………

-0-

—

Units started during November ……

Total units to account for …………….

Units completed and transferred

out during November ………………

36,000

Work in process, November 30 …….

—

Total units accounted for …………….

Direct

Material

Conversion

Total

Work in process, November 1 ………………………

-0-

-0-

-0-

Costs incurred during November …………………

$352,080

Total costs to account for …………………………...

$352,080

Equivalent units ………………………………………….

Costs per equivalent unit …………………………….

$2.40

$9.78

Cost of goods completed and transferred out of the Grading Department

during November:

Cost remaining in November 30 work-in-process inventory in the

Grading Department ………………………………………………………………………….

-0-

Check: Cost of goods completed and transferred out ………….

Process Costing in Sequential Production Departments: Weighted-Average Method

Supp 4-6

Total costs accounted for ……………………………………….

CASE 7 (CONTINUED)

PRODUCTION REPORT: HOME GARDEN COMPANY – FINISHING DEPARTMENT

Weighted-Average Method

Physical

Units

(pounds)

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Transferred

in

Conversion

Work in process, November 1 ………

1,600

50%

Units transferred in during November

36,000

Total units to account for …………….

37,600

Units completed and transferred

out during November ………………

35,600

100%

35,600

35,600

Work in process, November 30 …….

50%

Total units accounted for …………….

37,600

Transferred

In

Conversion

Total

Work in process, November 1 ………………………

$ 13,850

$ 3,750

$ 17,600

Costs incurred during November …………………

Total costs to account for …………………………...

Equivalent units ………………………………………….

Costs per equivalent unit …………………………….

$2.45

Supp 4-7

CASE 7 (CONTINUED)

Cost of goods completed and transferred out of the Finishing

Department during November:

Cost remaining in November 30 work-in-process inventory in the

Finishing Department:

Transferred-in costs:

in–dtransferre

of number

Direct material:

None

Conversion:

conversion

of number

Total cost of November 30 work in process …………………………………….

$21,914

Check: Cost of goods completed and transferred out ………….

$433,686

Cost of November 30 work-in–process inventory ……..

Total costs accounted for ……………………………………….

$455,600

†Rounded

Supp 4-8

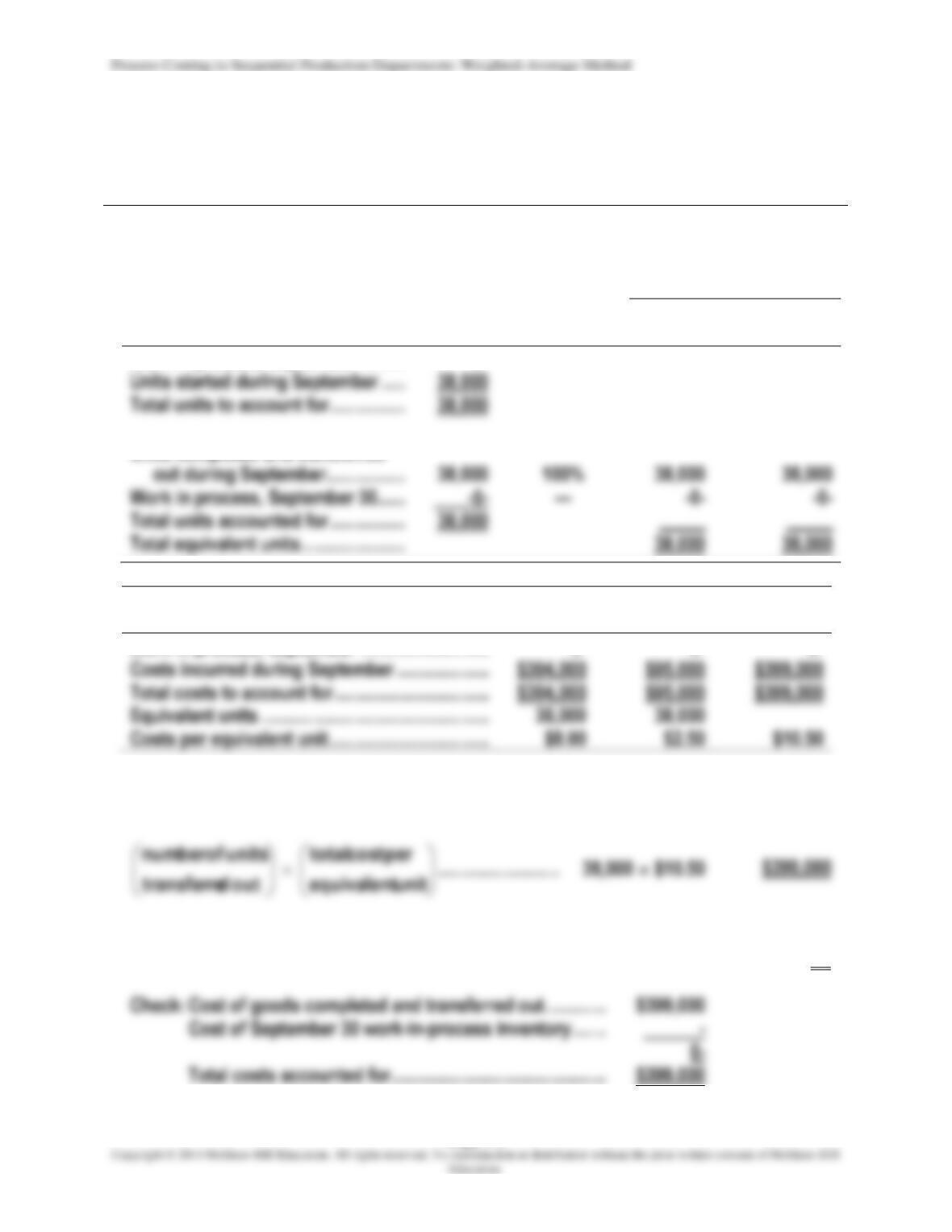

CASE 8 (60 MINUTES)

PRODUCTION REPORT: AGRITECH, INC. – MIXING DEPARTMENT

Weighted-Average Method

Physical

Units

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Direct

Material

Conversion

Work in process, September 1 ……..

-0-

—

Units started during September …..

Total units to account for …………….

out during September ……………..

38,000

Work in process, September 30 ……

—

Total units accounted for …………….

Units completed and transferred

Direct

Material

Conversion

Total

Work in process, September 1 ……………………..

-0-

-0-

-0-

Costs incurred during September ………………..

$399,000

Total costs to account for …………………………...

$399,000

Equivalent units ………………………………………….

Costs per equivalent unit …………………………….

$2.50

Cost of goods completed and transferred out of the Mixing Department

during September:

Cost remaining in September 30 work-in-process inventory in the

Mixing Department …………………………………………………………………………….

-0-

Check: Cost of goods completed and transferred out ………….

Cost of September 30 work-in–process inventory …….

0-

Supp 4-9

CASE 8 (CONTINUED)

PRODUCTION REPORT: AGRITECH, INC. – SATURATING DEPARTMENT

Weighted-Average Method

Physical

Units

Percentage

of

Completion

with

Respect to

Conversion

Equivalent Units

Transferred

in

Conversion

Work in process, September 1 ………………

2,000

40%

Units transferred in during September ….

Total units to account for ……………………..

out during September ………………………

Work in process, September 30 …………….

3,000

40%

Total units accounted for ……………………..

Units completed and transferred

Transferred

In

Conversion

Total

Work in process, September 1 ……………………..

$ 41,000

$ 24,600

$ 65,600

Costs incurred during September ………………..

90,000

Total costs to account for …………………………...

$114,600

$554,600

Equivalent units ………………………………………….

Costs per equivalent unit …………………………….

Supp 4-10

CASE 8 (CONTINUED)

Cost of goods completed and transferred out of the Saturating

Department during September:

Cost remaining in September 30 work-in-process inventory in the

Saturating Department:

Transferred-in costs:

Direct material:

None

Conversion:

Total cost of September 30 work in process ……………………………………

Check: Cost of goods completed and transferred out ………….

Cost of September 30 work-in–process inventory …….

Total costs accounted for ……………………………………….

conversion

of number